Global Stop-Start-System Market Size, Growth & Revenue 2024-2034

Global Stop-Start-System Market is segmented by Product Type (Integrated Stop-Start System, Belt-Driven Stop-Start System, Integrated Starter Generator, Micro Hybrid, Mild Hybrid), Application (Passenger Cars, Commercial Vehicles, Two-Wheelers, Off-Highway Vehicles, Electric Vehicles), End-Use Industry (Automotive OEMs, Aftermarket, Fleet Operators, Rental and Leasing Companies), Distribution Channel (OEM Supply, Aftermarket Retail, Online Sales), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global Stop-Start-System market represents an essential segment of the automotive industry's efforts to improve fuel efficiency and reduce emissions. These systems automatically switch off the engine when the vehicle is stationary and restart it when the driver intends to move, contributing to lower fuel consumption and pollutant output. The market includes a wide variety of technologies, from belt-driven systems to advanced integrated starter generators and micro hybrid solutions, catering to passenger cars, commercial vehicles, two-wheelers, and emerging electric vehicle segments. As regulatory frameworks tighten worldwide, adoption of stop-start technologies has accelerated, especially in regions with stringent emission norms. Key applications span urban commuting, commercial logistics, and specialized off-highway vehicles, underscoring the broad utility of these systems. The market's growth is driven by increasing environmental awareness, government incentives, and rising fuel prices, which collectively encourage automakers to integrate these systems. Market players are focusing on innovation, strategic partnerships, and regional expansion to capitalize on emerging opportunities globally. The competitive landscape is marked by intense rivalry among established automotive component manufacturers and new entrants focusing on micro hybrid and mild hybrid technologies.

