Global Synthetic Single Crystal Diamond Market Size, Growth & Revenue 2025-2034

Global Synthetic Single Crystal Diamond Market is segmented by Product Type (Chemical Vapor Deposition (CVD) Synthetic Diamond, High Pressure High Temperature (HPHT) Synthetic Diamond, Polycrystalline Diamond, Detonation Diamond, Other Synthetic Diamond Types), Application (Electronics, Cutting Tools, Optical Components, Semiconductors, Jewelry), End-Use Industry (Automotive, Aerospace, Electronics Manufacturing, Industrial Machinery), Distribution Channel (Direct Sales, Distributors, Online Platforms), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global Synthetic Single Crystal Diamond market involves the manufacture and application of synthetic single crystal diamonds created predominantly by Chemical Vapor Deposition (CVD) and High Pressure High Temperature (HPHT) techniques. These diamonds are prized for their superior hardness, thermal conductivity, and optical clarity, making them indispensable in industries such as electronics, cutting tools, optics, semiconductors, and jewelry. The market scope covers the entire value chain from raw material procurement, diamond synthesis, processing, and finishing to distribution and end-use deployment. Demand is driven by technological advancements in electronics and semiconductor industries requiring high-performance materials, alongside increasing adoption in precision cutting and optical components manufacturing. The market is witnessing rapid innovation, with manufacturers focusing on improving synthesis efficiency and product quality, reducing costs, and expanding applications. End users span high-tech manufacturing, luxury goods, and industrial sectors, reflecting the broad utility of synthetic single crystal diamonds. This market is poised for strong growth due to expanding industrial requirements, evolving production technologies, and increasing global investments in synthetic diamond capabilities, providing a robust opportunity landscape for stakeholders.

