Global Natural Single Crystal Diamond Market Size, Growth & Revenue 2024-2034

Global Natural Single Crystal Diamond Market is segmented by Type (Gem-Quality Diamonds, Industrial-Grade Diamonds, Synthetic Diamonds, High-Pressure High-Temperature (HPHT) Diamonds, Chemical Vapor Deposition (CVD) Diamonds), Application (Industrial Cutting, Electronics, Jewelry, Optical Devices, Research & Development), End-Use Industry (Automotive, Aerospace, Consumer Electronics, Luxury Goods), Distribution Channel (Direct Sales, Distributors & Dealers, Online Retail), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

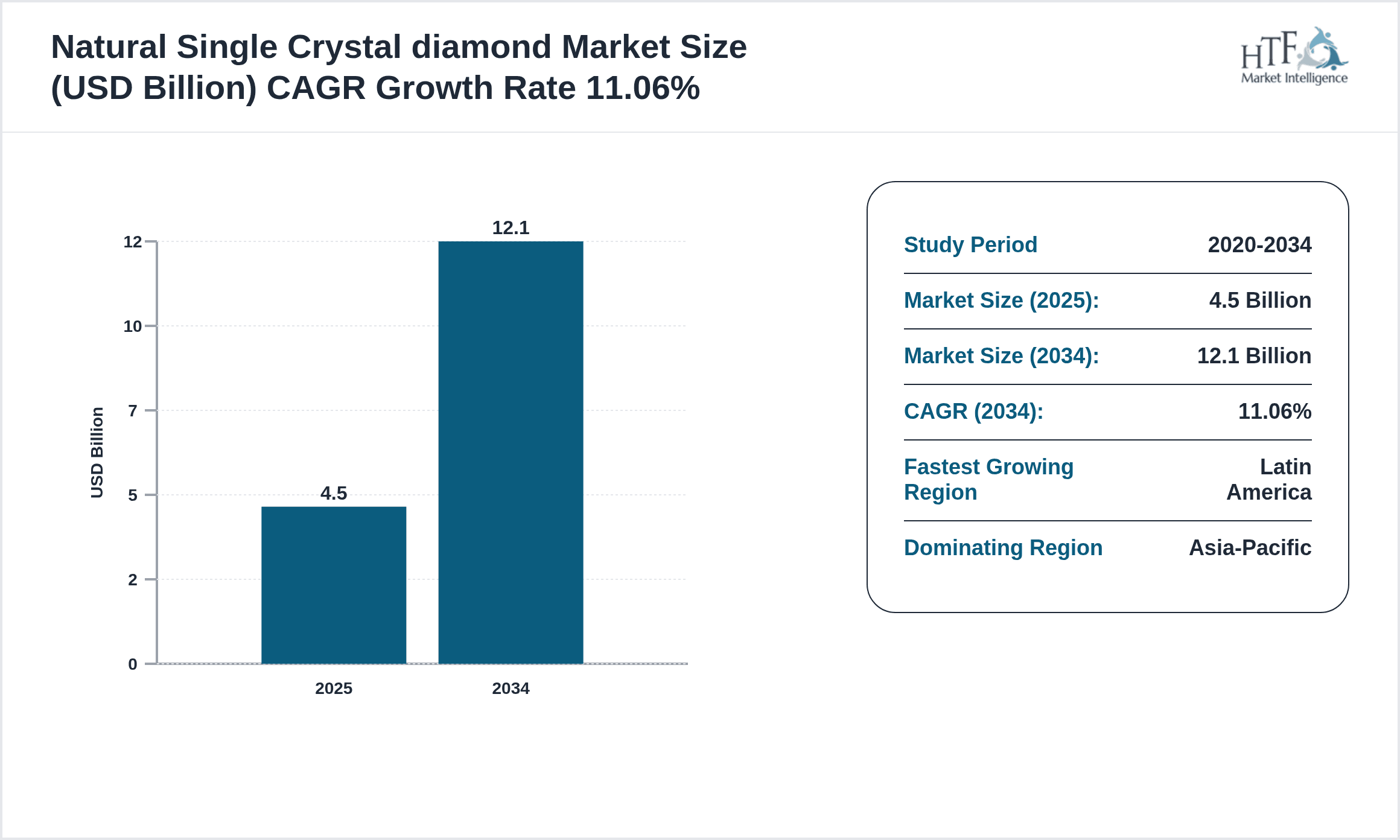

- •The global Natural Single Crystal Diamond market is defined by the extraction and utilization of naturally occurring single crystal diamonds valued for their unmatched hardness, thermal conductivity, and optical properties. These diamonds are primarily segmented into gem-quality stones for jewelry and industrial-grade diamonds utilized in cutting, grinding, and electronics. The market also includes synthetic variants produced via HPHT and CVD technologies, broadening the application scope to include advanced electronics and scientific research. The industry’s scope encompasses mining, processing, and distribution across key regions worldwide, with significant demand from sectors such as jewelry, precision engineering, and optics. The market excludes polycrystalline diamond forms, concentrating on single crystal types due to their superior performance characteristics. Increasing technological innovations and expanding industrial applications are pivotal, while geographical factors such as resource-rich regions and emerging economies shape market dynamics. This market analysis covers historical data from 2020 to 2024, with a forecast through 2034, providing comprehensive insights into growth drivers, trends, challenges, and opportunities.

- •Key market highlights include a base market valuation of USD 4.5 Billion in 2024, projected to reach USD 12.1 Billion by 2034, reflecting a robust CAGR of approximately 11.06%. Gem-quality diamonds dominate the product segment, driven by sustained demand in global jewelry markets, while synthetic diamonds exhibit the fastest growth owing to technological advancements and cost efficiency. Asia-Pacific emerges as the leading region, attributed to burgeoning manufacturing hubs and consumer markets. Latin America is identified as the fastest growing region, supported by increasing mining activities and expanding industrial usage. The market exhibits dynamic segmentation across applications such as industrial cutting, electronics, and optical devices, each contributing to diversified revenue streams. Year-over-year growth rates maintain a steady upward trajectory, underscoring the market’s resilience amid fluctuating economic conditions.

