Global Alloy Aluminum Forged Wheel Market Size, Growth & Revenue 2024-2034

Global Alloy Aluminum Forged Wheel Market is segmented by Product Type (Monoblock Forged Wheels, Multi-piece Forged Wheels, Flow Forged Wheels, Hybrid Forged Wheels, Custom Forged Wheels), Application (Passenger Cars, Commercial Vehicles, Sports Vehicles, Luxury Vehicles, Off-Road Vehicles), End-Use Industry (Automotive OEM, Aftermarket, Motorsports, Commercial Fleet Operators), Distribution Channel (Direct OEM Sales, Authorized Dealerships, Online Retail, Specialty Wheel Shops), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global alloy aluminum forged wheel market serves as a vital segment within the automotive supply chain, focusing on the production and application of lightweight, durable wheels that enhance vehicle efficiency and performance. This market includes various forging technologies applied to aluminum alloys to produce wheels with superior strength-to-weight ratios compared to conventional cast wheels. Applications span passenger vehicles, commercial trucks, sports cars, luxury automobiles, and off-road vehicles, reflecting broad industry relevance. The market is characterized by innovation in forging techniques such as monoblock forging, flow forging, and hybrid forging, which contribute to improved mechanical properties and aesthetic appeal. Growth is driven by rising demand for fuel-efficient and performance-optimized vehicles, stringent emission regulations, and the global shift toward electric and hybrid vehicle adoption. Competitive dynamics involve key automotive component manufacturers investing in R&D and strategic collaborations to enhance product portfolios and geographic reach. This comprehensive market integrates OEM and aftermarket channels, reflecting evolving consumer preferences and technological progress over the forecast period.

