Global Automotive Power Amplifier Market Size, Growth & Revenue 2024-2034

Global Automotive Power Amplifier Market is segmented by Product Type (Class A Power Amplifiers, Class B Power Amplifiers, Class AB Power Amplifiers, Class D Power Amplifiers, Class G Power Amplifiers), Application (Audio Systems, Safety Systems, Infotainment, Navigation, Communication), End-Use Industry (Passenger Cars, Commercial Vehicles, Electric Vehicles, Aftermarket), Distribution Channel (OEMs, Aftermarket Dealers, E-commerce Platforms), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global automotive power amplifier market is a critical segment within the automotive electronics industry, focusing on devices that enhance vehicular audio and electronic performance. This market includes amplifiers designed to support various applications such as audio entertainment systems, safety and communication modules, navigation aids, and infotainment platforms within passenger and commercial vehicles. The amplifiers vary by technology type—Class A, B, AB, D, and G—each providing specific benefits in terms of power efficiency, sound fidelity, and thermal performance. Rapid technological advancements and increasing consumer demand for premium in-car audio and connectivity solutions drive market expansion. Furthermore, the rise in electric vehicle adoption and integration of advanced driver assistance systems (ADAS) expands the application scope of automotive power amplifiers. Key end-users include OEMs and aftermarket service providers worldwide. The market’s geographic footprint spans North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, each with unique growth dynamics influenced by regional regulations and consumer preferences.

