Global Single-photon Emission Computed Tomography (SPECT) Systems Market Size, Growth & Revenue 2025-2034

Global Single-photon Emission Computed Tomography (SPECT) Systems Market is segmented by Product Type (Compact SPECT Systems, Conventional SPECT Systems, Hybrid SPECT/CT Systems, Portable SPECT Systems, Digital SPECT Systems), Application (Cardiology, Neurology, Oncology, Orthopedics, Others), End-Use Industry (Hospitals, Diagnostic Centers, Ambulatory Care Centers, Research Institutes), Distribution Channel (Direct Sales, Distributors, Online Platforms), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The Global Single-photon Emission Computed Tomography (SPECT) Systems Market represents a critical segment of the nuclear medical imaging industry, delivering vital diagnostic capabilities across cardiology, neurology, oncology, orthopedics, and other medical fields. SPECT technology utilizes gamma ray detection from radiotracers to produce detailed functional imaging, enabling clinicians to assess physiological processes in three dimensions with high precision. The market includes a variety of system types such as conventional, compact, and portable SPECT devices, alongside more advanced hybrid SPECT/CT and digital SPECT systems that offer enhanced imaging clarity and diagnostic accuracy. Growth in this market is propelled by the increasing incidence of cardiovascular diseases, neurological disorders, and cancers globally, alongside rising awareness of early diagnosis and personalized treatment approaches. Technological advancements in image processing, device portability, and hybrid imaging platforms augment the clinical utility and adoption of SPECT systems. Additionally, expanding healthcare infrastructure, growing nuclear medicine adoption in emerging regions, and ongoing research initiatives contribute to market expansion. This report provides a detailed analysis of market dynamics, segmentation, regional performance, key players, and strategic insights to support stakeholders in navigating the evolving landscape of global SPECT systems.

