Global Cooked Cereal Market Size, Growth & Revenue 2025-2034

Global Cooked Cereal Market is segmented by Product Type (Oat-based Cooked Cereals, Rice-based Cooked Cereals, Wheat-based Cooked Cereals, Corn-based Cooked Cereals, Multigrain Cooked Cereals), Application (Breakfast Foods, Infant Nutrition, Snack Foods, Convenience Foods, Animal Feed), End-Use Industry (Retail, Foodservice, Infant Food Manufacturing, Animal Feed Production), Distribution Channel (Supermarkets & Hypermarkets, Convenience Stores, Online Retail, Specialty Stores), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global cooked cereal market comprises processed cereal products prepared through cooking or steaming, offering a versatile range of types including oat-based, rice-based, wheat-based, corn-based, and multigrain variants. These cereals find applications in breakfast meals, infant nutrition, snack foods, convenience foods, and animal feed, catering to diverse consumer needs across multiple channels. The market’s value chain integrates key stages such as grain cultivation, harvesting, processing, fortification, packaging, and distribution through retail and foodservice outlets worldwide. Health-conscious consumers are increasingly driving demand for fortified, gluten-free, and organic cooked cereals, while busy lifestyles propel growth in convenience-oriented products. The industry is marked by continuous innovation in processing technologies, enhancing texture, flavor, and nutritional content. Regional preferences vary, with North America maintaining dominance due to mature markets and high consumer awareness, whereas the Asia-Pacific region is rapidly expanding, supported by rising disposable incomes and shifting dietary habits. Global supply chain developments and regulatory frameworks also shape market dynamics, influencing product safety, labeling, and fortification standards. Overall, the market is poised for robust growth from 2025 to 2034, driven by evolving consumer trends and technological advancements.