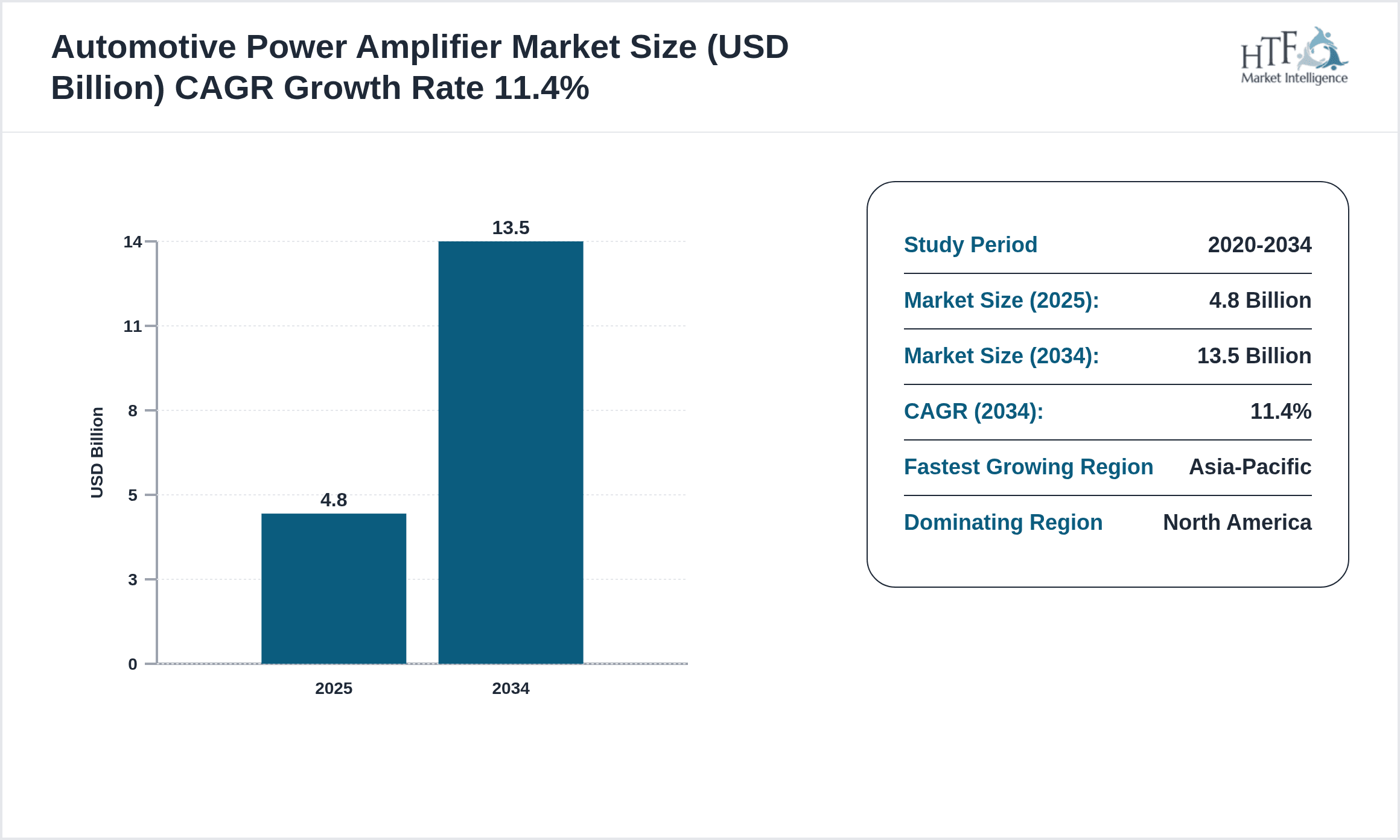

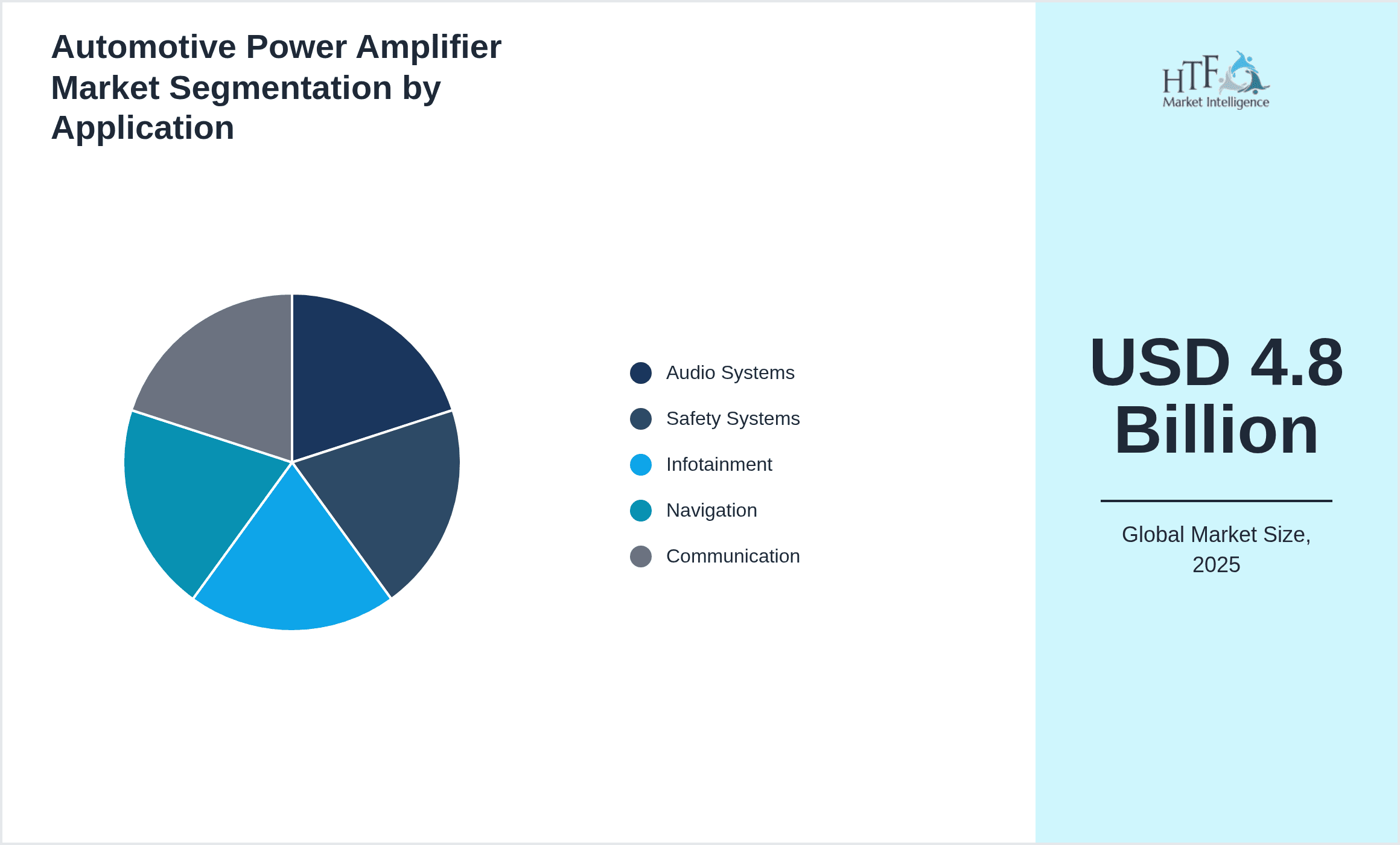

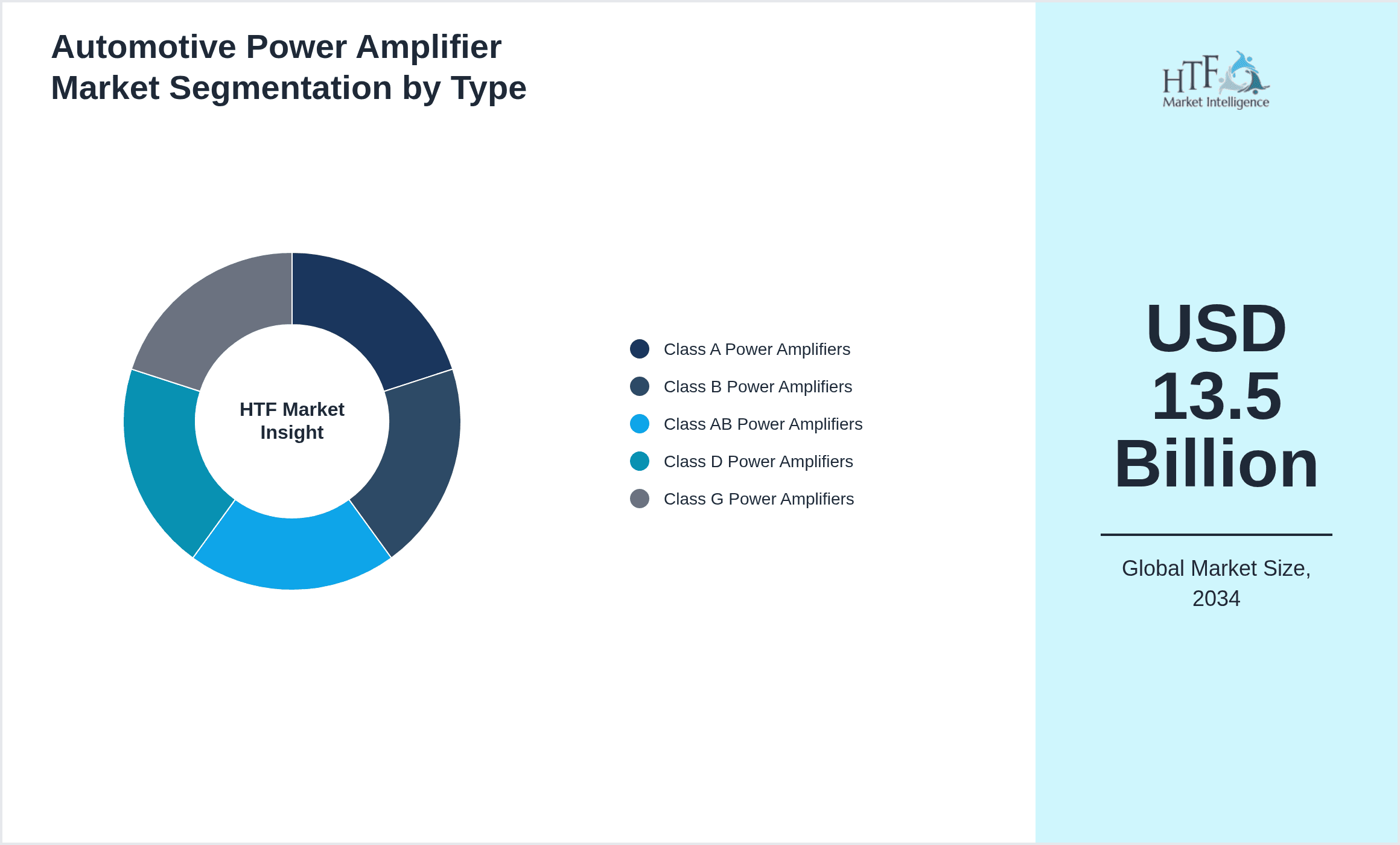

- •Key highlights of the market include a base size of USD 4.8 Billion in 2024, projected to reach USD 13.5 Billion by 2034, reflecting a CAGR of approximately 11.4%. North America currently dominates the market in terms of revenue share, supported by strong automotive manufacturing and high consumer spending on vehicle electronics. However, Asia-Pacific is poised to be the fastest-growing region due to rapid automotive production, increased vehicle electrification, and rising disposable incomes. Class D amplifiers lead the product segment owing to their superior efficiency and compact design, while Class G amplifiers are expected to witness the highest growth as manufacturers seek improved power savings and performance. Among applications, audio systems hold the largest market share, with infotainment and safety systems following closely, driven by consumer demand for immersive and safe driving experiences.

- •This market offers substantial value propositions to automotive OEMs, electronic component manufacturers, and end consumers by enabling enhanced audio quality, improved safety features, and integrated communication within vehicles. Strategic investments in R&D and collaborations between amplifier manufacturers and automotive electronics providers are essential to address evolving