- •The natural single crystal diamond market offers significant strategic value to industries reliant on high-performance materials, including electronics, automotive, aerospace, and luxury sectors. Its unique properties support innovations in cutting-edge technologies and precision tools, enhancing product durability and efficiency. Stakeholders benefit from expanding applications and increasing consumer demand for premium gemstones. Furthermore, the integration of synthetic diamond technologies presents opportunities for cost reduction and scalability. The market's growth potential is underpinned by continuous research and development, regional resource optimization, and favorable regulatory frameworks. This positions the market as a critical component in global supply chains and innovation ecosystems, providing a compelling investment and growth landscape for manufacturers, distributors, and end-users alike.

Competitive Landscape

The competitive environment of the global Natural Single Crystal Diamond market is characterized by intense rivalry among established mining corporations, synthetic diamond manufacturers, and technology innovators. Market leaders leverage advanced extraction techniques, proprietary synthesis methods, and strategic partnerships to maintain and enhance their market positioning. Innovation is a critical differentiator, with companies investing significantly in R&D to develop higher quality synthetic diamonds and improve processing efficiencies. Competitive strategies also include geographic expansion, vertical integration, and portfolio diversification to cater to various end-use industries. Pricing strategies are influenced by raw material availability, production costs, and demand dynamics, with premium pricing maintained for gem-quality diamonds. The market exhibits moderate entry barriers due to the capital-intensive nature of mining and synthesis operations, while emerging players focus on niche applications and regional markets. Future trends indicate consolidation through mergers and acquisitions, increased focus on sustainable practices, and adoption of digital technologies to optimize supply chains and customer engagement.

