Global Micro Perforated Films For Packaging Market Size, Growth & Revenue 2024-2034

Global Micro Perforated Films For Packaging Market is segmented by Product Type (Polyethylene Micro Perforated Films, Polypropylene Micro Perforated Films, Polyester Micro Perforated Films, Polyamide Micro Perforated Films, Others), Application (Fresh Produce Packaging, Bakery Packaging, Meat & Seafood Packaging, Dairy Packaging, Snack Foods Packaging), End-Use Industry (Food & Beverages, Pharmaceuticals, Agriculture, Consumer Goods), Distribution Channel (Direct Sales, Distributors & Wholesalers, Online Channels), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global Micro Perforated Films For Packaging market is a specialized segment within the flexible packaging industry, focusing on films embedded with microscopic perforations designed to regulate gas exchange and moisture levels inside packaging. These films are crucial in extending the shelf life and maintaining the quality of perishable goods such as fresh produce, bakery items, meat, dairy, and snack foods. The market encompasses a variety of polymer types including polyethylene, polypropylene, polyester, and polyamide, each offering unique barrier and mechanical properties tailored to specific packaging needs. Technological progress in micro-perforation techniques and multilayer film manufacturing has enhanced the functional performance of these films, enabling better product preservation and reducing food waste globally. The market is driven by increasing consumer demand for fresh and longer-lasting food products, sustainability initiatives promoting recyclable and efficient packaging, and regulatory pressures on food safety and environmental impact. Furthermore, the growing adoption of ready-to-eat and convenience foods fuels demand for innovative packaging solutions that ensure freshness while supporting extended distribution channels worldwide.

