Global Polysulfide Sealant Market Size, Growth & Revenue 2024-2034

Global Polysulfide Sealant Market is segmented by Product Type (Single-component Polysulfide Sealants, Two-component Polysulfide Sealants, Preformed Polysulfide Sealants, Modified Polysulfide Sealants, Others), Application (Construction, Aerospace, Automotive, Marine, Electronics), End-Use Industry (Building & Infrastructure, Transportation, Oil & Gas, Electronics & Electrical), Distribution Channel (Direct Sales, Distributors & Wholesalers, Online Retail), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global polysulfide sealant market represents a critical sector within the chemical and construction materials industries, characterized by the manufacture and application of sealants that utilize polysulfide polymers for superior resilience, chemical resistance, and elasticity. These sealants serve vital functions in sealing, bonding, and protecting surfaces against moisture, fuel, and weathering effects, extensively applied in construction for window glazing, aerospace for fuel tank sealing, automotive for component protection, marine for hull sealing, and electronics for device encapsulation. The scope of the market includes various product types such as single-component and two-component formulations, preformed and modified variants, each tailored to specific application needs. The market's global reach spans regions with diverse industrial bases and regulatory frameworks, necessitating innovation in environmentally friendly and high-performance formulations. Key use cases include waterproofing, structural bonding, and chemical containment, positioning polysulfide sealants as indispensable materials for industries requiring durable, flexible sealing solutions.