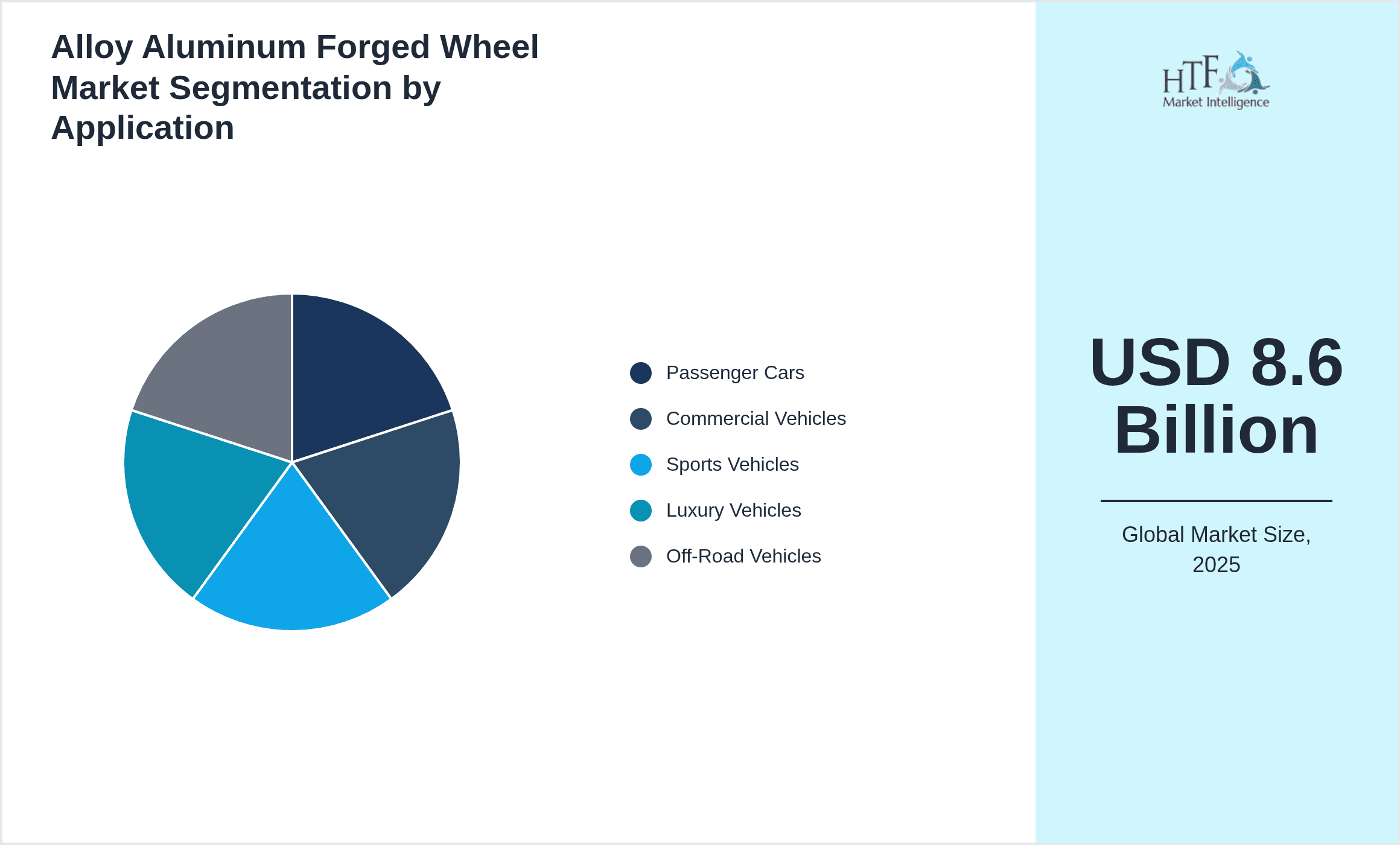

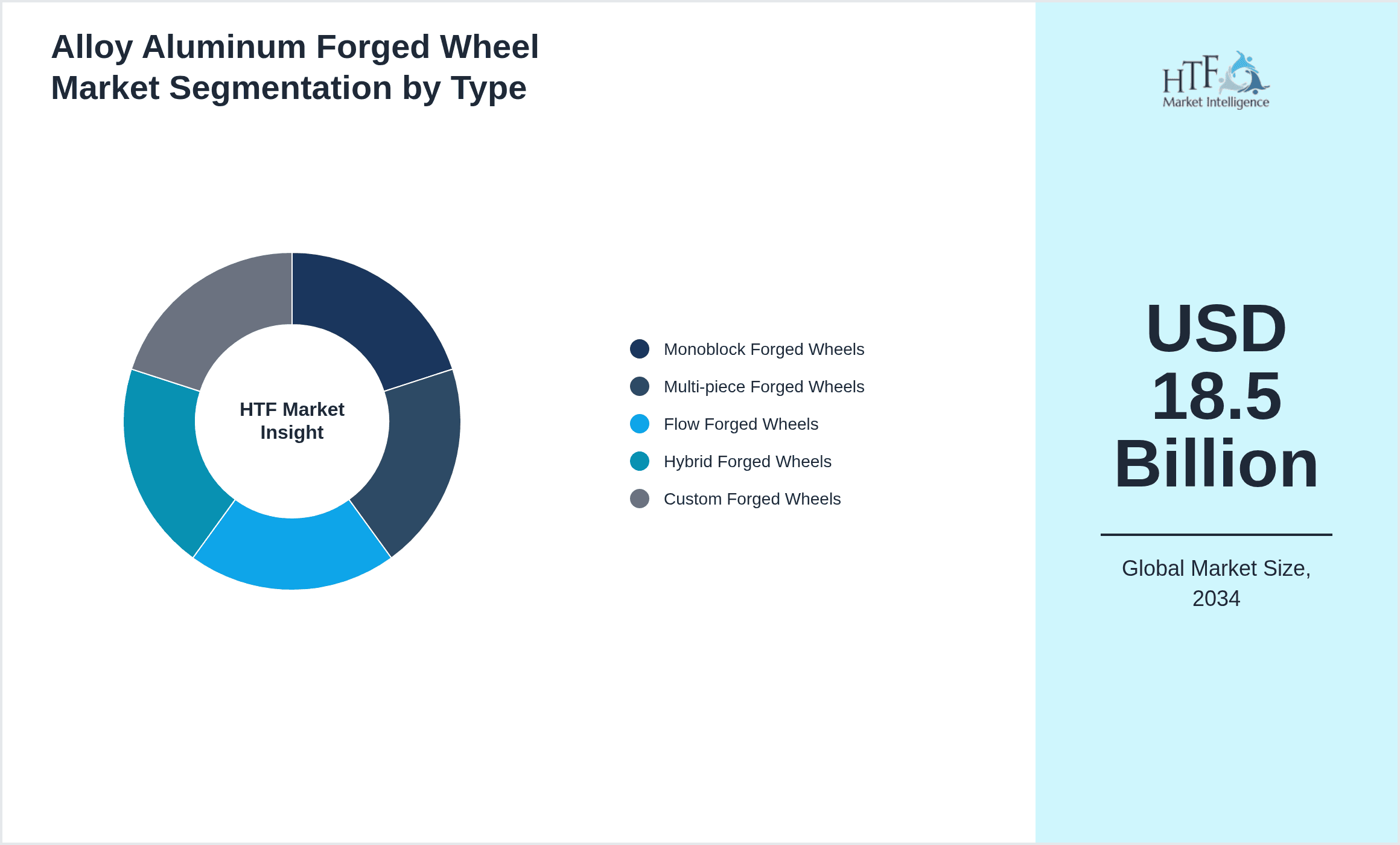

- •Key market highlights include a base market size of USD 8.6 billion in 2024 with a projected growth to USD 18.5 billion by 2034, representing a robust CAGR of 7.7%. North America currently dominates due to advanced automotive manufacturing infrastructure and high adoption of premium vehicles, while Asia-Pacific is the fastest-growing region driven by expanding automotive production and increasing consumer demand. Monoblock forged wheels lead the product type segment, favored for their cost-efficiency and performance balance, whereas hybrid forged wheels exhibit the fastest growth due to innovative manufacturing combining multiple forging processes. Passenger cars remain the dominant application segment, supported by increasing personalization trends and aftermarket demand. Market growth is further catalyzed by technological advancements, rising environmental concerns promoting lightweight materials, and the expansion of electric vehicle fleets globally.

- •The alloy aluminum forged wheel market presents strategic value to automotive manufacturers, suppliers, and aftermarket retailers by enabling enhanced vehicle performance, fuel efficiency, and aesthetic appeal. Its growth aligns with the automotive industry's focus on sustainability and lightweight technologies, directly impacting vehicle emissions and operational costs. For stakeholders, including OEMs and tier-1 suppliers, investing in advanced forging technologies and expanding production capacities in high-growth regions offers competitive advantage. Additionally, the aftermarket segment benefits from customization trends and replacement demand, creating diversified revenue streams. Overall, the market's evolution reflects broader automotive industry dynamics, encompassing regulatory pressures, consumer preferences, and innovation, making it a critical area for strategic development and investment through 2034.

