Global Cold Cereal Food Market Size, Growth & Revenue 2024-2034

Global Cold Cereal Food Market is segmented by Product Type (Flakes, Granola, Puffed Cereals, Muesli, Oats), Application (Breakfast, Snack, Ingredient, Health & Wellness, Convenience), End-Use Industry (Retail, Foodservice, Online Sales, Institutional), Distribution Channel (Supermarkets/Hypermarkets, Convenience Stores, Online Retail, Specialty Stores), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global cold cereal food market represents a robust segment of the packaged food industry characterized by a variety of grain-based breakfast and snack products designed for convenience and nutrition. This market includes key product categories like flakes, granola, puffed cereals, muesli, and oats, which cater to diverse consumer preferences worldwide. The scope extends to multiple applications such as breakfast consumption, healthy snacking, ingredient use in food manufacturing, health and wellness-focused diets, and convenience foods. The market is influenced by consumer trends towards healthy living, increasing demand for organic and natural ingredients, and innovation in product formulations and packaging. Distribution occurs through supermarkets, hypermarkets, online retail, and specialty health stores globally. Regional consumption patterns vary significantly, with North America and Europe leading in market size, while Asia-Pacific registers the fastest growth owing to rising urbanization and changing lifestyles. The market's growth is supported by technological advancements in cereal processing, fortification, and sustainable sourcing, making it a dynamic and competitive sector globally.

