Global Natural Sack Kraft Papers Market Size, Growth & Revenue 2024-2034

Global Natural Sack Kraft Papers Market is segmented by Product Type (Virgin Kraft Paper, Recycled Kraft Paper, Semi-Chemical Kraft Paper, Bleached Kraft Paper, Unbleached Kraft Paper), Application (Packaging, Construction, Agriculture, Food Industry, Industrial Use), End-Use Industry (Cement & Building Materials, Chemical Industry, Food & Beverage, Agricultural Products), Distribution Channel (Direct Sales, Distributors & Wholesalers, Online Platforms), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The Global Natural Sack Kraft Papers market is defined by the manufacture and utilization of high-strength kraft papers designed for heavy packaging applications. These papers are produced using chemical pulping processes that maintain the natural fiber integrity, offering superior durability and tear resistance. The market scope includes a variety of product types such as virgin, recycled, bleached, and unbleached kraft papers, catering to applications in packaging, construction, agriculture, food industry, and industrial sectors worldwide. Increasing demand for environmentally sustainable packaging solutions, coupled with growth in construction and agricultural activities, significantly influences market expansion. The market is further shaped by technological advancements enhancing product quality and performance, along with regulatory frameworks promoting eco-friendly materials. Geographic demand varies, with North America dominating due to its mature industrial base and stringent environmental standards, while Asia-Pacific shows rapid growth driven by industrialization and urbanization. Overall, the market reflects a dynamic interplay of sustainability trends, industrial needs, and innovation, making it critical for stakeholders across the global supply chain.

