Global Industrial Hydrofluoric Acid Market Size, Growth & Revenue 2024-2034

Global Industrial Hydrofluoric Acid Market is segmented by Product Type (Anhydrous Hydrofluoric Acid, Aqueous Hydrofluoric Acid, Other Types), Application (Petrochemical Processing, Aluminum Production, Fluorocarbon Manufacture, Glass Etching, Other Industrial Uses), End-Use Industry (Chemical Manufacturing, Metallurgy, Electronics, Automotive), Distribution Channel (Direct Sales, Distributors, Online Platforms), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global Industrial Hydrofluoric Acid Market is a pivotal segment within the chemical industry, primarily involving the synthesis and application of hydrofluoric acid in diverse industrial processes. This highly reactive and corrosive acid is indispensable in petrochemical refining, facilitating alkylation units that enhance fuel quality and production efficiency. Additionally, its role in aluminum production as a flux agent and in fluorocarbon manufacturing for refrigerants and pharmaceuticals underscores its broad utility. The market's scope extends to encompass both anhydrous and aqueous forms of hydrofluoric acid, each tailored for specific applications and regulatory compliance needs. Safety and environmental considerations are integral, given HF's hazardous nature, influencing technological advancements and process optimizations. Geographically, the market is distributed across key regions including North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, each exhibiting unique demand drivers and regulatory landscapes. The increasing industrialization, expansion of downstream chemical industries, and stricter environmental policies collectively shape the market's trajectory, driving innovation and competitive dynamics globally.

