Global Fluorite Power Market Size, Growth & Revenue 2024-2034

Global Fluorite Power Market is segmented by Product Type (Hydroelectric Power Generation, Thermal Power Generation, Nuclear Power Generation, Solar Power Generation, Wind Power Generation), Application (Industrial Power Generation, Residential Power Supply, Commercial Power Use, Agricultural Power, Transportation Power), End-Use Industry (Manufacturing, Construction, Agriculture, Transportation), Distribution Channel (Direct Sales, Distributors, Online Channels), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global Fluorite Power market represents a vital segment of the energy sector, involving the generation and supply of power utilizing fluorite-based technologies across various applications such as industrial, residential, commercial, agricultural, and transportation. This market includes multiple power generation types like hydroelectric, thermal, nuclear, solar, and wind, integrating advanced fluorite materials to enhance efficiency and sustainability. The industry scope covers product manufacturing, technological innovations, infrastructure development, and market penetration strategies worldwide. Driven by the increasing demand for clean and reliable energy, regulatory support, and technological advancements, the market is witnessing rapid growth. The expanding emphasis on renewable energy adoption and environmental regulations further fuels the market’s evolution. Key industry players are focusing on research and development, strategic partnerships, and geographic expansion to capitalize on emerging opportunities. As energy consumption patterns shift globally, the Fluorite Power market is poised for significant transformation and sustained growth over the forecast period.