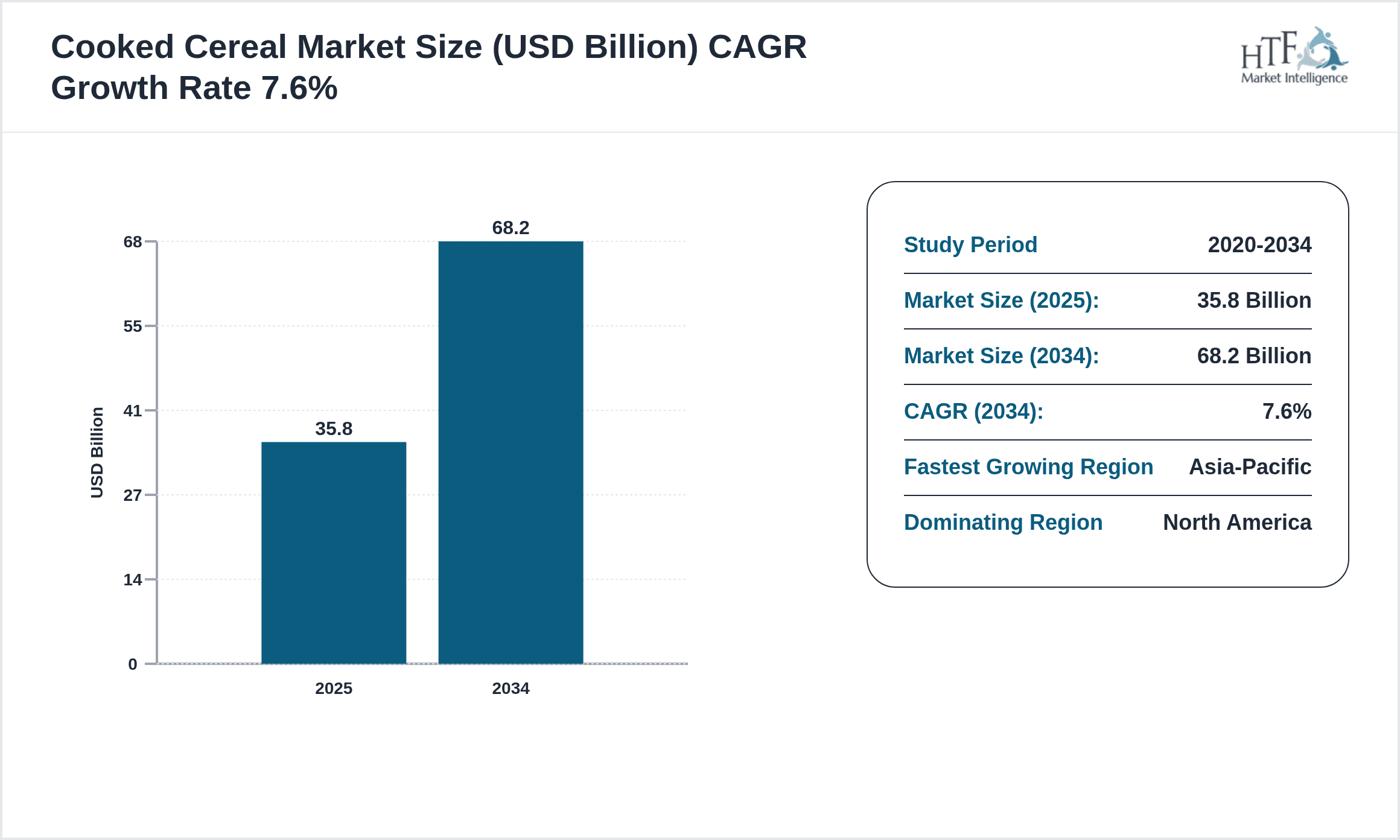

- •Key market highlights include a base year market size of USD 35.8 Billion in 2025, with a forecast to reach USD 68.2 Billion by 2034, representing a compound annual growth rate (CAGR) of 7.6%. The year-on-year growth rate is estimated at 7.4%, reflecting steady demand across regions. The oat-based segment leads in product type due to its nutritional benefits and consumer preference, while multigrain cereals are the fastest-growing product category, propelled by rising awareness of whole grains and dietary fiber. North America dominates the regional market owing to its established manufacturing base and high consumer penetration, whereas Asia-Pacific is the fastest-growing region, driven by urbanization and rising health consciousness.

- •The cooked cereal market offers strategic value to various stakeholders including manufacturers, distributors, retailers, and foodservice providers. For manufacturers, continuous product innovation and diversification into health-oriented segments provide competitive advantages. Retailers benefit from expanding consumer demand for convenience foods and fortified cereals, while consumers gain access to nutritious, ready-to-eat options enhancing dietary quality. Investors and market entrants can capitalize on emerging opportunities in developing regions and premium segments. Overall, the market’s growth trajectory underscores its importance within the global food and beverage industry.

Competitive Landscape

The global cooked cereal market operates within a highly competitive environment characterized by intense rivalry among established multinational corporations and emerging regional players. Companies are leveraging product innovation, brand differentiation, and strategic partnerships to enhance market share and cater to diverse consumer preferences. Competitive strategies include launching fortified and organic product lines, expanding distribution through e-commerce platforms, and investing in sustainable sourcing practices. Market players also engage in mergers and acquisitions to consolidate capabilities and broaden geographic reach. Pricing strategies vary, balancing affordability with premium product positioning to appeal to different consumer segments. Technological advancements in processing and packaging further differentiate offerings, while regulatory compliance and quality assurance remain critical to maintaining brand reputation. Regional competition dynamics are influenced by local consumer behavior, supply chain efficiency, and economic factors. Future trends indicate a shift towards personalized nutrition and clean-label products, compelling companies to adopt agile innovation models and strengthen consumer engagement. Overall, the competitive landscape demands continuous adaptation to evolving market conditions, with a focus on sustainability and health-driven innovation.