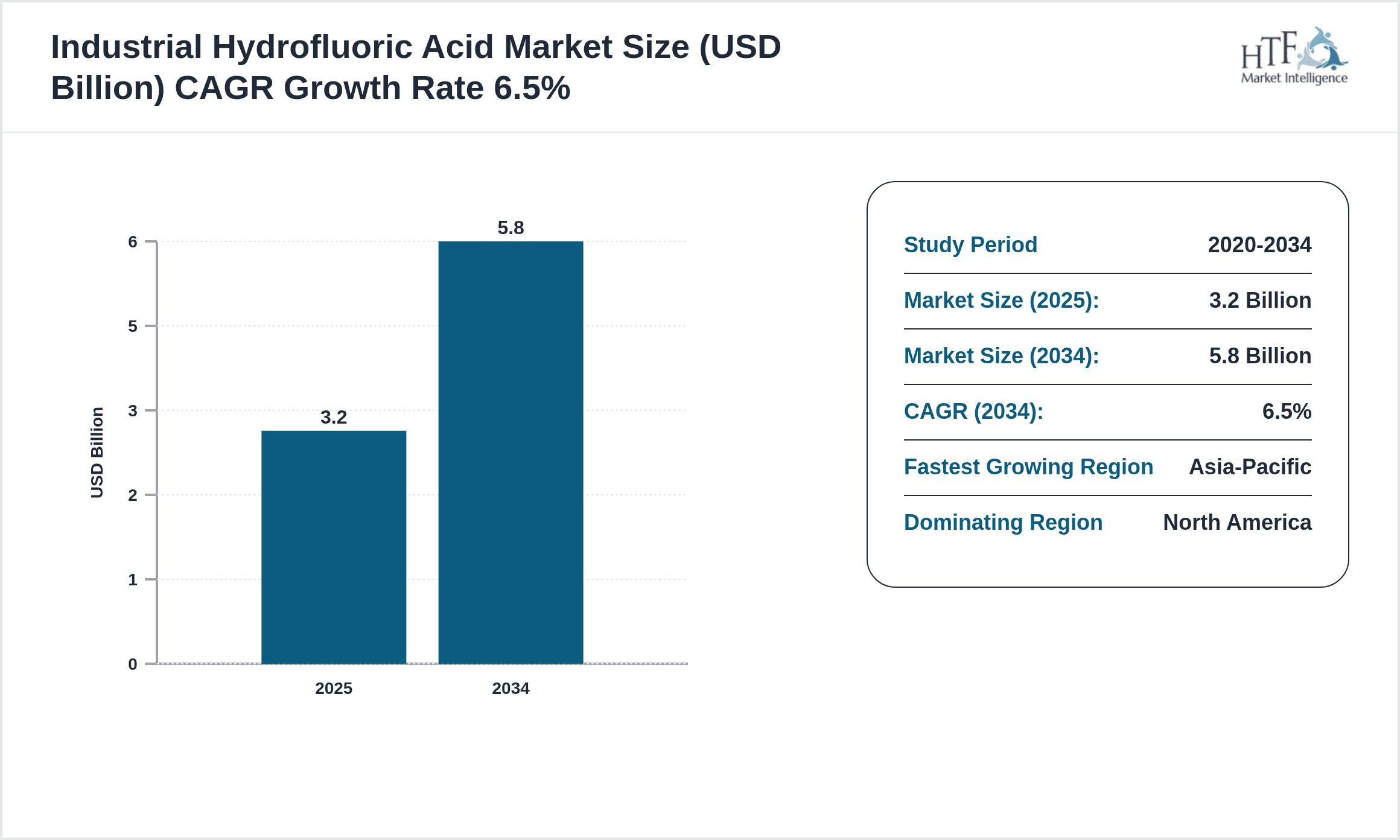

- •Key highlights of the market include a base size of USD 3.2 Billion in 2025, with projections to reach USD 5.8 Billion by 2034, registering a robust CAGR of 6.5%. The anhydrous hydrofluoric acid segment dominates due to its extensive usage in petrochemical and aluminum sectors, while aqueous HF is the fastest growing, propelled by safer handling techniques and expanding applications in glass etching and pharmaceuticals. North America leads in market share, supported by advanced petrochemical infrastructure and stringent quality standards. Meanwhile, Asia-Pacific emerges as the fastest-growing region, driven by rapid industrialization and expanding chemical manufacturing hubs in China and India. Market growth is underpinned by rising demand for high-purity hydrofluoric acid and innovations in delivery and containment systems, as well as increasing regulatory scrutiny fostering safer production practices.

- •The industrial hydrofluoric acid market offers significant value propositions to stakeholders by enabling critical chemical processes that enhance fuel production, metal processing, and specialty chemical manufacturing. Its strategic importance is evident in industries reliant on fluorinated compounds and aluminum products, which are foundational to automotive, aerospace, electronics, and refrigeration sectors. Market participants benefit from continuous innovation in product formulations and safety measures, addressing environmental and health concerns while optimizing operational efficiency. The evolving regulatory framework worldwide mandates stringent handling and emission controls, incentivizing adoption of advanced technologies and sustainable practices. Consequently, investors and manufacturers are presented with opportunities to expand into emerging markets, leverage technological advancements, and develop differentiated product portfolios, reinforcing hydrofluoric acid's essential role in industrial chemistry and global economic development.

Competitive Landscape

The global Industrial Hydrofluoric Acid Market is characterized by a competitive environment where major chemical manufacturers leverage innovation, strategic partnerships, and geographic expansion to strengthen market position. Competition centers on product purity, safety standards, and cost efficiency, with companies investing heavily in R&D to develop environmentally compliant production processes and safer delivery mechanisms. Market rivalry is intensified by the presence of established global leaders and regional players who focus on niche applications and localized supply chains. Strategic alliances and mergers and acquisitions are common to consolidate capabilities and expand product portfolios. Pricing strategies are influenced by raw material availability and regulatory compliance costs. Distribution network optimization and technological differentiation serve as key competitive advantages. Emerging markets are increasingly targeted through capacity expansions and tailored products, while companies adopt digitalization for supply chain transparency and operational efficiency. Overall, the competitive landscape is dynamic, driven by innovation, regulation, and the need for sustainable practices to mitigate HF's hazardous profile.