Competitive Landscape

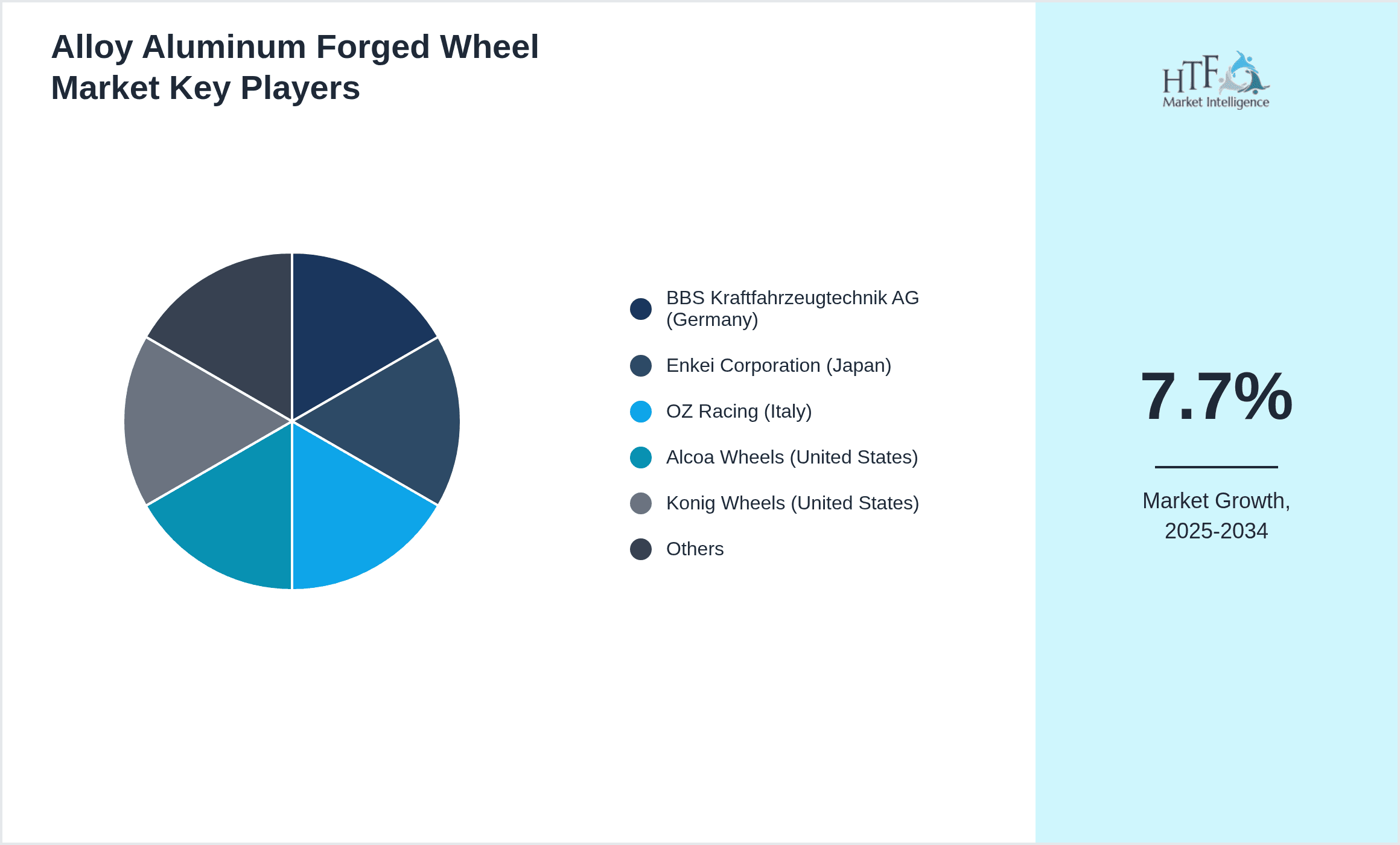

The global alloy aluminum forged wheel market is highly competitive, characterized by a mix of established multinational corporations and regional specialists focusing on innovation, quality, and cost efficiency. Market participants invest heavily in R&D to develop advanced forging techniques that improve wheel strength, reduce weight, and enhance aesthetic appeal, thus differentiating their offerings. Competitive strategies include expanding global manufacturing footprints, forming strategic partnerships with automotive OEMs, and leveraging technological advancements such as flow forging and hybrid forging processes. Rivalry centers on product performance, customization options, and after-sales support, with pricing pressures influenced by raw material costs and supply chain dynamics. Mergers and acquisitions play a significant role in consolidating market share, enabling companies to enhance capacity and technological capabilities. Regional competition is pronounced, especially between North American and Asia-Pacific players, with emerging markets contributing to shifting dynamics. Looking forward, innovation in materials science and integration with electric vehicle platforms will shape competitive advantages and industry structure.

Prominent Players in Alloy Aluminum Forged Wheel Market

- •BBS Kraftfahrzeugtechnik AG (Germany)

- •Enkei Corporation (Japan)

- •OZ Racing (Italy)

- •Alcoa Wheels (United States)

- •Konig Wheels (United States)

- •Momo Srl (Italy)

- •SSR Wheels (Japan)

- •Rays Engineering (Japan)

- •American Racing (United States)

- •Forgeline Motorsports (United States)

- •HRE Performance Wheels (United States)

- •Rotiform Wheels (United States)

- •Vossen Wheels (United States)

- •Fuel Off-Road Wheels (United States)

- •Advanti Racing (Taiwan)