technical requirements and regulatory standards. The market’s growth is further propelled by the global shift towards connected and autonomous vehicles, which necessitate robust amplifier solutions. Stakeholders benefit from tapping into emerging markets, leveraging technological innovation, and aligning product developments with sustainability and energy efficiency trends. Overall, the automotive power amplifier market represents a dynamic and expanding sector critical to the future of automotive electronics and mobility solutions.

Competitive Landscape

The global automotive power amplifier market is characterized by intense competition among established semiconductor manufacturers, automotive electronics suppliers, and emerging technology firms. Companies differentiate themselves through innovation in amplifier design, focusing on enhancing power efficiency, miniaturization, and integration with vehicle electronic systems. Strategic partnerships and collaborations with automotive OEMs enable tailored solutions that meet stringent automotive standards. Market leaders invest heavily in R&D to develop next-generation amplifier technologies that cater to electric and autonomous vehicles. Competitive strategies also include mergers and acquisitions to consolidate market presence and expand geographic reach. Pricing strategies are balanced with product quality and technological advancements to maintain profitability while addressing cost pressures. Distribution channels include direct OEM supply and aftermarket sales, with increasing emphasis on digital marketing and e-commerce platforms. The competitive environment continues to evolve with the entry of startups specializing in advanced amplifier technologies and the push for sustainable, energy-efficient automotive components.

Key Participants in Automotive Power Amplifier Market

- •Texas Instruments (United States)

- •Infineon Technologies AG (Germany)

- •NXP Semiconductors (Netherlands)

- •Analog Devices, Inc. (United States)

- •Renesas Electronics Corporation (Japan)

- •ON Semiconductor Corporation (United States)

- •STMicroelectronics N.V. (Switzerland)

- •Qualcomm Incorporated (United States)

- •Broadcom Inc. (United States)

- •Maxim Integrated Products, Inc. (United States)

- •Sony Corporation (Japan)

- •Skyworks Solutions, Inc. (United States)

- •Cirrus Logic, Inc. (United States)

- •Harman International Industries, Inc. (United States)

- •Analogic Corporation (United States)

- •Microchip Technology Inc. (United States)

- •Murata Manufacturing Co., Ltd. (Japan)

- •Toshiba Corporation (Japan)

- •SK hynix Inc. (South Korea)

- •Analog Devices (United States)

- •Allegro MicroSystems, LLC (United States)

- •Semtech Corporation (United States)

- •Xilinx, Inc. (United States)

- •Vishay Intertechnology, Inc. (United States)

- •Rohm Semiconductor (Japan)