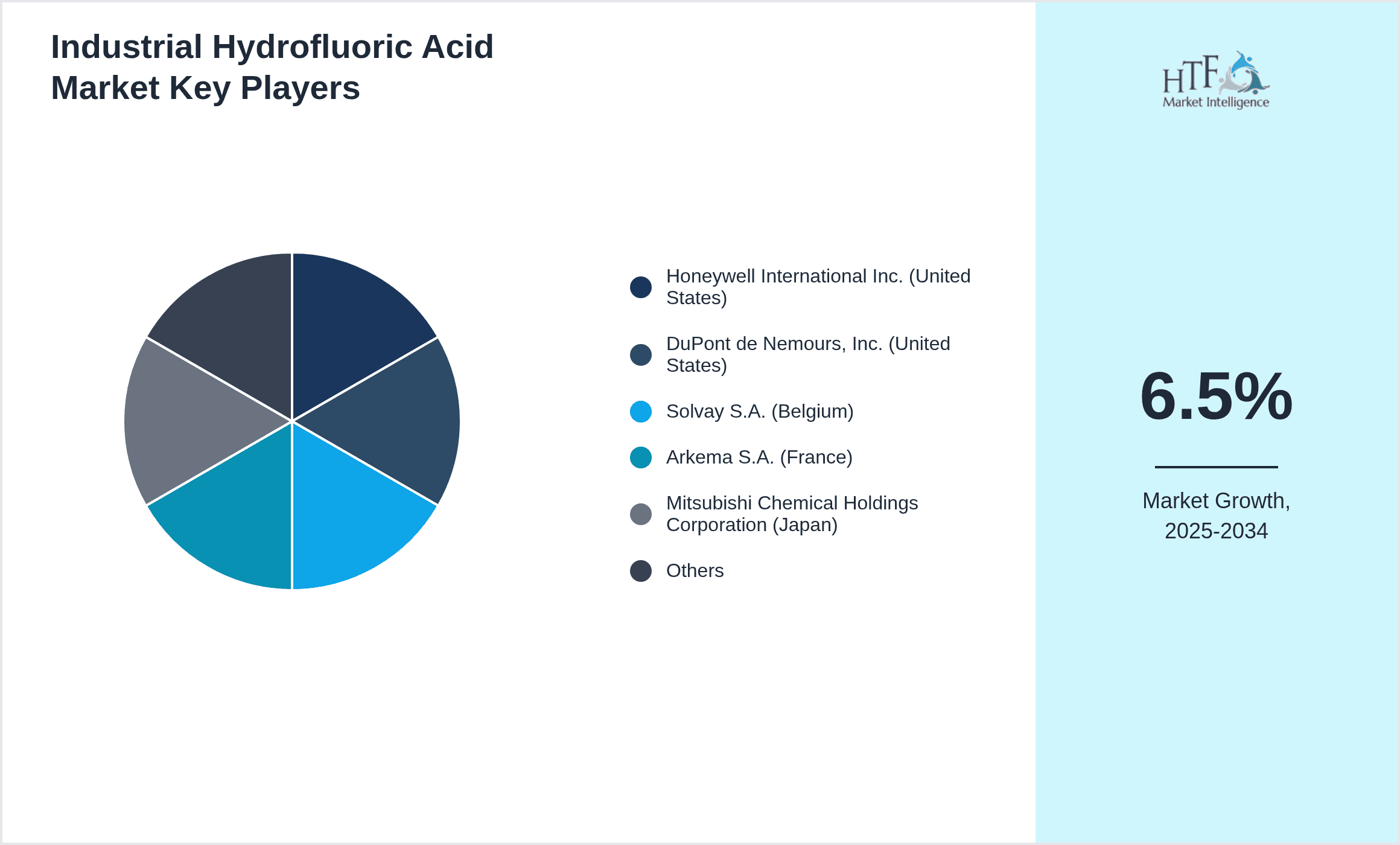

Leading Companies in Industrial Hydrofluoric Acid Market

- •Honeywell International Inc. (United States)

- •DuPont de Nemours, Inc. (United States)

- •Solvay S.A. (Belgium)

- •Arkema S.A. (France)

- •Mitsubishi Chemical Holdings Corporation (Japan)

- •Honeywell UOP (United States)

- •Honeywell Specialty Chemicals (United States)

- •Fuji Oil Company, Limited (Japan)

- •Honeywell Process Solutions (United States)

- •Honeywell Performance Materials and Technologies (United States)

- •China Fluorine Chemical Industry Co., Ltd. (China)

- •Mexichem S.A.B. de C.V. (Mexico)

- •Daikin Industries, Ltd. (Japan)

- •Honeywell International Inc. Specialty Chemicals Division (United States)

- •Gujarat Fluorochemicals Limited (India)

- •Honeywell Advanced Materials (United States)

- •Solvay Specialty Polymers (Belgium)

- •Arkema Fluorochemicals (France)