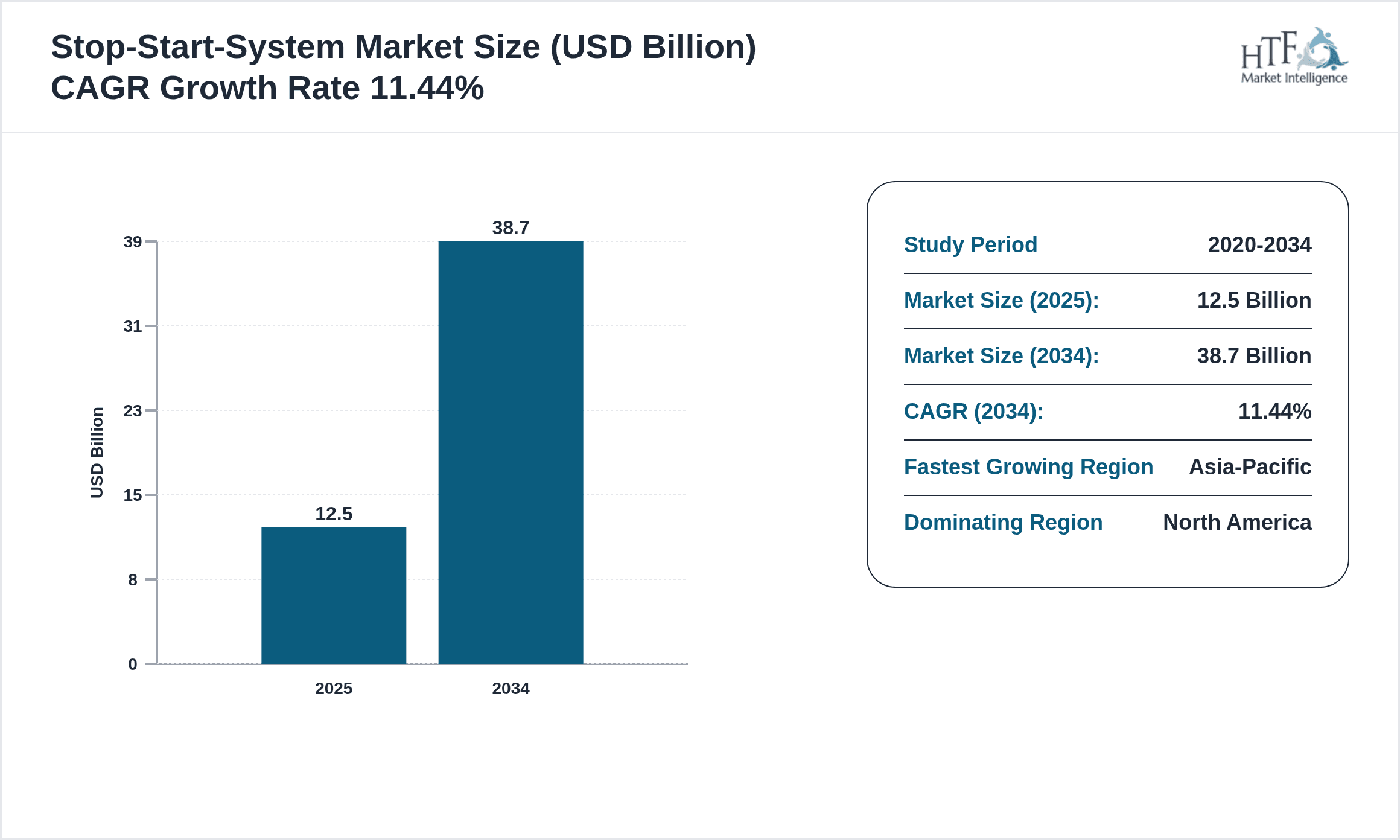

- •Market highlights include a robust CAGR of 11.44% projected from 2024 to 2034, with the global market size expected to grow from USD 12.5 Billion in 2024 to USD 38.7 Billion by 2034. North America currently dominates the market owing to early adoption and regulatory support, while Asia-Pacific is the fastest-growing region driven by rising vehicle production and urbanization. Integrated stop-start systems hold the largest market share due to their efficiency and widespread application, whereas micro hybrid systems are gaining traction as the fastest-growing product type. Key industry players are investing in research and development to enhance system reliability and reduce costs, ensuring market penetration across various vehicle segments.

- •The stop-start system market offers significant value to automotive manufacturers, environmental regulators, and consumers by enabling substantial reductions in fuel consumption and carbon emissions. The technology aligns with global sustainability goals and helps manufacturers meet tightening emission standards, creating a strategic imperative for adoption. Additionally, the market supports innovation in hybrid electric vehicles and contributes to the broader transition towards greener transportation solutions. Stakeholders benefit from the integration of advanced electronics and control systems that improve vehicle performance and user experience while maintaining regulatory compliance. Overall, the market's growth prospects make it a crucial area of focus for industry players and policymakers alike.

Competitive Landscape

The global stop-start-system market is characterized by a highly competitive environment with numerous established automotive component manufacturers and emerging technology firms vying for market share. Competitors focus heavily on innovation, particularly in enhancing system integration, reliability, and cost-effectiveness to meet diverse vehicle requirements worldwide. Strategic partnerships and collaborations with automakers are common to accelerate technology adoption and tailor solutions to specific vehicle platforms. Market rivalry also extends to the development of micro hybrid and mild hybrid technologies, which offer incremental benefits in fuel savings and emission reductions. Pricing strategies vary, with companies balancing affordability and advanced features to appeal to different customer segments. Distribution channels include OEM supply agreements and aftermarket service providers, broadening the market reach. Barriers to entry include high R&D costs, stringent regulatory compliance, and the need for extensive validation. Regional competition is influenced by local emission standards and vehicle production volumes, with Asia-Pacific emerging as a hotspot for rapid growth and innovation. Future competitive trends indicate increased emphasis on software-driven control systems and integration with electrification technologies.