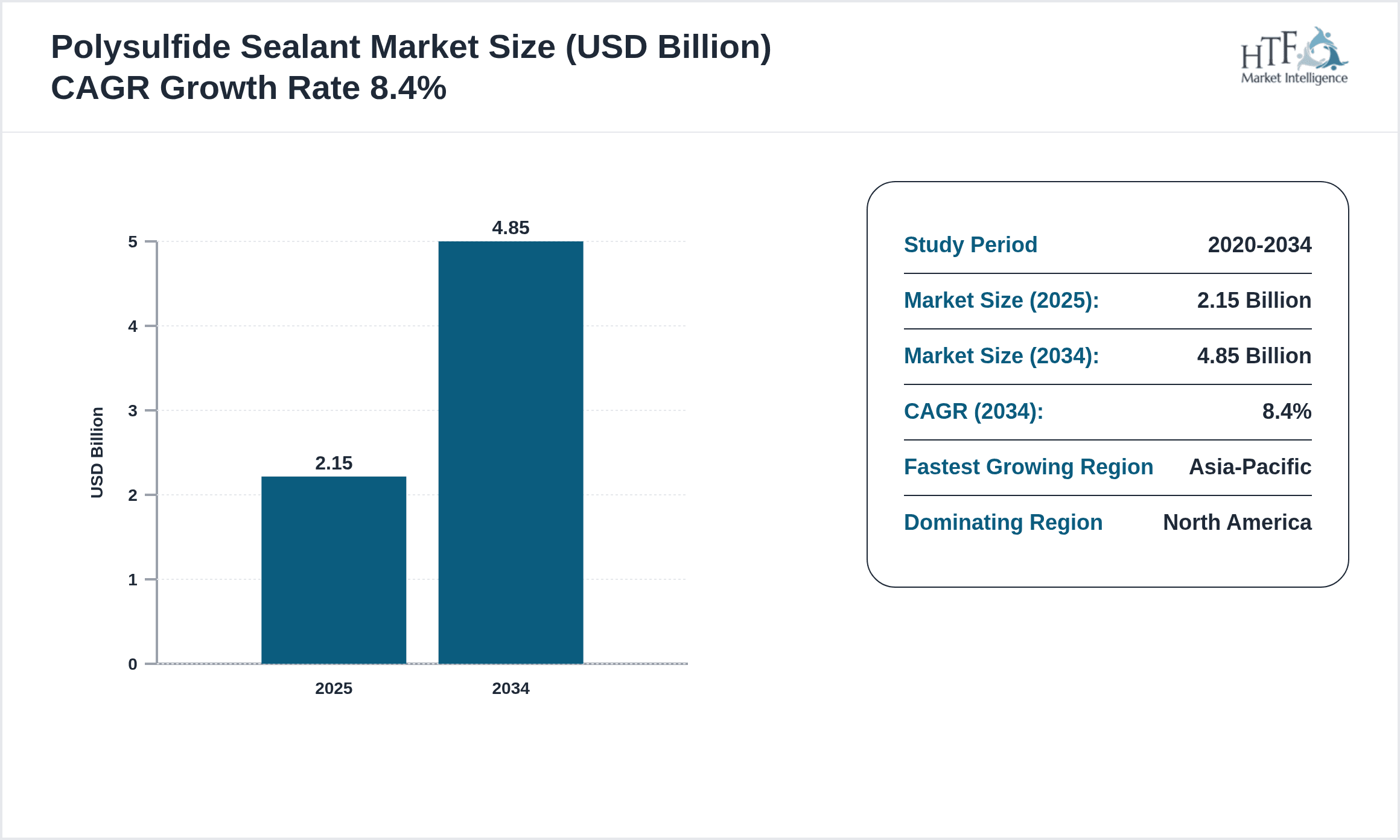

- •Market highlights reveal a robust growth trajectory with the global polysulfide sealant market valued at USD 2.15 Billion in 2024, projected to reach USD 4.85 Billion by 2034, reflecting a CAGR of 8.4%. This growth is driven by increasing demand from construction and aerospace sectors, advancements in sealant technology, and the expansion of infrastructure projects worldwide. The two-component polysulfide sealants currently dominate the market due to their superior performance characteristics, while modified polysulfide sealants are experiencing the fastest growth, attributed to innovations enhancing environmental compliance and application versatility. Regionally, North America holds the largest market share supported by a mature industrial base, with Asia-Pacific identified as the fastest-growing region, propelled by rapid urbanization and industrialization in emerging economies.

- •The value proposition of polysulfide sealants lies in their ability to deliver long-lasting, flexible sealing solutions that withstand harsh chemical and environmental conditions, making them indispensable across multiple industries. Their strategic importance is underscored by the growing emphasis on sustainability, infrastructure resilience, and technological advancements in materials science. Stakeholders including manufacturers, end-users, and regulatory bodies benefit from these sealants through enhanced product performance, compliance with stringent environmental standards, and opportunities to innovate within expanding markets. The polysulfide sealant market thus represents a dynamic landscape driven by industrial demand, regulatory evolution, and continuous product development.

Competitive Landscape

The competitive landscape of the global polysulfide sealant market is marked by intense rivalry among established multinational corporations and specialized regional players. Market dynamics are shaped by strategic investments in research and development to innovate high-performance, eco-friendly sealant formulations that meet evolving regulatory requirements and client specifications. Leading companies adopt differentiation strategies through product quality, technology advancements, and broad distribution networks. Competition extends to pricing strategies, with players balancing cost-effectiveness against premium quality offerings to capture diverse market segments. Mergers and acquisitions, strategic partnerships, and regional expansions are common tactics to consolidate market presence and enter new geographic and application niches. The competitive environment also involves continuous monitoring of supply chain efficiencies to mitigate raw material cost volatility. As market demand shifts towards sustainable and multi-functional sealants, companies invest heavily in innovation and marketing to maintain leadership while navigating barriers such as stringent environmental regulations and raw material constraints.