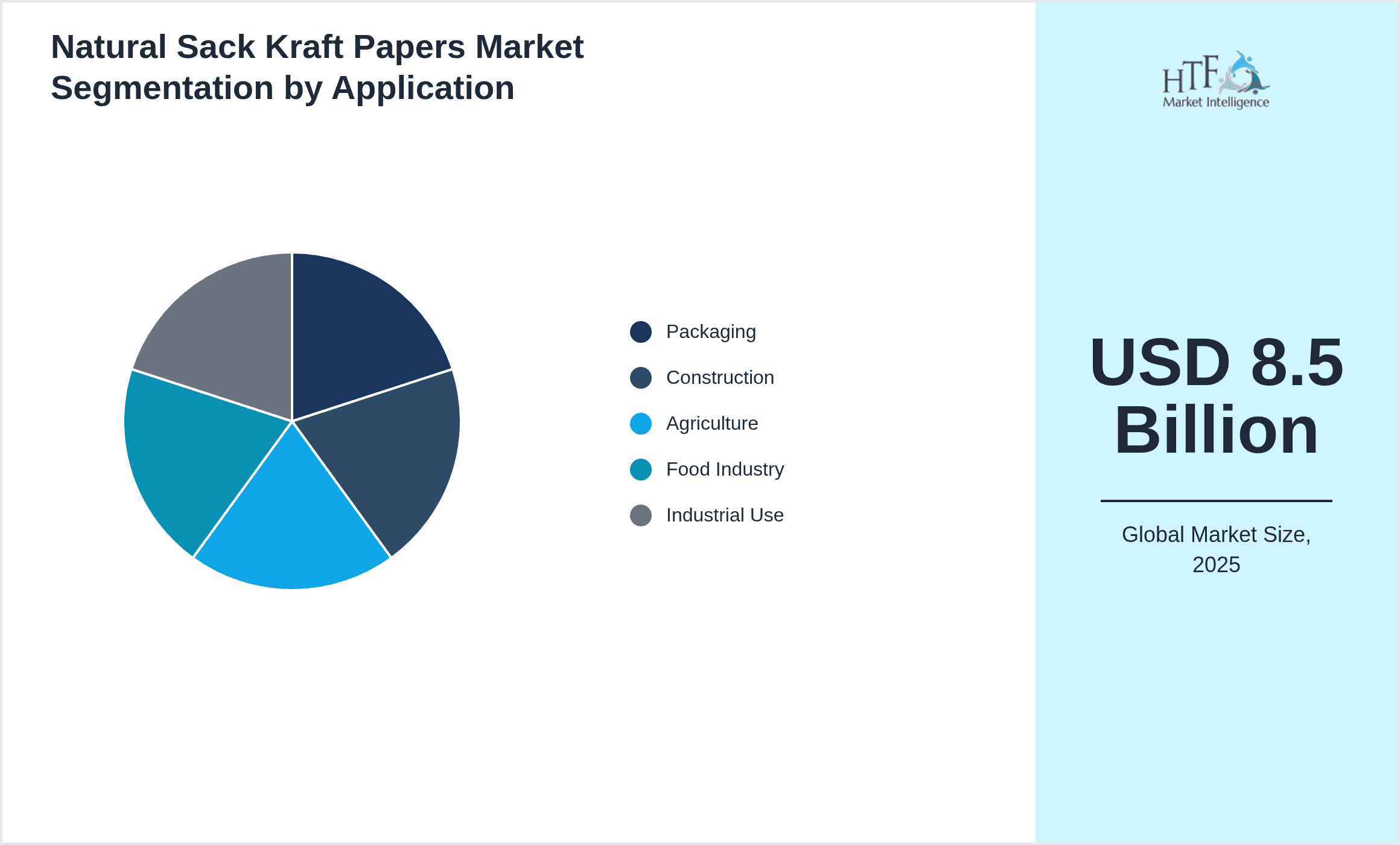

- •Key market highlights include a projected CAGR of 6.1% from 2024 to 2034, with the market size expanding from USD 8.5 Billion in 2024 to USD 15.7 Billion by 2034. Virgin kraft paper remains the leading product type, commanding the largest market share due to its superior strength and reliability. The packaging sector dominates application-wise, driven by increasing demand for sustainable and durable packaging materials globally. North America leads the market with the highest revenue share, attributed to advanced manufacturing infrastructure and regulatory emphasis on eco-friendly products. Meanwhile, Asia-Pacific is the fastest-growing region, propelled by burgeoning industrialization, population growth, and rising environmental awareness. Year-over-year growth is steady at approximately 6.0%, reflecting consistent adoption across industries and regions. These data points underscore the market’s robust potential and evolving dynamics in response to environmental, economic, and technological factors.

- •The natural sack kraft papers market offers significant value propositions to various industries by providing sustainable, durable, and cost-effective packaging solutions. Its strategic importance is underscored by the global push for reduced plastic usage and enhanced recyclability in packaging materials. Industries such as construction, agriculture, and food processing benefit from kraft papers’ protective qualities and environmental compliance. Additionally, manufacturers leverage innovation to produce eco-friendly products that meet evolving consumer demands and regulatory requirements. The market’s growth trajectory supports stakeholders including raw material suppliers, converters, end-users, and logistics providers by fostering a sustainable supply chain ecosystem. This market's expansion also stimulates investment in advanced production technologies and recycling capabilities, reinforcing global sustainability goals and economic development.

Competitive Landscape

The competitive environment in the global Natural Sack Kraft Papers market is characterized by the presence of several multinational and regional players who compete through innovation, quality enhancement, and strategic partnerships. Companies strive to differentiate their offerings by focusing on sustainable raw material sourcing, advanced production technologies, and product customization to meet diverse application needs. Market leaders leverage extensive distribution networks and invest in R&D to develop eco-friendly and high-performance kraft papers. Competitive rivalry is intensified by increasing demand for recycled and biodegradable products, prompting firms to adopt cost-efficient manufacturing and green certifications. Mergers and acquisitions are common strategies to consolidate market position and expand geographic presence. Pricing strategies vary across regions, influenced by raw material availability and regulatory compliance costs. The market also witnesses new entrants focusing on niche applications and eco-innovations, contributing to dynamic competition. Overall, the market demonstrates a high degree of competitiveness shaped by sustainability trends, technological evolution, and global demand fluctuations.