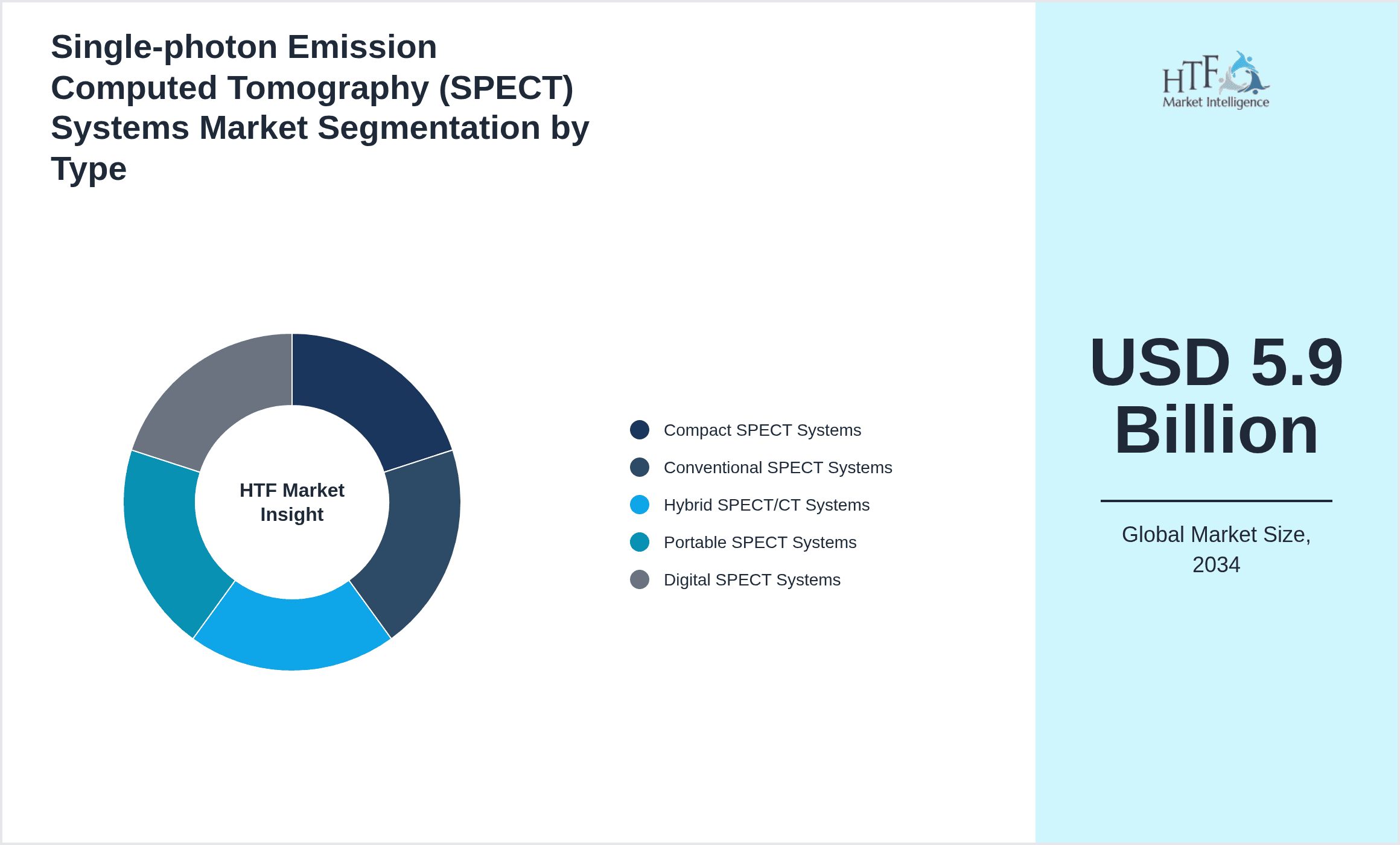

- •Key highlights of the market include a base market size of USD 2.8 Billion in 2025, projected to reach USD 5.9 Billion by 2034 at a CAGR of 7.9%. North America dominates the market due to robust healthcare infrastructure, technological leadership, and high prevalence of chronic diseases, while the Asia-Pacific region is identified as the fastest-growing market driven by increasing healthcare investments and rising disease burden. Hybrid SPECT/CT systems currently lead in product type share, favored for their combined anatomical and functional imaging capabilities, whereas digital SPECT systems are the fastest-growing segment, offering enhanced diagnostic resolution and workflow efficiency. The report also underscores emerging trends such as integration of artificial intelligence, miniaturization of devices, and growing demand for portable systems catering to point-of-care diagnostics. These factors collectively shape the competitive landscape and growth trajectory of the global SPECT systems market.

- •The strategic importance of the SPECT systems market spans multiple healthcare stakeholders, including hospitals, diagnostic centers, imaging specialists, and medical device manufacturers. The technology enables early and accurate diagnosis, improving patient outcomes and optimizing treatment pathways, particularly in chronic and complex diseases. For investors and industry players, the market offers significant growth potential fueled by continuous innovation, expanding applications, and increasing global healthcare expenditure. This report equips decision-makers with actionable intelligence on market segmentation, competitive dynamics, regulatory frameworks, and investment scenarios, facilitating informed strategy formulation and market positioning.

Competitive Landscape

The global Single-photon Emission Computed Tomography (SPECT) Systems market exhibits a highly competitive environment characterized by the presence of several multinational corporations, regional manufacturers, and emerging technology providers. Market dynamics are influenced by rapid technological innovation, with companies investing heavily in research and development to enhance imaging resolution, reduce scan times, and integrate hybrid functionalities such as SPECT/CT. Competitive strategies include product portfolio expansion, strategic partnerships, and mergers and acquisitions aimed at consolidating technological expertise and geographic reach. Pricing strategies vary across regions, reflecting differing healthcare economics and reimbursement policies, with premium pricing for advanced hybrid and digital systems balanced by demand for cost-effective compact and portable units in emerging markets. Distribution channels encompass direct sales to hospitals and diagnostic centers, collaborations with healthcare providers, and online platforms for equipment servicing and upgrades. Market entry barriers include stringent regulatory approvals, high capital investments, and the need for extensive clinical validation. Regional competition is notable, with North America and Europe hosting established players with strong brand equity, while Asia-Pacific witnesses rapid growth from both global entrants and local manufacturers focusing on affordability and tailored solutions. Future competitive trends are expected to emphasize artificial intelligence integration, minimally invasive imaging, and enhanced patient-centric features, driving differentiation and market expansion.

Leading Companies in Single-photon Emission Computed Tomography (SPECT) Systems Market

- •Siemens Healthineers (Germany)

- •GE Healthcare (United States)

- •Philips Healthcare (Netherlands)

- •Canon Medical Systems Corporation (Japan)

- •Spectrum Dynamics Medical (Israel)

- •Digirad Corporation (United States)

- •Neusoft Medical Systems (China)

- •Shimadzu Corporation (Japan)

- •Mediso Medical Imaging Systems (Hungary)

- •Dilon Technologies (United States)

- •Carestream Health (United States)

- •Molecular Imaging Corporation (United States)

- •Spectrum Medical Imaging (United States)

- •Rayence Co., Ltd. (South Korea)

- •Esaote S.p.A. (Italy)

- •Planar Systems Inc. (United States)

- •Toshiba Medical Systems Corporation (Japan)