- •Honeywell Fluorine Products (United States)

- •Chemours Company (United States)

- •Honeywell UOP LLC (United States)

- •Dongyue Group Ltd. (China)

- •Honeywell International Inc. Performance Materials (United States)

- •Arkema Inc. (United States)

- •Honeywell Specialty Chemicals Group (United States)

Market Breakdown

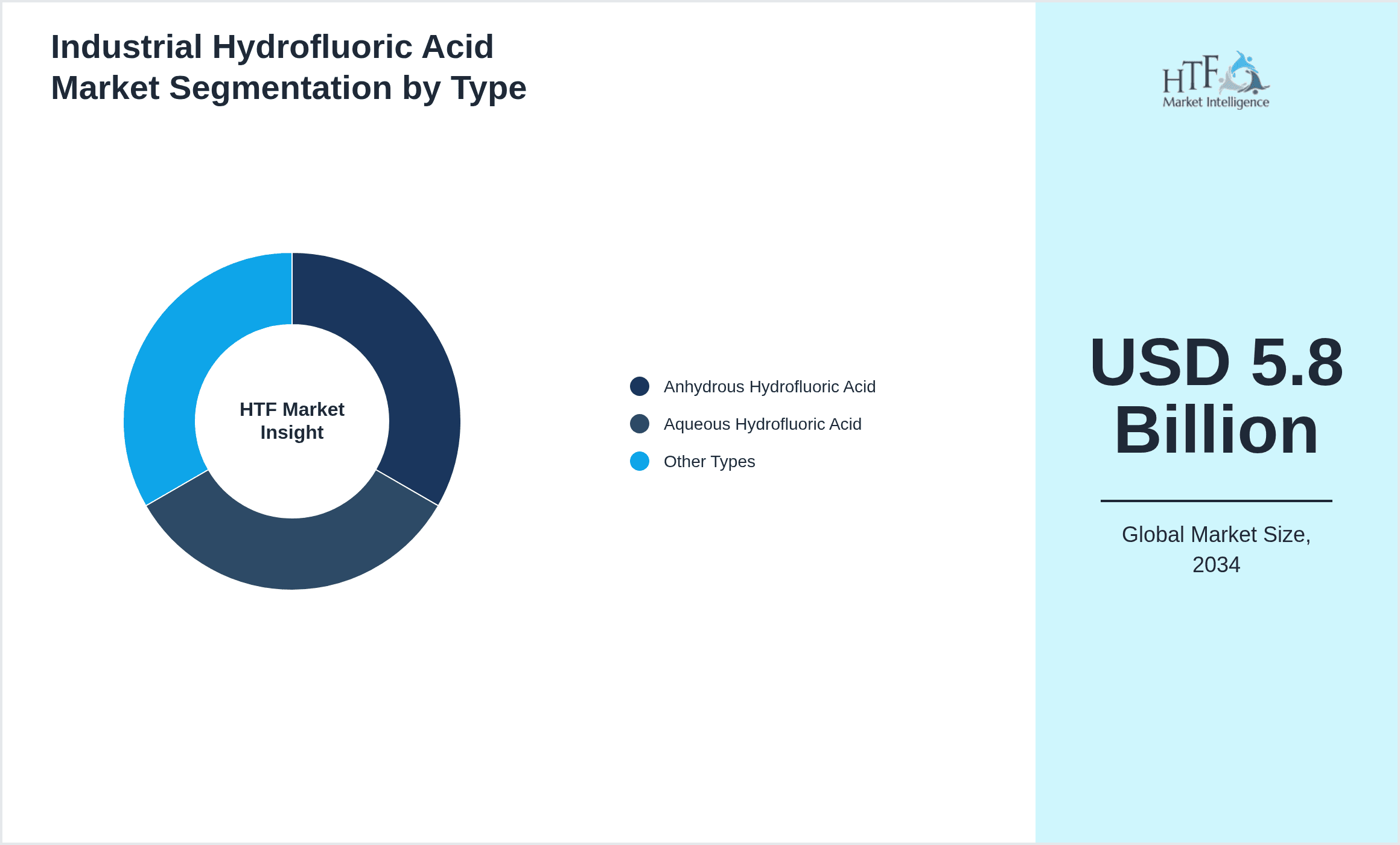

- •By Product Type

- ◦Anhydrous Hydrofluoric Acid

- ◦Aqueous Hydrofluoric Acid

- ◦Other Types

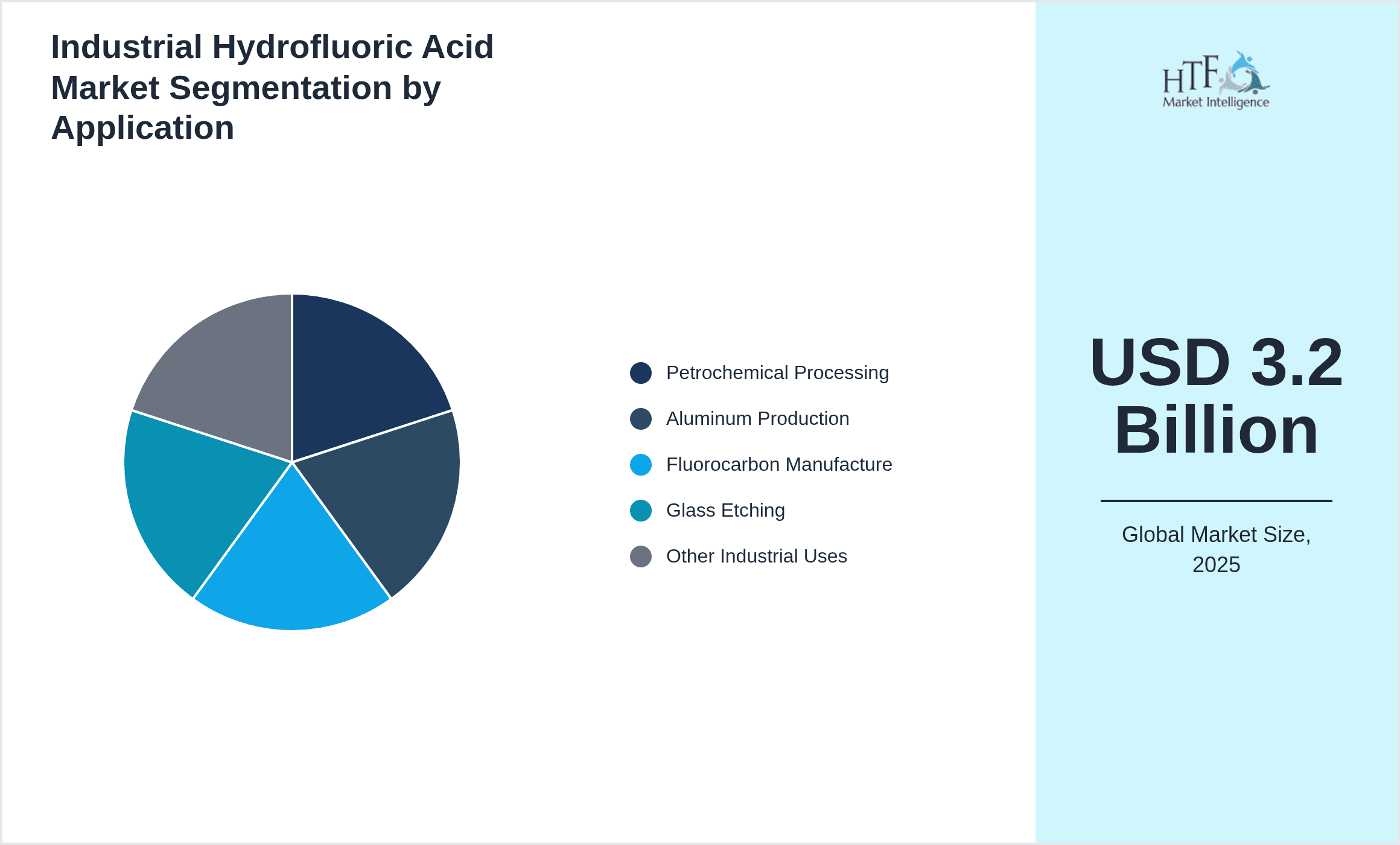

- •By Application

- ◦Petrochemical Processing

- ◦Aluminum Production

- ◦Fluorocarbon Manufacture

- ◦Glass Etching

- ◦Other Industrial Uses

- •By End-Use Industry

- ◦Chemical Manufacturing

- ◦Metallurgy

- ◦Electronics

- ◦Automotive

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors

- ◦Online Platforms

Growth Dynamics

The global Industrial Hydrofluoric Acid Market's growth is primarily driven by the expanding petrochemical sector, where HF acts as a critical catalyst in alkylation processes that enhance gasoline quality. The growing demand for cleaner fuels and stringent emission regulations worldwide are fueling investment in advanced refining technologies that rely heavily on high-purity hydrofluoric acid. Concurrently, burgeoning aluminum production, especially in emerging economies, sustains demand for HF as a fluxing agent, essential for metal purification and shaping. Technological advancements improving acid handling safety and reducing environmental impact have catalyzed adoption, broadening HF's application scope. Furthermore, the increasing production of fluorinated compounds for pharmaceuticals and refrigerants complements market growth by generating steady demand across diverse chemical manufacturing industries. These factors collectively contribute to the sustained expansion of the Industrial Hydrofluoric Acid Market globally.