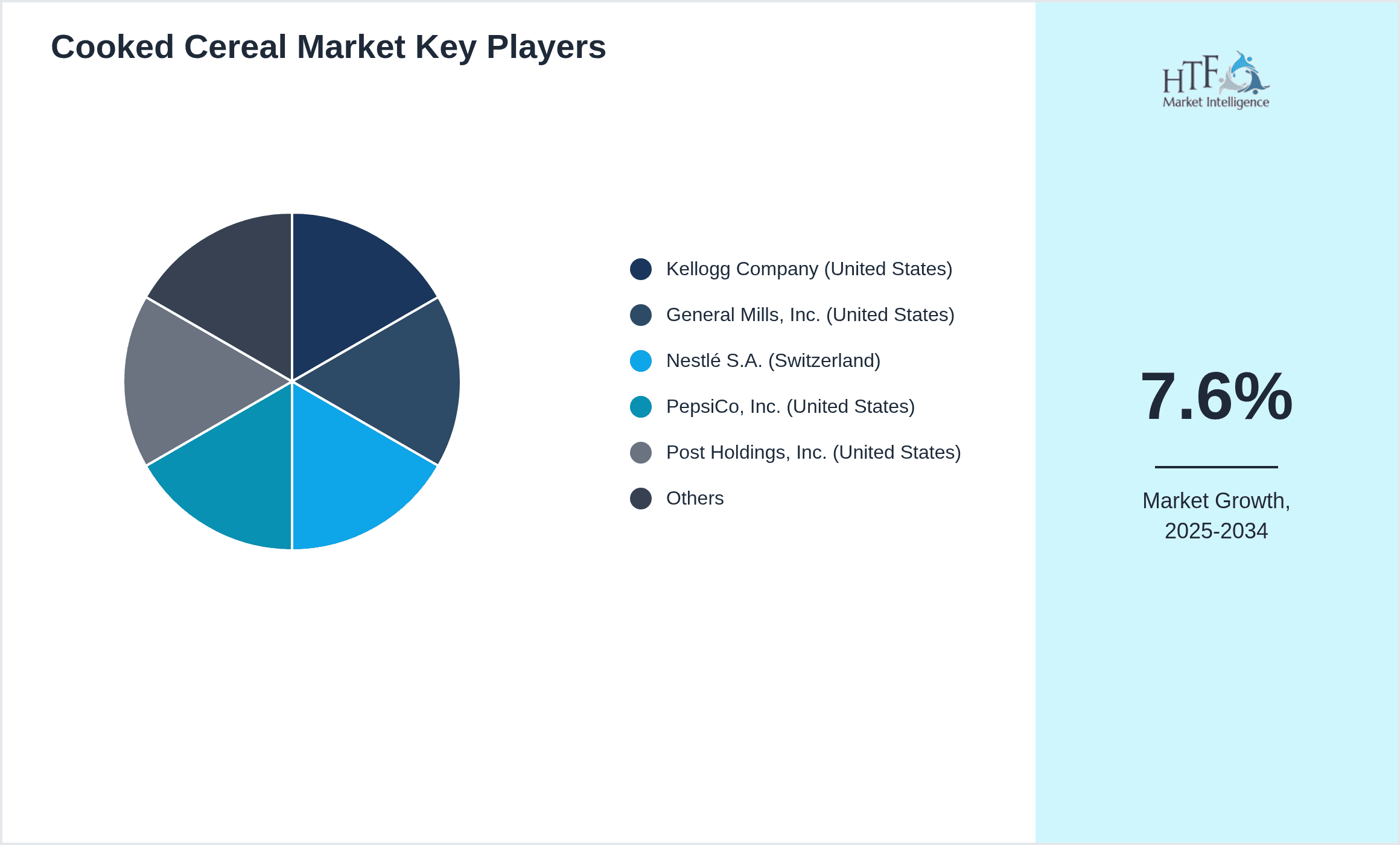

Leading Companies in Cooked Cereal Market

- •Kellogg Company (United States)

- •General Mills, Inc. (United States)

- •Nestlé S.A. (Switzerland)

- •PepsiCo, Inc. (United States)

- •Post Holdings, Inc. (United States)

- •Archer Daniels Midland Company (United States)

- •Quaker Oats Company (United States)

- •The Hain Celestial Group, Inc. (United States)

- •Associated British Foods plc (United Kingdom)

- •Weetabix Limited (United Kingdom)

- •B&G Foods, Inc. (United States)

- •Mornflake Oats Ltd (United Kingdom)

- •Nature’s Path Foods, Inc. (Canada)

- •Bob’s Red Mill Natural Foods, Inc. (United States)

- •Post Consumer Brands (United States)

- •Ebro Foods, S.A. (Spain)

- •Fonterra Co-operative Group Limited (New Zealand)

- •Cargill, Incorporated (United States)

- •SunOpta Inc. (Canada)

- •Peet’s Coffee (United States)

- •General Mills Canada Corporation (Canada)

- •Kashi Company (United States)

- •MGP Ingredients, Inc. (United States)

- •Nature's Path Organic Foods Inc. (Canada)

- •Bell Plantation (United States)

