Global Generator Belt Market Size, Growth & Revenue 2024-2034

Global Generator Belt Market is segmented by Product Type (V-Ribbed Belts, V-Belts, Timing Belts, Flat Belts, Poly-V Belts), Application (Power Generation, Industrial Machinery, Automotive, Agricultural Equipment, Construction Equipment), End-Use Industry (Energy & Utilities, Manufacturing, Transportation, Agriculture), Distribution Channel (OEM, Aftermarket, Online Retail), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

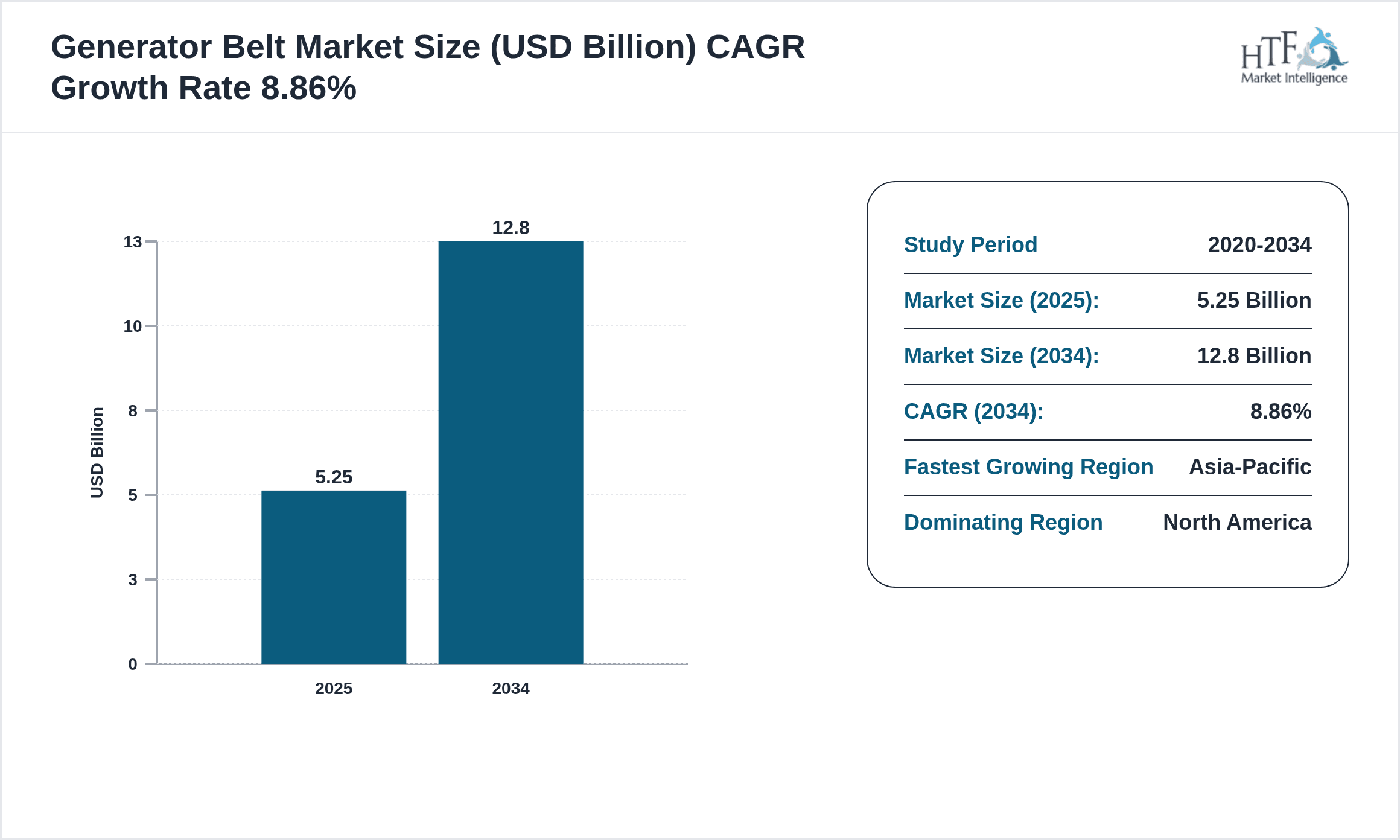

- •The Global Generator Belt Market represents an essential segment within the mechanical power transmission industry, serving a critical function in diverse sectors including power generation, automotive, industrial machinery, agriculture, and construction equipment. These belts are engineered to transfer power from engines or motors to generators efficiently, ensuring reliability and performance under varying operational conditions. The market is segmented by product types such as V-Ribbed belts, V-belts, timing belts, flat belts, and poly-V belts, each tailored to specific applications based on load, speed, and environmental factors. The industry scope spans OEM and aftermarket replacement belts, incorporating advancements in materials like reinforced polymers and improved belt designs that enhance durability and energy efficiency. Growing global industrialization, expanding power generation infrastructure, and rising demand for uninterrupted power supply drive the market’s growth. Moreover, the increasing adoption of renewable energy systems and sophisticated generator technologies are creating new avenues for innovation and expansion. The market’s strategic importance is underscored by its role in optimizing generator performance, reducing downtime, and supporting sustainable energy initiatives worldwide.

- •Key highlights of the Global Generator Belt Market include a projected CAGR of approximately 8.86% from 2024 to 2034, with the market size expected to increase from USD 5.25 billion in 2024 to USD 12.8 billion by 2034. North America currently dominates the market in terms of revenue share, driven by established industrial infrastructure and stringent quality standards. However, the Asia-Pacific region is identified as the fastest-growing market, fueled by rapid industrialization, urbanization, and increased investments in power generation and automotive sectors. V-Ribbed belts lead the product segment due to their versatility and efficiency, while timing belts are experiencing the fastest growth owing to their precision and application in advanced generator systems. Power generation remains the primary application segment, followed closely by industrial machinery. These insights reflect dynamic market trends and suggest robust growth opportunities for manufacturers and stakeholders globally.