Market Trends

A prominent trend shaping the Industrial Hydrofluoric Acid Market is the adoption of safer and more sustainable production technologies aimed at minimizing hazardous emissions and workplace accidents. Leading manufacturers are investing in closed-loop systems and advanced containment solutions to comply with evolving environmental and safety regulations. Another notable trend is the increasing integration of digital monitoring and automation in production and distribution processes, enhancing operational efficiency and real-time risk management. Additionally, there's a rising demand for aqueous hydrofluoric acid variants that offer safer handling properties for specific applications such as glass etching and electronics manufacturing. These trends indicate a market evolving towards improved safety, environmental stewardship, and technological sophistication to meet regulatory and customer expectations.

Market Opportunities

Emerging opportunities in the Industrial Hydrofluoric Acid Market include expansion into rapidly industrializing regions such as Asia-Pacific and Latin America, where growing petrochemical and aluminum sectors require increased HF supply. The development of specialty HF grades tailored for pharmaceutical and electronics applications presents avenues for product differentiation and premium pricing. Strategic collaborations with end-user industries can facilitate customized solutions and integrated supply chains. Additionally, innovations in green chemistry and sustainable HF production methods offer potential for market leadership and regulatory advantage. The increasing use of HF in novel applications like battery manufacturing and advanced materials further broadens the market scope, enabling companies to capitalize on evolving industrial needs and technological breakthroughs.

Market Challenges