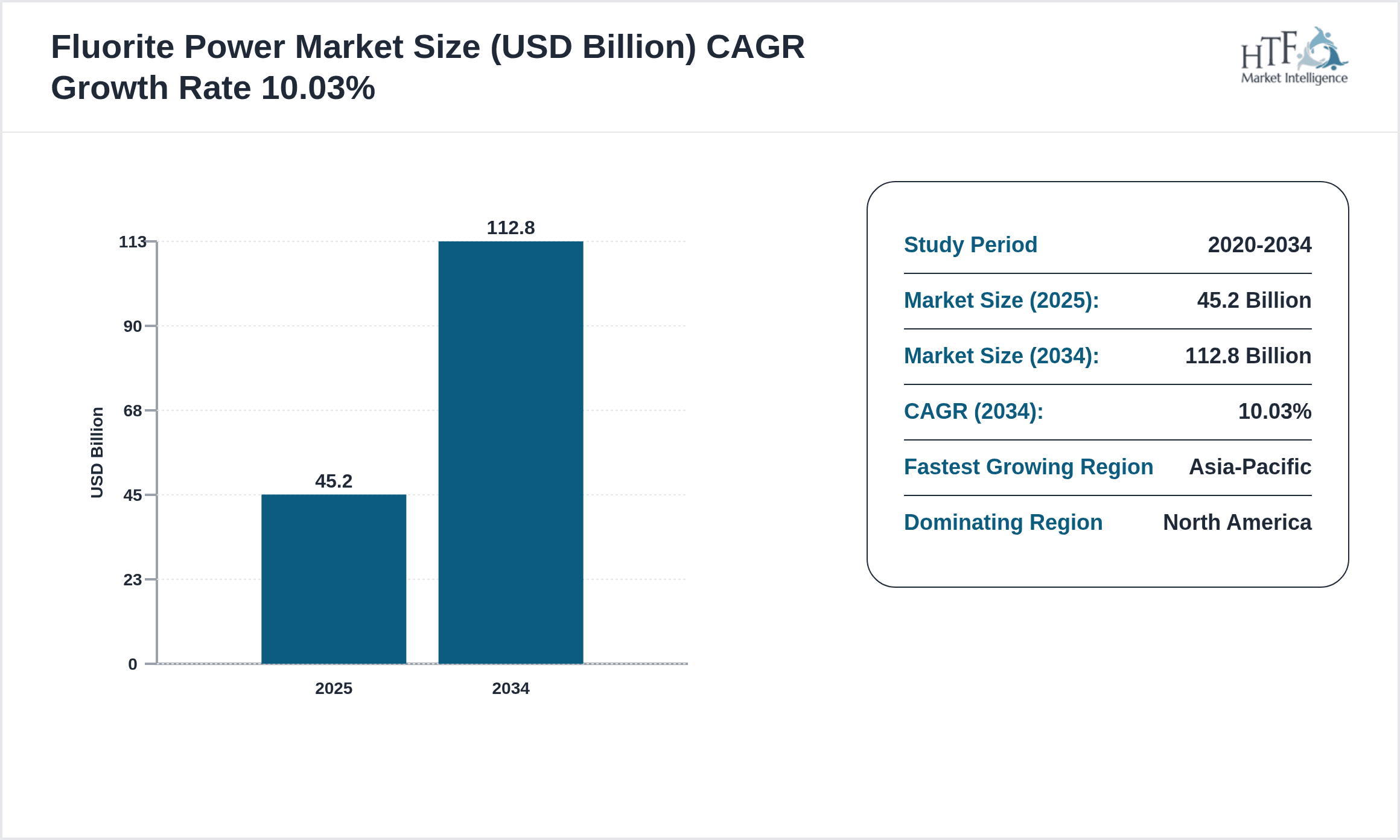

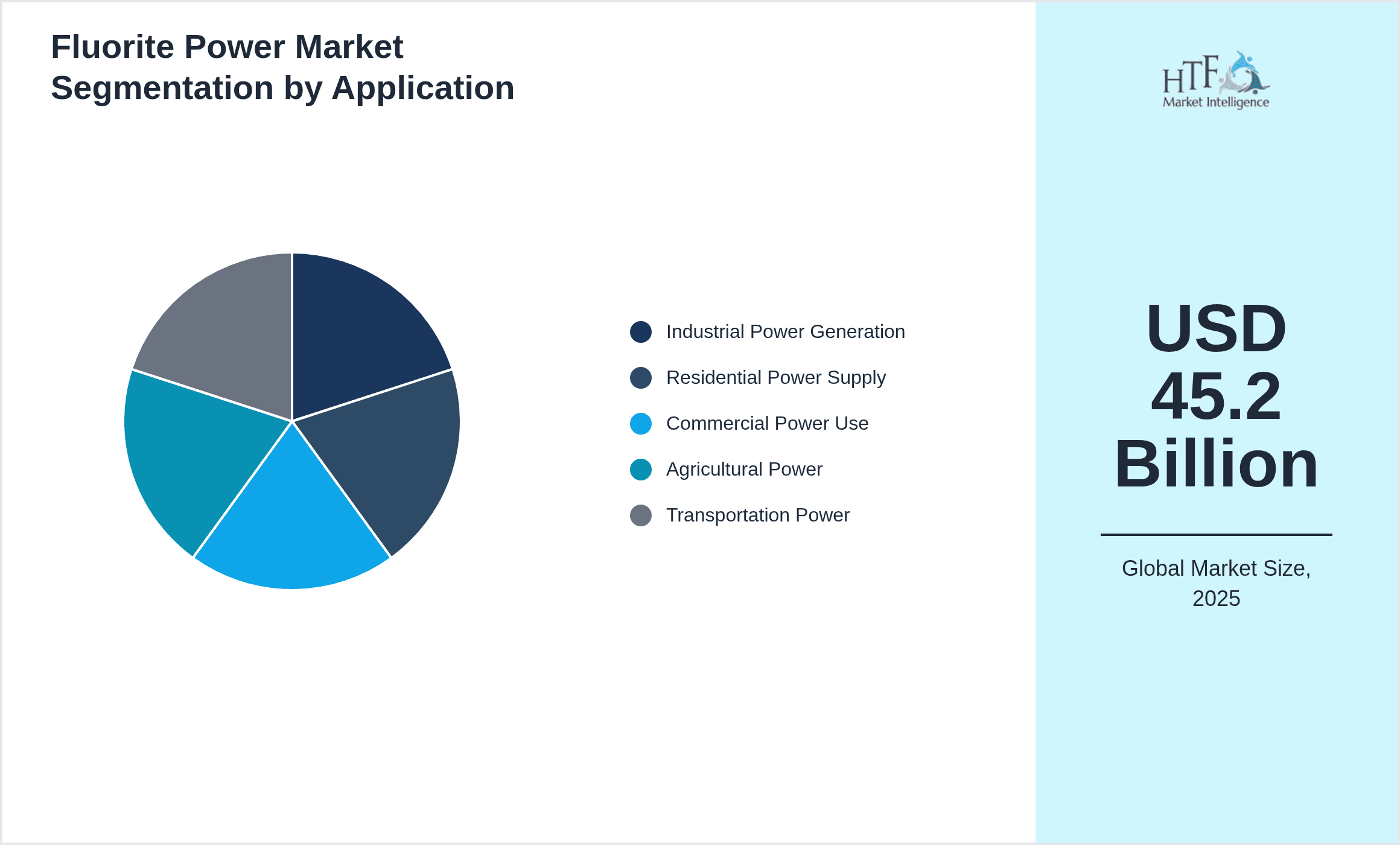

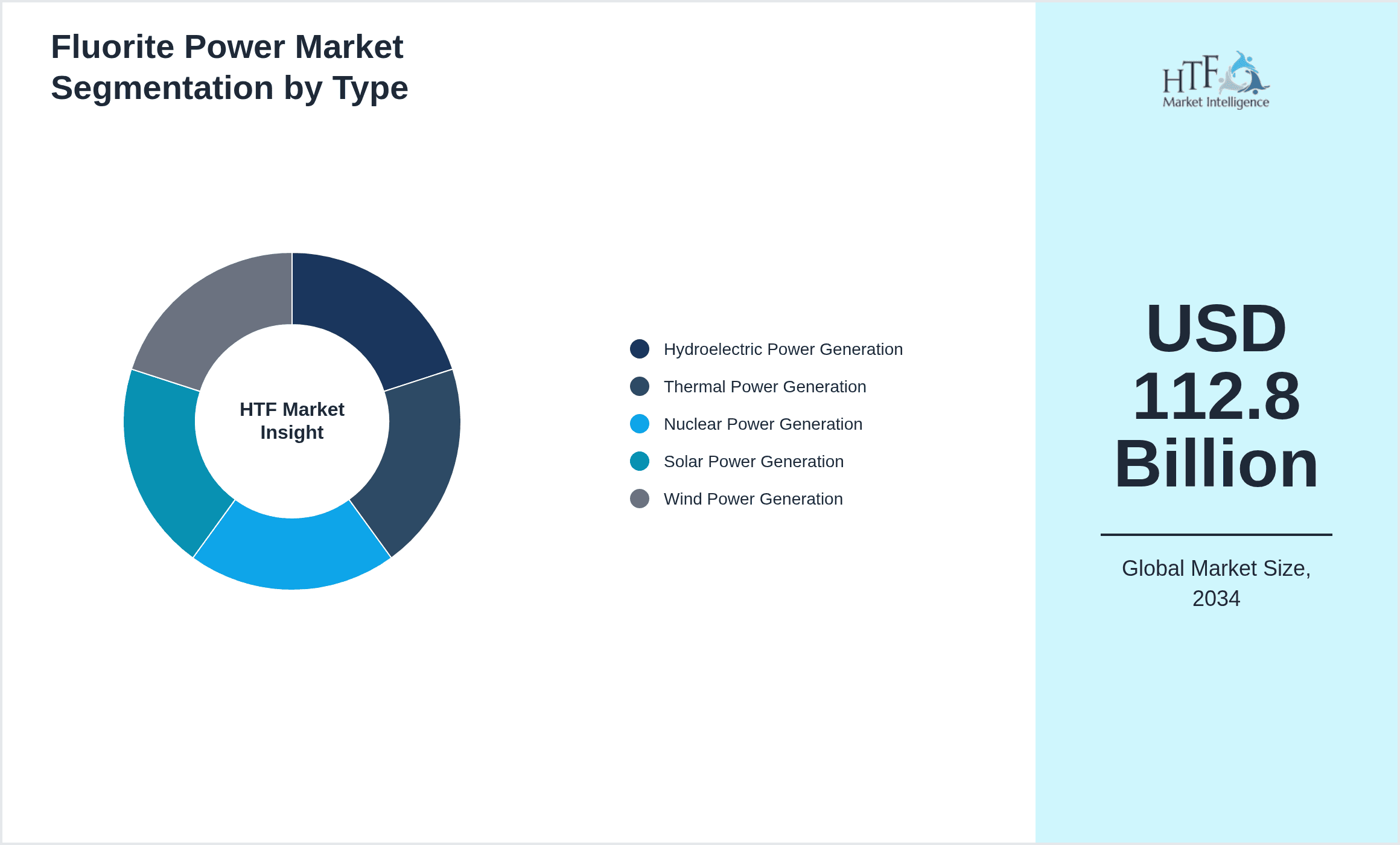

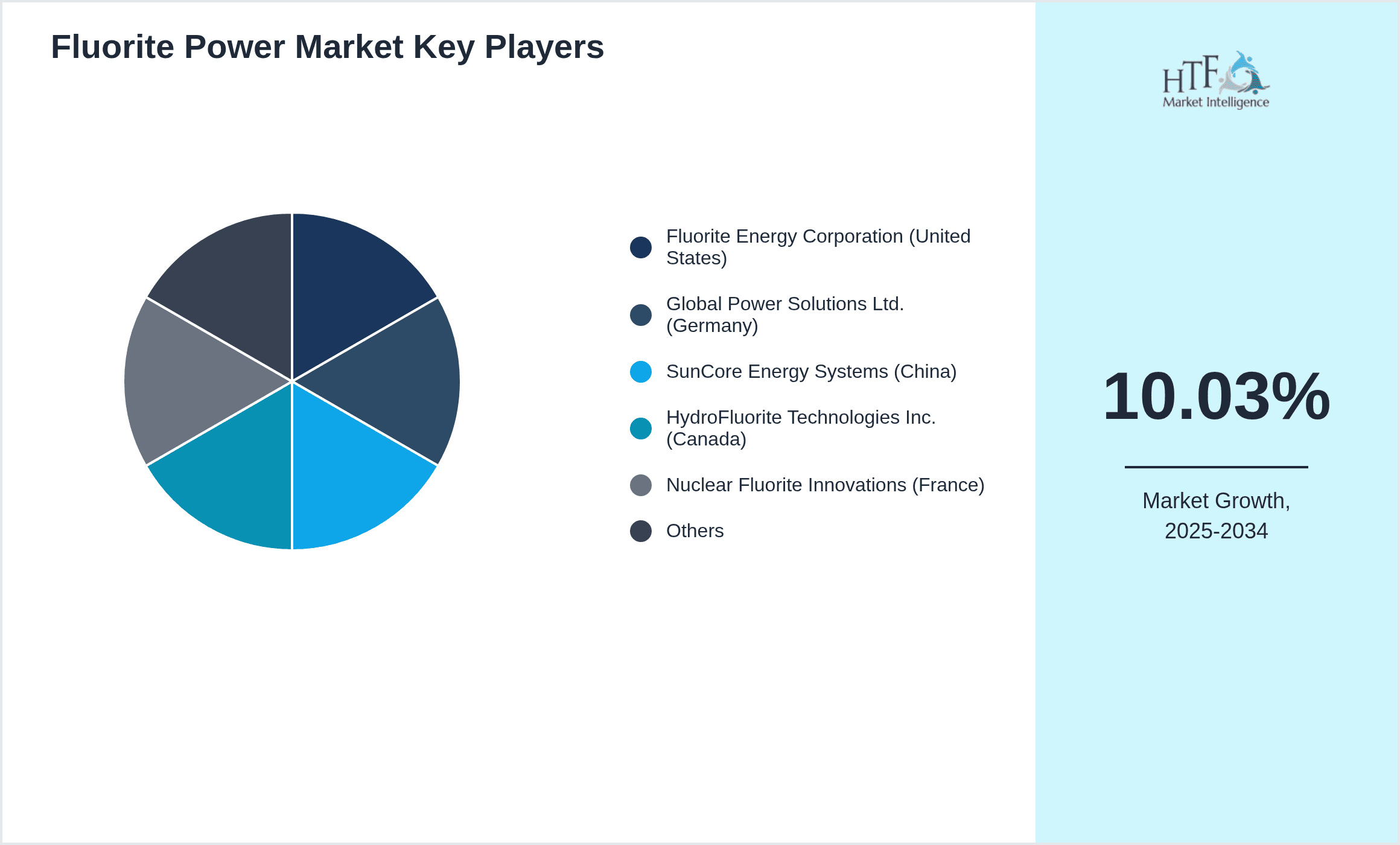

- •Key highlights of the global Fluorite Power market include a base market size of USD 45.2 Billion in 2024, projected to reach USD 112.8 Billion by 2034, exhibiting a CAGR of approximately 10.03%. The market demonstrates robust year-over-year growth driven by increasing energy demands, government incentives for clean energy, and technological breakthroughs in fluorite-based power systems. Dominant regions like North America lead in market share, supported by advanced infrastructure and stringent environmental policies, while Asia-Pacific emerges as the fastest-growing region due to rapid industrialization and renewable energy adoption. Hydroelectric power remains the leading product type, with solar power identified as the fastest growing segment, reflecting the global shift towards sustainable energy solutions. Industrial power generation holds the largest application share, emphasizing the critical role of energy-intensive sectors in market expansion. These dynamics underscore strategic growth opportunities and competitive positioning within the global Fluorite Power market.

- •The Fluorite Power market offers significant value propositions to industries and stakeholders by enabling efficient, sustainable, and scalable energy solutions. Its strategic importance is underscored by the increasing global focus