Global Rangefinders Market Size, Growth & Revenue 2025-2034

Global Rangefinders Market is segmented by Product Type (Laser Rangefinders, Optical Rangefinders, Ultrasonic Rangefinders, Radar Rangefinders, Infrared Rangefinders), Application (Military, Hunting, Surveying, Sports & Recreation, Industrial), End-Use Industry (Defense & Military, Construction & Surveying, Outdoor Sports & Recreation, Manufacturing & Industrial Automation), Distribution Channel (Direct Sales, Authorized Dealers, E-commerce Platforms), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

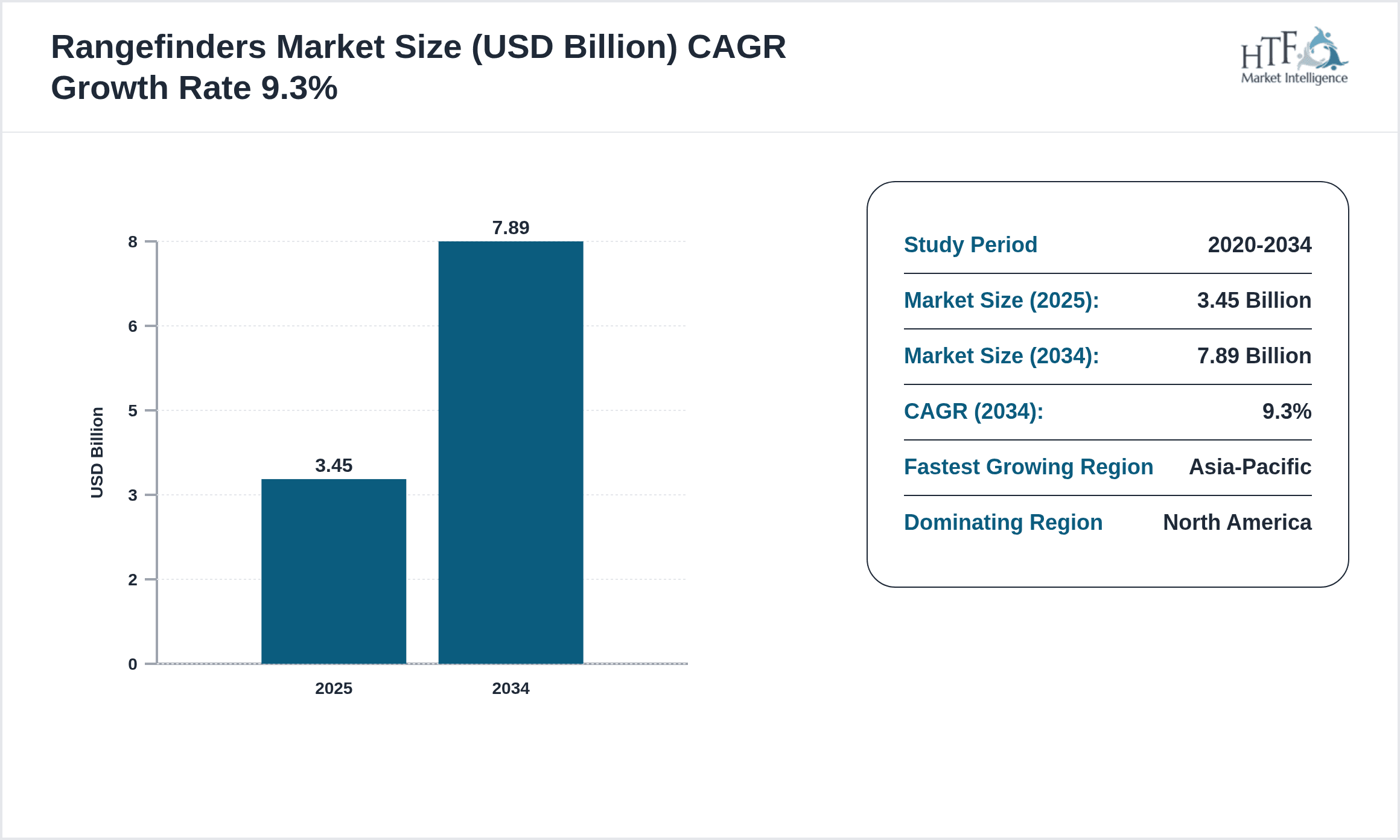

- •The global rangefinders market comprises technologically advanced devices designed to measure distances with high accuracy across multiple sectors including military, hunting, surveying, sports, and industrial applications. These devices employ various technologies such as laser, optical, ultrasonic, radar, and infrared, catering to specific needs for precision and operational efficiency. The market's value chain spans component manufacturing, device assembly, software integration, distribution, and after-sales support, ensuring comprehensive service delivery. Increasing adoption of rangefinders in defense for targeting and reconnaissance, in surveying for construction and mapping accuracy, and in sports for performance enhancement drives market growth. Furthermore, the rise in hunting and outdoor recreational activities, coupled with industrial automation demands, expands the market scope. Technological advancements including miniaturization, integration with digital systems like GPS and IoT, and improved sensor capabilities support enhanced device functionality. Regional market evolution is propelled by investments in defense and infrastructure development predominantly in North America and Asia-Pacific. The market is forecasted to grow significantly from USD 3.45 billion in 2025 to USD 7.89 billion by 2034, reflecting a compounded annual growth rate of 9.3%. This growth is underpinned by expanding applications, innovation in product technology, and increasing awareness of precision measurement devices globally.

- •Key market highlights include the dominance of laser rangefinders driven by their superior accuracy and reliability, the rapid growth of ultrasonic rangefinders due to their cost-effectiveness and ease of integration in industrial applications, and the expanding penetration of rangefinders in emerging markets within Asia-Pacific and Latin America. The military segment remains the largest