Market Breakdown

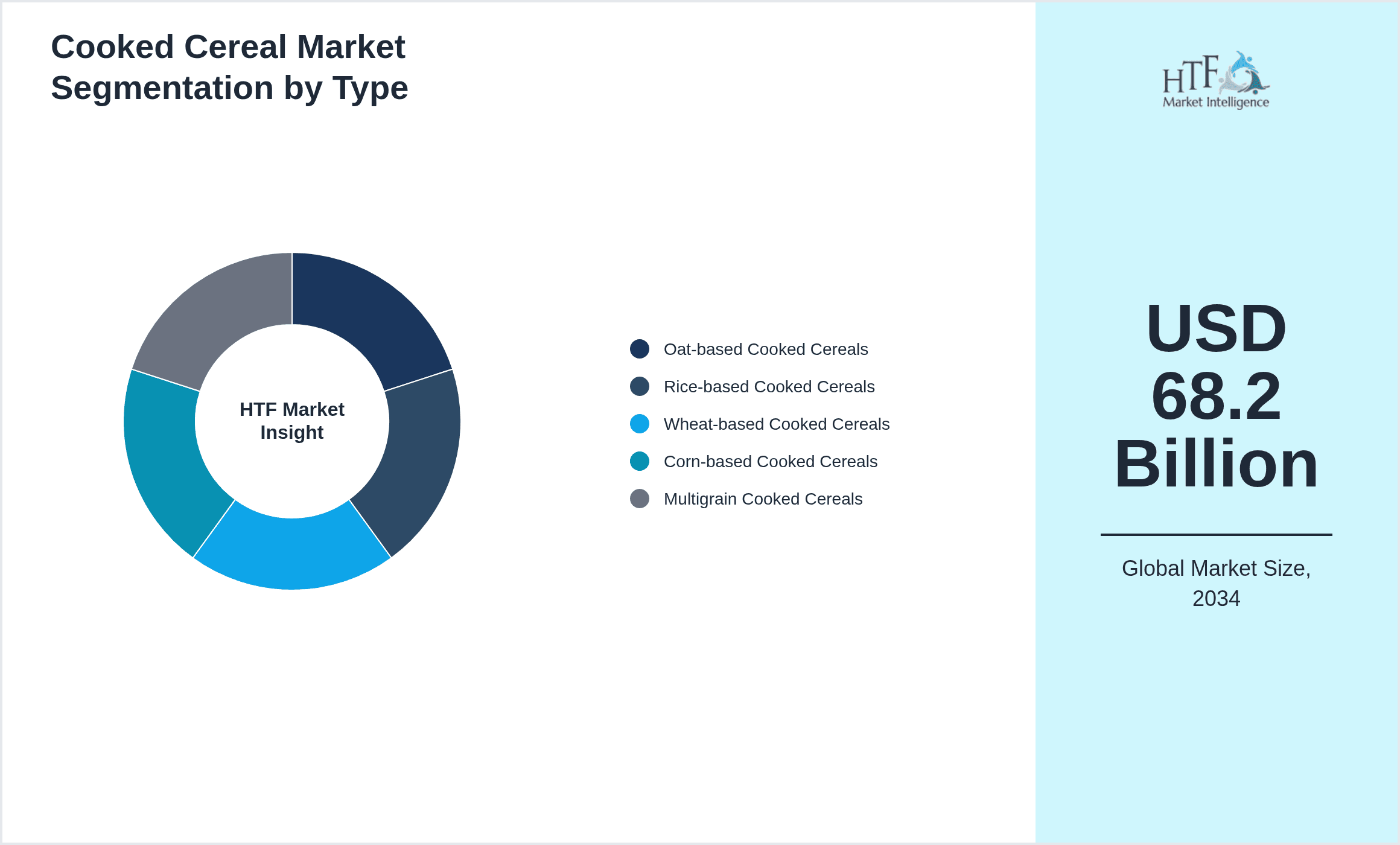

- •By Product Type

- ◦Oat-based Cooked Cereals

- ◦Rice-based Cooked Cereals

- ◦Wheat-based Cooked Cereals

- ◦Corn-based Cooked Cereals

- ◦Multigrain Cooked Cereals

- •By Application

- ◦Breakfast Foods

- ◦Infant Nutrition

- ◦Snack Foods

- ◦Convenience Foods

- ◦Animal Feed

- •By End-Use Industry

- ◦Retail

- ◦Foodservice

- ◦Infant Food Manufacturing

- ◦Animal Feed Production

- •By Distribution Channel

- ◦Supermarkets & Hypermarkets

- ◦Convenience Stores

- ◦Online Retail

- ◦Specialty Stores

Growth Dynamics

- •Rising health awareness globally has significantly bolstered demand for cooked cereals, especially those rich in fiber and essential nutrients, driving product innovation and market expansion. Consumers increasingly prefer oat-based and multigrain products due to their health benefits, which has encouraged manufacturers to diversify offerings.

- •Urbanization and busier lifestyles have accelerated the adoption of convenience foods, including ready-to-eat cooked cereals, fostering growth in the breakfast foods and snack categories. This trend is particularly pronounced in emerging markets within Asia-Pacific and Latin America.

