Global Vehicle-borne Intelligent Communication Systems Market Size, Growth & Revenue 2024-2034

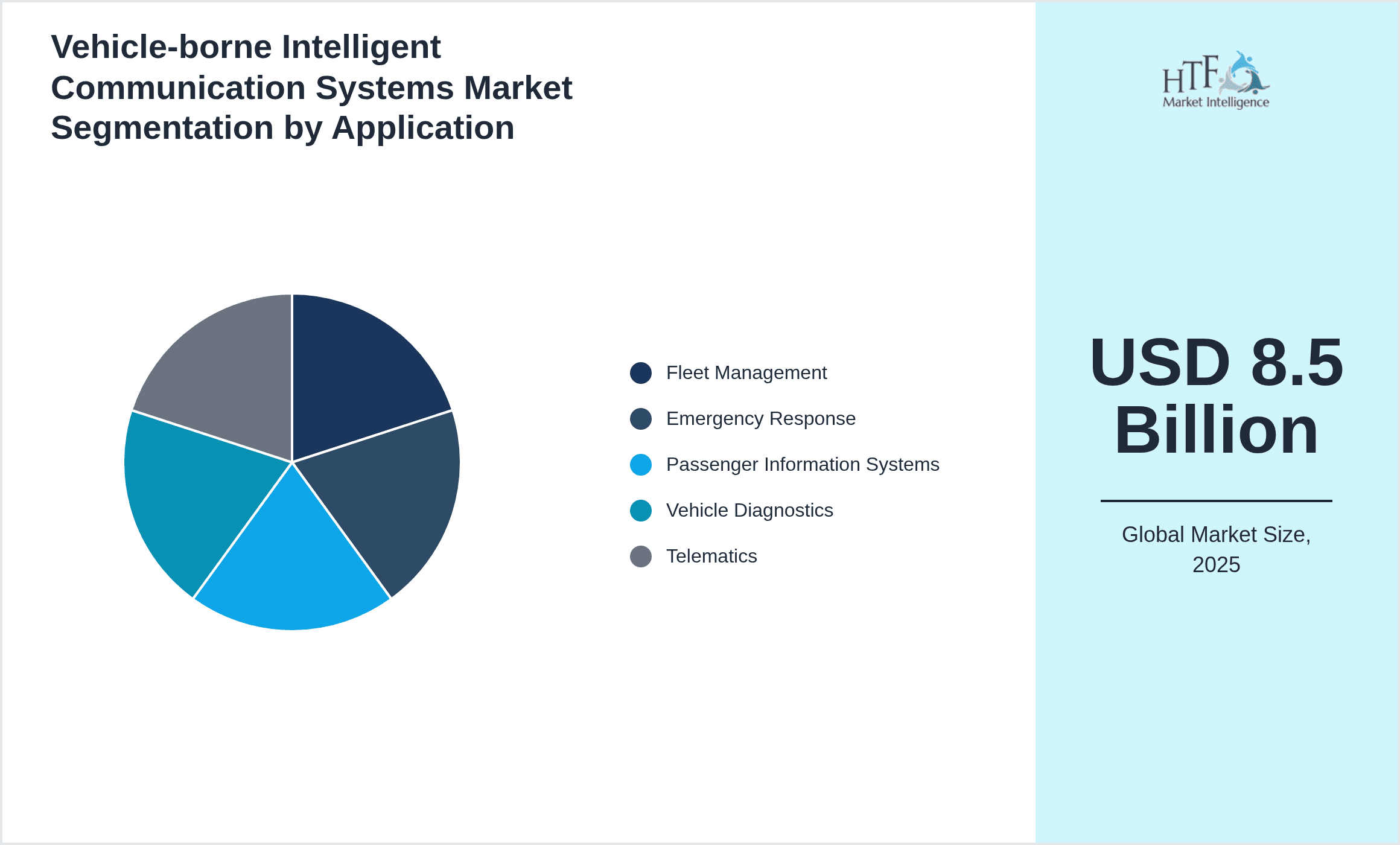

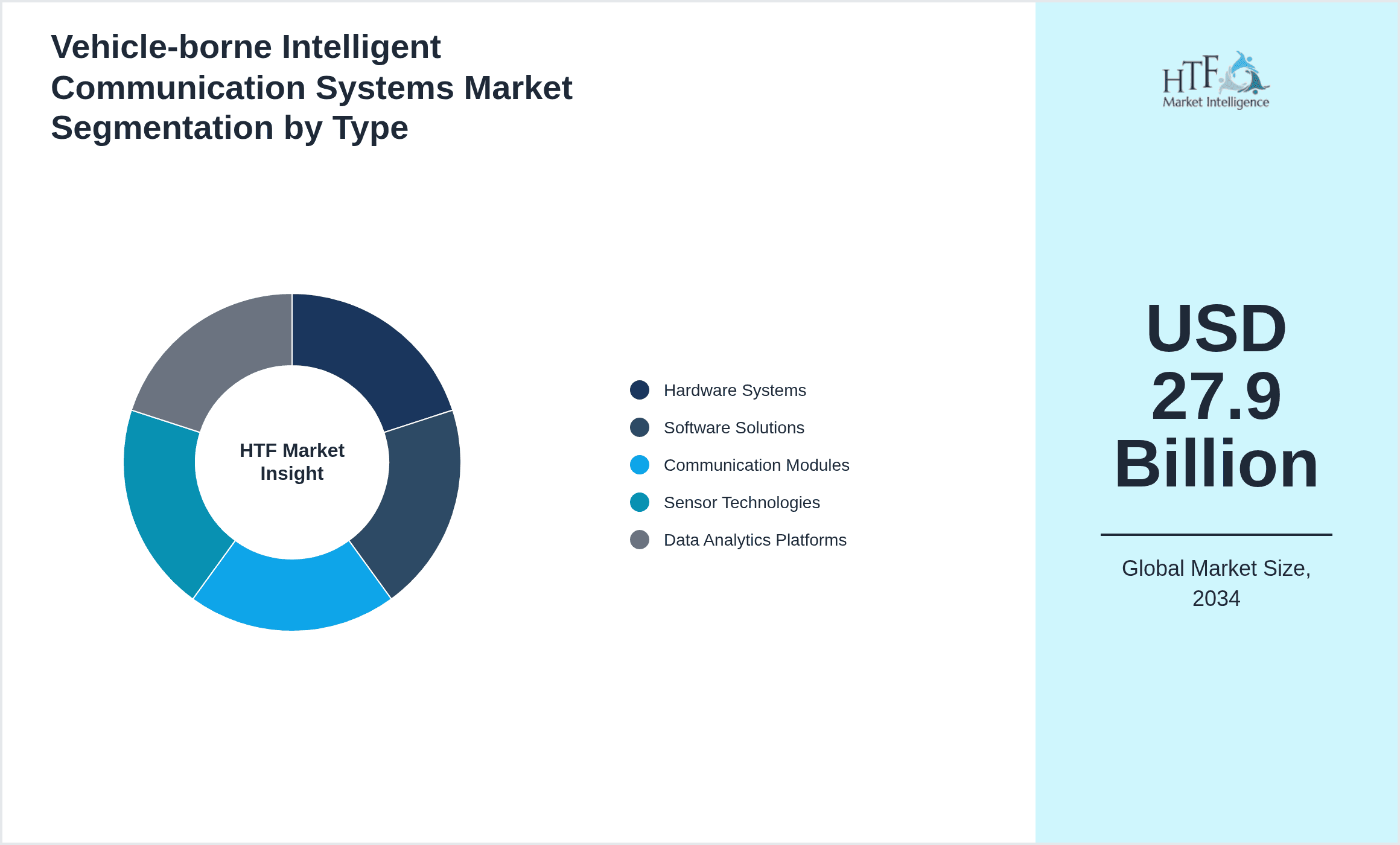

Global Vehicle-borne Intelligent Communication Systems Market is segmented by Product Type (Hardware Systems, Software Solutions, Communication Modules, Sensor Technologies, Data Analytics Platforms), Application (Fleet Management, Emergency Response, Passenger Information Systems, Vehicle Diagnostics, Telematics), End-Use Industry (Commercial Vehicles, Passenger Vehicles, Public Transportation, Emergency Services), Distribution Channel (Direct Sales, OEM Partnerships, Third-Party Distributors), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The Global Vehicle-borne Intelligent Communication Systems market represents a dynamic sector focused on integrating cutting-edge communication technologies into vehicles to enhance connectivity, safety, and operational efficiency. This market includes a diverse range of products such as hardware communication modules, sensor technologies, software solutions, and data analytics platforms designed to enable real-time vehicular data exchange with external infrastructures and control centers. Applications span across fleet management, emergency response coordination, passenger information dissemination, vehicle diagnostics, and telematics services, serving both commercial and passenger vehicle segments worldwide. The industry benefits from advancements in IoT, AI, and cloud computing, which collectively drive innovation and expand market opportunities. Increasing demand for connected vehicles and smart transportation systems across major global regions, including North America, Europe, and Asia-Pacific, underpins market growth. This report delivers an in-depth analysis of market segmentation, key players, regional dynamics, growth drivers, challenges, and strategic insights to guide stakeholders in capitalizing on emerging trends and opportunities.