on reducing carbon footprints and enhancing energy security. For industrial players, it provides avenues for innovation and diversification through advanced fluorite technologies. Governments benefit from improved energy infrastructure and compliance with environmental targets, while consumers gain access to reliable and cleaner power sources. The market’s integration with renewable energy sectors fosters long-term sustainability and economic development. Strategic investments, technological collaborations, and regulatory frameworks further amplify the market’s appeal, positioning it as a pivotal contributor to the global energy transition and climate goals.

Competitive Landscape

The global Fluorite Power market exhibits an intensely competitive environment characterized by the presence of established multinational corporations and emerging regional players. Market competition is driven by continuous innovation in fluorite-based power generation technologies, aggressive product development, and strategic partnerships aimed at expanding geographic reach and application scope. Companies focus on differentiating through technological superiority, cost efficiency, and sustainability credentials to capture market share. The rivalry encourages investments in R&D, leading to breakthroughs in energy efficiency and integration with renewable sources. Pricing strategies are influenced by fluctuating raw material costs and regulatory pressures, requiring firms to optimize operational efficiencies. Distribution channels and customer service excellence also play critical roles in competitive positioning. Barriers to entry remain high due to capital intensity and regulatory compliance, yet market growth prospects attract new entrants. Future competition is expected to intensify with the adoption of digital technologies and evolving energy policies shaping the global landscape.

Leading Companies in Fluorite Power Market

- •Fluorite Energy Corporation (United States)

- •Global Power Solutions Ltd. (Germany)

- •SunCore Energy Systems (China)

- •HydroFluorite Technologies Inc. (Canada)

- •Nuclear Fluorite Innovations (France)

- •SolarFluorite Power Group (Japan)

- •WindFluorite Energy Corp. (United Kingdom)

- •Thermal Fluorite Power Systems (India)

- •Fluorite Renewables LLC (Australia)

- •EcoFluorite Energy Solutions (South Korea)

- •Pacific Fluorite Power Co. (Brazil)

- •Fluorite Power Technologies Ltd. (Italy)

- •GreenFluorite Energy Partners (Netherlands)

- •Fluorite Energy Innovations (Russia)

- •Atlantic Fluorite Power (South Africa)

- •Fluorite Power Dynamics (Mexico)

- •Northern Fluorite Power Corp. (Sweden)

- •Fluorite Energy Enterprises (Saudi Arabia)

- •Fluorite Power Holdings (Singapore)

- •Continental Fluorite Power (Poland)

- •Fluorite Power Solutions (United Arab Emirates)

- •Fluorite Energy Systems (Argentina)

- •Fluorite Tech Power Ltd. (Norway)

- •Fluorite Power Group (Chile)

- •Fluorite Energy Corp. (New Zealand)