- •Technological advancements in cereal processing, such as extrusion and fortification techniques, have improved product texture, taste, and nutritional value, enabling manufacturers to meet evolving consumer preferences and regulatory standards with enhanced product portfolios.

- •Increasing penetration of e-commerce platforms has expanded distribution channels, providing consumers with easier access to diverse cooked cereal products, and facilitating market growth through direct-to-consumer sales and subscription models.

- •Government initiatives promoting healthy diets and childhood nutrition have stimulated demand for fortified infant nutrition cereals, representing a critical growth driver in both developed and developing regions.

- •The rising demand for gluten-free and organic cooked cereals is influencing product development strategies, with manufacturers investing in sourcing non-GMO and organic raw materials to cater to niche consumer segments.

- •Strategic collaborations and partnerships among key players and ingredient suppliers are enhancing R&D capabilities, enabling faster innovation cycles and expansion into untapped regional markets.

Market Trends

- •The cooked cereal market is witnessing a shift toward clean-label products, with consumers demanding transparency about ingredients, sourcing, and processing methods, prompting companies to reformulate products without artificial additives.

- •Product innovation is increasingly focused on functional cereals enriched with probiotics, vitamins, and minerals, targeting health-conscious consumers seeking added nutritional benefits beyond basic sustenance.

- •Sustainability has become a key theme, with manufacturers adopting eco-friendly packaging and sustainable sourcing practices to reduce carbon footprint and appeal to environmentally conscious buyers.

- •Digital marketing and social media engagement have become critical for brand differentiation, enabling companies to connect directly with consumers and build loyalty through personalized communication and influencer partnerships.

- •The rise of plant-based diets is influencing product portfolios, encouraging the development of cereals that align with vegan and vegetarian lifestyles, broadening market appeal.

- •Emerging markets are experiencing increased demand for fortified and convenient cooked cereals, driven by growing middle-class populations and increasing retail infrastructure development.

- •Cross-category innovation blending cereals with other food products, such as bars and snacks, is creating new consumption occasions and expanding market reach.

Market Opportunities

- •Expanding urban populations in Asia-Pacific and Latin America present significant growth opportunities for manufacturers introducing convenience-focused and health-oriented cooked cereal products tailored to local tastes and preferences.

- •Innovation in multigrain and gluten-free cereal formulations offers potential to capture niche consumer segments seeking specialized dietary options, enhancing market penetration.

- •Investment in digital sales channels and direct-to-consumer platforms can accelerate market reach and consumer engagement, particularly among younger, tech-savvy demographics.

- •Collaborative ventures with agricultural producers to secure sustainable and high-quality raw materials can strengthen supply chains and support premium product development.

- •Opportunities exist in fortifying cereals with emerging superfoods and functional ingredients, aligning with wellness trends and expanding product differentiation.

- •Developing innovative packaging solutions that enhance product shelf life and convenience can improve consumer experience and reduce waste, fostering brand loyalty.

- •Leveraging data analytics and consumer insights to tailor product offerings regionally can optimize marketing strategies and increase market share in diverse geographic segments.

Market Challenges

- •Fluctuations in raw material prices, particularly cereal grains, pose significant cost pressures on manufacturers, impacting profitability and pricing strategies.

- •Stringent regulatory requirements related to food safety, labeling, and fortification standards vary globally, creating compliance complexities and potential market entry barriers.

- •High competition and market saturation in developed regions necessitate continuous innovation and marketing investments to maintain consumer interest and brand loyalty.

- •Supply chain disruptions, including logistics challenges and geopolitical tensions, can affect raw material availability and distribution efficiency, limiting market growth temporarily.

- •Consumer skepticism regarding processed food products may hinder adoption of certain cooked cereals, requiring enhanced transparency and education efforts from manufacturers.

- •Environmental concerns related to agricultural practices and packaging waste are prompting calls for more sustainable industry practices, which may increase operational costs.

- •Balancing affordability with premium product features remains a challenge, especially in price-sensitive emerging markets where cost competitiveness drives purchasing decisions.

Regulatory Framework

- •The Food Safety Modernization Act (FSMA) enacted in the United States between 2011 and 2025 imposes rigorous standards on food manufacturing practices, including cooked cereals, enhancing safety but increasing compliance costs. It mandates preventive controls and supply chain oversight to reduce contamination risks.