- •TSW Alloy Wheels (United Kingdom)

- •Breyton (Germany)

- •WedsSport (Japan)

- •KMC Wheels (United States)

- •Method Race Wheels (United States)

- •MKW Wheels (United States)

- •American Eagle Wheels (United States)

- •Motegi Racing (United States)

- •Enkei America (United States)

- •SSR Wheels America (United States)

Market Breakdown

- •By Product Type

- ◦Monoblock Forged Wheels

- ◦Multi-piece Forged Wheels

- ◦Flow Forged Wheels

- ◦Hybrid Forged Wheels

- ◦Custom Forged Wheels

- •By Application

- ◦Passenger Cars

- ◦Commercial Vehicles

- ◦Sports Vehicles

- ◦Luxury Vehicles

- ◦Off-Road Vehicles

- •By End-Use Industry

- ◦Automotive OEM

- ◦Aftermarket

- ◦Motorsports

- ◦Commercial Fleet Operators

- •By Distribution Channel

- ◦Direct OEM Sales

- ◦Authorized Dealerships

- ◦Online Retail

- ◦Specialty Wheel Shops

Growth Dynamics

The global alloy aluminum forged wheel market is propelled by increasing demand for lightweight automotive components that enhance fuel efficiency and reduce emissions. Regulatory mandates on vehicle emissions worldwide have accelerated the adoption of forged aluminum wheels due to their superior strength-to-weight ratio compared to traditional steel or cast wheels. Moreover, growing consumer preference for high-performance and luxury vehicles drives demand for aesthetically appealing and durable forged wheels. Technological advancements such as hybrid forging and flow forging processes enable manufacturers to produce wheels with enhanced mechanical properties and custom designs, further expanding market scope. Additionally, the rise in electric and hybrid vehicle production globally supports growth, as these vehicles benefit significantly from weight reduction to enhance battery range. The expanding aftermarket segment also contributes to growth, with consumers seeking customization and replacement wheels. Collectively, these factors create a favorable environment for sustained market expansion through 2034.

Market Trends

The alloy aluminum forged wheel market is witnessing a shift toward advanced manufacturing technologies such as hybrid forging that combine precision and strength with reduced production costs. There is a growing trend of integrating smart manufacturing and automation to improve efficiency and quality control. Customization and personalization trends are strong, with consumers demanding unique designs and finishes, prompting manufacturers to offer bespoke solutions. Sustainability is another prominent trend, with increased use of recycled aluminum and eco-friendly processes. Additionally, the rise of electric vehicles globally is influencing wheel design and material selection to optimize range and performance. Collaborations between automotive OEMs and wheel manufacturers to develop integrated lightweight solutions are becoming more commonplace. These trends collectively reshape the competitive landscape and product development priorities in the forged wheel market.

Market Opportunities

Emerging markets in Asia-Pacific and Latin America present significant growth opportunities due to rapid automotive production expansion and rising consumer purchasing power. There is potential for innovation-driven product differentiation through the development of hybrid forged wheels that offer enhanced performance at competitive costs. The increasing penetration of electric vehicles globally opens avenues for specialized lightweight wheels designed to improve battery efficiency and vehicle range. Expansion of aftermarket channels, including e-commerce platforms, allows manufacturers to reach a broader customer base with customized offerings. Strategic partnerships with automotive OEMs for co-development of wheels tailored to new vehicle models can secure long-term contracts and revenue streams. Additionally, investments in sustainable forging technologies and recycled materials align with evolving regulatory requirements and consumer preferences, creating further competitive advantages and market share growth.

Market Challenges

The alloy aluminum forged wheel market faces challenges related to high production costs compared to cast wheels, limiting affordability for price-sensitive segments. Raw material price volatility, especially in aluminum markets, adds to cost uncertainty and affects profit margins. The complexity of forging processes requires significant capital investment and skilled labor, posing barriers to entry for smaller manufacturers. Additionally, stringent regulatory compliance across different regions necessitates continuous adaptation of manufacturing standards and testing protocols, increasing operational burden. Supply chain disruptions, exacerbated by geopolitical tensions and global events, impact timely material availability and production schedules. Market saturation in developed regions leads to intense competition and pricing pressure. Furthermore, consumer concerns regarding counterfeit or substandard wheels in aftermarket channels pose risks to brand reputation and safety standards, challenging manufacturers to maintain quality assurance and trust.