application area given the critical requirement for precise distance measurement in defense operations. Additionally, the survey and industrial sectors are witnessing increased adoption due to infrastructure development and automation trends. Market growth is further supported by advancements in sensor technology, increased R&D investments, and strategic partnerships among technology providers and manufacturers.

- •The rangefinders market offers strategic value to stakeholders including manufacturers, technology developers, end-users, and investors by enabling enhanced operational efficiency, safety, and accuracy across applications. For defense agencies, this translates to improved targeting and surveillance capabilities. In industrial contexts, rangefinders contribute to automation and quality control, while in sports and recreation, they enhance user experience and precision. The continued evolution of technology and expanding application scope present significant revenue opportunities. Consequently, the market holds substantial potential for innovation-driven growth and strategic collaborations, making it a focal point for long-term investments and development initiatives.

Competitive Landscape

The global rangefinders market exhibits a highly competitive environment characterized by rapid technological innovation, aggressive product development, and strategic collaborations. Market participants focus on differentiating their product portfolios through enhanced accuracy, compact designs, multi-functionality, and integration with digital technologies such as GPS and IoT. Competitive strategies include mergers and acquisitions, joint ventures, and partnerships aimed at expanding geographical reach and technological capabilities. Pricing strategies vary, with premium products targeting defense and professional surveying sectors, while cost-effective models cater to hunting and recreational users. The distribution channels involve direct sales, authorized dealers, and e-commerce platforms, enabling broad market penetration. Market entry barriers include technological expertise requirements, regulatory compliance, and intellectual property protections. Regional competition is influenced by localized manufacturing capabilities and government defense spending, particularly in North America, Europe, and Asia-Pacific. Future competitive trends indicate increased focus on miniaturization, software integration, and sustainable manufacturing practices to address evolving customer demands and regulatory pressures.

