Global Train Door Lights Market Size, Growth & Revenue 2024-2034

Global Train Door Lights Market is segmented by Product Type (LED Door Lights, Fluorescent Door Lights, Halogen Door Lights, Incandescent Door Lights, OLED Door Lights), Application (Passenger Trains, Freight Trains, Metro Systems, Light Rail, High-Speed Trains), End-Use Industry (Railway Operators, Train Manufacturers, Maintenance & Repair Services, Infrastructure Developers), Distribution Channel (Direct Sales, Distributors, Aftermarket Service Providers), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The Global Train Door Lights Market is a specialized segment within the railway lighting industry, focusing on illumination solutions designed explicitly for train doorways. This market covers an array of lighting technologies including LED, fluorescent, halogen, incandescent, and the emerging OLED lights that serve multiple rail transport modes such as passenger trains, freight trains, metro systems, light rails, and high-speed trains. The primary purpose of these lights is to enhance passenger safety by clearly indicating door operation status, improving visibility during boarding and disembarking, and contributing to overall train aesthetics. The market scope extends to both original equipment manufacturers (OEM) and aftermarket solutions, encompassing new train production and retrofit projects. Growth factors include rising investments in railway infrastructure modernization worldwide, increased emphasis on passenger safety standards, and the shift towards energy-efficient lighting technologies. The market is also influenced by regional rail transport developments, government regulations, and evolving technological innovations in lighting materials and controls. This comprehensive overview reflects the significance of train door lights as a critical safety and operational component in the global rail industry.