Market Breakdown

- •By Product Type

- ◦Class A Power Amplifiers

- ◦Class B Power Amplifiers

- ◦Class AB Power Amplifiers

- ◦Class D Power Amplifiers

- ◦Class G Power Amplifiers

- •By Application

- ◦Audio Systems

- ◦Safety Systems

- ◦Infotainment

- ◦Navigation

- ◦Communication

- •By End-Use Industry

- ◦Passenger Cars

- ◦Commercial Vehicles

- ◦Electric Vehicles

- ◦Aftermarket

- •By Distribution Channel

- ◦OEMs

- ◦Aftermarket Dealers

- ◦E-commerce Platforms

Growth Dynamics

- •Increasing demand for high-quality in-car audio systems is a primary growth driver, as consumers seek enhanced entertainment experiences. This trend is supported by advancements in Class D amplifier technology, which offers high efficiency and compact design suitable for modern vehicles.

- •The rising adoption of electric and hybrid vehicles globally is fueling the need for energy-efficient power amplifiers that minimize power consumption while maintaining performance, driving innovation in Class G amplifiers and other advanced types.

- •Integration of automotive power amplifiers with advanced driver assistance systems (ADAS) and infotainment platforms promotes growth by expanding application scope and increasing the complexity of in-vehicle electronics.

- •Technological advancements in semiconductor materials and amplifier design, including the use of GaN and SiC technologies, enable improved thermal management and power density, supporting market expansion.

- •Emerging markets in Asia-Pacific and Latin America present significant growth opportunities due to increasing vehicle production, urbanization, and rising consumer disposable incomes, contributing to amplified demand for automotive power amplifiers.

Market Trends

- •The market is witnessing a shift towards digital and smart amplifier technologies that integrate with vehicle network systems to enable adaptive sound and power management, enhancing user experience and energy efficiency.

- •Sustainability trends are encouraging manufacturers to develop eco-friendly amplifiers with reduced power consumption and recyclable materials, aligning with global automotive emission reduction goals.

- •Collaborations between semiconductor companies and automotive OEMs are increasing to co-develop customized amplifier solutions that meet specific vehicle requirements and regulatory standards.

- •The rise of connected vehicles and IoT integration is driving demand for multi-functional amplifiers capable of supporting diverse in-car communication and entertainment systems simultaneously.

- •Modular amplifier designs are gaining traction, facilitating easier upgrades and maintenance, which appeals to both manufacturers and end-users by reducing lifecycle costs.

Market Opportunities

- •Expanding electric vehicle markets globally offer opportunities for power amplifier manufacturers to innovate energy-efficient and compact solutions tailored to EV architectures.

- •Emerging technologies such as GaN-based amplifiers provide avenues for higher performance and smaller form factors, opening new market segments in premium and luxury vehicle categories.

- •Aftermarket growth driven by vehicle upgrades and retrofitting activities creates additional revenue streams for amplifier providers, particularly in regions with aging vehicle fleets.

- •Partnerships with infotainment system developers and telematics providers allow amplifier companies to integrate their products into holistic automotive electronics ecosystems.

- •Geographical expansion into Latin America and Middle East & Africa, where automotive markets are underpenetrated, offers significant growth potential for early entrants.

Market Challenges

- •High costs associated with research and development of advanced amplifier technologies pose challenges for smaller players attempting market entry or expansion.

- •Stringent automotive safety and electromagnetic interference (EMI) regulations require complex compliance efforts, increasing time-to-market and operational costs.

- •Supply chain disruptions, particularly in semiconductor components, have affected production schedules and increased lead times, impacting market growth temporarily.

- •Competition from low-cost manufacturers in emerging economies pressures pricing and profit margins for established global players.

- •Rapid technological changes demand continuous innovation, which can be resource-intensive and challenging to sustain over long periods.

Regulatory Framework

- •Between 2022 and 2024, global automotive electronics faced increased regulation on electromagnetic compatibility (EMC) and interference, requiring manufacturers to adopt stricter amplifier designs to mitigate emissions and ensure operational safety.

- •New vehicle emission standards introduced in multiple regions mandated lower energy consumption for electronic components, prompting the adoption of high-efficiency Class D and G power amplifiers.