The Industrial Hydrofluoric Acid Market faces significant challenges stemming from the hazardous nature of HF, which necessitates stringent safety, handling, and transportation protocols to prevent accidents and environmental contamination. Regulatory restrictions and compliance costs are substantial barriers, particularly in regions with rigorous environmental standards. Additionally, the volatility of raw material prices and supply chain disruptions can impact production costs and market stability. Public perception and community opposition related to HF's toxicity also affect plant siting and expansion plans. Furthermore, competition from alternative chemicals and emerging technologies poses a threat to traditional HF applications, requiring continuous innovation and risk mitigation strategies by market players.

Regulatory Framework

Between 2020 and 2025, regulatory authorities globally have intensified oversight on the production, storage, and transportation of hydrofluoric acid due to its high toxicity and environmental risks. Key regulations mandate stringent emission controls, mandatory safety training for handlers, and robust emergency response plans to mitigate accidental releases. Regions such as North America and Europe have updated chemical safety standards, including REACH and OSHA regulations, that require manufacturers to implement advanced containment and monitoring technologies. Additionally, regulatory frameworks increasingly emphasize reporting transparency and community right-to-know provisions. Governments are promoting green chemistry initiatives encouraging the development of safer HF alternatives and production methods, influencing industry investments and compliance strategies. These evolving regulations significantly impact market dynamics by increasing operational costs but also fostering innovation in safety and environmental technology adoption.