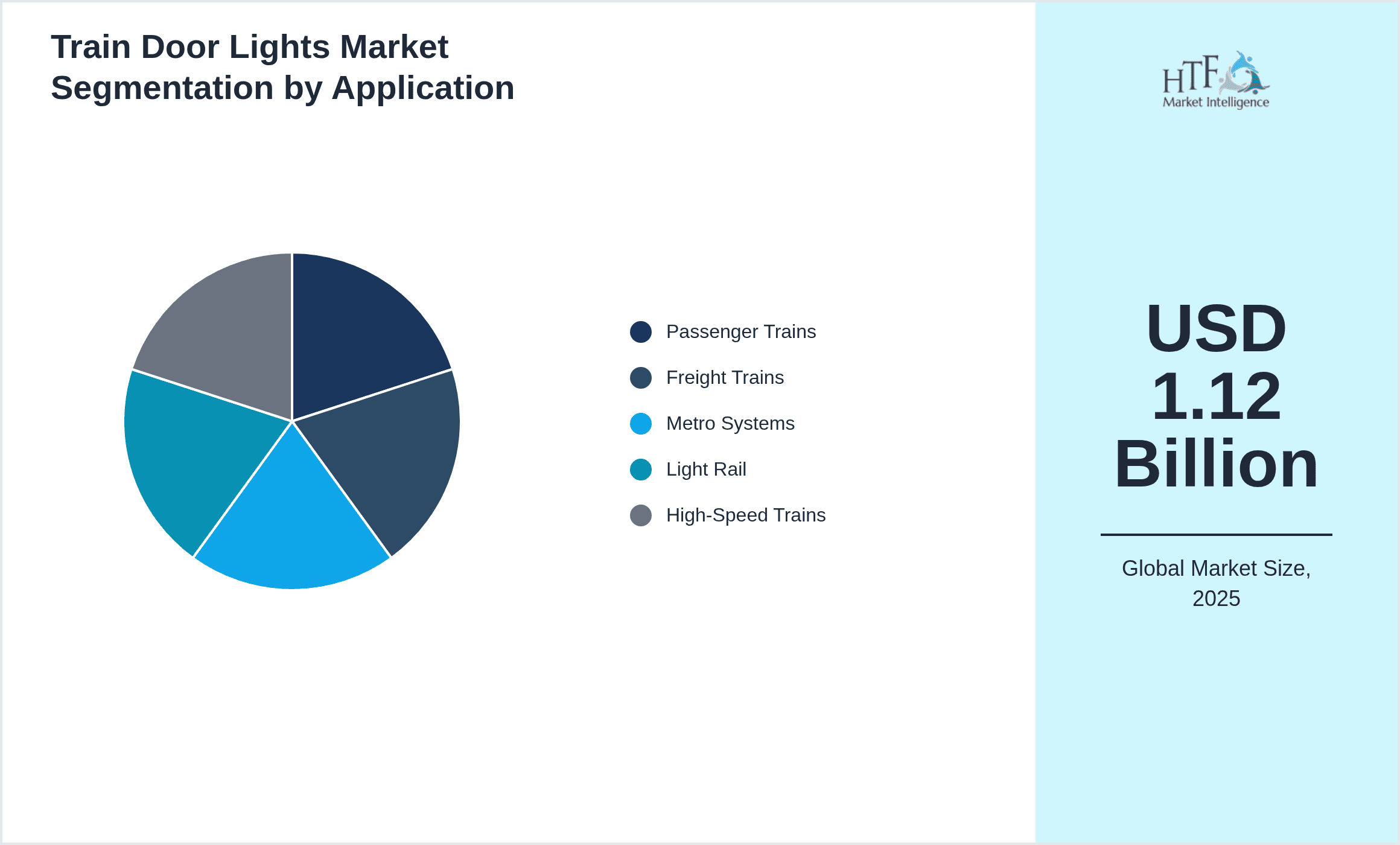

- •Key market highlights include a robust CAGR of 10.5% projected from 2024 to 2034, with market valuation expected to reach USD 2.91 Billion by 2034, up from USD 1.12 Billion in 2024. LED door lights currently dominate the market due to their energy efficiency, longevity, and low maintenance requirements, closely followed by fluorescent lighting solutions. Passenger trains constitute the largest application segment, driven by increasing global urbanization and the expansion of metro and light rail networks. Regionally, North America holds the largest market share, attributed to advanced rail infrastructure and stringent safety regulations, while Asia-Pacific is the fastest growing region, fueled by rapid railway modernization and government investments.

- •The value proposition of train door lights spans enhanced safety, operational efficiency, and compliance with international railway standards, making them indispensable for train operators, manufacturers, and maintenance service providers. Strategic importance is underscored by their role in accident prevention, passenger guidance, and energy conservation, which collectively contribute to reducing operational costs and improving passenger satisfaction. Stakeholders benefit from ongoing technological advancements such as smart lighting controls and integration with train control systems, which further elevate the safety and functional capabilities of train door lighting solutions. This market also offers lucrative opportunities for innovation in sustainable lighting technologies and expansion in emerging economies with growing rail transport demand.

Competitive Landscape

The Global Train Door Lights Market is characterized by a moderately concentrated competitive environment with a mix of multinational corporations and specialized regional players. Competition revolves around technological innovation, product quality, energy efficiency, and compliance with stringent safety standards. Leading companies focus on developing advanced LED and OLED lighting solutions that offer longer life cycles and enhanced visibility. The market sees aggressive strategies including strategic partnerships, joint ventures, and acquisitions to expand product portfolios and geographic reach. Differentiation is often achieved through customization capabilities, integration with train control systems, and offering smart lighting solutions with IoT connectivity. Pricing strategies are influenced by raw material costs, technological sophistication, and service agreements. Regional competition varies with North America and Europe emphasizing high-end technology adoption, while Asia-Pacific players compete on price and rapid deployment capabilities. Future trends indicate increased focus on sustainability, regulatory compliance, and digitalization within the competitive landscape.