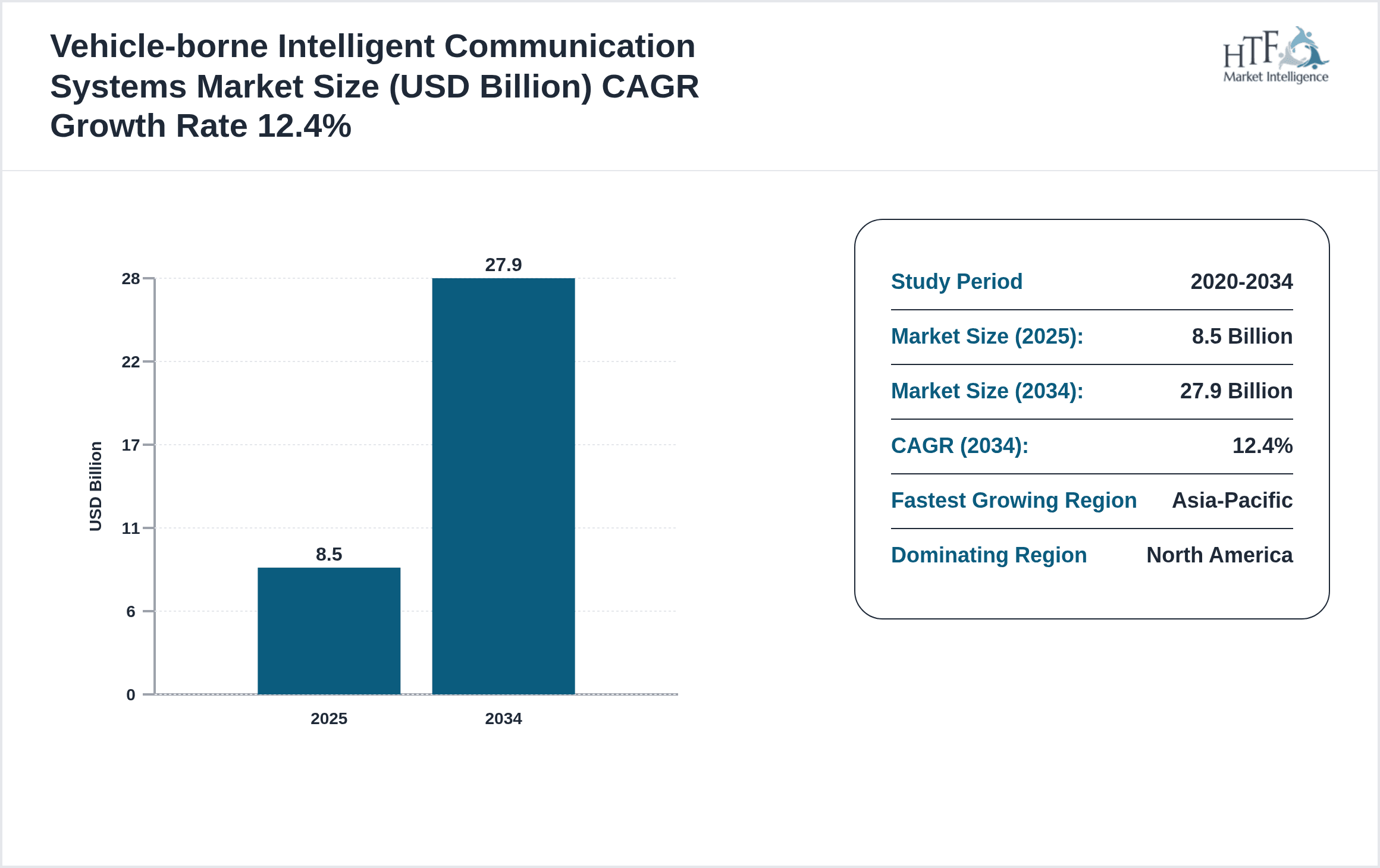

- •Key market highlights include a base market valuation of USD 8.5 Billion in 2024, projected to reach USD 27.9 Billion by 2034, exhibiting a robust CAGR of 12.4%. North America currently dominates the market due to early technology adoption and strong infrastructure, while Asia-Pacific is identified as the fastest-growing region fueled by rapid industrialization and smart city initiatives. Hardware Systems lead the product type segment by market share, whereas Data Analytics Platforms show the highest growth potential driven by increasing demand for predictive maintenance and enhanced data-driven decision-making. Fleet Management remains the primary application area, followed closely by Emergency Response systems, reflecting growing safety and logistics requirements worldwide.

- •The value proposition of Vehicle-borne Intelligent Communication Systems lies in their ability to transform transportation ecosystems by enabling real-time communication, enhancing safety protocols, optimizing fleet operations, and supporting regulatory compliance. These systems offer strategic importance to automotive manufacturers, logistics providers, emergency services, and technology vendors by fostering operational efficiencies, reducing costs, and facilitating innovation in connected vehicle services. The market's trajectory is shaped by continuous technological advancements, evolving regulatory landscapes, and growing consumer demand for intelligent vehicular communication solutions.

Competitive Landscape

The competitive landscape of the global Vehicle-borne Intelligent Communication Systems market is characterized by intense rivalry among established multinational corporations and innovative regional players. Market participants focus heavily on technological innovation, strategic partnerships, and product diversification to maintain and enhance market positioning. Companies invest in R&D to develop integrated communication modules, advanced sensor technologies, and sophisticated data analytics platforms tailored to diverse vehicular applications. Pricing strategies, extensive distribution networks, and compliance with evolving regulatory standards further influence competitive dynamics. The market also witnesses frequent mergers and acquisitions aimed at consolidating technological capabilities and expanding geographical reach. Regional competition varies with North America and Europe showcasing mature markets driven by early adopters, while Asia-Pacific presents high growth potential attracting new entrants and investments. Future trends indicate a shift towards AI-enabled communication systems and enhanced cybersecurity features as key differentiators in the competitive arena.