- •The generator belt market holds significant strategic value across multiple industries by enabling efficient power transmission and contributing to operational reliability. For power generation companies, these belts ensure uninterrupted electricity supply, critical for both traditional and renewable energy plants. Automotive manufacturers rely on high-performance belts to enhance engine-generator synergy, improving fuel efficiency and reducing emissions. Industrial and agricultural equipment sectors benefit from belts that withstand harsh environments and heavy loads, minimizing maintenance costs and downtime. Stakeholders including manufacturers, distributors, and end-users can leverage market insights to optimize product development, expand geographic reach, and align with evolving regulatory standards. The market's growth trajectory underscores the importance of continuous innovation in belt materials and design, alongside strategic partnerships and investments aimed at capturing emerging demand in fast-expanding regions like Asia-Pacific and Latin America.

Competitive Landscape

The Global Generator Belt Market features a highly competitive environment characterized by a mix of established multinational corporations and agile regional players. Market competition revolves around innovations in belt materials, design enhancements, durability, and energy efficiency to meet stringent industry standards and diverse application needs. Companies employ strategies such as research and development investments, strategic partnerships, and expanding production capacities to strengthen market positioning. Product differentiation through advanced technologies including reinforced composites and precision manufacturing helps maintain competitive advantages. Pricing strategies are influenced by raw material costs and regional economic conditions, while distribution channel optimization ensures timely availability across global markets. The competitive rivalry is intensified by the entry of new players focused on niche applications and emerging markets, compelling incumbents to enhance customer service and after-sales support. Additionally, mergers and acquisitions serve as key mechanisms for consolidating market share and accessing new technologies, thereby shaping the evolving competitive dynamics and fostering sustained market growth.