- •The European Union's Food Information to Consumers Regulation (EU FIC), updated through 2020-2025, requires transparent labeling of allergens, nutritional information, and ingredient origin, influencing product formulation and packaging within the cooked cereal market.

- •Codex Alimentarius standards established by the FAO and WHO provide international guidelines for cereal products, including fortification levels and hygiene protocols, facilitating global trade while ensuring consumer safety and product quality.

- •China's National Food Safety Standard revisions from 2018 to 2025 include specific regulations on infant cereals and fortified foods, impacting product formulations and market entry strategies for global players targeting the region.

- •Government initiatives in emerging markets such as India’s Food Safety and Standards Authority (FSSAI) programs promote nutritional fortification and quality assurance, encouraging development of healthier cooked cereal products aligned with public health objectives.

Market Intelligence

- •15th March 2025, Kellogg Company launched its new line of organic multigrain cooked cereals featuring enhanced fiber content and natural sweeteners, targeting health-conscious consumers in North America and Asia-Pacific. The product emphasizes clean-label ingredients and sustainable sourcing, aiming to capture the growing demand for functional breakfast options. Kellogg’s strategic marketing campaign includes digital outreach and retail partnerships to maximize market penetration. This launch aligns with global trends favoring organic and high-fiber foods, positioning Kellogg competitively for the forecast period. Source: Kellogg Company Official Press Release

- •10th June 2025, Nestlé S.A. introduced a fortified rice-based cooked cereal enriched with essential vitamins and minerals designed specifically for infant nutrition markets in Latin America and Middle East & Africa. The product addresses regional nutritional deficiencies and complies with local regulatory standards for infant food safety. Nestlé's innovation leverages advanced extrusion technology to enhance digestibility and taste, supported by clinical trials. The launch marks Nestlé’s commitment to improving childhood nutrition globally, with expansion plans across emerging markets. Source: Nestlé Corporate Communications

- •22nd September 2025, General Mills, Inc. announced a strategic partnership with agricultural cooperative groups in Asia-Pacific to secure sustainable oat supplies for its cooked cereal product lines. This initiative aims to ensure raw material quality, reduce environmental impact, and support local farming communities. It also facilitates the development of region-specific products tailored to local consumer preferences. The partnership exemplifies growing industry focus on sustainability and supply chain resilience amid increasing raw material cost volatility. Source: General Mills Investor Relations

- •5th December 2025, Post Holdings, Inc. completed the acquisition of a leading organic cereal manufacturer based in Europe, expanding its product portfolio and strengthening market presence in the health and wellness segment. The acquisition enables Post Holdings to leverage advanced manufacturing technologies and distribution networks to accelerate growth. This consolidation reflects broader industry trends toward mergers and acquisitions aimed at enhancing competitive positioning and innovation capabilities in the global cooked cereal market. Source: Post Holdings Press Release

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 35.8 Billion |

| Forecast Year Market Size | USD 68.2 Billion |

| CAGR | 7.6% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7.4% |

| Scope of Report | Market is segmented by Product Type (Oat-based Cooked Cereals, Rice-based Cooked Cereals, Wheat-based Cooked Cereals, Corn-based Cooked Cereals, Multigrain Cooked Cereals), Application (Breakfast Foods, Infant Nutrition, Snack Foods, Convenience Foods, Animal Feed), End-Use Industry (Retail, Foodservice, Infant Food Manufacturing, Animal Feed Production), Distribution Channel (Supermarkets & Hypermarkets, Convenience Stores, Online Retail, Specialty Stores) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Kellogg Company (United States), General Mills, Inc. (United States), Nestlé S.A. (Switzerland), PepsiCo, Inc. (United States), Post Holdings, Inc. (United States), Archer Daniels Midland Company (United States), Quaker Oats Company (United States), The Hain Celestial Group, Inc. (United States), Associated British Foods plc (United Kingdom), Weetabix Limited (United Kingdom), B&G Foods, Inc. (United States), Mornflake Oats Ltd (United Kingdom), Nature’s Path Foods, Inc. (Canada), Bob’s Red Mill Natural Foods, Inc. (United States), Post Consumer Brands (United States), Ebro Foods, S.A. (Spain), Fonterra Co-operative Group Limited (New Zealand), Cargill, Incorporated (United States), SunOpta Inc. (Canada), Peet’s Coffee (United States), General Mills Canada Corporation (Canada), Kashi Company (United States), MGP Ingredients, Inc. (United States), Nature's Path Organic Foods Inc. (Canada), Bell Plantation (United States) |

Global Cooked Cereal Market Size, Growth & Revenue 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.