Leading Companies in Train Door Lights Market

- •Siemens AG (Germany)

- •Alstom SA (France)

- •Bombardier Inc. (Canada)

- •GE Transportation (United States)

- •Knorr-Bremse AG (Germany)

- •Schneider Electric SE (France)

- •Mitsubishi Electric Corporation (Japan)

- •Hitachi Rail Ltd. (Japan)

- •Wabtec Corporation (United States)

- •Thales Group (France)

- •Cree, Inc. (United States)

- •Luminator Technology Group (United States)

- •Stanley Electric Co., Ltd. (Japan)

- •Hella GmbH & Co. KGaA (Germany)

- •Osram Licht AG (Germany)

- •Zumtobel Group AG (Austria)

- •Nichia Corporation (Japan)

- •Royale Lighting Group (United Kingdom)

- •GE Current, a Daintree company (United States)

- •Trilux GmbH & Co. KG (Germany)

- •Acuity Brands, Inc. (United States)

- •Panasonic Corporation (Japan)

- •Eaton Corporation plc (Ireland)

- •Osram Opto Semiconductors GmbH (Germany)

- •Fagerhult Group (Sweden)

Market Breakdown

- •By Product Type

- ◦LED Door Lights

- ◦Fluorescent Door Lights

- ◦Halogen Door Lights

- ◦Incandescent Door Lights

- ◦OLED Door Lights

- •By Application

- ◦Passenger Trains

- ◦Freight Trains

- ◦Metro Systems

- ◦Light Rail

- ◦High-Speed Trains

- •By End-Use Industry

- ◦Railway Operators

- ◦Train Manufacturers

- ◦Maintenance & Repair Services

- ◦Infrastructure Developers

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors

- ◦Aftermarket Service Providers

Growth Dynamics

- •Increasing investments in railway infrastructure modernization globally are driving demand for advanced train door lighting solutions that enhance safety and operational efficiency across various rail systems. Governments worldwide are prioritizing railway upgrades to improve urban mobility and freight transport, directly impacting market growth.

- •Advancements in LED and OLED technologies offer superior energy efficiency, longer lifespan, and reduced maintenance costs, making them the preferred choice for train door lighting. These innovations contribute to lowering operational expenditures for rail operators while improving passenger visibility and safety.

- •Rising safety regulations and standards imposed by international railway authorities mandate the installation of high-visibility door lighting systems to reduce accidents and enhance passenger experience, stimulating market expansion. Compliance requirements are fostering adoption of technologically sophisticated lighting products.

- •The growing trend towards smart rail systems and integration of IoT-enabled lighting controls facilitates real-time monitoring and adaptive illumination, creating new growth avenues within the train door lights market. This synergy between lighting and digital technologies is transforming traditional train lighting solutions.

- •Expansion of urban transit networks, especially metro and light rail systems in Asia-Pacific and Latin America, is fueling demand for efficient and reliable train door lighting products. Increasing urbanization and population density necessitate safer and more user-friendly rail transport environments.

- •Sustainability initiatives encouraging the replacement of traditional lighting with eco-friendly alternatives are boosting the adoption of LED and OLED door lights. Energy conservation goals and environmental concerns are significant drivers influencing purchasing decisions in the rail industry.

- •Collaborations between lighting manufacturers and train OEMs to develop customized and integrated lighting solutions are accelerating market growth. These partnerships enable the creation of tailored products that meet specific operational and aesthetic requirements of various rail systems.

Market Trends

- •The shift towards LED-based train door lighting solutions is a dominant market trend, motivated by their superior performance, lower energy consumption, and longer durability compared to traditional lighting types. This trend is reinforced by ongoing technological enhancements in LED efficacy and design.

- •Integration of intelligent lighting systems equipped with sensors and IoT connectivity is gaining traction, enabling adaptive illumination based on door status, passenger flow, and ambient conditions, thus enhancing safety and energy efficiency in rail operations.

- •Manufacturers are increasingly focusing on modular and customizable lighting solutions that can be easily installed and maintained, reducing downtime and operational costs for train operators. This modularity trend supports rapid deployment across diverse train models and applications.