Leading Companies in Rangefinders Market

- •Leica Geosystems AG (Switzerland)

- •Trimble Inc. (United States)

- •Nikon Corporation (Japan)

- •Fujifilm Holdings Corporation (Japan)

- •Bushnell Corporation (United States)

- •Garmin Ltd. (Switzerland)

- •Zeiss Group (Germany)

- •Sony Corporation (Japan)

- •Raytheon Technologies Corporation (United States)

- •FLIR Systems, Inc. (United States)

- •Topcon Corporation (Japan)

- •Vortex Optics (United States)

- •Leupold & Stevens, Inc. (United States)

- •Sokkia (Japan)

- •Hensoldt AG (Germany)

- •Bushnell Outdoor Products (United States)

- •Canon Inc. (Japan)

- •Carl Zeiss Meditec AG (Germany)

- •L3Harris Technologies, Inc. (United States)

- •Leica Microsystems GmbH (Germany)

- •TPI Corporation (United States)

- •Kongsberg Gruppen ASA (Norway)

- •FLIR Systems, Inc. (United States)

- •Swarovski Optik (Austria)

- •Pentax Ricoh Imaging Company (Japan)

Market Breakdown

- •By Product Type

- ◦Laser Rangefinders

- ◦Optical Rangefinders

- ◦Ultrasonic Rangefinders

- ◦Radar Rangefinders

- ◦Infrared Rangefinders

- •By Application

- ◦Military

- ◦Hunting

- ◦Surveying

- ◦Sports & Recreation

- ◦Industrial

- •By End-Use Industry

- ◦Defense & Military

- ◦Construction & Surveying

- ◦Outdoor Sports & Recreation

- ◦Manufacturing & Industrial Automation

- •By Distribution Channel

- ◦Direct Sales

- ◦Authorized Dealers

- ◦E-commerce Platforms

Growth Dynamics

- •The rising adoption of laser rangefinders in defense and surveying sectors is a primary growth driver, supported by their high accuracy and reliability in critical applications. Increased military modernization programs across North America and Asia-Pacific significantly boost demand for advanced rangefinding technologies. Additionally, the surge in outdoor recreational activities such as hunting and golfing, particularly in developed regions, expands the consumer base for portable rangefinders. Enhanced integration of rangefinders with GPS and IoT platforms facilitates real-time data acquisition and analysis, driving industry adoption in industrial automation. Furthermore, government investments in infrastructure development and smart city projects catalyze demand for precise surveying equipment, fostering market expansion. Technological advancements focusing on miniaturization and energy efficiency further stimulate product innovation and customer interest. The growing emphasis on safety and operational efficiency in industrial processes incentivizes adoption of ultrasonic and radar rangefinders, strengthening market growth prospects.

- •Emerging markets in Asia-Pacific and Latin America present significant growth opportunities due to increasing defense expenditure, infrastructure projects, and rising consumer awareness. These regions are witnessing rapid urbanization and technological adoption, creating a fertile environment for rangefinder market expansion. Collaborative initiatives between technology providers and local manufacturers enhance product accessibility and affordability. Additionally, favorable government policies promoting smart technologies and innovation ecosystems contribute to long-term growth momentum. The rise of e-commerce platforms facilitates broader market reach and consumer engagement in these regions, boosting sales and market penetration.

- •Strategic partnerships and mergers among key market players drive innovation and expand product portfolios, enabling companies to cater to diverse applications and customer needs. These collaborations foster research and development, accelerating the introduction of next-generation rangefinding solutions with improved accuracy, multifunctionality, and user-friendliness. The trend towards integrating artificial intelligence and machine learning with rangefinder technologies enhances data analytics capabilities, offering competitive advantages. Additionally, customization and modular design approaches allow tailored solutions for specific industry requirements, enhancing market appeal.

- •Environmental concerns and regulatory standards encourage the adoption of energy-efficient and eco-friendly rangefinder devices. Manufacturers are investing in sustainable materials and production processes to meet compliance requirements and consumer expectations. This focus on sustainability not only improves brand reputation but also opens avenues for innovation in device design and functionality. Furthermore, the increasing preference for wireless and portable rangefinders aligns with consumer demand for convenience and mobility, expanding market segments.