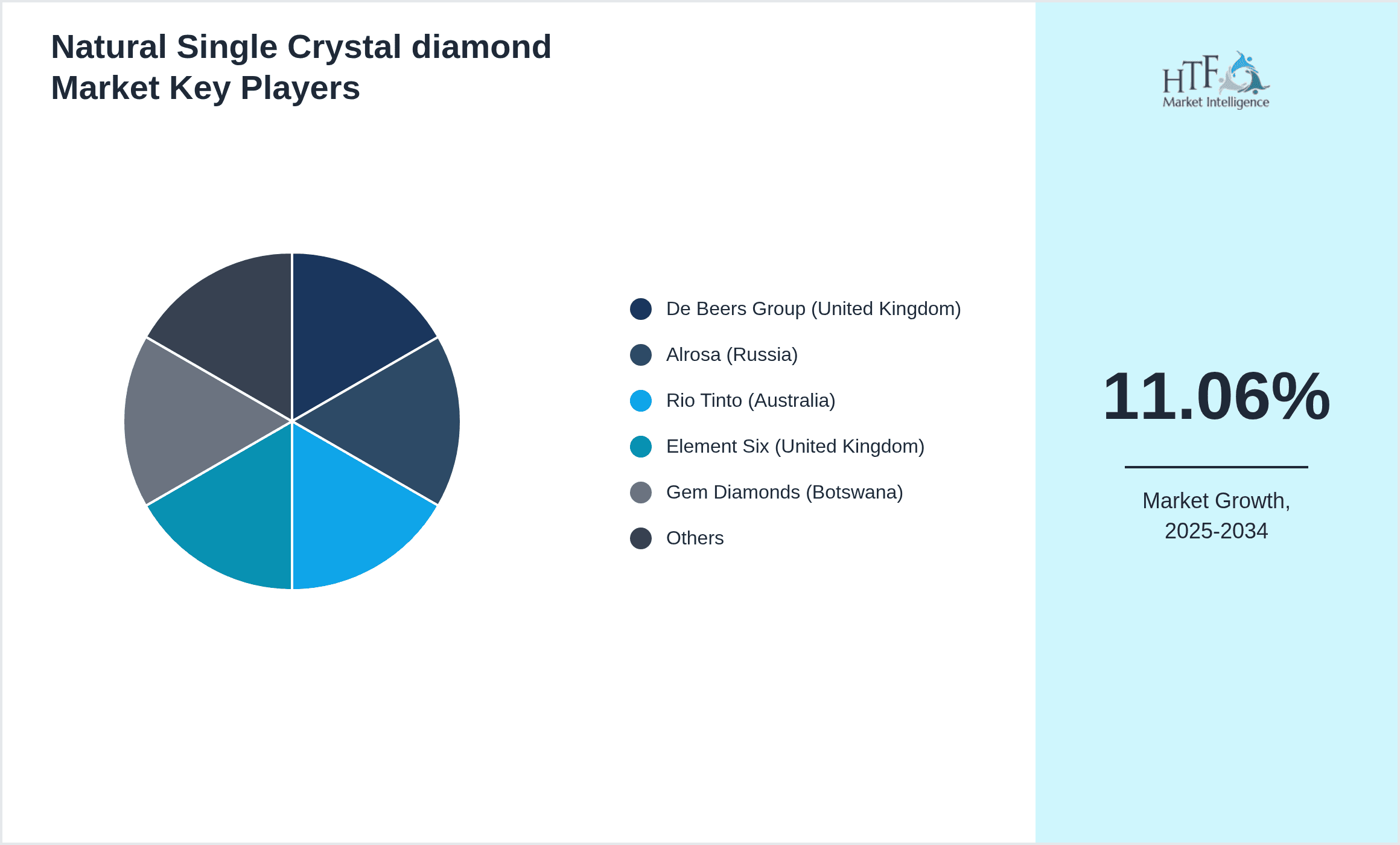

Leading Companies in Natural Single Crystal Diamond Market

- •De Beers Group (United Kingdom)

- •Alrosa (Russia)

- •Rio Tinto (Australia)

- •Element Six (United Kingdom)

- •Gem Diamonds (Botswana)

- •Lucara Diamond Corp. (Canada)

- •Stornoway Diamond Corporation (Canada)

- •Shandong Gold Group (China)

- •Sarine Technologies Ltd. (Israel)

- •Tiffany & Co. (United States)

- •Graff Diamonds (United Kingdom)