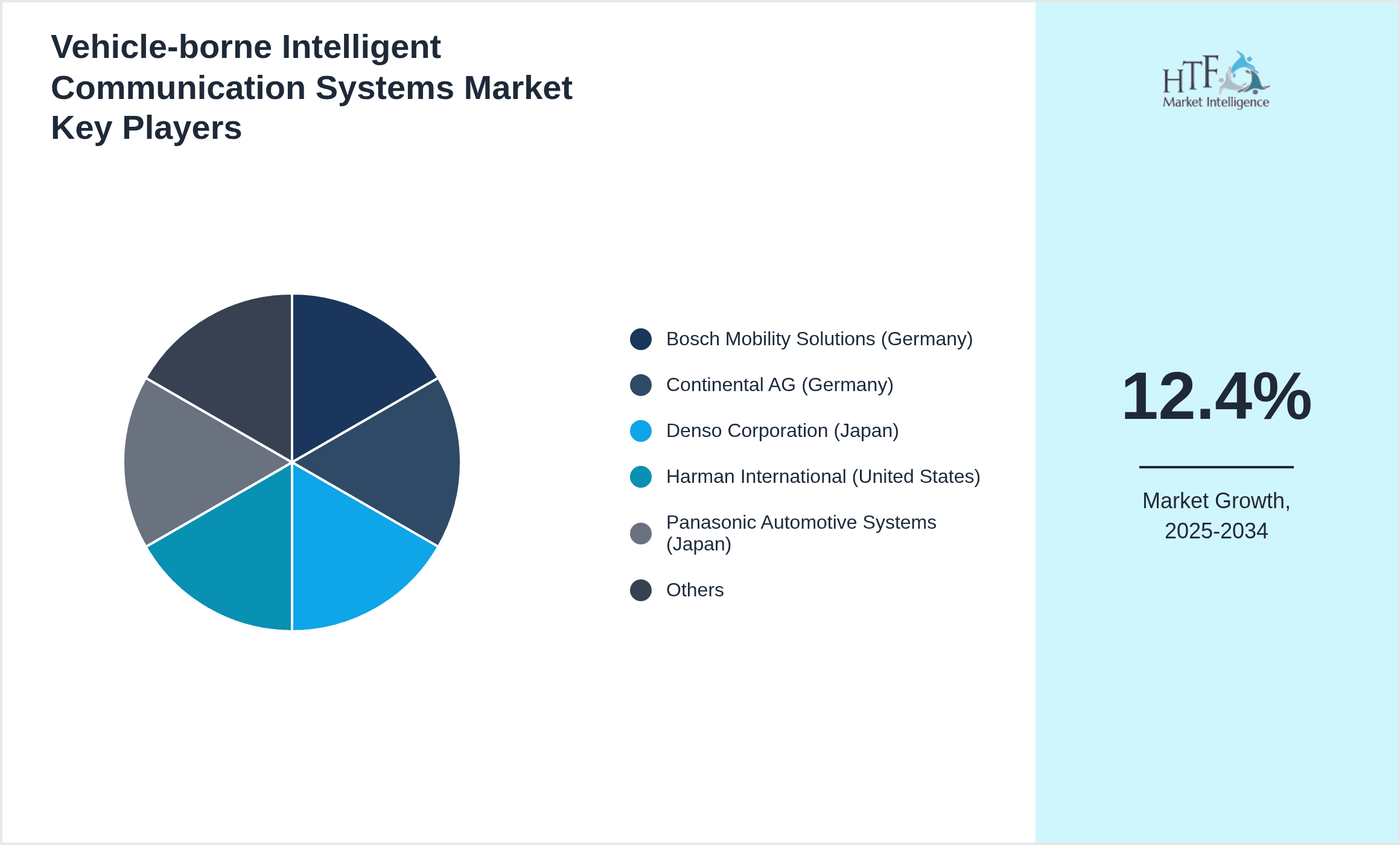

Leading Companies in Vehicle-borne Intelligent Communication Systems Market

- •Bosch Mobility Solutions (Germany)

- •Continental AG (Germany)

- •Denso Corporation (Japan)

- •Harman International (United States)

- •Panasonic Automotive Systems (Japan)

- •Aptiv PLC (Ireland)

- •ZF Friedrichshafen AG (Germany)

- •NXP Semiconductors (Netherlands)

- •Qualcomm Technologies, Inc. (United States)

- •Telematics Wireless Solutions (United States)

- •Delphi Technologies (United Kingdom)

- •Magneti Marelli (Italy)

- •Valeo SA (France)

- •Autoliv Inc. (Sweden)

- •Garmin Ltd. (Switzerland)

- •Sensata Technologies (United States)

- •Veoneer Inc. (Sweden)

- •Panasonic Corporation (Japan)

- •TomTom NV (Netherlands)

- •Nokia Corporation (Finland)

- •Samsung Electronics (South Korea)

- •Siemens AG (Germany)

- •Texas Instruments Incorporated (United States)

- •Renesas Electronics Corporation (Japan)

- •Infineon Technologies AG (Germany)

Market Breakdown

- •By Product Type

- ◦Hardware Systems

- ◦Software Solutions

- ◦Communication Modules

- ◦Sensor Technologies

- ◦Data Analytics Platforms

- •By Application

- ◦Fleet Management

- ◦Emergency Response

- ◦Passenger Information Systems

- ◦Vehicle Diagnostics

- ◦Telematics

- •By End-Use Industry

- ◦Commercial Vehicles

- ◦Passenger Vehicles

- ◦Public Transportation

- ◦Emergency Services

- •By Distribution Channel

- ◦Direct Sales

- ◦OEM Partnerships

- ◦Third-Party Distributors

Growth Dynamics

- •Rising demand for connected and autonomous vehicles globally is a primary growth driver, facilitating the adoption of intelligent communication systems that enhance vehicle-to-everything (V2X) connectivity and safety.