- •The growing use of rangefinders in industrial automation and safety monitoring is another growth catalyst, as sectors seek to optimize operations and reduce workplace hazards. Ultrasonic and radar rangefinders find extensive applications in robotics, material handling, and quality control processes. The integration of these technologies with industrial IoT platforms enables real-time monitoring and predictive maintenance, driving efficiency gains. This trend is particularly prominent in developed economies with advanced manufacturing infrastructures, reinforcing market growth.

- •Increasing R&D investments and government funding in defense and smart infrastructure projects contribute to sustained market growth. These initiatives promote innovation, technology adoption, and commercialization of advanced rangefinder products. Public-private partnerships and innovation hubs facilitate knowledge sharing and collaboration, accelerating development cycles. Investors are increasingly attracted to the market due to its technological dynamism and expanding application landscape.

- •The adoption of digital and cloud-based platforms for data management and analysis in rangefinder applications enhances decision-making and operational efficiency. This shift towards digital transformation enables integration with geographic information systems (GIS) and building information modeling (BIM), providing comprehensive spatial data solutions. The market benefits from improved user experience and increased functionality, driving broader acceptance across industries.

Market Trends

- •The proliferation of compact and lightweight laser rangefinders designed for field operatives and outdoor enthusiasts is transforming user experiences. Manufacturers focus on ergonomic designs, extended battery life, and enhanced optical clarity, responding to consumer demands. These developments improve portability and ease of use, expanding market penetration in hunting and sports segments.

- •Integration of rangefinders with augmented reality (AR) and heads-up display (HUD) technologies is an emerging trend, particularly in military and industrial applications. This fusion enables real-time data visualization, situational awareness, and improved operational efficiency. Companies are investing in R&D to develop seamless AR-enabled rangefinding solutions, setting new industry standards.

- •Sustainability and eco-conscious manufacturing practices are gaining prominence, with companies adopting recyclable materials and energy-saving technologies. This trend aligns with global environmental goals and regulatory requirements, enhancing brand reputation and consumer trust. Sustainable product lines are increasingly marketed to environmentally aware customer segments.

- •The growth of e-commerce and digital sales channels is reshaping distribution strategies, enabling manufacturers to reach global audiences directly. Online platforms facilitate product customization, customer feedback, and after-sales support, improving customer engagement and satisfaction. This trend is especially significant in emerging markets with expanding internet penetration.

- •Collaborative innovation ecosystems involving technology startups, research institutions, and established corporations drive rapid advancement in rangefinder functionalities. These partnerships accelerate the integration of AI, machine learning, and advanced sensor technologies, fostering competitive differentiation. The collaborative approach enhances speed to market and responsiveness to evolving customer needs.

- •Consumer demand for multi-functional devices combining rangefinding with other capabilities such as GPS, mapping, and environmental sensing is on the rise. Manufacturers respond by developing integrated solutions that offer comprehensive utility across applications. This trend supports market growth by appealing to diverse user segments seeking value-added features.

- •The adoption of subscription-based models and software-as-a-service (SaaS) offerings for rangefinder data analytics and management is becoming prevalent. This shift provides recurring revenue streams for companies and flexible solutions for customers, enhancing market dynamics. It also facilitates continuous software updates and feature enhancements without hardware changes.

Market Opportunities

- •Expanding applications of rangefinders in emerging sectors such as autonomous vehicles, drones, and robotics present significant growth opportunities. These sectors demand precise distance measurement and environmental sensing, creating new market segments. Companies investing in tailored solutions for these technologies stand to gain competitive advantage.

- •Untapped markets in Latin America and Middle East & Africa offer potential due to increasing infrastructure projects, defense modernization, and growing outdoor recreational activities. Strategic market entry and localized product development can capitalize on these opportunities. Partnerships with regional distributors and governments can facilitate adoption.

- •Innovation in miniaturized and wearable rangefinder devices opens avenues for consumer electronics and sports applications. These products enhance user convenience and functionality, appealing to tech-savvy consumers. Investment in R&D targeting portability and integration drives market differentiation.