- •Chow Tai Fook Jewellery Group (Hong Kong)

- •Swarovski (Austria)

- •Tata Steel (India)

- •Sumitomo Electric Industries (Japan)

- •Applied Diamond Inc. (United States)

- •Morgan Technical Ceramics (United Kingdom)

- •IIa Technologies (Singapore)

- •Lucent Diamonds (India)

- •HB Company Ltd. (South Korea)

- •New Diamond Technology (Russia)

- •Mitsubishi Corporation (Japan)

- •Advanced Diamond Technologies Inc. (United States)

- •Kiran Gems (India)

- •Shandong Huasheng Diamond Co. Ltd. (China)

Market Breakdown

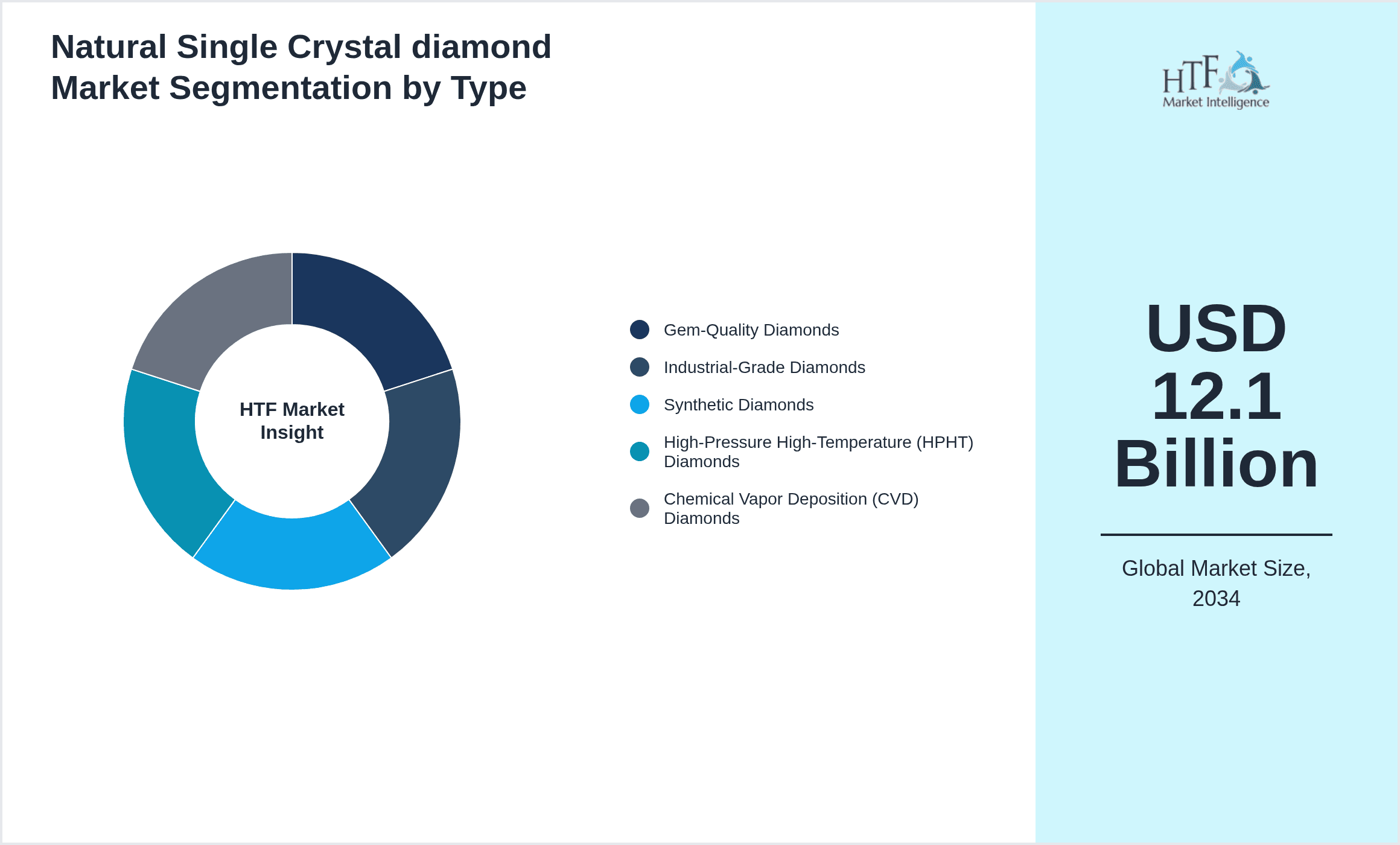

- •By Type

- ◦Gem-Quality Diamonds

- ◦Industrial-Grade Diamonds

- ◦Synthetic Diamonds

- ◦High-Pressure High-Temperature (HPHT) Diamonds

- ◦Chemical Vapor Deposition (CVD) Diamonds

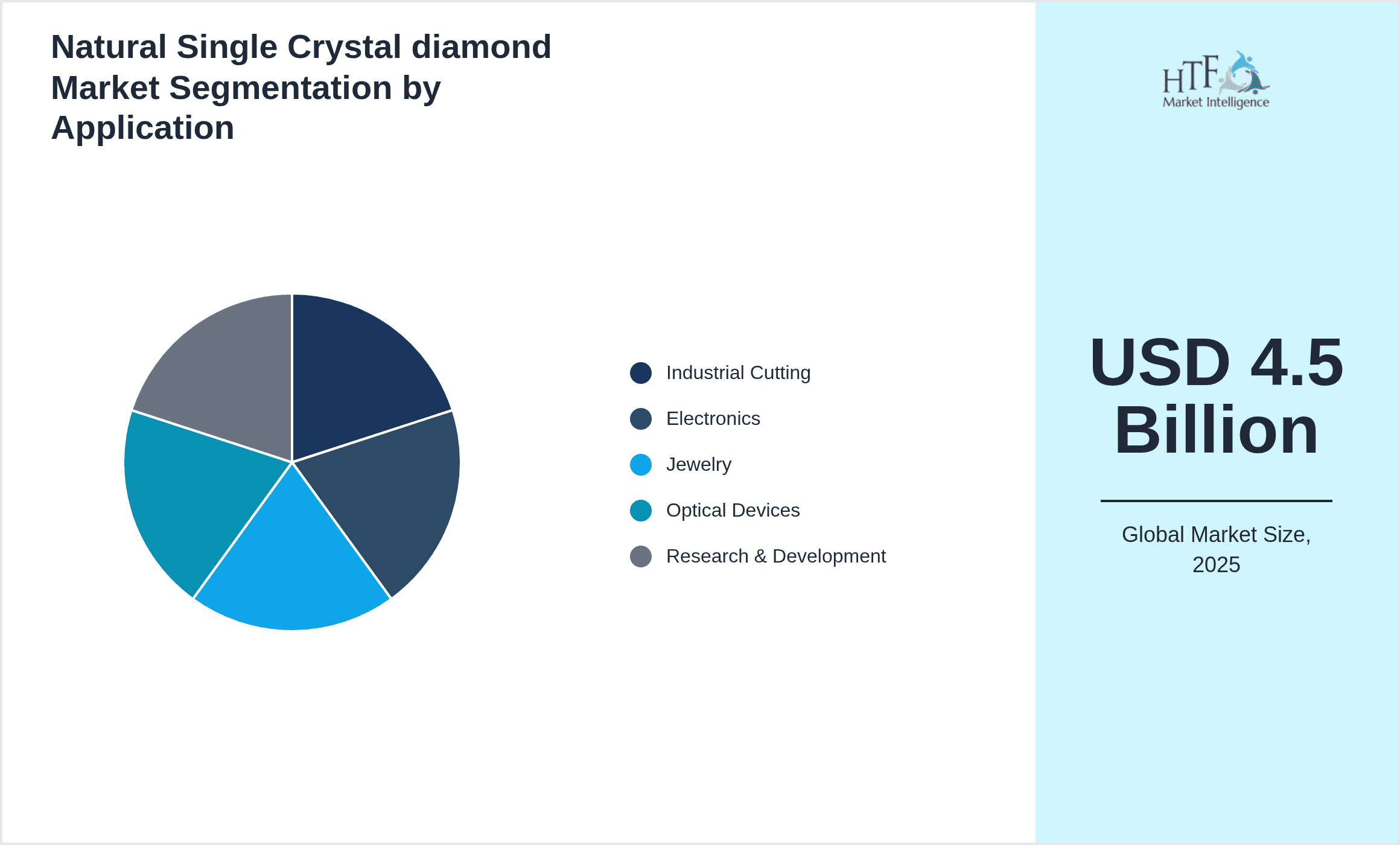

- •By Application

- ◦Industrial Cutting

- ◦Electronics

- ◦Jewelry

- ◦Optical Devices

- ◦Research & Development

- •By End-Use Industry

- ◦Automotive

- ◦Aerospace

- ◦Consumer Electronics

- ◦Luxury Goods

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors & Dealers

- ◦Online Retail

Growth Dynamics

The global Natural Single Crystal Diamond market is propelled by robust demand for gem-quality diamonds in the luxury jewelry sector, driven by rising disposable incomes and evolving consumer preferences. Concurrently, the expanding electronics industry leverages diamonds for heat dissipation and semiconductor applications, fostering technological advancements. Growth is further supported by increasing industrial utilization of diamonds in cutting, grinding, and drilling tools due to their superior hardness and durability. Synthetic diamond production via HPHT and CVD methods accelerates market expansion by offering