- •Safety regulations for Advanced Driver Assistance Systems (ADAS) necessitated rigorous testing and certification of amplifier modules integrated within these systems to ensure reliability under diverse driving conditions.

- •Regional mandates in Europe and North America have introduced recycling and environmental compliance requirements for automotive electronic components, influencing material selection and manufacturing processes for amplifiers.

- •Government incentives for electric vehicle production in Asia-Pacific have indirectly stimulated demand for compliant and efficient power amplifiers, aligning with energy conservation policies.

Market Intelligence

- •15th January 2025, Texas Instruments announced the launch of a new Class G automotive power amplifier optimized for electric vehicles, featuring 30% higher efficiency and integrated thermal management capabilities. This product aims to support next-generation audio and safety systems while reducing overall power consumption, addressing both OEM and aftermarket demands. The launch positions Texas Instruments to strengthen its foothold in the growing EV segment, leveraging advanced semiconductor processes to deliver superior performance. The amplifier complies with stringent automotive standards and supports scalable architectures for diverse vehicle models. Source: Texas Instruments Official Press Release

- •10th March 2025, Infineon Technologies AG introduced an innovative GaN-based power amplifier targeting automotive infotainment systems. This amplifier offers enhanced power density and reduced size, enabling manufacturers to design compact and efficient audio solutions. Infineon's strategic move aligns with the increasing demand for high-fidelity sound and energy efficiency in premium vehicles. The product integrates seamlessly with existing vehicle networks and supports smart sound processing features. This launch underscores Infineon's commitment to driving innovation in automotive electronics with sustainable and high-performance technologies. Source: Infineon Technologies Newsroom

- •22nd April 2025, NXP Semiconductors announced a strategic partnership with a leading automotive OEM to co-develop customized power amplifier modules for advanced driver assistance systems. The collaboration focuses on integrating highly efficient amplifiers with ADAS sensor arrays to enhance signal processing reliability and reduce electromagnetic interference. This partnership is expected to accelerate the adoption of connected and autonomous vehicle technologies by providing robust audio and communication capabilities. The initiative reflects the growing importance of tailored electronic solutions in modern vehicles and NXP’s role as a key technology enabler. Source: NXP Corporate Announcement

- •5th May 2025, Analog Devices, Inc. completed the acquisition of a specialized amplifier technology startup to expand its portfolio in automotive power amplification. The acquisition enables Analog Devices to incorporate novel amplifier designs that improve energy efficiency and thermal performance in electric and hybrid vehicles. This strategic move aims to bolster Analog Devices’ competitive position in the automotive semiconductor market and accelerate innovation cycles. The integration of the startup’s technology is expected to enhance product offerings across audio, safety, and communication applications. Source: Analog Devices Press Release

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 4.8 Billion |

| Forecast Year Market Size | USD 13.5 Billion |

| CAGR | 11.4% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 11.4% |

| Scope of Report | Market is segmented by Product Type (Class A Power Amplifiers, Class B Power Amplifiers, Class AB Power Amplifiers, Class D Power Amplifiers, Class G Power Amplifiers), Application (Audio Systems, Safety Systems, Infotainment, Navigation, Communication), End-Use Industry (Passenger Cars, Commercial Vehicles, Electric Vehicles, Aftermarket), Distribution Channel (OEMs, Aftermarket Dealers, E-commerce Platforms) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Expanding electric vehicle markets globally offer opportunities for power amplifier manufacturers to innovate energy-efficient and compact solutions tailored to EV architectures., Emerging technologies such as GaN-based amplifiers provide avenues for higher performance and smaller form factors, opening new market segments in premium and luxury vehicle categories., Aftermarket growth driven by vehicle upgrades and retrofitting activities creates additional revenue streams for amplifier providers, particularly in regions with aging vehicle fleets., Partnerships with infotainment system developers and telematics providers allow amplifier companies to integrate their products into holistic automotive electronics ecosystems., Geographical expansion into Latin America and Middle East & Africa, where automotive markets are underpenetrated, offers significant growth potential for early entrants. |

Global Automotive Power Amplifier Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.