- •Integration of AI-driven analytics and cloud computing with rangefinder systems offers opportunities for advanced data insights and operational optimization. This development enables predictive maintenance, enhanced safety, and improved decision-making across industries. Companies focusing on software innovation alongside hardware can leverage this trend.

- •Geographical expansion through e-commerce and digital marketing enables access to a broader customer base, especially in remote and underserved regions. Tailored marketing strategies and localized content can increase brand visibility and customer acquisition. Digital platforms also support customer education and community building.

- •Collaborations and joint ventures with technology startups accelerate the introduction of disruptive innovations and niche solutions, creating new revenue streams. These partnerships foster agility and access to emerging technologies, enhancing competitive positioning. They also facilitate entry into specialized market segments.

- •Government incentives and funding programs for smart infrastructure and defense projects provide financial support for product development and market expansion. Companies aligning with these initiatives can benefit from reduced costs and enhanced credibility. Proactive engagement with policymakers supports regulatory compliance and market access.

Market Challenges

- •High initial costs and complexity of advanced rangefinder systems pose adoption barriers, especially for small and medium enterprises and individual consumers. These factors limit market penetration in price-sensitive segments and emerging economies. Companies must balance cost reduction with performance to address this challenge.

- •Technical limitations such as reduced accuracy in adverse weather conditions or complex terrains impact device reliability. These constraints affect user confidence and application scope, necessitating continuous innovation. Manufacturers invest in sensor fusion and adaptive algorithms to mitigate these issues.

- •Stringent regulatory requirements and certification processes in different regions increase compliance costs and time-to-market. Navigating diverse standards for safety, electromagnetic compatibility, and environmental impact complicates product launches. Companies must develop robust compliance strategies to overcome these hurdles.

- •Intense competition and rapid technological changes require sustained R&D investment and strategic agility. Smaller players may face difficulties maintaining pace with industry leaders, risking market share loss. Effective innovation management and strategic collaborations are critical to staying competitive.

- •Supply chain disruptions and component shortages, exacerbated by geopolitical tensions and global crises, affect production schedules and cost structures. These challenges impact product availability and pricing stability, influencing customer satisfaction. Diversification of suppliers and inventory management are vital mitigation approaches.

- •Limited consumer awareness and understanding of advanced rangefinder capabilities restrict market growth in certain regions and segments. Education and marketing efforts are necessary to demonstrate value propositions and encourage adoption. This challenge is particularly relevant in emerging markets.

- •Cybersecurity risks associated with connected and digital rangefinder systems pose challenges in data protection and user privacy. Ensuring secure communication and compliance with data regulations is essential to maintain trust and market acceptance. Investment in robust cybersecurity frameworks is required.

Regulatory Framework

- •The Federal Communications Commission (FCC) regulations enacted between 2020 and 2025 impose strict emission limits and certification requirements for laser and radio frequency-based rangefinders, ensuring user safety and minimizing interference with other devices. Compliance with these standards is mandatory for market entry in North America, influencing product design and testing protocols.

- •The European Union's Machinery Directive 2006/42/EC, updated with amendments through 2025, governs the safety and performance of measuring equipment including rangefinders. It mandates conformity assessments and CE marking, impacting manufacturers targeting the European market. The directive promotes harmonization of safety standards across member states.

- •China's National Standard GB/T 20350-2021 for laser rangefinders specifies technical and safety requirements applicable from 2021 onwards. This regulation ensures product quality and operational safety for the rapidly growing Chinese market, requiring compliance from domestic and international manufacturers operating there.

- •The United Nations' International Telecommunication Union (ITU) guidelines updated in 2023 address spectrum allocation and interference management for radar and radio-based rangefinder devices globally. These regulations facilitate cross-border compatibility and prevent signal disruptions, critical for international device interoperability.

- •Environmental regulations such as the Restriction of Hazardous Substances (RoHS) Directive and Waste Electrical and Electronic Equipment (WEEE) Directive in Europe, enforced between 2020 and 2025, mandate the reduction of hazardous materials and promote responsible disposal of electronic rangefinder components. Manufacturers comply to ensure environmental sustainability and market access.