cost-effective, high-quality alternatives, enabling penetration into emerging applications such as quantum computing and advanced optics. Government initiatives promoting mining activities and R&D investments in synthetic diamond technologies also stimulate growth. Overall, the market benefits from diversified applications, technological innovation, and geographic expansion, underpinning its strong CAGR trajectory toward 2034.

Market Trends

Emerging trends in the Natural Single Crystal Diamond market include the increasing adoption of synthetic diamonds produced through environmentally sustainable methods, responding to consumer demand for ethical sourcing. Integration of diamonds in next-generation electronics and photonics, such as quantum sensors and heat spreaders, exemplifies technological convergence driving market evolution. Strategic collaborations between mining companies and technology firms enhance innovation pipelines and supply chain efficiencies. Additionally, the luxury segment witnesses a shift toward bespoke and lab-grown diamond jewelry, reflecting changing consumer values. Digital platforms and e-commerce channels are revolutionizing diamond sales and distribution, enabling greater market reach and customer engagement. These trends collectively shape the competitive landscape and growth pathways, fostering resilience and adaptability in a dynamic global marketplace.

Market Opportunities

Significant opportunities lie in expanding applications of synthetic single crystal diamonds in high-tech industries including quantum computing, advanced optics, and biomedical devices, where diamond properties enhance performance and reliability. Geographic expansion into emerging markets with growing industrial bases