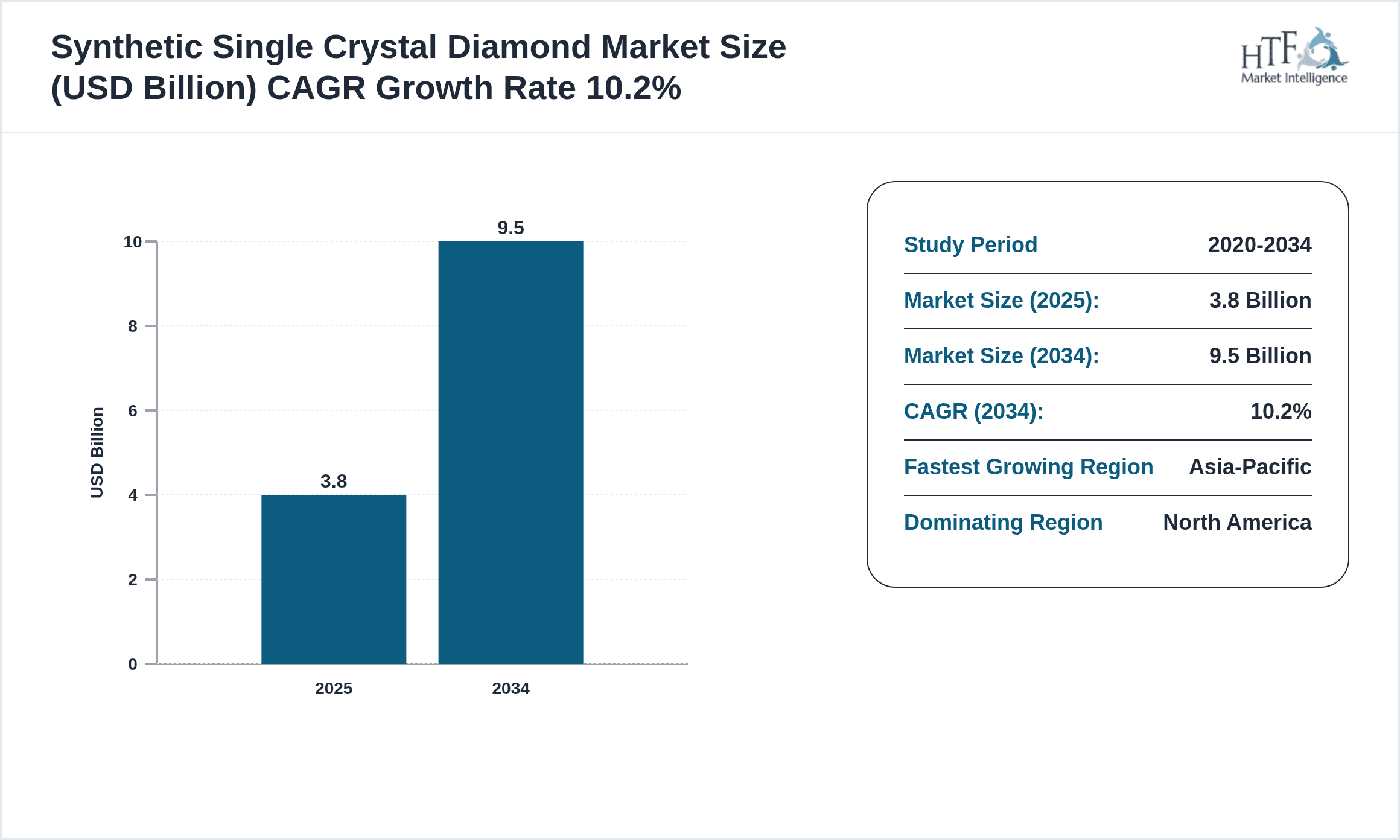

- •Key market highlights include a base year market size of USD 3.8 Billion in 2025, forecasted to reach USD 9.5 Billion by 2034, representing a CAGR of 10.2%. The year-on-year growth rate is approximately 9.8%, illustrating steady expansion driven by rising demand in electronics and cutting tool applications. North America currently dominates the market, benefiting from advanced technology adoption and strong R&D capabilities, while Asia-Pacific is projected to be the fastest-growing region due to burgeoning industrialization and increasing investments in semiconductor manufacturing facilities. Chemical Vapor Deposition (CVD) synthetic diamonds lead the product segment due to their superior quality and versatility, whereas the High Pressure High Temperature (HPHT) segment exhibits robust growth driven by cost efficiencies and expanding use in industrial applications.

- •The market offers strategic value propositions to sectors requiring materials with exceptional durability and thermal management capabilities. Its importance is underscored in electronics for thermal dissipation in power devices, in precision machining for durable cutting tools, and in optics for high-quality lenses and windows. Stakeholders including manufacturers, technology developers, and end users benefit from the synthetic diamonds’ ability to replace natural stones with consistent quality and scalability. The ongoing technological progress and expanding application horizons position this market as a vital contributor to innovation in high-performance materials globally.

Competitive Landscape

The Synthetic Single Crystal Diamond market is characterized by intense competition among global and regional players, driven by technological innovation and capacity expansion. Market leaders leverage advanced Chemical Vapor Deposition (CVD) and High Pressure High Temperature (HPHT) technologies to deliver high-quality products tailored to diverse industrial applications. Competitive strategies focus on product differentiation through enhanced performance characteristics, strategic partnerships for technology development, and expanding manufacturing footprints to meet growing demand. Mergers and acquisitions have facilitated consolidation, enabling companies to increase market share and optimize supply chains. Pricing strategies are influenced by raw material costs, technological sophistication, and end-user requirements, with premium pricing for superior quality crystals. Distribution channels are evolving, with direct sales to large industrial consumers complemented by specialized distributors serving niche applications. The market entry barriers include high capital expenditure, technical expertise requirements, and intellectual property protections. Regional competition is notable, with North America and Asia-Pacific being centers of innovation and manufacturing, respectively. Going forward, competition will intensify as emerging players invest in R&D and as synthetic diamond applications expand, necessitating continuous innovation and strategic agility.