Prominent Players in Stop-Start-System Market

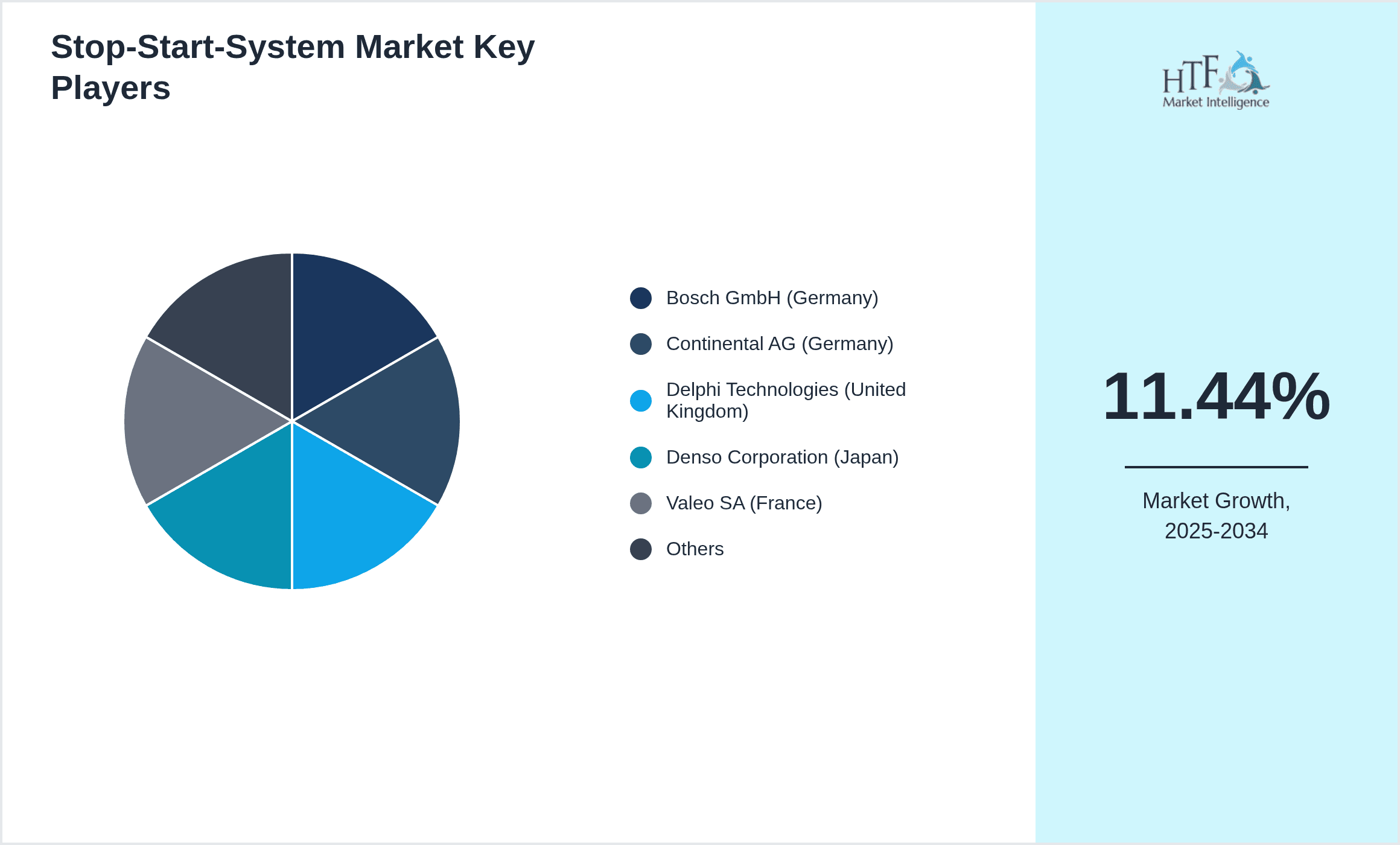

- •Bosch GmbH (Germany)

- •Continental AG (Germany)

- •Delphi Technologies (United Kingdom)

- •Denso Corporation (Japan)

- •Valeo SA (France)

- •Johnson Controls International (United States)

- •Magneti Marelli S.p.A. (Italy)

- •Hyundai Mobis (South Korea)

- •Hitachi Automotive Systems (Japan)

- •ZF Friedrichshafen AG (Germany)

- •Mitsubishi Electric Corporation (Japan)

- •Lear Corporation (United States)

- •Robert Bosch Engineering and Business Solutions (India)

- •Autoliv Inc. (Sweden)

- •Faurecia (France)

- •Aisin Seiki Co., Ltd. (Japan)

- •NGK Spark Plug Co., Ltd. (Japan)

- •Valeo Siemens eAutomotive (Germany)

- •BorgWarner Inc. (United States)

- •Mahle GmbH (Germany)

- •Delphi Automotive PLC (United Kingdom)

- •Calsonic Kansei Corporation (Japan)

- •Hitachi Automotive Systems Americas, Inc. (United States)

- •Johnson Matthey (United Kingdom)

- •Tenneco Inc. (United States)