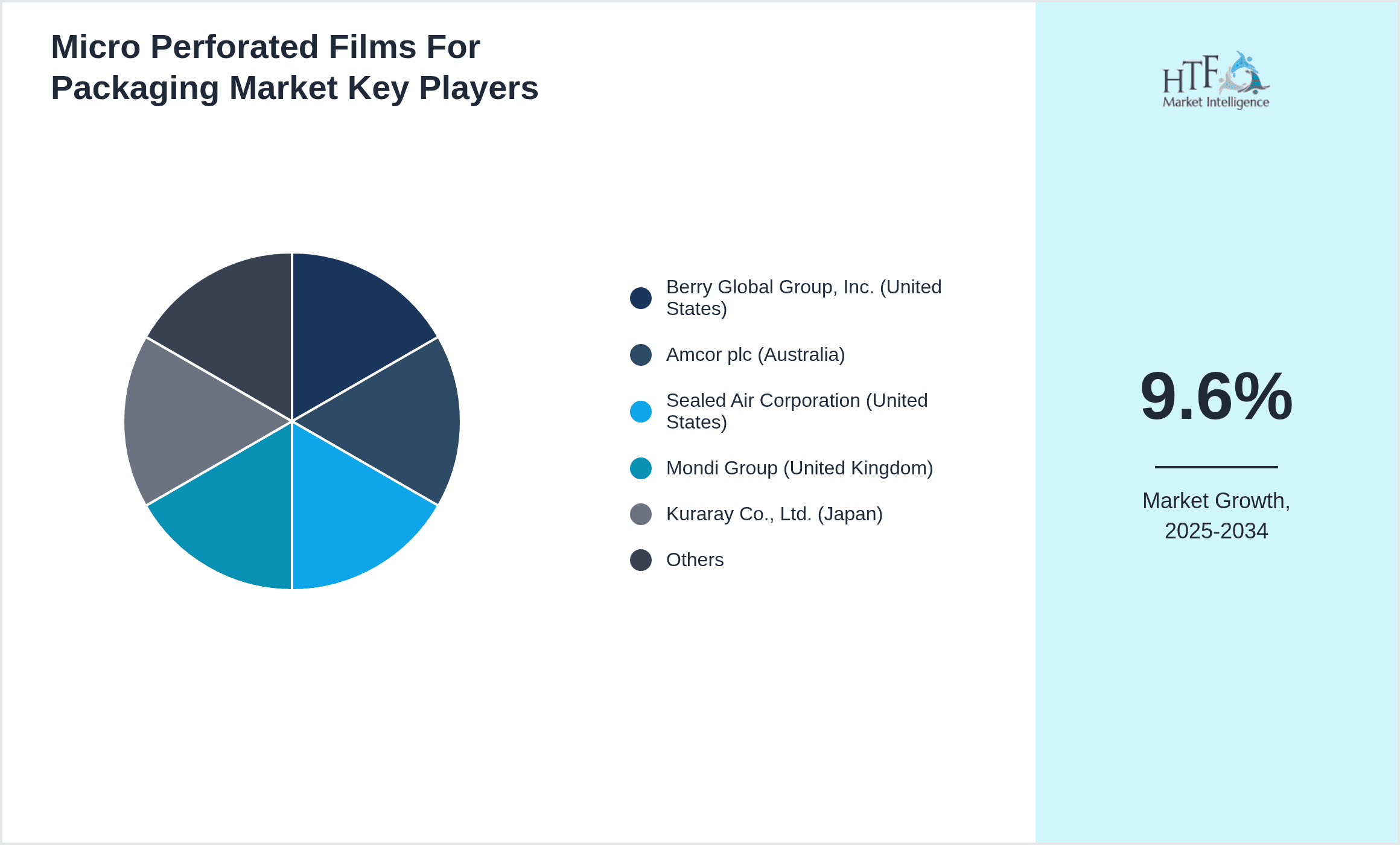

- •Market highlights include a robust compound annual growth rate (CAGR) of approximately 9.6% projected between 2024 and 2034, with the global market size expected to increase from USD 2.85 billion in 2024 to USD 7.45 billion by 2034. North America currently dominates the market, attributed to advanced packaging technologies and strong demand for fresh food packaging, while Asia-Pacific is identified as the fastest-growing region, driven by rising urbanization, expanding food processing industries, and increasing consumer awareness regarding food quality. Polyethylene micro perforated films hold the largest market share due to their versatility and cost-effectiveness, whereas polyamide films are gaining traction as the fastest-growing type owing to their superior barrier properties. Fresh produce packaging remains the leading application segment, benefiting from the increasing global demand for fresh fruits and vegetables and stringent quality control standards. Key players continue to invest in research and development to innovate product offerings and expand their global footprint.

- •The strategic importance of micro perforated films in packaging spans across multiple industries including food and beverages, pharmaceuticals, and agriculture, where product freshness and shelf life directly impact consumer satisfaction and profitability. These films offer a sustainable alternative to traditional packaging by enabling reduced food spoilage and waste, aligning with global sustainability goals. Stakeholders such as packaging manufacturers, food producers, and retailers leverage these technologies to enhance product value and comply with regulatory standards. The market's growth is further supported by advancements in film extrusion and perforation technologies, increasing demand for flexible and eco-friendly packaging solutions, and expanding applications across emerging markets. Consequently, micro perforated films are positioned as a critical enabler in the evolving packaging landscape, providing opportunities for innovation, market expansion, and collaboration among industry participants worldwide.

Competitive Landscape

The competitive environment in the global Micro Perforated Films For Packaging market is characterized by a mix of multinational corporations and regional manufacturers focused on technological innovation, strategic partnerships, and capacity expansion to secure market share. Companies prioritize R&D investments to develop advanced polymer blends and optimized perforation techniques that enhance film breathability while maintaining barrier properties. Market players differentiate through product customization, sustainability initiatives such as developing biodegradable and recyclable films, and expanding distribution networks to cater to diverse geographical markets. Intense competition fosters continuous innovation, driving efficiency improvements and cost reductions. Additionally, mergers and acquisitions are common strategies to consolidate capabilities, access new markets, and broaden product portfolios. Market entry barriers include high capital investment for production technology and stringent regulatory compliance. Regional competition varies, with Asia-Pacific witnessing rapid growth encouraging new entrants, while North America and Europe focus on premium and high-performance films. Future trends indicate an increased emphasis on digitalization of supply chains and collaboration across the value chain to enhance responsiveness and customer satisfaction.

Prominent Players in Micro Perforated Films For Packaging Market

- •Berry Global Group, Inc. (United States)

- •Amcor plc (Australia)

- •Sealed Air Corporation (United States)

- •Mondi Group (United Kingdom)

- •Kuraray Co., Ltd. (Japan)

- •Innovia Films Ltd. (United Kingdom)

- •Uflex Limited (India)

- •Jindal Poly Films Limited (India)

- •Toray Industries, Inc. (Japan)

- •Solenis LLC (United States)

- •DuPont de Nemours, Inc. (United States)

- •Crown Holdings, Inc. (United States)

- •Constantia Flexibles Group GmbH (Austria)

- •Bemis Company, Inc. (United States)

- •BASF SE (Germany)

- •Mitsubishi Chemical Corporation (Japan)

- •Treofan Group (Germany)

- •Polyplex Corporation Limited (India)

- •Celplast Metallized Products Limited (India)

- •Clondalkin Group Holdings BV (Netherlands)