- •Medtronic plc (Ireland)

- •Hologic, Inc. (United States)

- •Fujifilm Holdings Corporation (Japan)

- •Samsung Medison (South Korea)

- •Hitachi Medical Corporation (Japan)

- •Analogic Corporation (United States)

- •Esaote North America, Inc. (United States)

- •CareRay Healthcare Co., Ltd. (China)

Market Breakdown

- •By Product Type

- ◦Compact SPECT Systems

- ◦Conventional SPECT Systems

- ◦Hybrid SPECT/CT Systems

- ◦Portable SPECT Systems

- ◦Digital SPECT Systems

- •By Application

- ◦Cardiology

- ◦Neurology

- ◦Oncology

- ◦Orthopedics

- ◦Others

- •By End-Use Industry

- ◦Hospitals

- ◦Diagnostic Centers

- ◦Ambulatory Care Centers

- ◦Research Institutes

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors

- ◦Online Platforms

Growth Dynamics

The global Single-photon Emission Computed Tomography (SPECT) Systems market is propelled by several key growth drivers including the rising prevalence of chronic diseases such as cardiovascular disorders, neurological conditions, and cancers that necessitate advanced diagnostic imaging for effective management. Increasing healthcare expenditure worldwide, coupled with expanding nuclear medicine infrastructure in emerging markets, facilitates greater adoption of SPECT technology. Advancements in imaging modalities, notably the integration of hybrid SPECT/CT and the emergence of digital SPECT systems, enhance diagnostic accuracy and clinical utility, thereby driving demand. Additionally, technological improvements have led to more compact and portable systems, enabling expanded point-of-care diagnostics and improved patient accessibility. Growing awareness among clinicians and patients regarding the benefits of early and precise diagnosis further stimulates market expansion. Regulatory support and reimbursement policies favoring nuclear imaging contribute positively, while ongoing research and development activities focusing on AI-assisted imaging and workflow optimization offer promising avenues for growth. These factors collectively create a conducive environment for sustained market progression through the forecast period.

Market Trends

The Single-photon Emission Computed Tomography (SPECT) Systems market is witnessing significant trends including the increased adoption of hybrid imaging systems that combine anatomical and functional imaging to improve diagnostic specificity and patient outcomes. Digital SPECT technology is gaining traction due to its superior image resolution, faster processing times, and lower radiation doses, aligning with the trend towards patient-centric care. Integration of artificial intelligence and machine learning algorithms in image reconstruction and interpretation enhances diagnostic accuracy and operational efficiency. Miniaturization and development of portable SPECT devices are facilitating decentralized diagnostics and expanding usage in ambulatory and remote care settings. Furthermore, manufacturers are increasingly emphasizing sustainability and energy efficiency in device design, responding to broader healthcare environmental goals. Collaborations between technology developers, healthcare providers, and research institutions are fostering innovation, accelerating the introduction of next-generation systems into the market.

Market Opportunities

The expanding application of Single-photon Emission Computed Tomography (SPECT) beyond traditional cardiology and oncology into neurology and orthopedics presents significant growth opportunities. Emerging markets in Asia-Pacific, Latin America, and the Middle East & Africa offer substantial potential due to increasing healthcare infrastructure investments and rising disease burden. Innovations in hybrid and digital SPECT systems provide avenues for product differentiation and premium pricing. The integration of artificial intelligence and cloud-based platforms opens new possibilities for remote diagnostics and telemedicine applications. Additionally, strategic partnerships between medical imaging companies and healthcare providers can enhance market penetration and service offerings. Opportunities also exist in the development of cost-effective compact and portable devices tailored to resource-constrained settings, enabling broader access and adoption.

Market Challenges

The Single-photon Emission Computed Tomography (SPECT) Systems market faces several challenges including high initial capital investment and maintenance costs that limit adoption, particularly in developing regions. Stringent regulatory requirements and long approval timelines pose barriers to market entry and product launch. Technical complexities related to image quality, radiation safety, and the need for specialized operator training can restrict widespread utilization. Competition from alternative imaging modalities such as PET and MRI, which offer complementary or superior diagnostic capabilities in certain applications, also challenges market growth. Additionally, reimbursement uncertainties and inconsistent healthcare policies across regions may impact purchasing decisions. Supply chain disruptions and component shortages further complicate manufacturing and distribution, necessitating robust risk mitigation strategies.