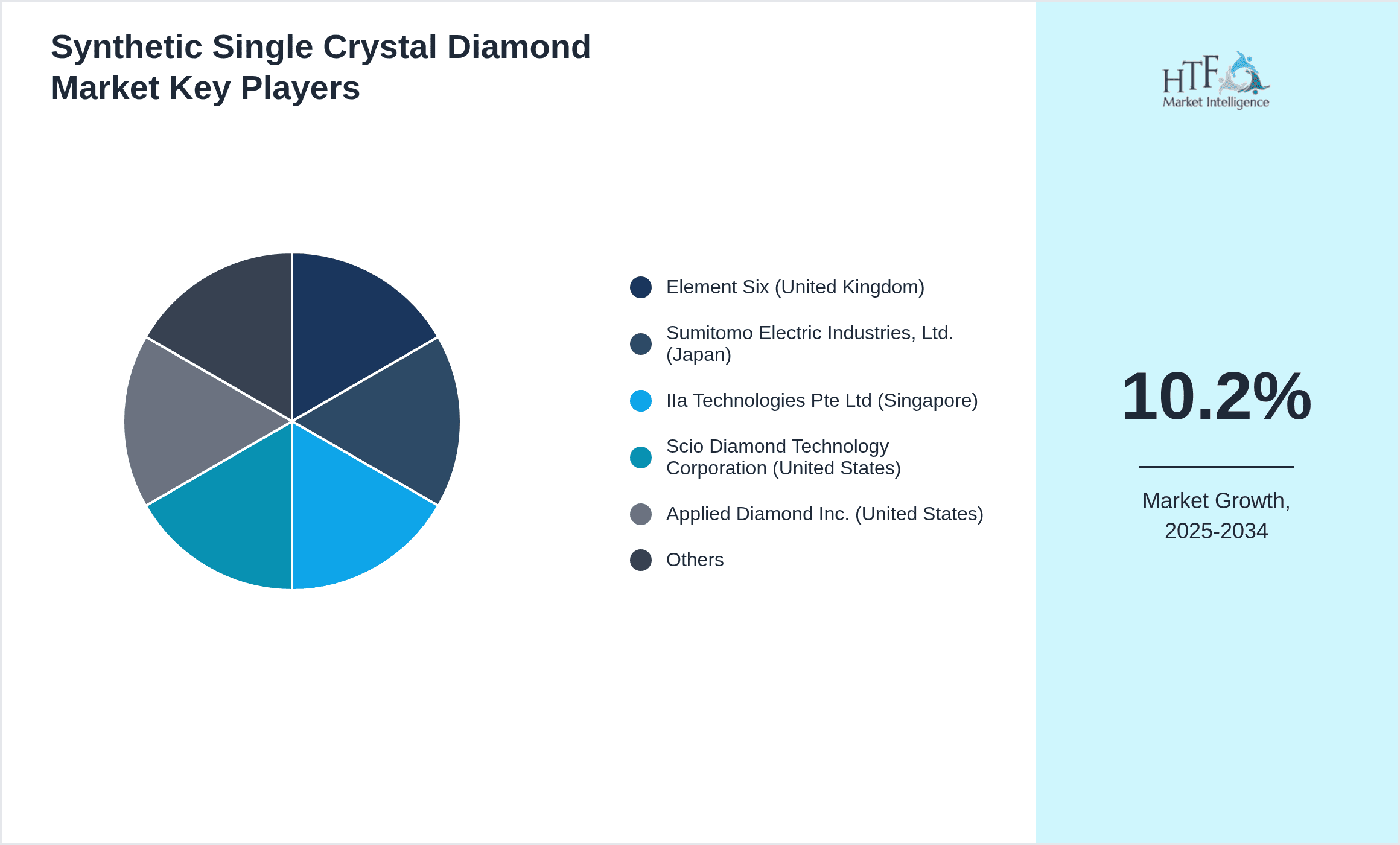

Key Players in Synthetic Single Crystal Diamond Market

- •Element Six (United Kingdom)

- •Sumitomo Electric Industries, Ltd. (Japan)

- •IIa Technologies Pte Ltd (Singapore)

- •Scio Diamond Technology Corporation (United States)

- •Applied Diamond Inc. (United States)

- •Diamond Materials GmbH (Germany)

- •New Diamond Technology (Russia)

- •Mitsubishi Electric Corporation (Japan)

- •Henan Huanghe Whirlwind Co., Ltd. (China)

- •Element Six Abrasives (South Africa)

- •Advanced Diamond Technologies (United States)

- •Diamond Innovations (United States)

- •Crystalox Limited (United Kingdom)

- •Adamas Nanotechnologies, Inc. (United States)

- •Diamond Materials (Switzerland)

- •Pure Grown Diamonds (United States)

- •Shenzhen Sinuote Technology Co., Ltd. (China)

- •PicoDiamond, Inc. (United States)

- •Apollo Diamond, Inc. (United States)

- •Meiwa Denko Corporation (Japan)

- •New Diamond Technology (Russia)