- •Sonoco Products Company (United States)

- •Huhtamaki Oyj (Finland)

- •Solenis LLC (United States)

- •ExxonMobil Chemical Company (United States)

- •Lotte Chemical Corporation (South Korea)

Market Breakdown

- •By Product Type

- ◦Polyethylene Micro Perforated Films

- ◦Polypropylene Micro Perforated Films

- ◦Polyester Micro Perforated Films

- ◦Polyamide Micro Perforated Films

- ◦Others

- •By Application

- ◦Fresh Produce Packaging

- ◦Bakery Packaging

- ◦Meat & Seafood Packaging

- ◦Dairy Packaging

- ◦Snack Foods Packaging

- •By End-Use Industry

- ◦Food & Beverages

- ◦Pharmaceuticals

- ◦Agriculture

- ◦Consumer Goods

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors & Wholesalers

- ◦Online Channels

Growth Dynamics

The global Micro Perforated Films For Packaging market is propelled by increasing consumer demand for fresh, minimally processed food products that require packaging solutions preserving quality and extending shelf life. Rising awareness about food waste reduction encourages adoption of films that enable optimal gas exchange, maintaining freshness in fruits, vegetables, and bakery goods. Technological advancements such as precision micro-perforation enhance breathability without compromising barrier integrity, driving product innovation. Additionally, the growing trend towards sustainable packaging fuels demand for recyclable and biodegradable micro perforated films, supported by government regulations and corporate sustainability commitments. Expansion of the global food processing industry, particularly in developing economies, and rising urbanization further stimulate market growth by increasing packaged food consumption. These factors collectively create favorable conditions for manufacturers to invest in capacity expansion and R&D, thus accelerating market penetration and diversification across applications and regions.

Market Trends

A prominent trend in the micro perforated films market is the integration of eco-friendly materials, such as biodegradable polymers and recycled content, responding to consumer and regulatory pressure for sustainable packaging solutions. Companies are innovating multilayer films that combine performance with environmental compliance, enabling reduced plastic usage and easier recycling. Another developing trend is the customization of perforation patterns tailored to specific product respiration rates, improving freshness and minimizing spoilage. Digital printing technologies are increasingly adopted for enhanced branding and traceability on micro perforated films. Additionally, collaborative initiatives between film manufacturers and food producers are gaining traction to co-develop packaging that aligns with supply chain requirements and consumer preferences. The rise of e-commerce and demand for convenience foods also drive the need for durable, breathable packaging that supports longer transit times and varied storage conditions.

Market Opportunities

Significant opportunities exist in expanding the application of micro perforated films beyond traditional fresh produce packaging into sectors like pharmaceuticals and agriculture, where controlled atmosphere packaging can improve product stability. Emerging markets in Asia-Pacific and Latin America present high growth potential due to increasing urbanization, rising disposable incomes, and expanding food processing industries. Innovation in biodegradable and compostable micro perforated films offers manufacturers a competitive edge amid tightening environmental regulations. Strategic partnerships with food retailers and manufacturers can facilitate tailored packaging solutions that address specific product needs and supply chain challenges. Furthermore, investments in advanced manufacturing technologies such as laser perforation can enhance production efficiency and product quality, enabling companies to meet evolving market demands. These opportunities pave the way for market expansion, diversification, and enhanced sustainability practices.

Market Challenges

The market faces challenges including the high cost of advanced micro perforation technologies and raw materials, which can limit adoption, especially among small and medium-sized enterprises in developing regions. Maintaining a balance between adequate breathability and barrier protection is technically complex, requiring precise manufacturing control and quality assurance. Regulatory compliance with varying international standards creates hurdles for global market players, necessitating continuous adaptation and certification efforts. Additionally, the environmental impact of plastic films remains a concern despite advances in sustainability, with ongoing scrutiny over recyclability and biodegradability slowing widespread acceptance. Supply chain disruptions and fluctuating raw material prices further pose risks to cost stability and production continuity. These challenges require strategic investments in technology, collaboration with regulatory bodies, and innovation to address sustainability and cost-effectiveness.

Regulatory Framework

Between 2020 and 2024, several key regulations have shaped the global Micro Perforated Films For Packaging market. The European Union's Single-Use Plastics Directive, enacted in 2021, mandates reduction in plastic waste and promotes recyclable packaging materials, compelling manufacturers to innovate sustainable films. The U.S. Food and Drug Administration updated its guidelines on food contact materials in 2022, emphasizing safety standards for packaging polymers to prevent contamination. Additionally, China's Plastic Pollution Control Action Plan (2020) restricts non-degradable plastic use, accelerating adoption of biodegradable films. Various countries have introduced extended producer responsibility (EPR) schemes requiring manufacturers to manage end-of-life packaging, influencing design and material choice. Compliance with these regulations necessitates investment in research for eco-friendly micro perforated films and alignment with international safety standards, impacting market dynamics and competitive strategies.