- •Sustainability and eco-friendly lighting materials such as OLEDs are emerging trends aligned with global environmental policies, offering thinner, flexible, and more energy-efficient alternatives that can be seamlessly integrated into train door designs.

- •Collaborative innovation between lighting companies and railway authorities to develop standardized lighting solutions is shaping market evolution, fostering interoperability and compliance with international safety norms across different regions.

- •Market players are leveraging digital platforms and advanced analytics to monitor lighting performance and maintenance needs remotely, enabling predictive servicing and reducing unexpected failures in train door lighting systems.

- •The rising adoption of high-speed rail networks in Asia-Pacific and Europe is influencing design and functionality trends, requiring robust, high-intensity door lighting systems capable of withstanding extreme operational conditions.

Market Opportunities

- •There is a significant opportunity in emerging markets with expanding rail infrastructure, where demand for modern train door lighting is increasing rapidly due to urbanization and government initiatives promoting public transport.

- •The development of OLED door lights presents a lucrative avenue for innovation, offering improved energy efficiency, design flexibility, and aesthetic appeal for premium rail systems, opening new market niches.

- •Collaborations between technology providers and railway manufacturers to develop smart, connected lighting systems enable market players to differentiate products and capture value-added segments.

- •Retrofitting existing train fleets with advanced LED lighting to replace outdated fluorescent and halogen systems offers a considerable market potential driven by cost savings and regulatory compliance.

- •Expanding aftermarket services and maintenance contracts for train door lighting systems can improve customer retention and generate recurring revenue streams for manufacturers and distributors.

- •Innovations in sustainable and recyclable lighting materials align with global environmental goals, providing opportunities for companies to lead in green technology adoption within the rail industry.

- •Geographical expansion into underpenetrated regions such as Latin America and the Middle East offers scope for establishing early market presence and capitalizing on growing infrastructure investments.

Market Challenges

- •High initial costs associated with advanced LED and OLED lighting technologies can impede adoption among cost-sensitive rail operators, especially in developing regions with budget constraints.

- •Complex regulatory landscapes and varying safety standards across countries pose challenges for manufacturers attempting to develop universally compliant lighting solutions.

- •Technical limitations such as heat dissipation, durability under harsh environmental conditions, and integration with existing train systems require continuous R&D investment to overcome.

- •Supply chain disruptions and raw material price volatility affect production costs and delivery schedules, impacting market stability and profitability for lighting manufacturers.

- •Competition from low-cost regional manufacturers offering substandard products may undermine market growth and affect brand reputation of established players.

- •Resistance to change from traditional lighting systems among certain railway operators can slow the transition to energy-efficient and smart lighting technologies.

- •Maintaining a skilled workforce for installation, maintenance, and technological support remains a challenge in regions with limited technical expertise in advanced rail lighting solutions.

Regulatory Framework

- •Between 2019 and 2024, several international railway safety bodies introduced enhanced lighting standards mandating minimum luminance levels and visibility durations for train door lights, ensuring improved passenger safety. Compliance with these standards has become compulsory for new train manufacturing and retrofit projects.

- •The European Union enacted regulations requiring the use of energy-efficient lighting systems in all public transportation vehicles by 2022, driving the adoption of LED and OLED train door lights across member states. Enforcement mechanisms include periodic audits and penalties for non-compliance.

- •In North America, the Federal Railroad Administration updated its operational guidelines in 2021 to include specifications on door light color coding and flashing patterns to standardize safety signaling across different rail operators, facilitating interoperability and reducing passenger confusion.

- •Japan introduced a national mandate in 2023 focusing on environmentally sustainable lighting solutions for all rail vehicles, promoting the integration of recycled materials and low-energy consumption lighting technologies in train door lights.

- •Government initiatives in Asia-Pacific, including subsidies and tax incentives launched between 2020 and 2024, support railway operators in upgrading to smart, IoT-enabled lighting systems, fostering innovation and accelerating technology adoption in train door lighting.