Market Breakdown

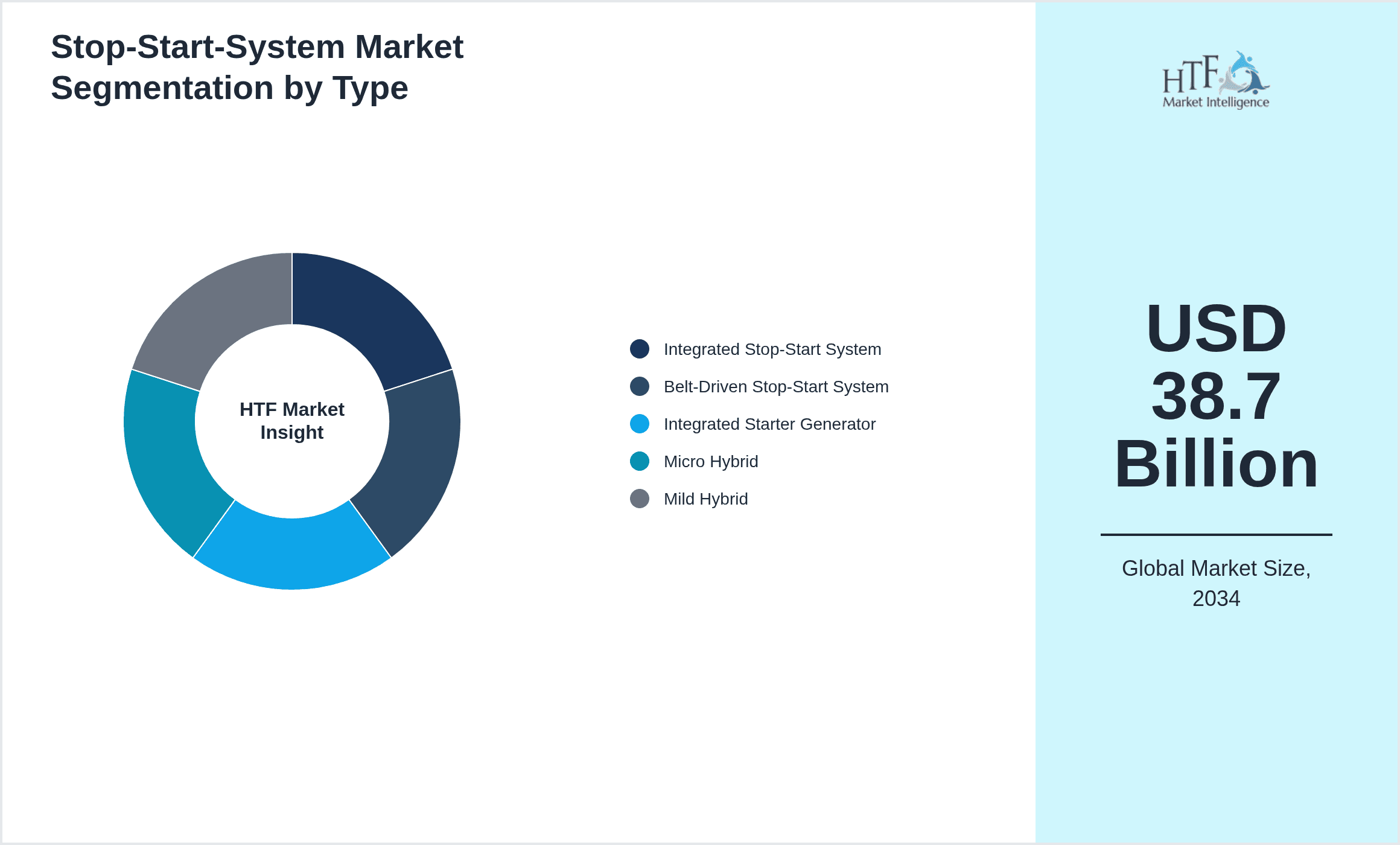

- •By Product Type

- ◦Integrated Stop-Start System

- ◦Belt-Driven Stop-Start System

- ◦Integrated Starter Generator

- ◦Micro Hybrid

- ◦Mild Hybrid

- •By Application

- ◦Passenger Cars

- ◦Commercial Vehicles

- ◦Two-Wheelers

- ◦Off-Highway Vehicles

- ◦Electric Vehicles

- •By End-Use Industry

- ◦Automotive OEMs

- ◦Aftermarket

- ◦Fleet Operators

- ◦Rental and Leasing Companies

- •By Distribution Channel

- ◦OEM Supply

- ◦Aftermarket Retail

- ◦Online Sales

Growth Dynamics

- •Increasing governmental regulations on vehicular emissions globally act as a primary growth driver for the stop-start-system market. For example, stricter CO2 emission targets in regions like Europe and North America necessitate the adoption of fuel-efficient technologies, boosting market demand.

- •Rising fuel prices worldwide encourage automotive manufacturers and consumers to adopt stop-start systems to reduce fuel consumption, making these systems economically attractive over the vehicle lifecycle.

- •Advancements in micro hybrid technology and integration with electric powertrains provide significant potential for growth, enabling manufacturers to meet both environmental standards and consumer expectations for efficiency.