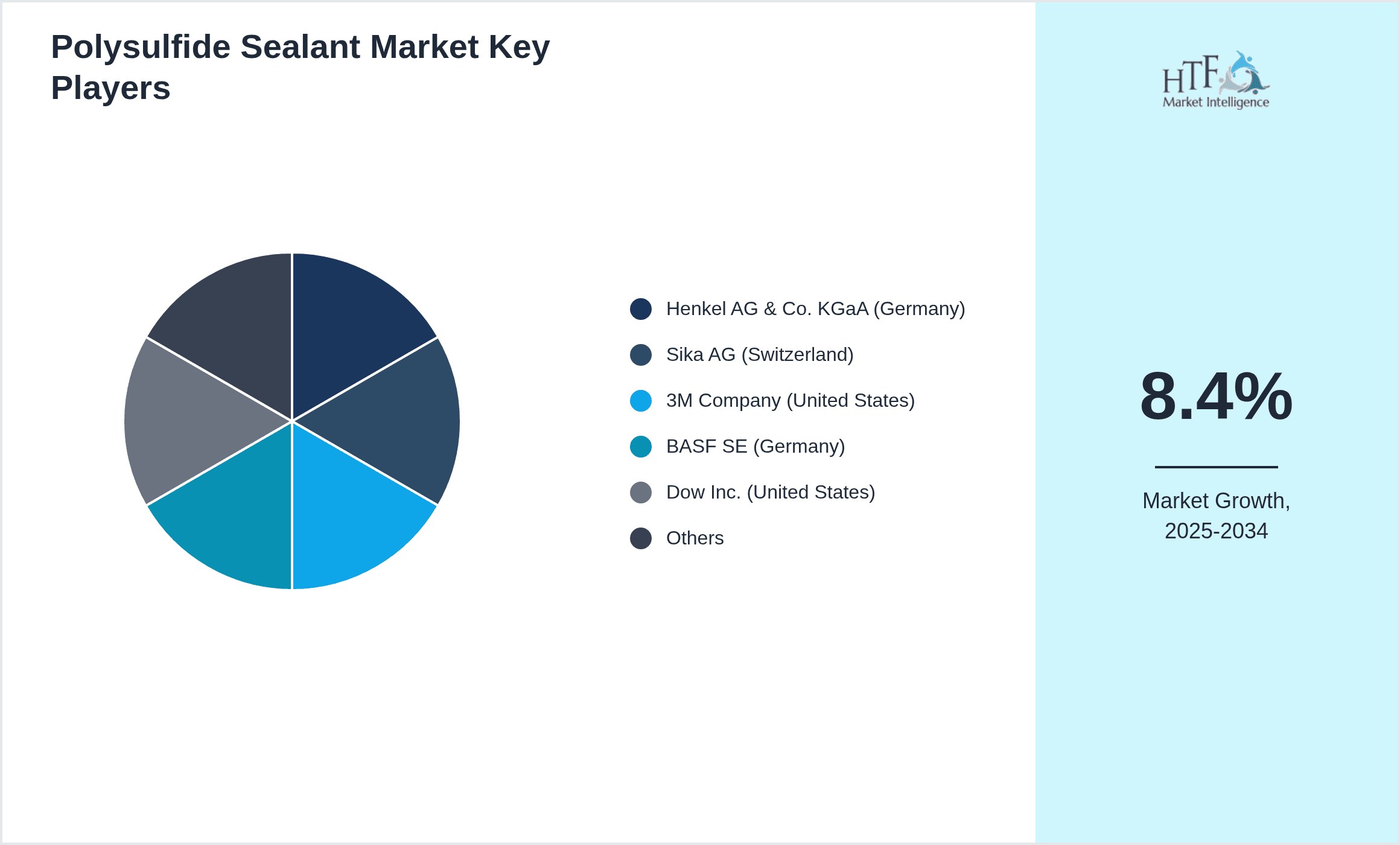

Prominent Players in Polysulfide Sealant Market

- •Henkel AG & Co. KGaA (Germany)

- •Sika AG (Switzerland)

- •3M Company (United States)

- •BASF SE (Germany)

- •Dow Inc. (United States)

- •Wacker Chemie AG (Germany)

- •H.B. Fuller Company (United States)

- •RPM International Inc. (United States)

- •Tremco Incorporated (United States)

- •Arkema Group (France)

- •Illinois Tool Works Inc. (United States)

- •PPG Industries, Inc. (United States)

- •Ashland Global Holdings Inc. (United States)

- •Kuraray Co., Ltd. (Japan)

- •Saint-Gobain S.A. (France)

- •Soudal N.V. (Belgium)

- •Bostik SA (France)

- •Huntsman Corporation (United States)

- •Jowat SE (Germany)

- •Tesa SE (Germany)

- •W.R. Grace & Co. (United States)

- •Carlisle Companies Incorporated (United States)