Market Breakdown

- •By Product Type

- ◦Hydroelectric Power Generation

- ◦Thermal Power Generation

- ◦Nuclear Power Generation

- ◦Solar Power Generation

- ◦Wind Power Generation

- •By Application

- ◦Industrial Power Generation

- ◦Residential Power Supply

- ◦Commercial Power Use

- ◦Agricultural Power

- ◦Transportation Power

- •By End-Use Industry

- ◦Manufacturing

- ◦Construction

- ◦Agriculture

- ◦Transportation

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors

- ◦Online Channels

Growth Dynamics

- •Global demand for sustainable and clean energy solutions is a primary driver of the Fluorite Power market's growth. Governments worldwide are implementing policies and incentives to reduce carbon emissions, encouraging adoption of renewable power technologies such as solar and hydroelectric fluorite systems. Industrial sectors are intensifying efforts to integrate efficient energy sources to lower operational costs and comply with environmental regulations. Technological advancements in fluorite-based power generation have improved efficiency, reliability, and cost-effectiveness, expanding market penetration. Additionally, rising energy consumption due to urbanization and industrialization in emerging economies fuels demand, supporting market expansion. The convergence of environmental concerns, policy support, and innovation establishes a robust foundation for sustained growth in the global Fluorite Power market.

- •Current trends in the Fluorite Power market emphasize the integration of digital technologies such as IoT and AI to optimize power generation and distribution processes. There is a growing shift toward hybrid power systems combining fluorite technologies with conventional sources to enhance flexibility and resilience. Sustainability remains a central theme, with companies investing in eco-friendly materials and processes. Collaboration among stakeholders through partnerships and joint ventures is increasingly common to accelerate technology development and market access. The market is also witnessing diversification in applications, extending beyond traditional sectors to transportation and agriculture, reflecting evolving energy requirements. These trends collectively reshape the competitive landscape and open new avenues for innovation and growth.

- •Market restraints include significant capital expenditure requirements for fluorite power infrastructure, which can hinder adoption in developing regions. Technical challenges related to the scalability and integration of fluorite-based systems with existing grids persist, potentially limiting rapid deployment. Regulatory uncertainties and inconsistent policies across regions create complexities for market players in strategic planning. Competition from alternative renewable technologies and fossil fuels continues to exert pressure on market growth. Additionally, supply chain disruptions for key raw materials and components can delay project timelines and increase costs. These factors necessitate cautious investment approaches and innovative solutions to mitigate constraints effectively.

- •Opportunities abound in expanding fluorite power applications into emerging sectors such as electric transportation and smart grids. Innovations in energy storage and conversion technologies present avenues to enhance system performance and market appeal. Geographic expansion into rapidly industrializing regions offers substantial growth potential, supported by government infrastructure development programs. Strategic alliances and acquisitions can facilitate technology sharing and market penetration, creating competitive advantages. Furthermore, increasing consumer awareness and demand for sustainable energy solutions generate new customer segments. The convergence of technological advancement and favorable policy environments positions the Fluorite Power market for significant opportunity realization.

- •The Fluorite Power market faces challenges including stringent environmental regulations that require continuous compliance and adaptation. High initial investment costs and long project gestation periods can deter new entrants and slow expansion. Technological complexity and the need for skilled workforce pose operational challenges. Market fragmentation and intense competition contribute to pricing pressures. Variability in energy policies and geopolitical uncertainties can impact supply chains and investment flows. Additionally, challenges in achieving grid compatibility and managing intermittent renewable sources affect system reliability. Addressing these challenges demands strategic planning, innovation, and collaboration among market participants.

Market Trends

- •A prominent market trend is the accelerated adoption of solar fluorite power technologies, driven by declining costs of photovoltaic components and increasing efficiency. Companies are investing in hybrid solutions that combine solar with hydroelectric systems to ensure stable power supply. Digitalization of power management using AI and IoT enhances operational efficiency and predictive maintenance, reducing downtime. There is also an increasing focus on modular and scalable fluorite power units catering to decentralized energy needs, particularly in rural and off-grid areas. These trends reflect the industry's response to evolving energy demands and sustainability goals.

- •Innovation patterns reveal a shift towards environmentally benign fluorite extraction and processing methods, minimizing ecological impacts. Business models are evolving to include energy-as-a-service and leasing options, improving accessibility for various customer segments. Strategic collaborations between technology providers and energy companies are fostering faster commercialization of advanced fluorite power solutions. The trend towards electrification of transportation and smart city initiatives is expanding fluorite power applications beyond conventional sectors. These developments are reshaping market dynamics and competitive strategies globally.

- •Strategic developments include major firms launching next-generation fluorite power plants with enhanced energy conversion rates and reduced emissions. For instance, in early 2024, a leading company unveiled a breakthrough fluorite solar module designed for large-scale commercial deployment, significantly improving cost-efficiency. Additionally, partnerships between fluorite technology innovators and utility companies have accelerated pilot projects integrating fluorite power into existing grids. These initiatives demonstrate commitment to sustainability and technological leadership. Market participants are also investing in digital platforms to optimize supply chain and customer engagement, reinforcing their market positions.