- •Advanced Diamond Technologies (United States)

- •Element Six Technologies (United Kingdom)

- •Sumitomo Electric Hardmetal Corp. (Japan)

- •IIa Technologies Pte Ltd (Singapore)

Market Breakdown

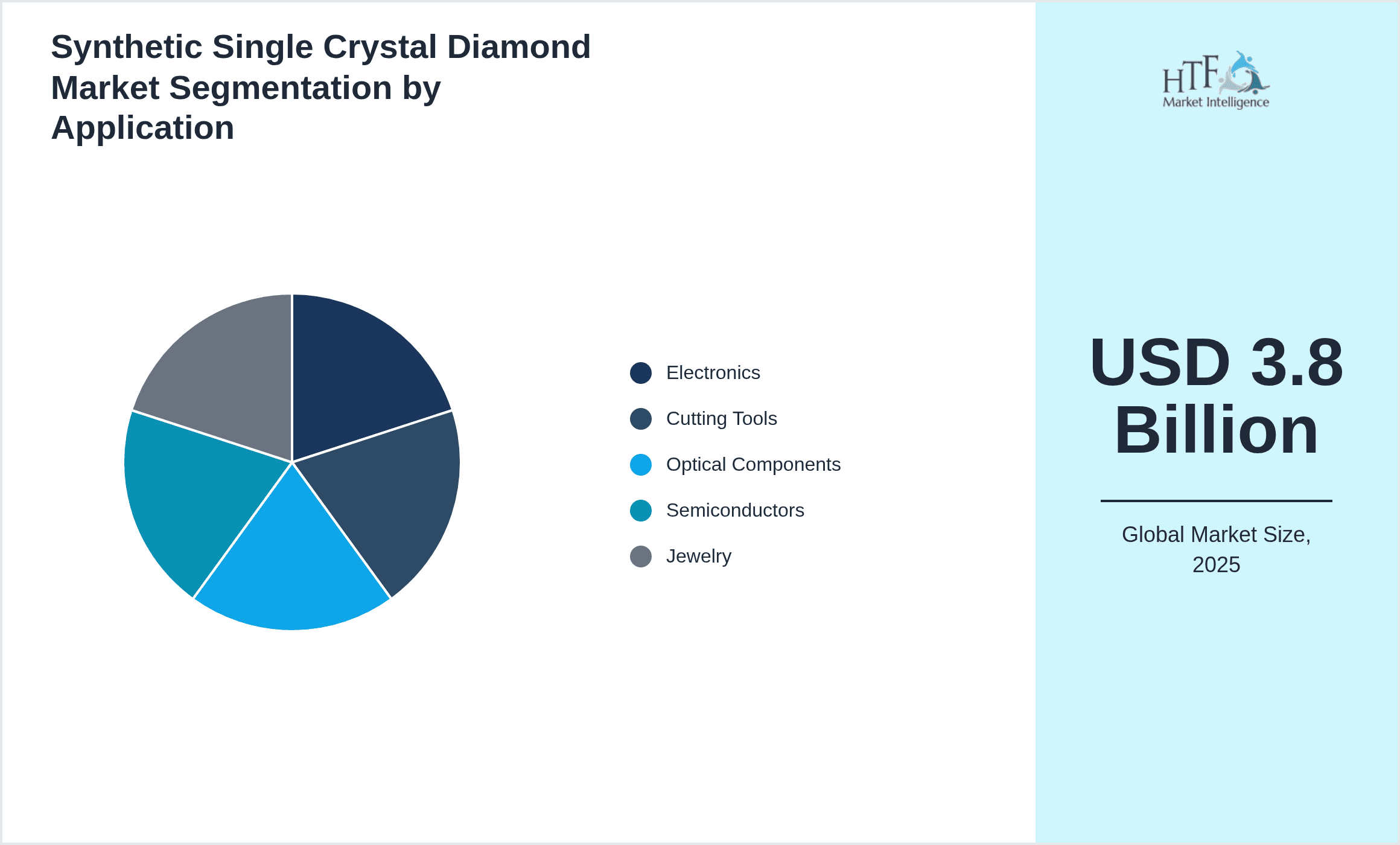

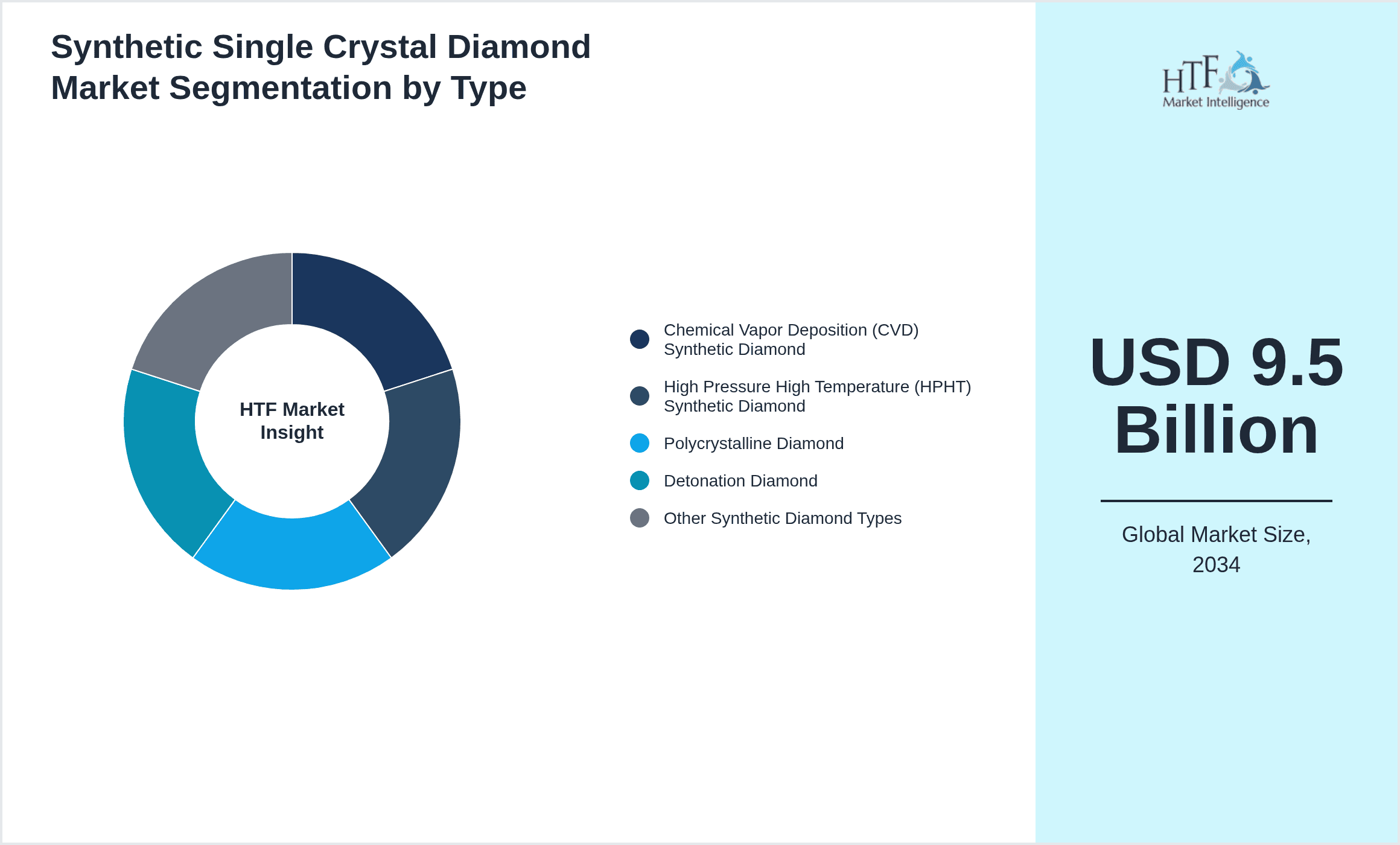

- •By Product Type

- ◦Chemical Vapor Deposition (CVD) Synthetic Diamond

- ◦High Pressure High Temperature (HPHT) Synthetic Diamond

- ◦Polycrystalline Diamond

- ◦Detonation Diamond

- ◦Other Synthetic Diamond Types

- •By Application

- ◦Electronics

- ◦Cutting Tools

- ◦Optical Components

- ◦Semiconductors

- ◦Jewelry

- •By End-Use Industry

- ◦Automotive

- ◦Aerospace

- ◦Electronics Manufacturing

- ◦Industrial Machinery

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors

- ◦Online Platforms

Growth Dynamics

- •The global synthetic single crystal diamond market growth is primarily propelled by increasing demand from the electronics sector, where diamond's superior thermal conductivity enhances device performance and longevity. Semiconductor manufacturers are integrating synthetic diamonds to improve heat dissipation in power devices, driving adoption. Additionally, the cutting tools segment benefits from diamond’s unparalleled hardness, enabling precision machining of tough materials, thereby increasing industrial efficiency. The rise in consumer electronics and automotive sectors further amplifies demand for diamond-based components.