Market Intelligence

- •15th January 2025, Leica Geosystems AG announced the launch of its new high-precision laser rangefinder equipped with integrated GPS and Bluetooth capabilities, targeting the surveying and construction industries. The device offers enhanced accuracy within 1 millimeter up to 2 kilometers, supports real-time data transfer to mobile and desktop applications, and features a rugged design suitable for harsh environments. This launch aims to streamline field data collection and improve project efficiency, positioning Leica as a leader in innovation. The strategic objective includes capturing increased market share in infrastructure development sectors globally. Source: Leica Geosystems Official Press Release.

- •22nd March 2025, Trimble Inc. introduced an advanced ultrasonic rangefinder system tailored for industrial automation and robotics applications. The product integrates AI-powered analytics to enable predictive maintenance and real-time obstacle detection, enhancing operational safety and efficiency. Its modular architecture allows customization for various manufacturing environments, addressing diverse industrial needs. Trimble anticipates significant adoption in smart factories and logistics, supporting its growth strategy in Industry 4.0 segments. This innovation reflects the company’s commitment to combining hardware excellence with software capabilities. Source: Trimble Inc. Corporate Announcement.

- •10th July 2025, Nikon Corporation completed the acquisition of a specialized sensor technology startup to enhance its rangefinder product line with next-generation LIDAR and imaging capabilities. The deal aims to leverage the startup’s expertise in compact sensor design and AI integration, accelerating Nikon’s development of multifunctional devices for military and recreational markets. This acquisition strengthens Nikon’s competitive positioning by expanding its technology portfolio and accelerating time-to-market for innovative solutions. The strategic move is expected to drive revenue growth and market penetration across Asia-Pacific and Europe. Source: Nikon Corporation Press Release.

- •5th November 2024, Raytheon Technologies Corporation announced a strategic partnership with a leading AI software developer to co-develop smart rangefinder systems with enhanced target recognition and data analytics. The collaboration focuses on integrating machine learning algorithms to improve accuracy and operational decision-making in defense applications. This initiative aligns with Raytheon’s commitment to advancing military technology and addressing evolving battlefield requirements. The partnership is expected to yield new product offerings by 2026, reinforcing Raytheon’s leadership in defense rangefinding solutions. Source: Raytheon Technologies Corporate News.

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 3.45 Billion |

| Forecast Year Market Size | USD 7.89 Billion |

| CAGR | 9.3% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 9% |

| Scope of Report | Market is segmented by Product Type (Laser Rangefinders, Optical Rangefinders, Ultrasonic Rangefinders, Radar Rangefinders, Infrared Rangefinders), Application (Military, Hunting, Surveying, Sports & Recreation, Industrial), End-Use Industry (Defense & Military, Construction & Surveying, Outdoor Sports & Recreation, Manufacturing & Industrial Automation), Distribution Channel (Direct Sales, Authorized Dealers, E-commerce Platforms) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Leica Geosystems AG (Switzerland), Trimble Inc. (United States), Nikon Corporation (Japan), Fujifilm Holdings Corporation (Japan), Bushnell Corporation (United States), Garmin Ltd. (Switzerland), Zeiss Group (Germany), Sony Corporation (Japan), Raytheon Technologies Corporation (United States), FLIR Systems, Inc. (United States), Topcon Corporation (Japan), Vortex Optics (United States), Leupold & Stevens, Inc. (United States), Sokkia (Japan), Hensoldt AG (Germany), Bushnell Outdoor Products (United States), Canon Inc. (Japan), Carl Zeiss Meditec AG (Germany), L3Harris Technologies, Inc. (United States), Leica Microsystems GmbH (Germany), TPI Corporation (United States), Kongsberg Gruppen ASA (Norway), FLIR Systems, Inc. (United States), Swarovski Optik (Austria), Pentax Ricoh Imaging Company (Japan) |

Global Rangefinders Market Size, Growth & Revenue 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.