- •Shin-Etsu Chemical Co., Ltd. (Japan)

- •Sika Group (Switzerland)

- •Mapei S.p.A (Italy)

Market Breakdown

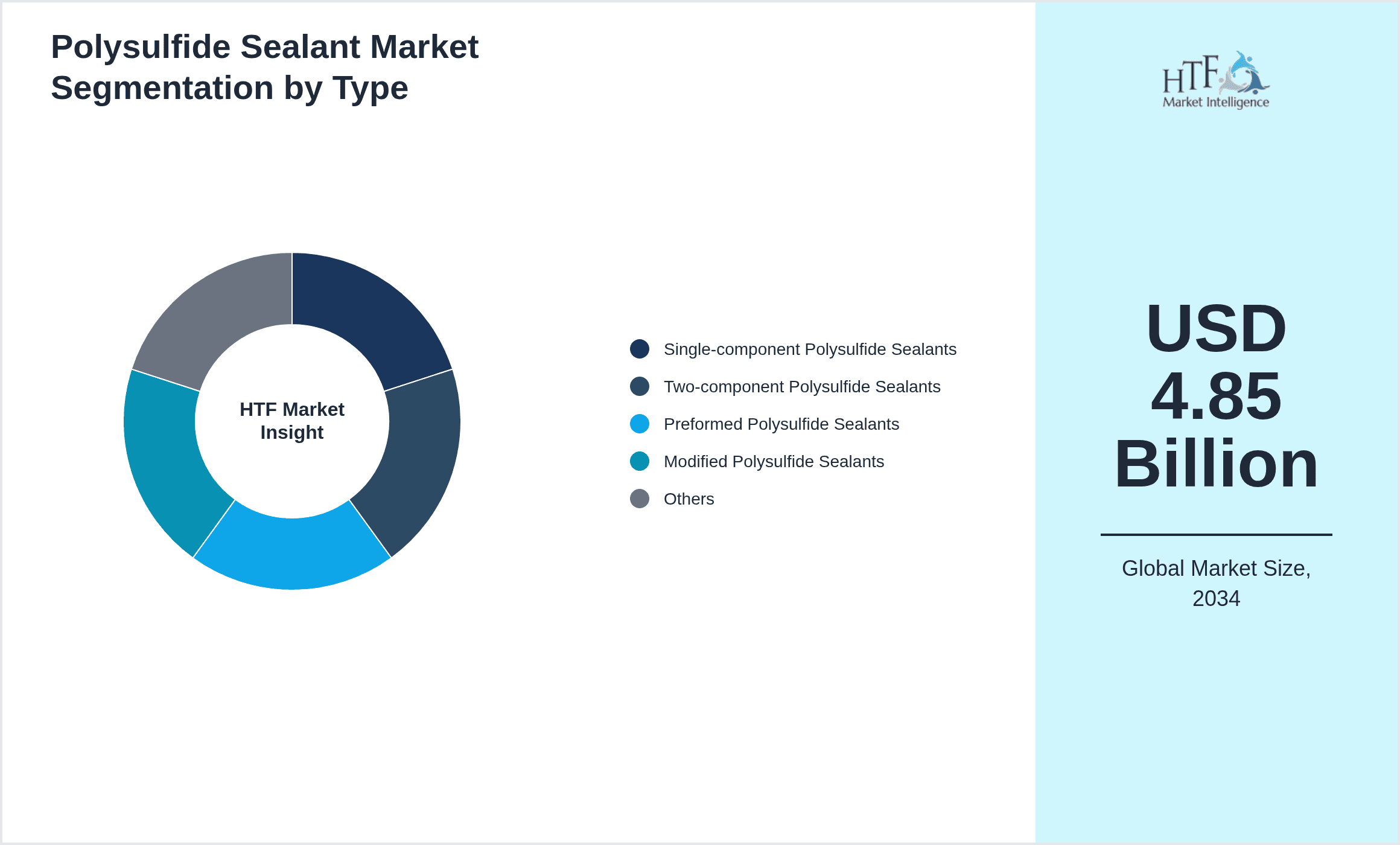

- •By Product Type

- ◦Single-component Polysulfide Sealants

- ◦Two-component Polysulfide Sealants

- ◦Preformed Polysulfide Sealants

- ◦Modified Polysulfide Sealants

- ◦Others

- •By Application

- ◦Construction

- ◦Aerospace

- ◦Automotive

- ◦Marine

- ◦Electronics

- •By End-Use Industry

- ◦Building & Infrastructure

- ◦Transportation

- ◦Oil & Gas

- ◦Electronics & Electrical

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors & Wholesalers

- ◦Online Retail

Growth Dynamics

- •The global polysulfide sealant market is driven by escalating demand for durable and chemically resistant sealing solutions in construction and aerospace industries. Rapid urbanization and infrastructure development, especially in emerging economies, fuel the need for advanced sealants capable of withstanding environmental stressors. Technological advancements in polymer chemistry have enhanced sealant performance, broadening application scopes. Environmental regulations promoting low-VOC and sustainable products have accelerated innovation in modified polysulfide formulations. Additionally, increased investments in transportation and marine sectors contribute substantially to market growth by necessitating reliable sealing materials that ensure operational safety and efficiency.

- •Rising adoption of polysulfide sealants in automotive manufacturing, particularly for sealing fuel tanks and joints, supports market expansion. Their exceptional resistance to fuels and chemicals extends vehicle component life and reduces maintenance costs. Moreover, growing aerospace sector demand for high-performance sealants capable of withstanding extreme conditions further propels growth. The sealant's versatility in electronics for encapsulating sensitive components against moisture and dust adds to the expanding applications. Combined with increasing awareness of product benefits among end-users and improvements in distribution networks, these factors collectively stimulate sustained market growth globally.

- •Government initiatives promoting infrastructure modernization and green building certifications globally encourage the use of eco-friendly polysulfide sealants. Such programs incentivize manufacturers to develop low-emission products, aligning with environmental sustainability goals. The construction sector’s focus on energy efficiency and durability benefits polysulfide sealants, which enhance building envelope integrity. Furthermore, the marine industry's demand for sealants resistant to saltwater corrosion creates niche growth opportunities. These macroeconomic and policy factors synergistically foster a favorable environment for polysulfide sealant market expansion across regions.