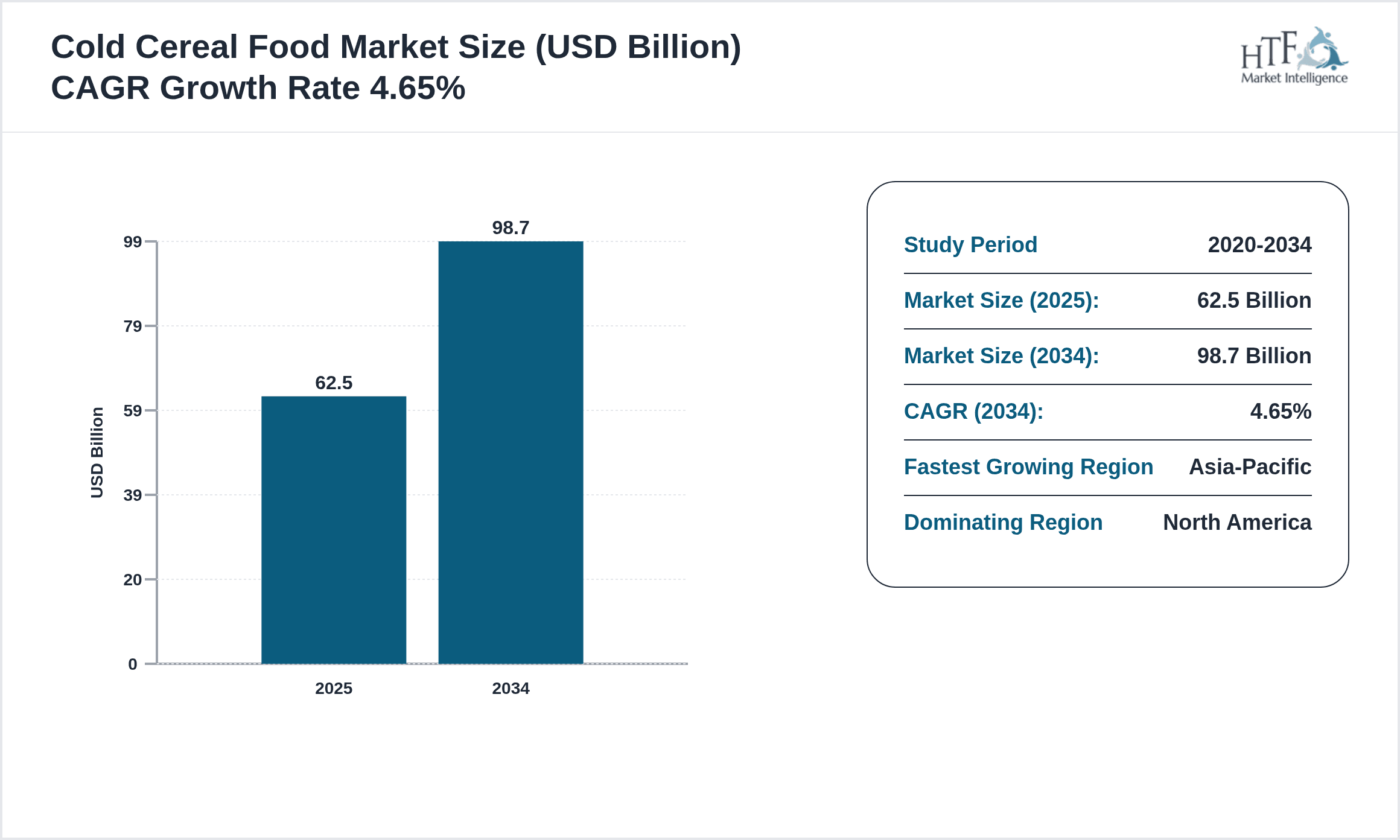

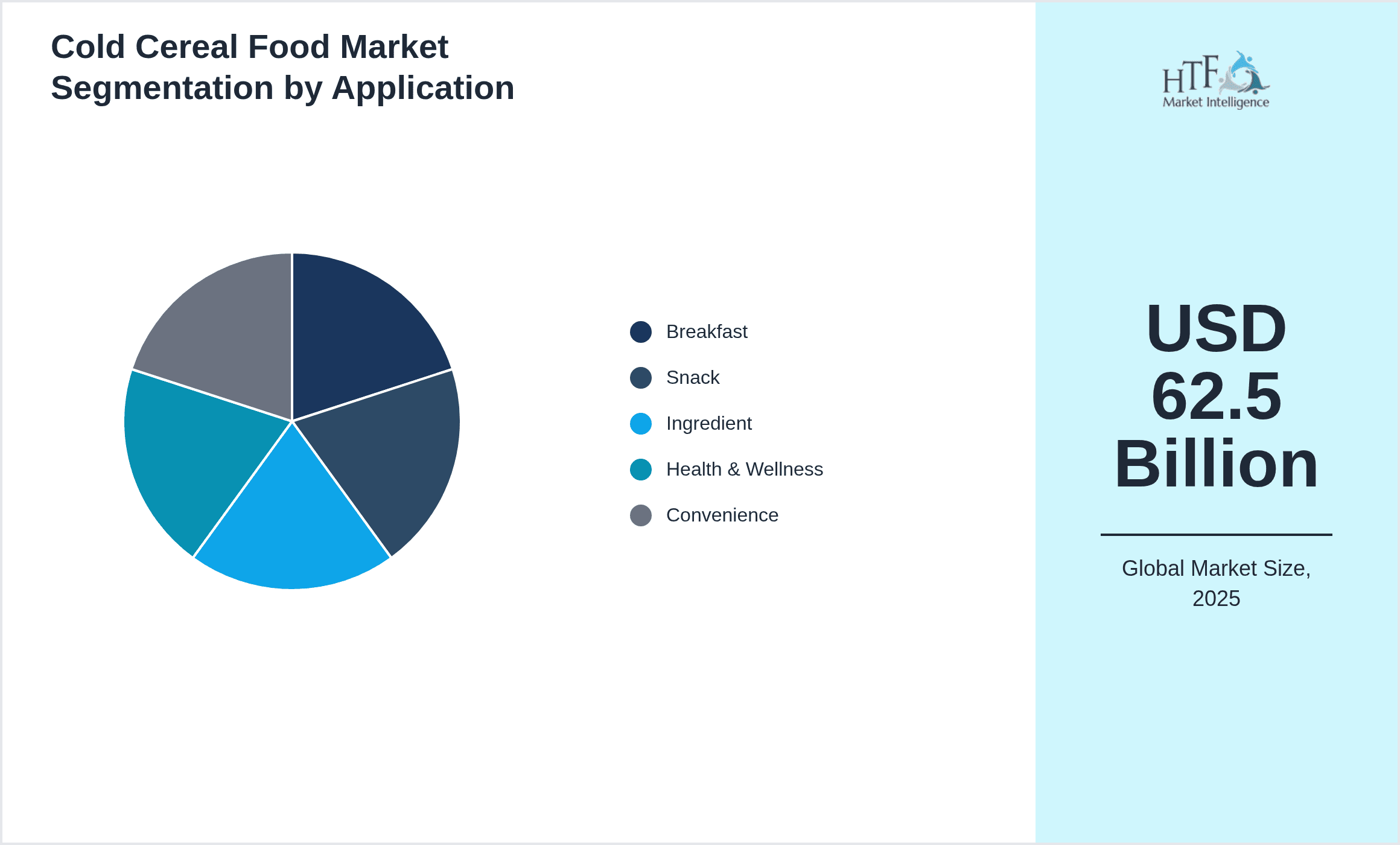

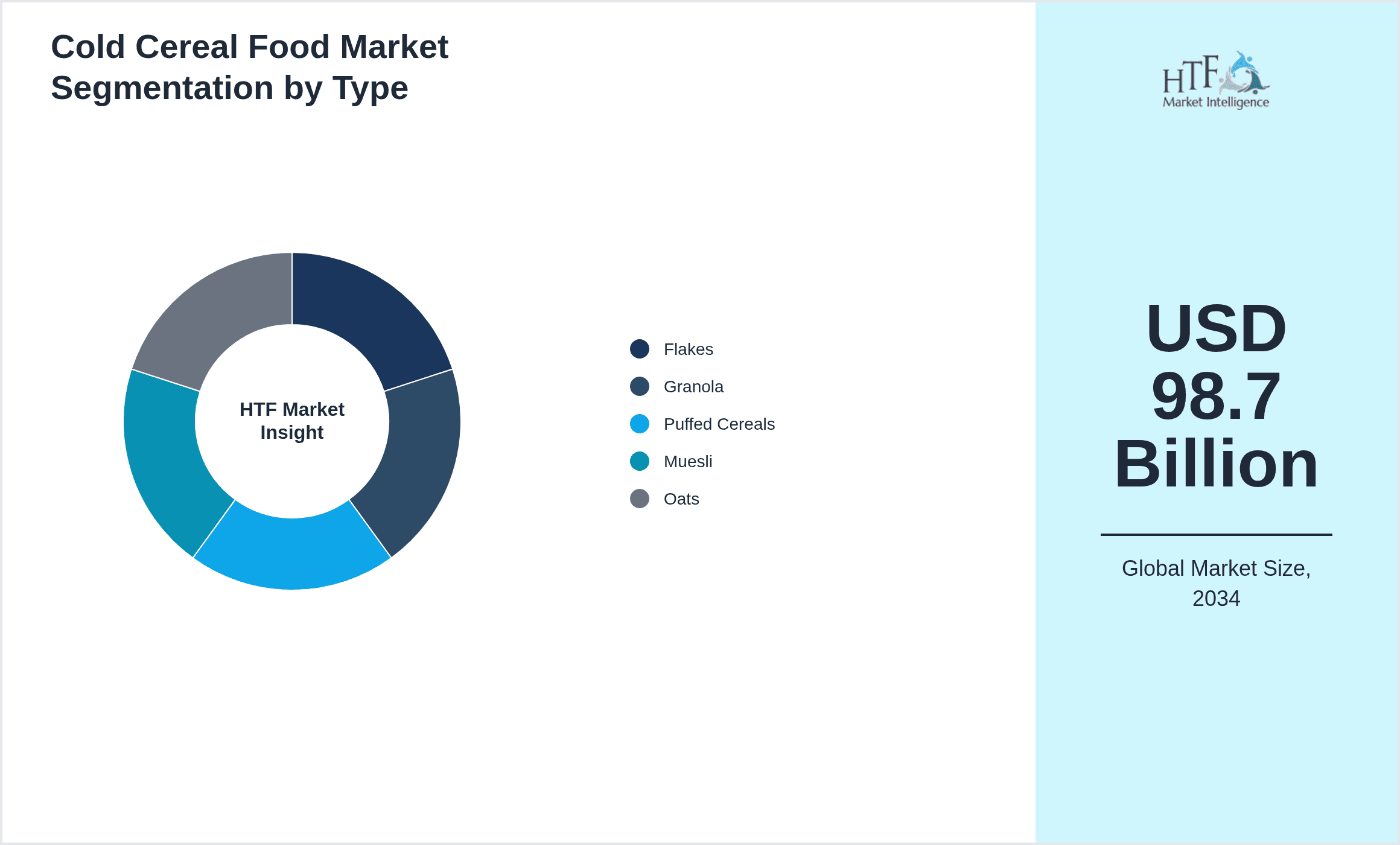

- •Key market highlights include a base market size of USD 62.5 billion in 2024 with a projected expansion to USD 98.7 billion by 2034, reflecting a compound annual growth rate (CAGR) of approximately 4.65%. North America dominates the market owing to high consumer awareness, established retail infrastructure, and premium product availability. Asia-Pacific is the fastest-growing region due to increasing disposable incomes, rapid urbanization, and shifting dietary habits favoring convenient breakfast options. Flakes remain the leading product type by revenue share, while granola is gaining traction as the fastest-growing segment, driven by health-conscious consumers. Breakfast remains the primary application segment, with snacks and health & wellness applications contributing to market diversification. The market exhibits steady year-on-year growth averaging 4.55%, supported by innovation, new product launches, and expanding distribution channels worldwide.

- •The global cold cereal food market offers significant value propositions to manufacturers, distributors, and retailers by catering to increasing consumer demands for convenience, nutrition, and variety in breakfast foods. Strategic importance lies in innovation around product formulation, including organic, gluten-free, and fortified cereals, which address evolving health trends. The market also presents opportunities for expansion into emerging regions with growing middle classes and rising health awareness. Key stakeholders benefit from diverse product portfolios and multi-channel distribution strategies that enhance market penetration. Additionally, the sector's adaptability to changing consumer preferences and technological enhancements in processing and packaging strengthens competitive positioning. The cold cereal market's alignment with global health and wellness trends further underscores its relevance across industries such as food manufacturing, retail, and nutrition-focused enterprises.