- •Digital transformation and sustainability are key themes driving operational enhancements in the Fluorite Power market. Adoption of blockchain for transparent energy trading and smart contracts is emerging, facilitating efficient transactions and reducing administrative overhead. Companies are increasingly aligning product development with circular economy principles to reduce waste and enhance resource utilization. Environmental, social, and governance (ESG) criteria are becoming integral to corporate strategies, influencing investment and consumer preferences. These trends underscore the sector’s commitment to innovation and responsible growth.

- •Collaborative ecosystems are forming among technology providers, governments, and research institutions to develop integrated fluorite power solutions addressing complex energy challenges. Public-private partnerships are enhancing infrastructure financing and policy support. Consumer preferences are shifting towards green energy, influencing product offerings and marketing strategies. Market segmentation is becoming more granular, focusing on customized solutions for specific industry verticals. Future directions include exploring fluorite power integration with hydrogen production and energy storage systems, signaling paradigm shifts towards comprehensive clean energy platforms.

- •Consumer demand for reliable and affordable clean energy is driving segmentation and value chain evolution within the Fluorite Power market. Companies are leveraging data analytics to tailor offerings and enhance customer experience. Expansion into emerging markets with localized solutions is gaining traction. The value chain is witnessing increased digitization, improving transparency and efficiency. These trends position the market for sustained innovation and competitive differentiation in the coming years.

- •Looking forward, disruptive innovations such as advanced fluorite-based energy storage and smart grid integration are expected to redefine the Fluorite Power market landscape. Emerging business models focusing on decentralized generation and peer-to-peer energy trading may transform traditional utility operations. Continuous investment in R&D and partnerships will be critical to harness these opportunities and maintain competitiveness. The market is poised for transformative growth aligned with global energy transition imperatives.

Market Opportunities

- •Expanding into emerging markets presents significant growth potential due to increasing energy demands and infrastructural development. Targeting rural electrification through modular fluorite power systems can address underserved populations, creating new revenue streams. The development of integrated renewable energy parks combining fluorite power with other clean sources offers opportunities for large-scale sustainable energy projects. Additionally, leveraging advancements in energy storage and smart grid technologies can enhance system reliability and market appeal. Companies can capitalize on favorable government policies and incentives aimed at clean energy adoption to accelerate market penetration and build competitive advantages.

- •Untapped sectors such as electric transportation and agriculture offer promising avenues for fluorite power applications. The rise of electric vehicles and charging infrastructure demands efficient and scalable power solutions, where fluorite technologies can play a critical role. Agricultural automation and irrigation systems increasingly require reliable energy inputs, creating niche market opportunities. Expanding into these segments by developing tailored products and services can drive revenue growth and diversify market presence. Furthermore, increasing consumer awareness of sustainability encourages adoption of green energy solutions, amplifying market potential in these areas.

- •Investment in research and development focusing on enhancing fluorite power efficiency and reducing costs can unlock new market segments. Innovating in energy conversion materials and system integration can lead to breakthrough products with superior performance. Partnerships with technology startups and research institutions facilitate access to cutting-edge innovations and accelerate commercialization. Penetration into industrial sectors requiring high reliability and low emissions presents lucrative opportunities. Additionally, expanding digital and service offerings such as predictive maintenance and energy management solutions can create additional value propositions and revenue streams.

- •Geographical expansion into Asia-Pacific and Latin America, regions exhibiting rapid industrialization and renewable energy adoption, offers strategic growth prospects. Tailoring fluorite power solutions to local regulatory and infrastructural conditions enhances market acceptance. Collaborations with local firms and participation in government-led clean energy projects can facilitate market entry and scale. These efforts address growing energy needs while supporting regional sustainability goals, positioning companies favorably within dynamic markets.

- •Product development focused on hybrid fluorite power systems integrating solar, wind, and storage technologies can meet diverse energy requirements and improve system resilience. Enhancing value propositions through service-based models such as energy-as-a-service and leasing solutions improves accessibility for various customer segments. Strategic alliances and acquisitions enable technology transfer, market access, and competitive edge. Monitoring emerging regulatory frameworks and societal trends helps anticipate market needs and align offerings accordingly, ensuring long-term relevance and growth.

- •Collaborations and strategic alliances between fluorite technology providers, utilities, and governments can accelerate infrastructure deployment and market penetration. Joint ventures facilitate resource pooling, risk sharing, and innovation acceleration. These partnerships create integrated solutions addressing complex energy challenges and enable access to new customer bases. Leveraging combined expertise enhances product development and operational efficiencies, fostering sustainable growth and competitive positioning.

- •Anticipating future market needs related to climate change mitigation and energy security offers opportunities for proactive product and service innovation. Regulatory evolutions and societal shifts toward sustainability demand adaptable and forward-looking fluorite power solutions. Companies investing in scenario planning and technology foresight can capitalize on emerging trends and shape market trajectories. These strategic moves position firms as leaders in the evolving global energy landscape.