- •Technological advancements in Chemical Vapor Deposition (CVD) and High Pressure High Temperature (HPHT) synthesis methods have significantly improved product quality and production scalability. These innovations reduce defects and enhance diamond crystal size, enabling broader application in high-tech industries. Companies are investing heavily in R&D to refine processes and lower costs, thus expanding market accessibility and fostering competitive advantage.

- •Increasing environmental regulations and sustainability concerns are encouraging industries to adopt synthetic diamonds as eco-friendly alternatives to mined diamonds. The synthetic process minimizes ecological impact while ensuring consistent quality and supply security, aligning with corporate responsibility goals and consumer preferences for ethically sourced materials.

- •Emerging economies in Asia-Pacific are witnessing rapid industrialization and infrastructure development, leading to heightened demand for synthetic diamonds in cutting tools and electronics applications. Government initiatives supporting high-tech manufacturing and innovation ecosystems further propel market expansion in this region.

- •Investment in semiconductor fabrication facilities and rising adoption of diamond-based optical components in telecommunications and defense sectors contribute to sustained growth. The integration of synthetic diamonds in emerging technologies such as quantum computing and photonics offers new growth avenues.

Market Trends

- •Rapid adoption of Chemical Vapor Deposition (CVD) techniques is transforming the synthetic diamond market by enabling production of larger, defect-free crystals suitable for high-performance electronics and optics. This trend reflects industry focus on quality enhancement and application diversification.

- •Integration of synthetic single crystal diamonds in semiconductor devices for thermal management and quantum applications is gaining momentum, driven by advancements in nano-fabrication and materials science. Companies are developing diamond-based substrates to improve chip performance and reliability.

- •Sustainability and ethical sourcing are increasingly influencing consumer and industrial preferences, fostering demand for lab-grown diamonds over natural stones. This shift supports market growth in jewelry and luxury goods segments, with a focus on traceability and environmental impact.

- •Collaborations between diamond manufacturers and technology firms to develop customized diamond solutions for emerging industries such as 5G, aerospace, and biomedical devices are shaping the market landscape. These partnerships accelerate innovation and market penetration.

- •Digitalization of supply chains and adoption of e-commerce platforms for diamond distribution are enhancing market reach and operational efficiency. Transparent online channels provide customers with access to high-quality synthetic diamonds and real-time product information.

Market Opportunities

- •Expansion into emerging applications such as quantum computing, photonics, and high-power laser systems presents significant growth potential due to synthetic diamond’s unique optical and thermal properties. Targeting these high-value niches can yield substantial returns.

- •Geographical expansion in rapidly industrializing regions like Asia-Pacific and Latin America offers opportunities to capitalize on growing electronics manufacturing and precision machining markets. Localized production and partnerships can enhance market access and reduce costs.

- •Investment in R&D for developing cost-effective synthesis methods and novel diamond composites can enable entry into new industrial segments such as automotive and aerospace, where material performance demands are increasing.

- •Strategic alliances and joint ventures with semiconductor and optical component manufacturers can facilitate co-development of application-specific diamond products, accelerating adoption and market penetration.

- •Enhancing online distribution channels and leveraging digital marketing can improve customer engagement and broaden end-user reach, especially in jewelry and consumer electronics segments.

Market Challenges

- •High capital expenditure and technical complexity associated with synthetic diamond production limit entry for new players and constrain capacity expansion, impacting market competitiveness and supply availability.

- •Volatility in raw material prices and dependence on specialized equipment pose risks to production cost stability, affecting pricing strategies and profitability.

- •Regulatory uncertainties and variations across regions regarding synthetic diamond certification and classification create compliance challenges and may affect market acceptance.