- •Urbanization and increased traffic congestion in emerging markets are driving demand for stop-start systems, as vehicles frequently idle in traffic, where these systems can provide maximum fuel savings and emission reductions.

- •Investment in R&D by leading automotive suppliers to enhance system reliability and reduce costs is facilitating wider adoption across diverse vehicle segments and geographic regions.

- •Government subsidies and incentives for hybrid and fuel-efficient vehicles in various countries stimulate market growth by lowering the cost barriers associated with stop-start technology integration.

- •Consumer awareness and demand for environmentally friendly vehicles are increasing, contributing to the adoption of stop-start systems as a visible and effective fuel-saving feature.

Market Trends

- •Integration of stop-start systems with advanced driver assistance systems (ADAS) is a growing trend, enabling seamless engine control and improved vehicle safety and efficiency.

- •The emergence of micro hybrid vehicles, which incorporate stop-start technology with mild electric assist, is growing rapidly as a cost-effective solution for emission reduction.

- •Automakers are increasingly offering stop-start systems as standard in new vehicle models across various segments to comply with regulatory requirements and customer demand.

- •Sustainability and green mobility initiatives are driving innovation in stop-start technology, including the use of lightweight components and improved battery systems for better performance.

- •Strategic collaborations between technology providers and automotive manufacturers are accelerating the development and deployment of next-generation stop-start solutions.

- •The trend towards electrification is integrating stop-start technology with hybrid and electric drivetrains, creating multi-functional energy management systems for vehicles.

- •Growing aftermarket demand for retrofit stop-start systems is observed, particularly in regions with older vehicle fleets seeking emission and fuel savings improvements.

Market Opportunities

- •Expansion into emerging markets with growing vehicle production and increasing regulatory pressure offers significant growth potential for stop-start system manufacturers.

- •Development of cost-effective micro hybrid systems tailored for two-wheelers and commercial vehicles presents untapped market segments with high adoption potential.

- •Innovating in battery technologies and energy recovery systems integrated with stop-start functions can enhance system efficiency and attract OEM interest.

- •Partnerships with electric vehicle manufacturers to integrate stop-start capabilities in hybrid platforms can expand the market footprint.

- •Aftermarket retrofit solutions for stop-start systems targeting older vehicles is an emerging opportunity supported by environmental regulations and fuel economy concerns.

- •Leveraging digitalization and IoT for smart engine management and predictive maintenance can improve system reliability and customer satisfaction.

- •Government incentives for hybrid vehicle adoption in developing economies can be capitalized upon through localized production and cost optimization strategies.

Market Challenges

- •High initial system costs and integration complexity remain significant barriers for widespread adoption, particularly in cost-sensitive vehicle segments and emerging markets.

- •Technical challenges related to battery durability, system reliability, and seamless engine restart can impact consumer acceptance and require continuous innovation.

- •Lack of uniform global regulations and varying emission standards complicate product development and marketing strategies across regions.

- •Consumer reluctance due to perceived inconvenience or safety concerns with frequent engine restarts can limit market penetration.

- •Competition from alternative fuel-efficient technologies such as full hybrid and electric powertrains may reduce the relative attractiveness of stop-start systems.

- •Supply chain disruptions and raw material price volatility can increase production costs and affect timely delivery of stop-start components.

- •Challenges in educating end-users and aftersales service providers about system benefits and maintenance requirements hinder market expansion.

Regulatory Framework

- •Between 2019 and 2024, multiple regions implemented stringent CO2 emission standards such as the European Union's Euro 6d regulations and the U.S. EPA Tier 3 standards, mandating significant reductions in vehicle emissions and encouraging the adoption of stop-start systems.

- •In 2021, China introduced the China 6 emission norm, which aligns closely with Euro 6 standards, pushing local manufacturers to integrate stop-start and hybrid technologies to comply with environmental targets.

- •Safety regulations enacted in North America and Europe require stop-start systems to meet rigorous engine restart and vehicle performance criteria to ensure driver safety and reliability.

- •Government incentive programs such as tax rebates and subsidies for hybrid and fuel-efficient vehicles have been implemented across Asia-Pacific and Europe between 2020 and 2024, promoting stop-start system integration.

- •New regulations introduced in 2023 in Latin America focus on reducing urban air pollution through mandatory fuel efficiency improvements, indirectly boosting stop-start system demand in the automotive sector.