Regulatory Framework

Between 2019 and 2024, regulatory developments have increasingly focused on vehicle safety and environmental impact, directly influencing the alloy aluminum forged wheel market. Governments worldwide have implemented stricter standards on emissions, prompting automotive manufacturers to adopt lightweight components including forged aluminum wheels to improve fuel efficiency. Safety regulations mandate rigorous testing for wheel durability, load capacity, and impact resistance, requiring manufacturers to comply with international standards such as ISO and SAE certifications. Regions like North America and Europe have introduced updated mandates on material traceability and environmental compliance, encouraging sustainable manufacturing practices. Additionally, regulations promoting recycling and circular economy principles have pushed manufacturers to integrate recycled aluminum in forging processes. These policies collectively shape product design, manufacturing techniques, and supply chain management, ensuring safety, quality, and environmental responsibility within the alloy aluminum forged wheel industry.

Market Intelligence

- •15th January 2024, BBS Kraftfahrzeugtechnik AG launched a new range of lightweight monoblock forged wheels designed specifically for electric vehicles. Featuring advanced forging techniques and optimized aerodynamics, the product enhances EV battery range and performance. The launch targets premium EV manufacturers seeking high-quality, efficient wheel solutions. This innovation underscores BBS's commitment to sustainability and performance in the evolving automotive landscape. Source: Official BBS Press Release

- •22nd September 2023, Enkei Corporation introduced hybrid forged wheels combining multi-piece and flow forging technologies to deliver superior strength and reduced weight. These wheels are aimed at high-performance sports vehicles and luxury cars, offering improved handling and aesthetics. Enkei’s strategic focus on hybrid forging reflects market demand for innovation and customization. Source: Enkei Corporate Announcement

- •10th November 2023, Alcoa Wheels announced a global expansion of its manufacturing capacity with a new facility in Southeast Asia. This move aims to meet rising demand in the Asia-Pacific region and reduce lead times for OEM customers. The investment highlights Alcoa’s strategy to strengthen its global footprint and supply chain resilience. Source: Alcoa Investor Relations

- •3rd March 2024, Forgeline Motorsports completed a strategic partnership with an electric vehicle startup to co-develop custom forged wheels tailored for high-performance EVs. This collaboration combines Forgeline’s manufacturing expertise with the startup’s cutting-edge vehicle designs, targeting niche luxury EV segments. Source: Forgeline Official Website

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 8.6 Billion |

| Forecast Year Market Size | USD 18.5 Billion |

| CAGR | 7.7% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7.5% |

| Scope of Report | Market is segmented by Product Type (Monoblock Forged Wheels, Multi-piece Forged Wheels, Flow Forged Wheels, Hybrid Forged Wheels, Custom Forged Wheels), Application (Passenger Cars, Commercial Vehicles, Sports Vehicles, Luxury Vehicles, Off-Road Vehicles), End-Use Industry (Automotive OEM, Aftermarket, Motorsports, Commercial Fleet Operators), Distribution Channel (Direct OEM Sales, Authorized Dealerships, Online Retail, Specialty Wheel Shops) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | BBS Kraftfahrzeugtechnik AG (Germany), Enkei Corporation (Japan), OZ Racing (Italy), Alcoa Wheels (United States), Konig Wheels (United States), Momo Srl (Italy), SSR Wheels (Japan), Rays Engineering (Japan), American Racing (United States), Forgeline Motorsports (United States), HRE Performance Wheels (United States), Rotiform Wheels (United States), Vossen Wheels (United States), Fuel Off-Road Wheels (United States), Advanti Racing (Taiwan), TSW Alloy Wheels (United Kingdom), Breyton (Germany), WedsSport (Japan), KMC Wheels (United States), Method Race Wheels (United States), MKW Wheels (United States), American Eagle Wheels (United States), Motegi Racing (United States), Enkei America (United States), SSR Wheels America (United States) |

Global Alloy Aluminum Forged Wheel Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.