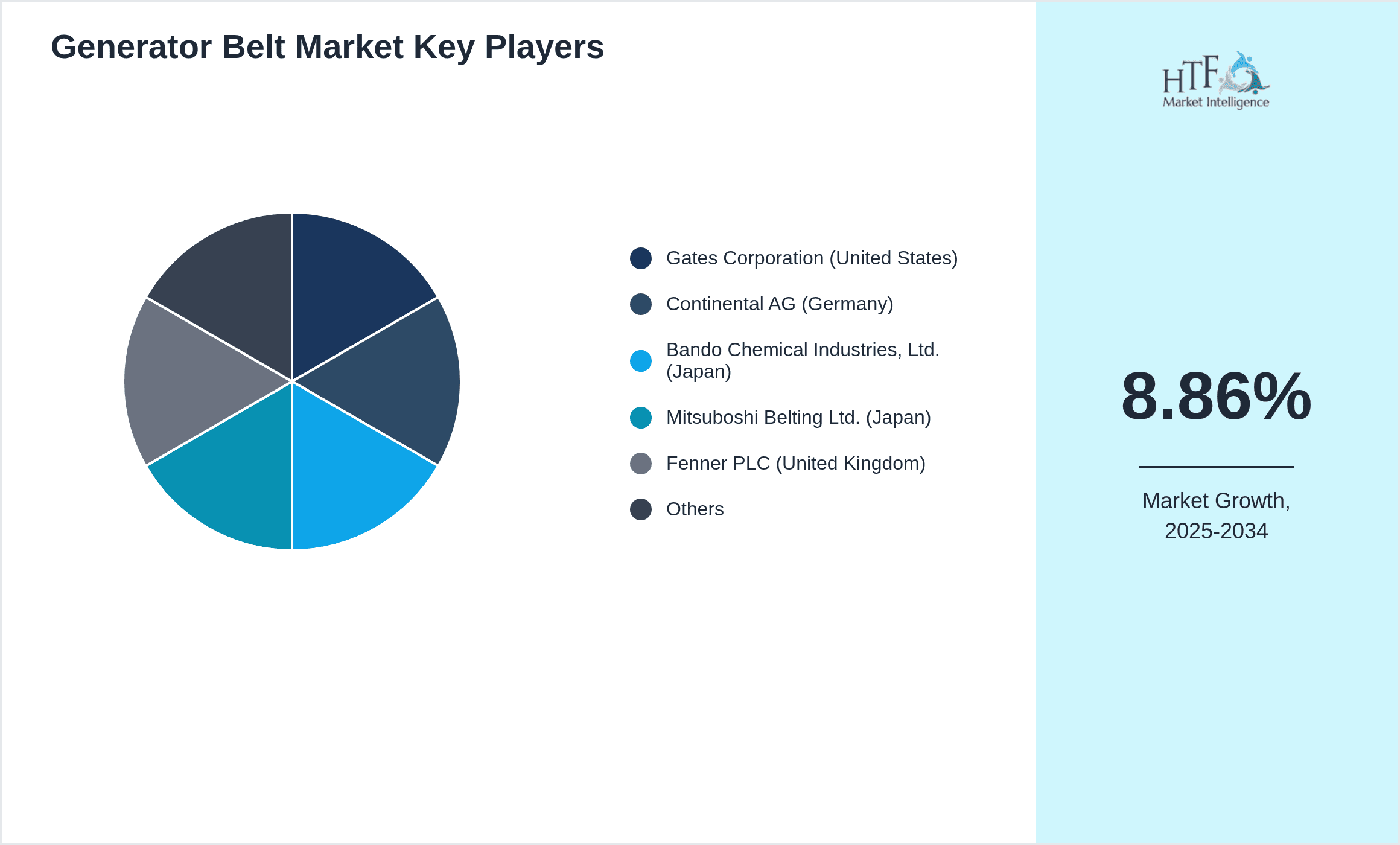

Prominent Players in Generator Belt Market

- •Gates Corporation (United States)

- •Continental AG (Germany)

- •Bando Chemical Industries, Ltd. (Japan)

- •Mitsuboshi Belting Ltd. (Japan)

- •Fenner PLC (United Kingdom)

- •Optibelt Group (Germany)

- •Dayco Products, LLC (United States)

- •Hutchinson SA (France)

- •Magma Belts (India)

- •Apex Industrial Corporation (Taiwan)

- •ContiTech AG (Germany)

- •Morse Industrial Belting (United States)

- •Bando Europe GmbH (Germany)

- •Dayco Europe (Italy)

- •Optibelt USA (United States)