Regulatory Framework

Between 2020 and 2025, several pivotal regulations have shaped the Single-photon Emission Computed Tomography (SPECT) Systems market. The U.S. Food and Drug Administration (FDA) implemented updated guidelines in 2023 emphasizing enhanced safety and efficacy requirements for nuclear imaging equipment, mandating rigorous clinical validation and improved radiation dose management. The European Union's Medical Device Regulation (MDR) enacted in 2021 introduced comprehensive compliance standards, quality management system requirements, and post-market surveillance obligations, significantly impacting device manufacturers targeting the European market. Japan's Pharmaceuticals and Medical Devices Agency (PMDA) strengthened approval frameworks during this period, facilitating expedited review pathways for innovative imaging technologies. Additionally, international organizations such as the International Atomic Energy Agency (IAEA) updated radiation safety protocols, influencing operational standards globally. Government initiatives promoting nuclear medicine adoption, reimbursement policies encouraging advanced diagnostics, and harmonization of regulatory requirements across regions collectively foster a more structured and transparent regulatory landscape. Compliance with these evolving mandates ensures patient safety, technological reliability, and market access, albeit presenting challenges in product development and commercialization timelines.

Market Intelligence

- •15th February 2025, Siemens Healthineers launched its next-generation digital SPECT/CT system featuring artificial intelligence-enabled image reconstruction and ultra-low radiation dose technology. The system targets cardiology and oncology applications, promising enhanced diagnostic accuracy and improved patient comfort. Siemens aims to strengthen its market leadership through this innovation, addressing growing demand for high-resolution imaging and workflow efficiency in hospitals and diagnostic centers worldwide. The launch was accompanied by strategic training programs to enhance user proficiency and accelerate adoption. Source: Siemens Healthineers Official Press Release

- •10th May 2025, GE Healthcare introduced an AI-driven software upgrade for its existing SPECT systems, enabling real-time image enhancement and automated anomaly detection. This innovation supports clinicians in faster and more precise diagnosis of neurological and cardiac conditions, reducing scan times and improving patient throughput. The company has positioned the software as a cost-effective upgrade for existing customers, facilitating technology adoption with minimal capital expenditure. This development aligns with the trend of integrating AI across medical imaging to augment clinical decision-making. Source: GE Healthcare Corporate Website

- •28th August 2025, Philips Healthcare announced a strategic partnership with a leading AI startup to co-develop cloud-based analytics platforms for SPECT imaging. The collaboration aims to leverage big data and machine learning to provide predictive diagnostics and personalized treatment planning. This initiative reflects Philips’ commitment to digital health transformation and expanding its portfolio of connected imaging solutions. The partnership is expected to accelerate innovation cycles and expand market reach in Asia-Pacific and Europe. Source: Philips Healthcare Newsroom

- •21st November 2024, Canon Medical Systems Corporation completed the acquisition of a portable SPECT device manufacturer, enhancing its portfolio with compact and mobile imaging solutions. This strategic move is designed to capture growing demand in emerging markets and point-of-care diagnostics. The acquisition is expected to generate synergies in R&D and distribution, positioning Canon for competitive advantage in the portable SPECT segment. Integration efforts focus on technology harmonization and expanded service offerings. Source: Canon Medical Systems Press Release

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 2.8 Billion |

| Forecast Year Market Size | USD 5.9 Billion |

| CAGR | 7.9% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7.6% |

| Scope of Report | Market is segmented by Product Type (Compact SPECT Systems, Conventional SPECT Systems, Hybrid SPECT/CT Systems, Portable SPECT Systems, Digital SPECT Systems), Application (Cardiology, Neurology, Oncology, Orthopedics, Others), End-Use Industry (Hospitals, Diagnostic Centers, Ambulatory Care Centers, Research Institutes), Distribution Channel (Direct Sales, Distributors, Online Platforms) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Siemens Healthineers (Germany), GE Healthcare (United States), Philips Healthcare (Netherlands), Canon Medical Systems Corporation (Japan), Spectrum Dynamics Medical (Israel), Digirad Corporation (United States), Neusoft Medical Systems (China), Shimadzu Corporation (Japan), Mediso Medical Imaging Systems (Hungary), Dilon Technologies (United States), Carestream Health (United States), Molecular Imaging Corporation (United States), Spectrum Medical Imaging (United States), Rayence Co., Ltd. (South Korea), Esaote S.p.A. (Italy), Planar Systems Inc. (United States), Toshiba Medical Systems Corporation (Japan), Medtronic plc (Ireland), Hologic, Inc. (United States), Fujifilm Holdings Corporation (Japan), Samsung Medison (South Korea), Hitachi Medical Corporation (Japan), Analogic Corporation (United States), Esaote North America, Inc. (United States), CareRay Healthcare Co., Ltd. (China) |

Global Single-photon Emission Computed Tomography (SPECT) Systems Market Size, Growth & Revenue 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.