- •Government initiatives promoting smart city and intelligent transportation systems encourage investments in vehicle-borne communication technologies, driving market expansion across Asia-Pacific and Europe.

- •Technological advancements in IoT, AI, and cloud computing enable real-time data processing and predictive analytics, boosting the appeal of data analytics platforms and software solutions in this market.

- •Increasing fleet management requirements in logistics and public transportation sectors create strong demand for integrated communication and telematics solutions that optimize operations and reduce costs.

- •Enhanced focus on vehicle safety regulations and emergency response systems stimulates the integration of sensor technologies and communication modules in modern vehicles worldwide.

- •Growing consumer preference for personalized in-vehicle experiences supports the development of passenger information systems, contributing to market growth.

- •Strategic collaborations between automotive manufacturers and technology providers accelerate innovation cycles and widen product offerings in vehicle-borne communication systems.

Market Trends

- •Integration of 5G technology in vehicle communication systems is increasingly prevalent, enabling faster data transmission and supporting advanced telematics and autonomous driving features.

- •Emergence of AI-powered predictive maintenance tools within vehicle diagnostics enhances system reliability and reduces downtime, attracting fleet operators globally.

- •Adoption of cloud-based platforms for data analytics and remote vehicle monitoring is reshaping communication system architectures towards scalability and flexibility.

- •Growing emphasis on cybersecurity in vehicle communication networks addresses rising concerns over data breaches and unauthorized access, influencing product development priorities.

- •Collaborative ecosystems formed by technology vendors, automotive OEMs, and telecom providers facilitate innovation and standardization in vehicle-borne communication solutions.

- •Increasing integration of infotainment and passenger information systems enhances user experience, driving demand for sophisticated software solutions.

- •Shift towards electric and autonomous vehicles boosts the need for advanced communication systems that support complex vehicular operations and connectivity requirements.

Market Opportunities

- •Expanding smart city initiatives worldwide present significant opportunities for deploying vehicle-borne communication systems that integrate with urban infrastructure for enhanced traffic management.

- •Untapped markets in Latin America and the Middle East & Africa offer potential for growth through increased adoption of telematics and fleet management solutions.

- •Innovation in data analytics platforms enables the development of predictive and prescriptive insights, opening avenues for new service models and revenue streams.

- •Collaborations between automotive OEMs and technology firms create opportunities for co-developing customized communication solutions tailored to regional market needs.

- •Increasing regulatory mandates for vehicle safety and emissions monitoring drive demand for integrated communication and diagnostic systems across all vehicle segments.

- •Growth in electric vehicle adoption necessitates advanced communication networks supporting battery management and charging infrastructure integration, expanding market scope.

- •Investment in cybersecurity solutions within vehicle communication systems presents opportunities to address emerging threats and comply with stringent data protection regulations.

Market Challenges

- •High initial investment costs for advanced hardware and software solutions limit adoption among small and medium-sized fleet operators, restraining market growth.

- •Complex regulatory environments across different regions create compliance challenges for manufacturers and service providers in deploying vehicle-borne communication systems globally.

- •Interoperability issues arising from diverse communication standards and protocols hinder seamless integration of systems across vehicle models and infrastructure.

- •Data privacy and cybersecurity concerns pose significant risks, requiring continuous innovation and investment to safeguard vehicle communication networks.

- •Limited availability of skilled professionals with expertise in automotive communication technologies constrains R&D and deployment efforts in emerging markets.

- •Supply chain disruptions and component shortages impact timely production and delivery of communication hardware, affecting market stability.

- •Resistance to technology adoption among traditional vehicle operators and end-users slows penetration rates in certain regions.

Regulatory Framework

- •Between 2019 and 2024, the implementation of the EU General Data Protection Regulation (GDPR) mandated strict data privacy and security protocols for vehicle communication systems operating in Europe, influencing product design and compliance strategies.

- •The United States Federal Communications Commission (FCC) introduced enhanced spectrum allocation regulations for vehicular communication frequencies in 2020, facilitating improved V2X communication capabilities while ensuring interference mitigation.

- •Safety standards such as the UNECE WP.29 regulations, enacted in 2021, require automotive manufacturers to integrate cybersecurity management systems in vehicles, impacting the development of communication technologies worldwide.