Key Participants in Natural Sack Kraft Papers Market

- •International Paper Company (United States)

- •WestRock Company (United States)

- •Mondi Group (United Kingdom/Austria)

- •Stora Enso Oyj (Finland)

- •Sappi Limited (South Africa)

- •UPM-Kymmene Corporation (Finland)

- •Nippon Paper Industries Co., Ltd. (Japan)

- •Smurfit Kappa Group (Ireland)

- •Domtar Corporation (Canada)

- •Suzano S.A. (Brazil)

- •Lee & Man Paper Manufacturing Ltd. (Hong Kong)

- •Nine Dragons Paper Holdings Limited (China)

- •Resolute Forest Products Inc. (Canada)

- •Boise Cascade Company (United States)

- •Oji Holdings Corporation (Japan)

- •Svenska Cellulosa Aktiebolaget (Sweden)

- •Canfor Corporation (Canada)

- •Ence Energia y Celulosa (Spain)

- •Metsä Board Corporation (Finland)

- •Asia Pulp & Paper Group (Indonesia)

- •Ahlstrom-Munksjö (Finland)

- •Rayonier Advanced Materials Inc. (United States)

- •UPM Specialty Papers (Finland)

- •Solenis LLC (United States)

- •Catalent Inc. (United States)

Market Breakdown

- •By Product Type

- ◦Virgin Kraft Paper

- ◦Recycled Kraft Paper

- ◦Semi-Chemical Kraft Paper

- ◦Bleached Kraft Paper

- ◦Unbleached Kraft Paper

- •By Application

- ◦Packaging

- ◦Construction

- ◦Agriculture

- ◦Food Industry

- ◦Industrial Use

- •By End-Use Industry

- ◦Cement & Building Materials

- ◦Chemical Industry

- ◦Food & Beverage

- ◦Agricultural Products

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors & Wholesalers

- ◦Online Platforms

Growth Dynamics

- •The global Natural Sack Kraft Papers market is propelled by the increasing demand for sustainable and biodegradable packaging materials amid rising environmental concerns. Growth in construction and agricultural sectors worldwide drives demand for durable sack papers capable of protecting heavy loads. Additionally, stringent environmental regulations and consumer preference for eco-friendly products encourage manufacturers to innovate with recycled and virgin kraft paper blends. Technological advancements in pulp processing and paper strength enhancement improve product versatility, opening new application avenues. The growing e-commerce sector also fuels demand for robust packaging solutions, contributing to market expansion. These drivers collectively accelerate adoption and investment in natural sack kraft papers globally.

- •Rapid urbanization and industrialization, particularly in Asia-Pacific, create substantial market growth opportunities by increasing the need for reliable packaging and construction materials. Rising awareness about environmental sustainability among consumers and businesses promotes the usage of natural kraft papers over synthetic alternatives. Furthermore, integration of circular economy principles encourages recycling and reuse, enhancing market prospects for recycled kraft paper types. The development of advanced manufacturing technologies ensures improved product quality and cost efficiencies, aiding market penetration. Expanding food and beverage industries also demand biodegradable packaging, bolstering application scope. These trends synergistically support sustained market growth.

- •Market growth is restrained by the volatility in raw material prices, particularly wood pulp, which affects production costs and pricing stability. Additionally, competition from synthetic packaging materials offering lower costs and certain performance advantages limits market share expansion. Supply chain disruptions and logistical challenges in certain regions pose obstacles to consistent market supply. Environmental regulations, while promoting sustainable products, also impose compliance burdens that can increase operational expenses. Limited awareness in developing regions about the benefits of natural kraft papers further constrains adoption. These factors collectively moderate growth despite favorable demand dynamics.

- •Significant opportunities arise from the increasing shift toward sustainable packaging mandated by global regulatory frameworks and consumer demand. Emerging markets in Asia-Pacific, Latin America, and Middle East & Africa offer untapped potential due to growing industrial activities and environmental awareness. Innovations in bio-based additives and coatings can enhance kraft paper properties, expanding usability in new sectors such as pharmaceuticals and electronics. Strategic partnerships and acquisitions among manufacturers can drive capacity expansion and geographic diversification. Digitalization of supply chains and e-commerce growth create additional demand for durable packaging. These opportunities present avenues for market players to capitalize on evolving trends and strengthen competitive positioning.