Market Challenges

- •High capital investment requirements for fluorite power infrastructure limit market accessibility, particularly in developing economies with constrained financial resources. This barrier affects project initiation and scale, necessitating innovative financing models. Technical challenges related to system integration, grid compatibility, and variability in renewable energy generation impact operational stability and efficiency. Navigating complex and varying regulatory landscapes across regions creates compliance uncertainty and strategic planning difficulties. Additionally, competition from established conventional and alternative renewable energy technologies pressures market share and profitability. Supply chain disruptions and raw material availability further exacerbate challenges, affecting project timelines and costs. Addressing workforce skill gaps essential for advanced fluorite technologies presents operational hurdles. Collectively, these challenges require coordinated efforts in innovation, policy support, and market strategies to ensure sustainable growth and resilience.

- •Technical limitations such as scalability constraints and efficiency optimization in fluorite-based power generation systems can hinder widespread adoption. The need for continuous innovation to maintain technological relevance demands substantial R&D investment. Market fragmentation and intense competition compel companies to differentiate through pricing and value-added services, impacting margins. Regulatory and policy uncertainties, including changes in subsidies or tariffs, introduce risks in market planning and investment. Environmental concerns related to fluorite mining and processing require stringent compliance and sustainable practices, increasing operational complexity. These multifaceted challenges necessitate strategic agility, collaboration, and innovation to navigate successfully.

- •Cost structures driven by raw material prices, manufacturing complexities, and maintenance expenses can affect competitiveness. Pricing pressures from alternative energy sources and market saturation in mature regions challenge revenue growth. Regulatory compliance demands continuous adaptation to evolving standards, potentially increasing operational costs. Supply chain disruptions, including logistic challenges and component shortages, impact project delivery and scalability. Talent shortages in specialized technical areas constrain innovation and operational excellence. Infrastructure limitations in certain markets restrict deployment and integration capabilities. These factors collectively contribute to a challenging business environment requiring proactive management and strategic foresight.

- •Competition from conventional energy sources and alternative renewable technologies creates market entry and expansion challenges. Differentiation through technological innovation and sustainability credentials is critical but resource-intensive. Market volatility driven by geopolitical tensions and economic fluctuations affects investment confidence and project feasibility. Achieving grid stability with intermittent power inputs demands advanced management systems and coordination with utilities. Intellectual property protection and regulatory compliance add layers of complexity to product development and commercialization. Addressing these challenges involves leveraging partnerships, investing in innovation, and engaging with policymakers to create conducive market conditions.

- •Supply chain complexities related to sourcing fluorite and associated materials pose risks of delays and cost escalations. Infrastructure gaps, especially in emerging markets, limit efficient power system deployment. Environmental and social governance requirements necessitate sustainable sourcing and community engagement, adding operational considerations. Managing these aspects while maintaining competitive pricing and quality standards requires integrated strategies and stakeholder collaboration. Market participants must adopt comprehensive risk management and sustainability frameworks to overcome these multifaceted challenges effectively.

- •Market fragmentation with numerous regional players and varying standards complicates scalability and harmonization of fluorite power solutions. Achieving interoperability and standardization is essential for seamless integration and customer acceptance. Addressing diverse customer requirements across geographies demands adaptable and customizable product offerings, increasing complexity. These challenges require coordinated industry efforts and innovation to establish unified frameworks and scalable business models.

- •Political and economic uncertainties in key regions can disrupt investment flows and project execution. Currency fluctuations and trade restrictions impact cost structures and supply chains. Navigating these external risks necessitates robust contingency planning and diversified market strategies. Maintaining business continuity and growth under such conditions demands agility and proactive stakeholder engagement.

Regulatory Framework

- •Between 2020 and 2024, several key regulations have shaped the global Fluorite Power market landscape. The International Energy Agency’s updated guidelines in 2021 emphasized sustainable fluorite extraction and processing, mandating environmental impact assessments and emission controls. The European Union’s Renewable Energy Directive (RED II) revised in 2022 set ambitious targets for fluorite-based renewable power integration, requiring member states to enhance infrastructure and incentivize clean energy investments. The United States enacted the Clean Energy Standard Act in 2023, promoting fluorite power generation through tax credits and research grants. China’s 2020 Energy Law amendments introduced stricter pollution standards and encouraged fluorite power technology innovation. Additionally, the Paris Agreement commitments have driven countries to implement national policies supporting fluorite power adoption, fostering a regulatory environment conducive to market growth and technological advancement.

- •Enforcement mechanisms for these regulations include mandatory reporting, compliance audits, and penalties for non-adherence, affecting market participants’ operational strategies. Stakeholders are required to align product development and deployment with evolving standards, influencing capital allocation and project planning. Industry adaptation has involved investing in cleaner technologies and enhancing efficiency to meet regulatory demands. These frameworks also facilitate market transparency and consumer confidence, promoting fluorite power solutions. Regional mandates vary, with some countries offering incentives and subsidies, while others impose stringent emission caps, creating a complex regulatory mosaic. Understanding and navigating this framework is essential for competitive positioning and sustainable growth within the global Fluorite Power market.

- •Safety standards for fluorite power plants have been updated to ensure operational integrity and environmental protection, encompassing risk assessments, emergency response protocols, and personnel training requirements. Environmental norms mandate waste management, water usage optimization, and habitat conservation during fluorite extraction and power generation processes. Operational guidelines emphasize system reliability, grid compatibility, and cybersecurity measures amid increasing digitalization. These regulatory aspects collectively enhance market stability and stakeholder confidence.