and luxury consumer segments offers untapped revenue potential. Innovations in cost-effective synthesis and scalable manufacturing processes enable broader adoption and price competitiveness. Opportunities also exist for strategic partnerships and acquisitions that consolidate expertise and resources, facilitating product diversification and market penetration. Furthermore, rising environmental and ethical concerns create openings for lab-grown diamonds as sustainable alternatives, appealing to conscientious consumers. Capitalizing on these opportunities requires focused R&D, agile supply chain management, and targeted marketing strategies to address diverse customer needs and regulatory landscapes.

Market Challenges

Challenges facing the Natural Single Crystal Diamond market include the high capital intensity of mining and synthetic diamond production, limiting entry for new players and constraining capacity expansion. Fluctuations in raw material availability and geopolitical uncertainties impact supply stability and pricing. The market contends with competition from alternative materials and synthetic substitutes, which may affect demand for natural diamonds. Regulatory complexities and compliance requirements across jurisdictions impose operational burdens. Additionally, consumer skepticism regarding synthetic versus natural diamonds influences purchasing decisions, requiring effective marketing and certification standards. Environmental concerns related to mining activities also necessitate sustainable practices, adding to operational costs. Addressing these challenges demands strategic investment, innovation, transparent communication, and collaboration among stakeholders to ensure long-term market viability.