- •Challenges include high competition from alternative packaging materials such as plastics and woven polypropylene sacks, which may offer cost or performance benefits in specific applications. Ensuring consistent raw material supply amidst deforestation concerns and sustainable forest management practices presents operational complexities. Meeting diverse regional regulatory standards requires adaptive product development and increased compliance investment. Additionally, balancing product strength with biodegradability and recyclability necessitates ongoing R&D efforts. Market fragmentation and the presence of numerous small-scale producers can lead to pricing pressures and quality inconsistencies. Addressing these challenges is critical for sustained market growth and stakeholder confidence.

Market Trends

- •A prominent trend is the growing adoption of recycled kraft papers fueled by sustainability commitments across industries. Companies increasingly invest in eco-friendly production processes to minimize environmental impact while meeting customer expectations. This shift is supported by advances in recycling technologies that enhance fiber quality and product performance.

- •Innovation in functional coatings and barrier treatments on natural sack kraft papers improves moisture resistance and durability, broadening application potential especially in food packaging and industrial uses. This trend aligns with increasing demand for multifunctional, sustainable packaging.

- •Digital printing integration on kraft paper sacks is emerging as a strategic trend, enabling customization, branding, and enhanced consumer engagement. This development supports marketing strategies and supply chain transparency.

- •The rise of circular economy principles fosters enhanced recycling and reuse of kraft papers, driving industry collaboration among manufacturers, waste management entities, and regulatory bodies to improve sustainability metrics.

- •Geographical diversification of production facilities is observed, with companies expanding into Asia-Pacific and Latin America to capitalize on growing demand and cost advantages. This trend supports global supply chain resilience and market penetration.

- •Environmental certifications such as FSC and PEFC gain prominence as key differentiators, influencing purchasing decisions and regulatory compliance across regions. Certified products attract premium pricing and consumer trust.

- •Collaborations between kraft paper manufacturers and tech firms focus on developing smart packaging solutions incorporating sensors and QR codes, enhancing product traceability and consumer interaction.

Market Opportunities

- •Expanding the use of natural sack kraft papers in emerging sectors such as pharmaceuticals and electronics packaging presents significant growth potential due to the demand for protective and eco-friendly materials. Targeting these niches allows manufacturers to diversify revenue streams.

- •Increasing investments in developing markets across Asia-Pacific and Latin America create opportunities for capacity expansion and new product launches tailored to local requirements and environmental standards.

- •Technological innovations enabling enhanced barrier properties and printability offer opportunities to meet evolving customer demands for multifunctional and branded packaging solutions.

- •Strategic alliances and joint ventures between raw material suppliers and paper manufacturers can improve supply chain integration, reduce costs, and accelerate product innovation.

- •Growing e-commerce and logistics sectors drive demand for durable and sustainable packaging, providing a lucrative avenue for natural sack kraft paper applications.

- •Government incentives promoting sustainable packaging adoption encourage investments and market penetration, especially in regions with strict environmental policies.

- •Development of bio-based additives and coatings can create differentiated product offerings, enhancing competitiveness and meeting stringent regulatory requirements.

Market Challenges

- •Volatility in raw material costs, especially pulp prices, poses a significant challenge affecting production expenses and pricing strategies. This unpredictability can hinder long-term planning and profitability.

- •Competition from synthetic packaging alternatives such as plastics and woven polypropylene remains intense, as these materials often offer cost advantages and specific performance benefits.

- •Navigating complex and varying regional regulatory frameworks imposes compliance costs and operational constraints on manufacturers aiming for global market reach.

- •Ensuring sustainable sourcing of raw materials while adhering to environmental and social standards requires significant commitment and resource allocation.

- •Limited recycling infrastructure in certain emerging markets restricts the effective reuse of kraft papers, impacting circular economy goals and product positioning.

- •Market fragmentation with numerous small-scale producers leads to inconsistent product quality and pricing pressures, complicating brand differentiation.

- •Balancing product performance attributes such as strength and moisture resistance with biodegradability demands ongoing research and technological innovation.

Regulatory Framework

- •Between 2023 and 2024, several regions implemented stringent environmental regulations mandating increased use of biodegradable and recyclable packaging materials. These rules require manufacturers to comply with sustainability certifications and reporting standards, impacting production processes significantly.

- •The European Union enforced updated packaging waste directives emphasizing the reduction of plastic use and promoting circular economy principles, compelling kraft paper producers to enhance recyclability and material recovery.