- •Mitsuboshi Belting Europe (Germany)

- •Fenner Dunlop (United Kingdom)

- •Hutchinson North America (United States)

- •Magma Belts Europe (Germany)

- •Apex Belting Europe (France)

- •Bando China (China)

- •Mitsuboshi Belting China (China)

- •Gates India (India)

- •Continental Asia Pacific (Singapore)

- •Fenner Asia Pacific (Singapore)

Market Breakdown

- •By Product Type

- ◦V-Ribbed Belts

- ◦V-Belts

- ◦Timing Belts

- ◦Flat Belts

- ◦Poly-V Belts

- •By Application

- ◦Power Generation

- ◦Industrial Machinery

- ◦Automotive

- ◦Agricultural Equipment

- ◦Construction Equipment

- •By End-Use Industry

- ◦Energy & Utilities

- ◦Manufacturing

- ◦Transportation

- ◦Agriculture

- •By Distribution Channel

- ◦OEM

- ◦Aftermarket

- ◦Online Retail

Growth Dynamics

The Global Generator Belt Market is propelled by robust industrial expansion and escalating demand for reliable power generation solutions worldwide. Increasing infrastructure developments and the rapid growth of automotive and agricultural sectors fuel the need for durable and efficient generator belts. Technological advancements in belt materials, such as the integration of reinforced polymers and heat-resistant composites, have significantly enhanced belt longevity and performance, driving adoption across diverse applications. Furthermore, the growing focus on renewable energy projects, including wind and solar power generators, has created new demand streams for specialized belts capable of withstanding variable operational stresses. Investment in modernization and maintenance of existing power plants also contributes to sustained market growth. These factors, combined with rising awareness of energy efficiency and stringent regulatory standards, ensure continuous innovation and expansion opportunities for market participants globally.

Market Trends

The market is witnessing a trend towards the adoption of high-performance timing belts in advanced generator systems due to their precision and minimal slippage characteristics. Manufacturers are increasingly integrating smart belt technologies embedded with sensors to monitor wear and performance in real-time, enhancing predictive maintenance capabilities. Sustainable and eco-friendly belt materials are gaining traction, aligning with global environmental regulations and corporate sustainability goals. The shift towards digitalization in supply chains and aftermarket services is improving product availability and customer engagement. Additionally, strategic collaborations between belt manufacturers and generator OEMs are on the rise, aiming to develop customized solutions tailored to specific industry requirements. These trends collectively contribute to the evolution of the generator belt market towards higher efficiency, reliability, and sustainability.

Market Opportunities

Emerging economies present significant growth opportunities for generator belt manufacturers due to expanding industrialization and increasing power infrastructure investments. The rise of renewable energy installations offers a niche for specialized belts designed for wind turbines and solar generators, where durability and precision are critical. Opportunities also exist in the aftermarket segment as aging power plants and machinery require regular maintenance and replacement parts. Technological innovation in belt materials, such as self-lubricating and heat-resistant compounds, can open new application areas and improve product differentiation. Furthermore, digital platforms enabling direct engagement with end-users facilitate market penetration and customer loyalty. Strategic partnerships and acquisitions aimed at integrating complementary technologies can accelerate growth and expand global reach.

Market Challenges

The generator belt market faces challenges including volatility in raw material prices, which impacts manufacturing costs and pricing strategies. Technical limitations in achieving optimal belt durability without compromising flexibility can restrict performance in extreme operating conditions. The market also contends with the threat of counterfeit and low-quality products, especially in emerging regions, affecting brand reputation and customer trust. Regulatory compliance across different geographies imposes additional costs and complexity for manufacturers. Furthermore, intense competition from regional players and alternative power transmission technologies requires continuous innovation and investment. Supply chain disruptions caused by geopolitical tensions or global crises can hinder timely product delivery and escalate costs, posing risks to market stability.