Market Intelligence

- •15th February 2025, Bosch GmbH launched an advanced integrated stop-start system featuring enhanced battery management and faster engine restart capabilities. This system targets passenger cars and light commercial vehicles aiming to meet upcoming emission regulations in Europe and North America. The product incorporates intelligent control algorithms that optimize fuel savings without compromising driver comfort. Bosch’s strategic objective is to expand its market share in the rapidly growing micro hybrid segment by offering cost-effective and reliable solutions. This launch positions Bosch competitively against other global suppliers while addressing rising consumer demand for fuel-efficient technologies. Source: Official Bosch Press Release

- •10th March 2025, Continental AG introduced a belt-driven stop-start system optimized for two-wheelers and small commercial vehicles in Asia-Pacific markets. The innovation integrates lightweight materials and a compact design, reducing system weight by 15% compared to previous models. Continental aims to capitalize on increasing urbanization and traffic congestion in the region by providing affordable fuel-saving solutions. The product’s market positioning emphasizes cost efficiency and ease of integration with existing vehicle platforms, appealing to OEMs looking to meet stringent emission norms. This development is expected to accelerate system adoption in emerging economies. Source: Continental Corporate Announcement

- •5th January 2025, Denso Corporation announced a strategic partnership with a leading electric vehicle manufacturer to co-develop integrated starter generator technology for mild hybrid applications. This collaboration seeks to combine Denso’s engineering expertise with the partner’s electric powertrain innovations to enhance vehicle efficiency and reduce emissions. The initiative includes joint R&D efforts and shared manufacturing facilities to expedite product commercialization by 2026. The partnership reflects growing industry trends towards electrification and hybridization, reinforcing Denso’s market position in advanced automotive technologies. Expected impacts include improved system performance and expanded market reach across Asia-Pacific and Europe. Source: Denso Corporate Website

- •20th April 2025, Valeo SA completed the acquisition of a specialized micro hybrid technology firm, strengthening its portfolio of stop-start and energy management solutions. This deal enhances Valeo’s capability to deliver innovative, cost-effective systems that meet evolving regulatory requirements globally. The acquisition supports Valeo’s growth strategy focused on sustainable mobility and expanding presence in emerging markets such as Latin America and Middle East & Africa. Integration of the new technology is anticipated to improve system reliability and reduce production costs, enabling competitive pricing. Valeo aims to leverage synergies across R&D and supply chain operations to accelerate time-to-market for new products. Source: Valeo Official Press Release

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 12.5 Billion |

| Forecast Year Market Size | USD 38.7 Billion |

| CAGR | 11.44% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 11.44% |

| Scope of Report | Market is segmented by Product Type (Integrated Stop-Start System, Belt-Driven Stop-Start System, Integrated Starter Generator, Micro Hybrid, Mild Hybrid), Application (Passenger Cars, Commercial Vehicles, Two-Wheelers, Off-Highway Vehicles, Electric Vehicles), End-Use Industry (Automotive OEMs, Aftermarket, Fleet Operators, Rental and Leasing Companies), Distribution Channel (OEM Supply, Aftermarket Retail, Online Sales) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Bosch GmbH (Germany), Continental AG (Germany), Delphi Technologies (United Kingdom), Denso Corporation (Japan), Valeo SA (France), Johnson Controls International (United States), Magneti Marelli S.p.A. (Italy), Hyundai Mobis (South Korea), Hitachi Automotive Systems (Japan), ZF Friedrichshafen AG (Germany), Mitsubishi Electric Corporation (Japan), Lear Corporation (United States), Robert Bosch Engineering and Business Solutions (India), Autoliv Inc. (Sweden), Faurecia (France), Aisin Seiki Co., Ltd. (Japan), NGK Spark Plug Co., Ltd. (Japan), Valeo Siemens eAutomotive (Germany), BorgWarner Inc. (United States), Mahle GmbH (Germany), Delphi Automotive PLC (United Kingdom), Calsonic Kansei Corporation (Japan), Hitachi Automotive Systems Americas, Inc. (United States), Johnson Matthey (United Kingdom), Tenneco Inc. (United States) |

Global Stop-Start-System Market Size, Growth & Revenue 2024-2034 - Table of Contents

Research enthusiast focused on transforming data uncovering into actionable insights through data-driven decision-making.

Frequently Asked Questions (FAQ):

The Market market is expected to see significant growth and value in 2025.

North America currently leads the market, followed by Europe and Asia-Pacific.

Key growth drivers include increasing activities, rising demand for innovative solutions, technological advancements, and growing preference for efficient products.