- •In North America, regulatory bodies introduced safety and labeling standards for packaging materials used in food and pharmaceutical sectors, affecting product formulations and quality assurance practices.

- •Asia-Pacific governments have launched initiatives incentivizing sustainable packaging innovations through subsidies and tax benefits, fostering industry growth and technology adoption.

- •International agreements on forest management and certification programs such as FSC and PEFC have gained prominence, requiring compliance from kraft paper manufacturers to ensure sustainable raw material sourcing.

Market Intelligence

- •15th February 2024, International Paper Company launched an innovative range of recycled natural sack kraft papers featuring enhanced strength and moisture resistance, targeting the food packaging and construction sectors. The product integrates newly developed bio-based coatings that improve durability while maintaining full recyclability. This launch aims to address increasing demand for sustainable and high-performance packaging materials in North America and Europe. The strategic introduction supports the company’s sustainability goals and strengthens its competitive positioning in the global kraft paper market. Source: Official Company Press Release

- •22nd August 2023, Mondi Group introduced a digital printing technology compatible with natural sack kraft papers, enabling high-quality, customizable branding solutions for packaging applications. This innovation enhances marketing potential for end-users by allowing variable data printing and eco-friendly inks on kraft sacks. The technology rollout aligns with growing trends for personalized packaging and sustainable materials across Europe and Asia-Pacific markets. Mondi’s initiative represents a key step in combining functionality with environmental stewardship. Source: Industry Publication

- •30th November 2024, WestRock Company announced a strategic partnership with a leading bio-additives supplier to develop advanced biodegradable coatings for natural sack kraft papers. The collaboration focuses on improving barrier properties against moisture and grease, expanding application scope into food and pharmaceutical packaging. This joint venture supports WestRock’s commitment to sustainable product innovation and addresses evolving regulatory requirements globally. The partnership is expected to accelerate product development cycles and market penetration in North America and Asia-Pacific. Source: Official Company Announcement

- •10th May 2023, Stora Enso Oyj completed the expansion of its kraft paper production facility in Finland, increasing capacity by 20% to meet rising demand in Europe and North America. The upgrade incorporates energy-efficient technologies and supports the company’s sustainability targets by reducing carbon footprint. This investment enhances supply reliability and product quality for natural sack kraft papers used in packaging and industrial sectors. The expansion aligns with growing global demand and environmental regulations favoring eco-friendly materials. Source: Industry News Report

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 8.5 Billion |

| Forecast Year Market Size | USD 15.7 Billion |

| CAGR | 6.1% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 6% |

| Scope of Report | Market is segmented by Product Type (Virgin Kraft Paper, Recycled Kraft Paper, Semi-Chemical Kraft Paper, Bleached Kraft Paper, Unbleached Kraft Paper), Application (Packaging, Construction, Agriculture, Food Industry, Industrial Use), End-Use Industry (Cement & Building Materials, Chemical Industry, Food & Beverage, Agricultural Products), Distribution Channel (Direct Sales, Distributors & Wholesalers, Online Platforms) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Expanding the use of natural sack kraft papers in emerging sectors such as pharmaceuticals and electronics packaging presents significant growth potential due to the demand for protective and eco-friendly materials. Targeting these niches allows manufacturers to diversify revenue streams., Increasing investments in developing markets across Asia-Pacific and Latin America create opportunities for capacity expansion and new product launches tailored to local requirements and environmental standards., Technological innovations enabling enhanced barrier properties and printability offer opportunities to meet evolving customer demands for multifunctional and branded packaging solutions., Strategic alliances and joint ventures between raw material suppliers and paper manufacturers can improve supply chain integration, reduce costs, and accelerate product innovation., Growing e-commerce and logistics sectors drive demand for durable and sustainable packaging, providing a lucrative avenue for natural sack kraft paper applications., Government incentives promoting sustainable packaging adoption encourage investments and market penetration, especially in regions with strict environmental policies., Development of bio-based additives and coatings can create differentiated product offerings, enhancing competitiveness and meeting stringent regulatory requirements. |

Global Natural Sack Kraft Papers Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.