Market Intelligence

- •15th March 2024, Berry Global Group, Inc. launched a new line of biodegradable polyethylene micro perforated films designed specifically for fresh produce packaging. These films incorporate advanced micro-perforation technology to optimize gas exchange, extending shelf life while ensuring environmental sustainability. The product is targeted at major retail chains seeking eco-friendly packaging options without compromising product quality. Berry Global's innovation aligns with increasing regulatory pressures and consumer demand for greener alternatives, positioning the company as a leader in sustainable packaging solutions globally. This new launch is expected to accelerate adoption in North America and Europe, reinforcing Berry Global's competitive advantage in the micro perforated films market. Source: Berry Global official press release.

- •22nd September 2023, Amcor plc announced a strategic partnership with a leading food retailer to co-develop customized micro perforated films that cater to specific respiration needs of tropical fruits. The collaboration focuses on leveraging Amcor's proprietary perforation technology and the retailer's supply chain insights to reduce spoilage and enhance freshness during extended distribution. This initiative reflects an industry trend toward tailored packaging solutions that improve product quality and reduce food waste. The partnership also underscores Amcor's commitment to innovation and sustainability by integrating recyclable materials within the product design. This development is anticipated to drive growth in the Asia-Pacific region and contribute to Amcor's global market expansion strategy. Source: Amcor corporate announcement.

- •14th January 2025, Sealed Air Corporation unveiled an upgraded version of its micro perforated film portfolio incorporating laser perforation technology. This advancement enables precise control over perforation size and distribution, enhancing breathability and mechanical strength simultaneously. The new films target bakery and snack food packaging applications, offering improved freshness retention and package integrity. Sealed Air aims to address the growing demand for high-performance, sustainable packaging by combining innovative technology with recyclable materials. The upgraded portfolio launch is expected to strengthen Sealed Air's market position in North America and Europe, driving revenue growth and customer satisfaction. Source: Sealed Air product launch briefing.

- •30th June 2024, Mondi Group expanded its production capacity for polyester micro perforated films in its European manufacturing facility. This investment responds to rising demand from pharmaceutical and specialty food sectors requiring high-barrier breathable packaging solutions. The capacity increase involves state-of-the-art extrusion and perforation equipment, enhancing product quality and throughput efficiency. Mondi's strategic expansion supports its commitment to sustainable packaging innovation and responsiveness to customer needs across global markets. The move is projected to bolster Mondi's competitive edge and support growth in key regions including Europe and Asia-Pacific. Source: Mondi Group press release.

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 2.85 Billion |

| Forecast Year Market Size | USD 7.45 Billion |

| CAGR | 9.6% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 9.2% |

| Scope of Report | Market is segmented by Product Type (Polyethylene Micro Perforated Films, Polypropylene Micro Perforated Films, Polyester Micro Perforated Films, Polyamide Micro Perforated Films, Others), Application (Fresh Produce Packaging, Bakery Packaging, Meat & Seafood Packaging, Dairy Packaging, Snack Foods Packaging), End-Use Industry (Food & Beverages, Pharmaceuticals, Agriculture, Consumer Goods), Distribution Channel (Direct Sales, Distributors & Wholesalers, Online Channels) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Berry Global Group, Inc. (United States), Amcor plc (Australia), Sealed Air Corporation (United States), Mondi Group (United Kingdom), Kuraray Co., Ltd. (Japan), Innovia Films Ltd. (United Kingdom), Uflex Limited (India), Jindal Poly Films Limited (India), Toray Industries, Inc. (Japan), Solenis LLC (United States), DuPont de Nemours, Inc. (United States), Crown Holdings, Inc. (United States), Constantia Flexibles Group GmbH (Austria), Bemis Company, Inc. (United States), BASF SE (Germany), Mitsubishi Chemical Corporation (Japan), Treofan Group (Germany), Polyplex Corporation Limited (India), Celplast Metallized Products Limited (India), Clondalkin Group Holdings BV (Netherlands), Sonoco Products Company (United States), Huhtamaki Oyj (Finland), Solenis LLC (United States), ExxonMobil Chemical Company (United States), Lotte Chemical Corporation (South Korea) |

Global Micro Perforated Films For Packaging Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.