- •Competition from natural diamonds in jewelry and some industrial applications remains a restraint, particularly in markets where consumer preference for natural stones is strong despite sustainability concerns.

- •Supply chain disruptions, including shortages of high-purity gases and substrate materials, can impact manufacturing continuity and delivery schedules.

Regulatory Framework

- •The Kimberley Process Certification Scheme, implemented during 2003-2025, established strict controls to prevent conflict diamonds from entering the market, indirectly influencing synthetic diamond acceptance by emphasizing ethical sourcing.

- •Regional regulations such as the EU’s REACH and RoHS directives have mandated restrictions on hazardous substances in manufacturing, encouraging synthetic diamond producers to adopt environmentally compliant processes and materials.

- •Certification standards for synthetic diamonds, including those developed by the Gemological Institute of America (GIA) and International Organization for Standardization (ISO), provide guidelines on quality, nomenclature, and consumer transparency, fostering market trust.

- •Country-specific mandates in North America and Asia require compliance with safety and environmental regulations governing high-pressure equipment and chemical usage in diamond synthesis, impacting operational protocols and cost structures.

- •Government incentives and funding programs targeting advanced material research, particularly in Asia-Pacific and Europe, have supported innovation and capacity building in synthetic diamond manufacturing sectors.

Market Intelligence

- •15th January 2025, Element Six announced the launch of an advanced Chemical Vapor Deposition (CVD) synthetic single crystal diamond product line designed specifically for semiconductor thermal management applications. This new line features enhanced crystal purity and size up to 30mm, targeting high-power electronic devices requiring superior heat dissipation. The product aims to reduce device failure rates and improve energy efficiency, positioning Element Six as a leader in high-performance diamond substrates. The launch is supported by a strategic partnership with major semiconductor manufacturers to accelerate adoption in next-generation chips. Source: Official Element Six Press Release

- •20th March 2025, Sumitomo Electric Industries, Ltd. introduced a novel High Pressure High Temperature (HPHT) synthetic diamond optimized for cutting tool applications in automotive and aerospace industries. The innovation provides significantly improved toughness and thermal stability, enabling longer tool life and higher precision machining. The company highlighted that this product supports sustainable manufacturing by reducing tool replacement frequency and associated waste. Sumitomo’s proactive R&D investment underscores its commitment to addressing evolving industrial demands with cutting-edge diamond solutions. Source: Sumitomo Electric Annual Report 2025

- •10th May 2025, IIa Technologies Pte Ltd announced a collaborative research initiative with a leading photonics company to develop synthetic single crystal diamond substrates for quantum computing applications. The project focuses on fabricating ultra-pure diamond crystals incorporating nitrogen-vacancy centers to serve as qubits, aiming to enhance quantum device coherence and scalability. This strategic partnership is expected to position IIa Technologies at the forefront of emerging quantum technology markets, diversifying its application portfolio beyond traditional industrial uses. Source: IIa Technologies Official Website

- •25th July 2025, Scio Diamond Technology Corporation completed the acquisition of a specialized diamond polishing technology firm to enhance its finishing capabilities for synthetic single crystal diamonds. This acquisition is intended to improve product quality and throughput for high-value applications in optics and electronics. The integration of advanced polishing techniques is expected to strengthen Scio Diamond’s competitive position and expand its addressable market segments. Source: Scio Diamond Corporate Announcement

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 3.8 Billion |

| Forecast Year Market Size | USD 9.5 Billion |

| CAGR | 10.2% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 9.8% |

| Scope of Report | Market is segmented by Product Type (Chemical Vapor Deposition (CVD) Synthetic Diamond, High Pressure High Temperature (HPHT) Synthetic Diamond, Polycrystalline Diamond, Detonation Diamond, Other Synthetic Diamond Types), Application (Electronics, Cutting Tools, Optical Components, Semiconductors, Jewelry), End-Use Industry (Automotive, Aerospace, Electronics Manufacturing, Industrial Machinery), Distribution Channel (Direct Sales, Distributors, Online Platforms) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Element Six (United Kingdom), Sumitomo Electric Industries, Ltd. (Japan), IIa Technologies Pte Ltd (Singapore), Scio Diamond Technology Corporation (United States), Applied Diamond Inc. (United States) |

Global Synthetic Single Crystal Diamond Market Size, Growth & Revenue 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.