Competitive Landscape

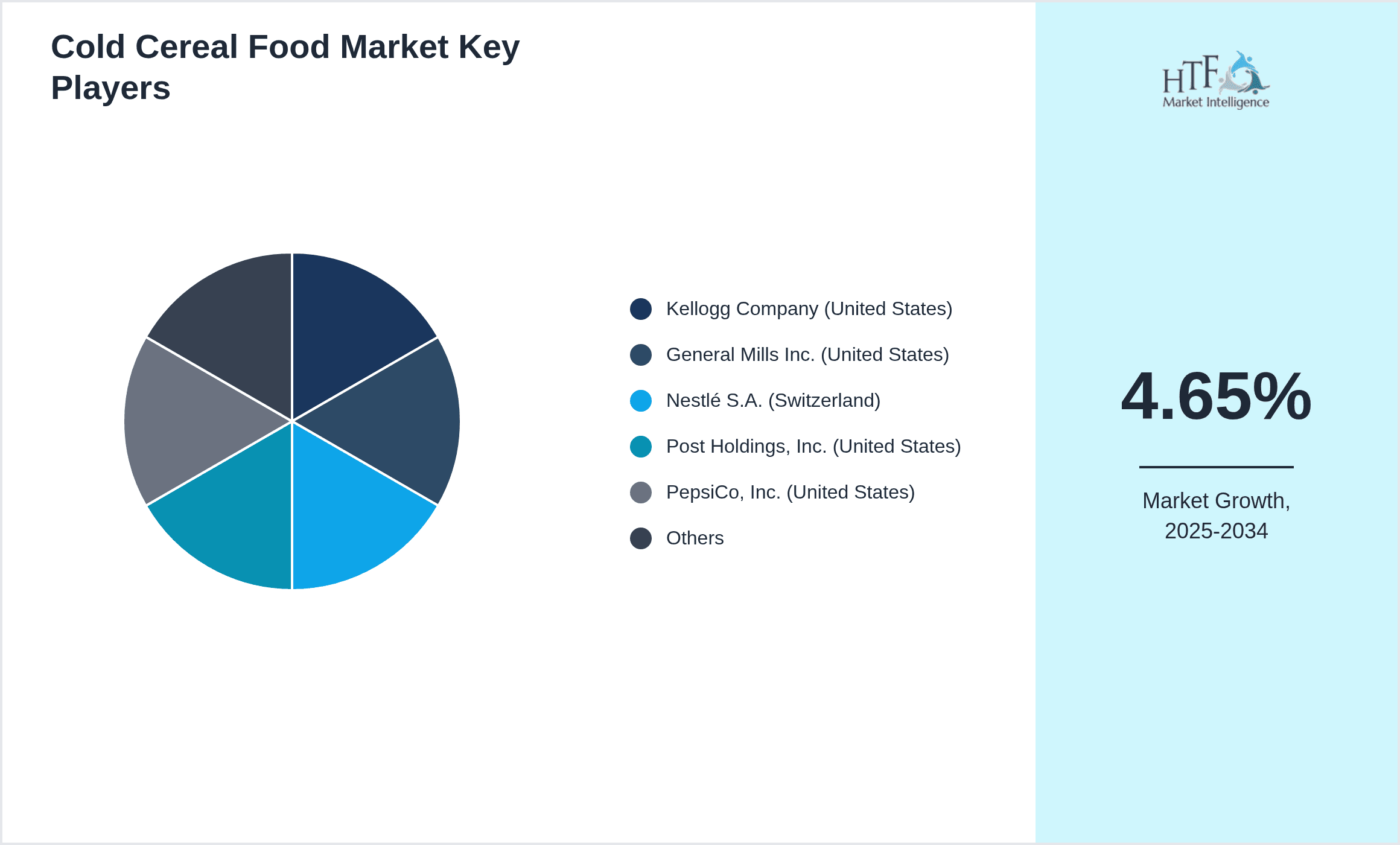

The global cold cereal food market is highly competitive with numerous multinational corporations and regional players vying for market share. Market dynamics are shaped by product innovation, branding, pricing strategies, and distribution channel expansion. Companies invest heavily in research and development to introduce new flavors, healthier ingredients, and convenient packaging solutions to differentiate themselves. Strategic partnerships and collaborations between manufacturers and retailers enhance product availability and consumer reach. Innovation in organic and specialty cereals caters to niche segments, intensifying competition. Mergers and acquisitions are frequent, facilitating portfolio diversification and geographic expansion. Competitive advantages arise from strong brand equity, supply chain efficiencies, and responsiveness to consumer trends. Regional competition varies, with North America and Europe exhibiting mature markets with intense rivalry, while Asia-Pacific features emerging competition driven by local and international players. The market also faces challenges from private label brands and alternative breakfast options, fueling competitive pressure and driving continuous improvement across the industry.

Leading Companies in Cold Cereal Food Market

- •Kellogg Company (United States)

- •General Mills Inc. (United States)

- •Nestlé S.A. (Switzerland)

- •Post Holdings, Inc. (United States)

- •PepsiCo, Inc. (United States)

- •Weetabix Limited (United Kingdom)

- •Quaker Oats Company (United States)

- •B&G Foods, Inc. (United States)

- •Nature's Path Foods Inc. (Canada)

- •Bob's Red Mill Natural Foods (United States)

- •Post Consumer Brands (United States)

- •Freedom Foods Group Limited (Australia)

- •Cereal Partners Worldwide (Switzerland)

- •Barilla Group (Italy)

- •General Mills India Pvt. Ltd. (India)