Market Intelligence

- •15th January 2025, Honeywell International Inc. launched an advanced hydrofluoric acid delivery system designed to enhance safety and reduce emissions in petrochemical plants. This system incorporates closed-loop containment and real-time monitoring sensors to detect leaks promptly, aiming to minimize environmental impact and workplace hazards. Targeted primarily at North American and European refineries, the innovation aligns with tightening regulatory requirements and growing industry demand for safer chemical handling solutions. Honeywell’s strategic objective is to consolidate its leadership in specialty chemicals by offering integrated solutions that improve operational efficiency while ensuring compliance. This launch is expected to drive adoption of advanced HF technologies globally, positioning Honeywell as a key innovator in the Industrial Hydrofluoric Acid Market. Source: Honeywell Official Press Release

- •10th October 2024, Solvay S.A. introduced a new grade of aqueous hydrofluoric acid tailored for the semiconductor and glass manufacturing industries. The product features enhanced purity levels and reduced corrosiveness, enabling safer and more efficient etching processes. This development responds to increasing demand for high-performance HF products in Asia-Pacific’s expanding electronics sector. Solvay’s innovation is part of a broader strategic initiative to diversify its fluorochemicals portfolio and penetrate emerging markets with specialized solutions. The launch supports the company’s commitment to sustainability by optimizing chemical usage and minimizing waste generation. Market analysts anticipate that this product will significantly impact market growth in the fastest-growing Asia-Pacific region. Source: Solvay Corporate Announcement

- •20th March 2025, DuPont de Nemours, Inc. announced a strategic partnership with a leading Asian petrochemical producer to co-develop environmentally friendly hydrofluoric acid production technologies. The collaboration aims to integrate green chemistry principles and advanced emission control systems to reduce the carbon footprint associated with HF manufacturing. This initiative targets compliance with stringent environmental regulations in Asia-Pacific and Europe, where industrial expansion is coupled with increasing ecological concerns. DuPont’s strategic move enhances its global footprint and accelerates innovation in sustainable chemical production. The partnership is expected to foster knowledge exchange and expedite the commercialization of next-generation HF products. Source: DuPont Industry News

- •5th June 2025, Arkema S.A. completed the expansion of its hydrofluoric acid production facility in Europe, increasing capacity by 20% to meet rising demand from the automotive and pharmaceutical sectors. The upgraded plant incorporates state-of-the-art safety and emission reduction technologies, reinforcing Arkema’s commitment to regulatory compliance and environmental stewardship. This expansion aligns with growing regional demand for HF in specialty applications and supports Arkema’s strategic objective to strengthen its position in the European Industrial Hydrofluoric Acid Market. The investment is also expected to enhance supply chain reliability and reduce lead times for customers across multiple industries. Source: Arkema Corporate Release

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 3.2 Billion |

| Forecast Year Market Size | USD 5.8 Billion |

| CAGR | 6.5% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 6.3% |

| Scope of Report | Market is segmented by Product Type (Anhydrous Hydrofluoric Acid, Aqueous Hydrofluoric Acid, Other Types), Application (Petrochemical Processing, Aluminum Production, Fluorocarbon Manufacture, Glass Etching, Other Industrial Uses), End-Use Industry (Chemical Manufacturing, Metallurgy, Electronics, Automotive), Distribution Channel (Direct Sales, Distributors, Online Platforms) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Honeywell International Inc. (United States), DuPont de Nemours, Inc. (United States), Solvay S.A. (Belgium), Arkema S.A. (France), Mitsubishi Chemical Holdings Corporation (Japan), Honeywell UOP (United States), Honeywell Specialty Chemicals (United States), Fuji Oil Company, Limited (Japan), Honeywell Process Solutions (United States), Honeywell Performance Materials and Technologies (United States), China Fluorine Chemical Industry Co., Ltd. (China), Mexichem S.A.B. de C.V. (Mexico), Daikin Industries, Ltd. (Japan), Honeywell International Inc. Specialty Chemicals Division (United States), Gujarat Fluorochemicals Limited (India), Honeywell Advanced Materials (United States), Solvay Specialty Polymers (Belgium), Arkema Fluorochemicals (France), Honeywell Fluorine Products (United States), Chemours Company (United States), Honeywell UOP LLC (United States), Dongyue Group Ltd. (China), Honeywell International Inc. Performance Materials (United States), Arkema Inc. (United States), Honeywell Specialty Chemicals Group (United States) |

Global Industrial Hydrofluoric Acid Market Size, Growth & Revenue 2024-2034 - Table of Contents

Research enthusiast focused on transforming data uncovering into actionable insights through data-driven decision-making.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.