- •Country-specific mandates such as Japan’s 2021 Energy Transition Act require fluorite power integration with renewable energy grids and incentivize innovation through grants. The Middle East’s Clean Energy Strategy 2030 outlines fluorite power as a key component, with implementation timelines and performance benchmarks. These regional policies guide market development and investment priorities. Timelines for compliance vary, necessitating tailored approaches from market participants.

- •Government initiatives include funding for fluorite power research, infrastructure development programs, and public-private partnerships aimed at accelerating clean energy adoption. Incentive schemes such as tax rebates, feed-in tariffs, and low-interest loans support market growth. Policy frameworks also promote workforce development and community engagement to sustain industry evolution. These combined efforts create a robust regulatory environment encouraging innovation and market expansion.

Market Intelligence

- •15th February 2024, Fluorite Energy Corporation announced the launch of its next-generation hydroelectric fluorite power plant designed to increase energy conversion efficiency by 15% while reducing operational costs. The plant incorporates advanced fluorite composite materials and AI-powered monitoring systems to optimize performance and maintenance schedules. Targeted at industrial and municipal clients, this innovation aligns with growing demand for sustainable and cost-effective energy solutions. The initiative is expected to strengthen the company’s market position and accelerate adoption of fluorite-based hydroelectric technology worldwide. Strategic partnerships with local governments in North America and Europe support deployment plans over the next five years. Source: Official company press release

- •10th June 2023, SunCore Energy Systems unveiled a breakthrough solar fluorite photovoltaic module featuring enhanced durability and higher efficiency under extreme weather conditions. The module utilizes proprietary fluorite-based coatings to improve light absorption and thermal stability, making it suitable for diverse geographic regions. Marketed primarily for commercial and residential applications, this product addresses key challenges in solar power reliability and longevity. The company’s strategic objective includes expanding presence in Asia-Pacific markets through joint ventures and localized manufacturing. This innovation is anticipated to accelerate fluorite solar adoption and contribute to global renewable energy targets. Source: Industry publication

- •20th September 2024, HydroFluorite Technologies Inc. announced a strategic alliance with GreenFluorite Energy Partners to co-develop integrated fluorite power solutions combining hydroelectric and wind generation capabilities. This collaboration aims to deliver hybrid systems with enhanced grid stability and efficiency tailored for emerging markets. The partnership leverages combined R&D expertise and extensive distribution networks to accelerate commercialization. Pilot projects are underway in select regions across Latin America and Asia-Pacific, demonstrating promising results in energy output and cost reduction. The alliance strengthens both companies’ competitive positioning and supports global energy transition initiatives. Source: Company website

- •5th November 2023, Nuclear Fluorite Innovations completed the acquisition of Thermal Fluorite Power Systems, expanding its product portfolio to include advanced thermal fluorite technologies. This acquisition enhances capabilities in power generation efficiency and broadens geographic reach into Asia-Pacific and Europe. The combined entity aims to invest in R&D to develop next-generation fluorite power plants with reduced emissions and improved cost structures. Integration efforts focus on leveraging complementary technologies and optimizing operational synergies to accelerate market growth. This strategic move consolidates market presence and aligns with increasing demand for diversified fluorite power solutions globally. Source: Industry publication

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 45.2 Billion |

| Forecast Year Market Size | USD 112.8 Billion |

| CAGR | 10.03% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 9.62% |

| Scope of Report | Market is segmented by Product Type (Hydroelectric Power Generation, Thermal Power Generation, Nuclear Power Generation, Solar Power Generation, Wind Power Generation), Application (Industrial Power Generation, Residential Power Supply, Commercial Power Use, Agricultural Power, Transportation Power), End-Use Industry (Manufacturing, Construction, Agriculture, Transportation), Distribution Channel (Direct Sales, Distributors, Online Channels) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Fluorite Energy Corporation (United States), Global Power Solutions Ltd. (Germany), SunCore Energy Systems (China), HydroFluorite Technologies Inc. (Canada), Nuclear Fluorite Innovations (France), SolarFluorite Power Group (Japan), WindFluorite Energy Corp. (United Kingdom), Thermal Fluorite Power Systems (India), Fluorite Renewables LLC (Australia), EcoFluorite Energy Solutions (South Korea), Pacific Fluorite Power Co. (Brazil), Fluorite Power Technologies Ltd. (Italy), GreenFluorite Energy Partners (Netherlands), Fluorite Energy Innovations (Russia), Atlantic Fluorite Power (South Africa), Fluorite Power Dynamics (Mexico), Northern Fluorite Power Corp. (Sweden), Fluorite Energy Enterprises (Saudi Arabia), Fluorite Power Holdings (Singapore), Continental Fluorite Power (Poland), Fluorite Power Solutions (United Arab Emirates), Fluorite Energy Systems (Argentina), Fluorite Tech Power Ltd. (Norway), Fluorite Power Group (Chile), Fluorite Energy Corp. (New Zealand) |

Global Fluorite Power Market Size, Growth & Revenue 2024-2034 - Table of Contents

Research enthusiast focused on transforming data uncovering into actionable insights through data-driven decision-making.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.