- •Bimbo Bakeries USA (United States)

- •The Hain Celestial Group, Inc. (United States)

- •Lantmännen (Sweden)

- •Grupo Bimbo, S.A.B. de C.V. (Mexico)

- •Pepsi Lipton International (United States)

- •Mornflake Oats Ltd. (United Kingdom)

- •J. M. Smucker Company (United States)

- •Roland Foods LLC (United States)

- •Arrowhead Mills (United States)

- •Kashi Company (United States)

Market Breakdown

- •By Product Type

- ◦Flakes

- ◦Granola

- ◦Puffed Cereals

- ◦Muesli

- ◦Oats

- •By Application

- ◦Breakfast

- ◦Snack

- ◦Ingredient

- ◦Health & Wellness

- ◦Convenience

- •By End-Use Industry

- ◦Retail

- ◦Foodservice

- ◦Online Sales

- ◦Institutional

- •By Distribution Channel

- ◦Supermarkets/Hypermarkets

- ◦Convenience Stores

- ◦Online Retail

- ◦Specialty Stores

Growth Dynamics

The global cold cereal food market experiences accelerated growth driven by rising consumer health awareness and demand for convenient breakfast options. Increasing urbanization and changing lifestyles have led to greater consumption of ready-to-eat cereals across emerging and developed markets. Innovation in product offerings, such as organic, gluten-free, and high-protein cereals, attracts a broad consumer base focused on nutrition. Expansion of modern retail formats and e-commerce platforms facilitates wider product availability and greater market penetration globally. Additionally, the growing trend toward plant-based diets and clean-label products further propels market growth by meeting evolving consumer preferences. Market players capitalize on these drivers through product diversification, strategic marketing, and geographic expansion, ensuring sustained revenue growth and competitive advantage in the dynamic global cold cereal food landscape.

Market Trends

Recent trends in the cold cereal food market include a surge in demand for health-focused products enriched with fiber, protein, and superfoods. Consumers increasingly prefer cereals with natural ingredients, minimal processing, and transparent labeling, driving reformulations and new product launches. The adoption of sustainable sourcing practices and environmentally friendly packaging aligns with growing consumer environmental consciousness. Additionally, digital marketing and direct-to-consumer sales channels have enhanced brand engagement and accessibility. Functional cereals targeting specific health benefits like gut health and immunity are gaining popularity. Regional flavor adaptations and premiumization through gourmet ingredients also shape market offerings. These trends reflect a broader shift towards personalized nutrition and ethical consumption, fostering innovation and growth opportunities across the global cold cereal sector.

Market Opportunities

Significant opportunities exist for market expansion in emerging regions such as Asia-Pacific and Latin America, where rising incomes and urban lifestyles fuel demand for convenient breakfast foods. The increasing popularity of plant-based and organic cereals offers avenues for innovative product development and premium pricing. Growth in e-commerce and online grocery retail enables brands to reach previously untapped consumer segments. Collaborations with health and wellness influencers and personalized nutrition platforms can further enhance market presence. Additionally, integrating functional ingredients that address specific health concerns like diabetes or weight management presents niche opportunities. Companies investing in sustainable production methods and eco-friendly packaging can differentiate themselves and appeal to environmentally conscious consumers. These factors collectively provide strategic pathways to capture additional market share and drive long-term growth in the global cold cereal food industry.

Market Challenges

The global cold cereal food market faces challenges including intense competition from alternative breakfast options such as ready-to-eat hot cereals, protein bars, and fresh foods. Price sensitivity among consumers, especially in emerging markets, limits premium product penetration. Supply chain disruptions and fluctuating raw material costs impact profitability and product availability. Regulatory compliance related to food safety, labeling, and health claims requires continuous adaptation and investment. Additionally, changing consumer preferences toward low-carb or keto diets may reduce demand for traditional cereal products. The increasing presence of private label brands poses a threat to established players by offering lower-priced alternatives. Companies must navigate these challenges through innovation, cost optimization, and effective marketing strategies to sustain competitiveness and growth.