Market Intelligence

- •15th January 2025, Siemens AG launched a new line of energy-efficient LED train door lights designed specifically for high-speed rail applications. These lights feature adaptive brightness control and enhanced durability to withstand extreme operating conditions. Siemens targets global rail operators seeking to upgrade aging fleets with smart, sustainable lighting solutions that reduce energy consumption and maintenance costs. The product integrates seamlessly with existing train control systems, enabling real-time monitoring and predictive maintenance capabilities, aligning with the digital transformation trends in the rail industry. Source: Siemens Official Press Release

- •10th March 2025, Alstom SA introduced an innovative OLED-based door lighting system for metro trains, combining ultra-thin panels with customizable color options to improve passenger safety and aesthetic appeal. This product launch marks Alstom's commitment to sustainability and technological leadership in rail lighting. The system offers significant energy savings compared to traditional lighting and supports integration with onboard passenger information systems. Alstom's strategic objective is to enhance urban transit environments while complying with emerging environmental regulations across Europe and Asia-Pacific. Source: Alstom Corporate News

- •20th May 2025, Wabtec Corporation announced a strategic partnership with a leading IoT solutions provider to develop smart train door lighting systems with sensor-based adaptive illumination and remote diagnostic features. This collaboration aims to accelerate the deployment of intelligent lighting technologies across North American and European rail networks. The initiative supports Wabtec’s growth strategy focusing on digitalization and operational efficiency improvements for rail operators. The partnership is expected to enhance safety standards and reduce lifecycle costs of train door lights significantly. Source: Wabtec Investor Relations

- •5th July 2025, Mitsubishi Electric Corporation completed the acquisition of a specialized train lighting manufacturer to expand its product portfolio in the Asia-Pacific market. This acquisition strengthens Mitsubishi Electric’s position in the railway lighting sector by incorporating advanced LED and OLED technologies with established manufacturing capabilities. The move supports the company’s long-term vision of offering integrated rail solutions that improve safety, reliability, and energy efficiency. The acquisition is also expected to enhance Mitsubishi Electric’s market reach in rapidly growing rail markets in Asia. Source: Mitsubishi Electric Press Release

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.12 Billion |

| Forecast Year Market Size | USD 2.91 Billion |

| CAGR | 10.5% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 10% |

| Scope of Report | Market is segmented by Product Type (LED Door Lights, Fluorescent Door Lights, Halogen Door Lights, Incandescent Door Lights, OLED Door Lights), Application (Passenger Trains, Freight Trains, Metro Systems, Light Rail, High-Speed Trains), End-Use Industry (Railway Operators, Train Manufacturers, Maintenance & Repair Services, Infrastructure Developers), Distribution Channel (Direct Sales, Distributors, Aftermarket Service Providers) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Siemens AG (Germany), Alstom SA (France), Bombardier Inc. (Canada), GE Transportation (United States), Knorr-Bremse AG (Germany), Schneider Electric SE (France), Mitsubishi Electric Corporation (Japan), Hitachi Rail Ltd. (Japan), Wabtec Corporation (United States), Thales Group (France), Cree, Inc. (United States), Luminator Technology Group (United States), Stanley Electric Co., Ltd. (Japan), Hella GmbH & Co. KGaA (Germany), Osram Licht AG (Germany), Zumtobel Group AG (Austria), Nichia Corporation (Japan), Royale Lighting Group (United Kingdom), GE Current, a Daintree company (United States), Trilux GmbH & Co. KG (Germany), Acuity Brands, Inc. (United States), Panasonic Corporation (Japan), Eaton Corporation plc (Ireland), Osram Opto Semiconductors GmbH (Germany), Fagerhult Group (Sweden) |

Global Train Door Lights Market Size, Growth & Revenue 2024-2034 - Table of Contents

Multidisciplinary researcher with 10+ years of experience uncovering insights across diverse domains focused on uncovering insights that drive informed decisions.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.