- •China’s Ministry of Industry and Information Technology (MIIT) released guidelines in 2023 promoting intelligent connected vehicle technologies, encouraging domestic innovation and standardization in vehicle-borne communication systems.

- •Government incentive programs in North America and Europe offer subsidies and tax benefits for adopting advanced telematics and communication systems in commercial fleets, fostering market growth since 2022.

Market Intelligence

- •15th January 2025, Bosch Mobility Solutions launched a new generation of vehicle communication modules featuring enhanced 5G connectivity and integrated AI for predictive diagnostics. This product targets fleet operators aiming to reduce downtime and improve safety through real-time data analytics and seamless network integration. The launch reflects Bosch's strategic focus on expanding its telematics portfolio to meet growing demands in connected vehicle technologies across global markets. The modules are designed to comply with emerging regulatory standards and support scalable deployments in diverse vehicular applications. Source: Bosch Official Press Release

- •10th March 2025, Aptiv PLC announced a strategic partnership with Qualcomm Technologies to co-develop next-generation software solutions for vehicle-borne intelligent communication systems. This collaboration aims to leverage Qualcomm's advanced chipset technologies and Aptiv's software expertise to accelerate the delivery of secure and high-performance telematics services. The joint initiative focuses on enhancing vehicle-to-everything communication capabilities, cybersecurity features, and cloud-based analytics platforms. Expected to influence market dynamics significantly, this partnership positions both companies at the forefront of innovation in the connected vehicle ecosystem. Source: Aptiv Corporate News

- •22nd May 2025, Continental AG unveiled its latest sensor technologies integrated with AI-driven communication modules designed for emergency response vehicles. The advanced system enables faster data transmission and improved situational awareness, facilitating more effective coordination during critical incidents. Continental's innovation supports regulatory compliance and aligns with global smart city initiatives, reinforcing its market leadership. The product launch is anticipated to drive adoption in public safety fleets worldwide, enhancing operational efficiency and safety outcomes. Source: Continental Annual Report

- •30th July 2025, Garmin Ltd. expanded its telematics portfolio with the release of cloud-based fleet management software aimed at small and medium-sized enterprises. The solution features real-time vehicle tracking, maintenance alerts, and driver behavior analytics, offering scalable options for diverse market segments. This expansion reflects Garmin's commitment to addressing evolving customer needs through user-friendly, cost-effective communication systems. The software integrates seamlessly with existing hardware, facilitating broad market penetration and competitive differentiation. Source: Garmin Press Release

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 8.5 Billion |

| Forecast Year Market Size | USD 27.9 Billion |

| CAGR | 12.4% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 12.5% |

| Scope of Report | Market is segmented by Product Type (Hardware Systems, Software Solutions, Communication Modules, Sensor Technologies, Data Analytics Platforms), Application (Fleet Management, Emergency Response, Passenger Information Systems, Vehicle Diagnostics, Telematics), End-Use Industry (Commercial Vehicles, Passenger Vehicles, Public Transportation, Emergency Services), Distribution Channel (Direct Sales, OEM Partnerships, Third-Party Distributors) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Bosch Mobility Solutions (Germany), Continental AG (Germany), Denso Corporation (Japan), Harman International (United States), Panasonic Automotive Systems (Japan), Aptiv PLC (Ireland), ZF Friedrichshafen AG (Germany), NXP Semiconductors (Netherlands), Qualcomm Technologies, Inc. (United States), Telematics Wireless Solutions (United States), Delphi Technologies (United Kingdom), Magneti Marelli (Italy), Valeo SA (France), Autoliv Inc. (Sweden), Garmin Ltd. (Switzerland), Sensata Technologies (United States), Veoneer Inc. (Sweden), Panasonic Corporation (Japan), TomTom NV (Netherlands), Nokia Corporation (Finland), Samsung Electronics (South Korea), Siemens AG (Germany), Texas Instruments Incorporated (United States), Renesas Electronics Corporation (Japan), Infineon Technologies AG (Germany) |

Global Vehicle-borne Intelligent Communication Systems Market Size, Growth & Revenue 2024-2034 - Table of Contents

Multidisciplinary researcher with 10+ years of experience uncovering insights across diverse domains focused on uncovering insights that drive informed decisions.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.