Regulatory Framework

From 2020 to 2024, the global Natural Single Crystal Diamond market has been influenced by a series of regulatory developments aimed at ensuring ethical sourcing, environmental sustainability, and product quality. Key regulations such as the Kimberley Process Certification Scheme have been reinforced to prevent conflict diamonds from entering the supply chain, impacting mining and trading entities worldwide. Environmental compliance mandates have been tightened, requiring mining companies to adopt sustainable extraction and rehabilitation practices. Synthetic diamond manufacturers face evolving standards related to labeling and consumer transparency to differentiate lab-grown products from natural stones. Regional regulations in major markets like North America, Europe, and Asia-Pacific include import-export controls and quality certification norms, shaping market entry and operational strategies. Government incentives supporting R&D in synthetic diamond technologies further influence market dynamics, balancing regulatory oversight with innovation promotion.

Market Intelligence

- •15th January 2024, De Beers Group launched its new line of lab-grown single crystal diamonds designed for industrial and jewelry applications, featuring enhanced purity and optical clarity. The initiative aims to meet growing consumer demand for ethically sourced diamonds while expanding technological applications in electronics and cutting tools. This launch underscores De Beers' strategic shift towards integrating synthetic diamond technology with its traditional mining operations, enhancing supply chain resilience and market reach. The product line incorporates advanced synthesis methods that reduce production costs and environmental impact, positioning the company competitively within the evolving diamond landscape. Source: De Beers Official Press Release

- •22nd September 2023, Element Six announced a breakthrough in chemical vapor deposition (CVD) technology, enabling the production of larger and more defect-free single crystal diamonds for semiconductor and quantum computing applications. This advancement is expected to accelerate adoption in high-tech industries requiring superior thermal management and electronic properties. The company plans to expand its manufacturing capacity and collaborate with technology partners to commercialize this innovation globally. This development reflects Element Six's commitment to maintaining technological leadership and addressing emerging market needs. Source: Industry Technology Review

- •Market Intelligence: Recent developments and industry insights are being monitored. For the latest updates, consult official company announcements and industry publications.

- •Market Intelligence: Recent developments and industry insights are being monitored. For the latest updates, consult official company announcements and industry publications.

Regional Outlook

The Asia-Pacific currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Latin America is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 4.5 Billion |

| Forecast Year Market Size | USD 12.1 Billion |

| CAGR | 11.06% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 11% |

| Scope of Report | Market is segmented by Type (Gem-Quality Diamonds, Industrial-Grade Diamonds, Synthetic Diamonds, High-Pressure High-Temperature (HPHT) Diamonds, Chemical Vapor Deposition (CVD) Diamonds), Application (Industrial Cutting, Electronics, Jewelry, Optical Devices, Research & Development), End-Use Industry (Automotive, Aerospace, Consumer Electronics, Luxury Goods), Distribution Channel (Direct Sales, Distributors & Dealers, Online Retail) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | De Beers Group (United Kingdom), Alrosa (Russia), Rio Tinto (Australia), Element Six (United Kingdom), Gem Diamonds (Botswana), Lucara Diamond Corp. (Canada), Stornoway Diamond Corporation (Canada), Shandong Gold Group (China), Sarine Technologies Ltd. (Israel), Tiffany & Co. (United States), Graff Diamonds (United Kingdom), Chow Tai Fook Jewellery Group (Hong Kong), Swarovski (Austria), Tata Steel (India), Sumitomo Electric Industries (Japan), Applied Diamond Inc. (United States), Morgan Technical Ceramics (United Kingdom), IIa Technologies (Singapore), Lucent Diamonds (India), HB Company Ltd. (South Korea), New Diamond Technology (Russia), Mitsubishi Corporation (Japan), Advanced Diamond Technologies Inc. (United States), Kiran Gems (India), Shandong Huasheng Diamond Co. Ltd. (China) |

Global Natural Single Crystal Diamond Market Size, Growth & Revenue 2024-2034 - Table of Contents

Research enthusiast focused on transforming data uncovering into actionable insights through data-driven decision-making.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.