Regulatory Framework

Between 2019 and 2024, global regulatory bodies have introduced stringent standards focusing on product safety, environmental impact, and energy efficiency for generator belts. Regulations such as REACH in Europe mandate the restriction of hazardous substances in manufacturing, compelling companies to adopt eco-friendly materials and processes. Safety standards require rigorous testing for mechanical strength and operational reliability, influencing product design and quality assurance protocols. Governments in North America and Asia-Pacific have implemented incentive programs promoting the adoption of energy-efficient and sustainable components in power generation equipment. These regulatory frameworks drive innovation towards greener technologies and enforce compliance through certifications and periodic audits. Manufacturers must navigate diverse regional policies to ensure market access and maintain competitive advantage, emphasizing the importance of proactive regulatory monitoring and adaptation strategies.

Market Intelligence

- •15 March 2025, Gates Corporation launched a new range of high-performance timing belts engineered for enhanced durability in renewable energy generators. These belts feature advanced polymer composites that withstand extreme temperature variations and mechanical stress, targeting wind and solar power applications. The initiative aims to support the growing demand for sustainable energy infrastructure with reliable power transmission components. Gates' strategic objective is to strengthen its position in the green energy sector by offering innovative, long-lasting solutions that reduce maintenance costs and improve operational efficiency. This product launch is expected to accelerate market adoption of eco-friendly belts and reinforce customer loyalty through superior performance.

- •10 January 2025, Continental AG introduced a smart belt system embedded with IoT sensors capable of real-time monitoring of belt wear and load conditions. This innovation enables predictive maintenance and reduces unexpected downtime in industrial and power generation applications. Continental's market positioning focuses on integrating digital technologies to enhance operational reliability and extend belt lifecycle. The smart belt system aligns with Industry 4.0 trends and offers a competitive edge by providing actionable data insights to end-users. Adoption of this technology is anticipated to transform maintenance practices and foster efficiency improvements across multiple sectors.

- •5 October 2024, Bando Chemical Industries announced a strategic partnership with major power plant operators in Asia-Pacific to supply customized V-Ribbed belts designed for heavy-duty generators. The collaboration aims to enhance belt performance tailored to specific operational environments, improving energy transmission efficiency and reducing downtime. Bando's initiative reflects a market trend toward co-development and customer-centric solutions, leveraging technical expertise and regional market knowledge. This partnership is expected to increase Bando's market share in the fastest-growing Asia-Pacific region and expand its global footprint.

- •22 August 2024, Fenner PLC completed the acquisition of a leading specialty belt manufacturer in Europe, enhancing its product portfolio with advanced flat and poly-V belts for generator applications. The acquisition supports Fenner's growth strategy focused on broadening its technological capabilities and geographic presence. This move is projected to strengthen Fenner’s competitive position in the European market by offering diversified solutions and improved supply chain efficiencies. The consolidation reflects ongoing market trends of consolidation and strategic expansion within the generator belt industry.

- •Source: Official company press releases and industry publications

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 5.25 Billion |

| Forecast Year Market Size | USD 12.8 Billion |

| CAGR | 8.86% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 8.5% |

| Scope of Report | Market is segmented by Product Type (V-Ribbed Belts, V-Belts, Timing Belts, Flat Belts, Poly-V Belts), Application (Power Generation, Industrial Machinery, Automotive, Agricultural Equipment, Construction Equipment), End-Use Industry (Energy & Utilities, Manufacturing, Transportation, Agriculture), Distribution Channel (OEM, Aftermarket, Online Retail) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Gates Corporation (United States), Continental AG (Germany), Bando Chemical Industries, Ltd. (Japan), Mitsuboshi Belting Ltd. (Japan), Fenner PLC (United Kingdom), Optibelt Group (Germany), Dayco Products, LLC (United States), Hutchinson SA (France), Magma Belts (India), Apex Industrial Corporation (Taiwan), ContiTech AG (Germany), Morse Industrial Belting (United States), Bando Europe GmbH (Germany), Dayco Europe (Italy), Optibelt USA (United States), Mitsuboshi Belting Europe (Germany), Fenner Dunlop (United Kingdom), Hutchinson North America (United States), Magma Belts Europe (Germany), Apex Belting Europe (France), Bando China (China), Mitsuboshi Belting China (China), Gates India (India), Continental Asia Pacific (Singapore), Fenner Asia Pacific (Singapore) |

Global Generator Belt Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.