Regulatory Framework

Between 2019 and 2024, the cold cereal food market has seen the implementation of stricter food safety regulations and labeling requirements across major regions including North America, Europe, and Asia-Pacific. Regulatory bodies have mandated transparent disclosure of nutritional information, ingredient sourcing, and allergen warnings to enhance consumer protection. Compliance with organic certification, non-GMO standards, and fortification guidelines has become increasingly important for market players targeting health-conscious segments. The introduction of sugar reduction targets and limits on artificial additives has driven reformulation efforts. Additionally, packaging regulations promoting sustainability and recyclability have influenced product design and supply chain practices. These regulatory frameworks require continuous monitoring and adaptation by manufacturers to ensure market access and maintain consumer trust globally.

Market Intelligence

- •15th June 2024, Kellogg Company launched a new line of plant-based granola cereals designed to meet growing consumer demand for sustainable and health-conscious products. The new range features organic ingredients, no added sugars, and recyclable packaging, targeting millennials and Gen Z consumers globally. This launch is aligned with Kellogg's strategic objectives to expand its presence in the health and wellness category and reduce environmental impact. The product rollout includes extensive digital marketing campaigns and partnerships with health influencers to boost brand engagement and market penetration.

- •10th October 2023, General Mills introduced an innovative oat-based muesli enriched with probiotics to enhance digestive health. Leveraging cutting-edge fermentation technology, this product targets health-conscious consumers seeking functional foods. The launch reflects General Mills’ focus on expanding its portfolio in emerging health categories and strengthening its competitive position in North America and Europe. The company also announced plans to increase production capacity and distribution through online and traditional retail channels.

- •20th March 2024, Nestlé S.A. announced a global partnership with a leading sustainable packaging firm to transition its cold cereal product lines to biodegradable materials by 2026. This initiative supports Nestlé's commitment to environmental sustainability and meeting regulatory requirements across key markets. The collaboration aims to reduce plastic waste significantly and enhance brand reputation among eco-conscious consumers. Implementation will begin with pilot programs in Europe and North America before worldwide expansion.

- •5th August 2023, Post Holdings completed the acquisition of a premium organic cereal manufacturer to diversify its portfolio and strengthen its position in the natural and organic segment. The acquisition includes product innovation capabilities and expanded distribution networks in North America and Europe. This strategic move allows Post Holdings to capitalize on increasing demand for clean-label and health-oriented breakfast products and accelerate growth in competitive markets.

- •Source: Official press releases, company websites, industry publications

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 62.5 Billion |

| Forecast Year Market Size | USD 98.7 Billion |

| CAGR | 4.65% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 4.55% |

| Scope of Report | Market is segmented by Product Type (Flakes, Granola, Puffed Cereals, Muesli, Oats), Application (Breakfast, Snack, Ingredient, Health & Wellness, Convenience), End-Use Industry (Retail, Foodservice, Online Sales, Institutional), Distribution Channel (Supermarkets/Hypermarkets, Convenience Stores, Online Retail, Specialty Stores) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Kellogg Company (United States), General Mills Inc. (United States), Nestlé S.A. (Switzerland), Post Holdings, Inc. (United States), PepsiCo, Inc. (United States), Weetabix Limited (United Kingdom), Quaker Oats Company (United States), B&G Foods, Inc. (United States), Nature's Path Foods Inc. (Canada), Bob's Red Mill Natural Foods (United States), Post Consumer Brands (United States), Freedom Foods Group Limited (Australia), Cereal Partners Worldwide (Switzerland), Barilla Group (Italy), General Mills India Pvt. Ltd. (India), Bimbo Bakeries USA (United States), The Hain Celestial Group, Inc. (United States), Lantmännen (Sweden), Grupo Bimbo, S.A.B. de C.V. (Mexico), Pepsi Lipton International (United States), Mornflake Oats Ltd. (United Kingdom), J. M. Smucker Company (United States), Roland Foods LLC (United States), Arrowhead Mills (United States), Kashi Company (United States) |

Global Cold Cereal Food Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.