- •Advancements in formulation technology enabling faster curing times and improved adhesion properties drive adoption across various industries. These innovations reduce downtime and improve operational efficiency for end-users. The growing preference for multi-functional sealants that combine sealing, bonding, and insulating features enhances product appeal. Partnerships between chemical manufacturers and end-use industries facilitate tailored solutions addressing specific application challenges, contributing to market growth. The increasing trend toward customization and formulation optimization signals a maturing market responsive to evolving consumer and regulatory demands.

- •The expansion of global supply chains and enhanced logistics infrastructure improve product availability and market penetration in developing regions. Increased investments in sales and marketing by key players raise product awareness and acceptance. The rising construction of airports, highways, and commercial buildings in Asia-Pacific and Latin America further boosts polysulfide sealant demand. Combined with digital transformation in procurement and distribution processes, these factors underpin sustained growth dynamics and increased market competitiveness at a global scale.

Market Trends

- •A prominent trend in the polysulfide sealant market is the shift toward environmentally friendly, low-VOC, and solvent-free formulations driven by stringent global regulations and consumer demand for sustainable products. Manufacturers are investing heavily in R&D to develop bio-based and recyclable sealants without compromising performance, aligning with circular economy principles. This transition supports compliance with international standards such as LEED and BREEAM in construction projects, enhancing market acceptance.

- •The adoption of digital technologies in product development and customer engagement is transforming market operations. Advanced simulation tools enable precise formulation adjustments to meet specific application requirements. E-commerce platforms and digital marketing strategies expand reach and streamline the supply chain, improving customer experience and reducing procurement lead times.

- •Strategic collaborations between chemical companies and end-users are increasingly common, focusing on co-developing customized polysulfide sealants for niche applications such as aerospace fuel tanks and marine vessels. These partnerships facilitate innovation and faster market introduction of specialized products, providing competitive differentiation and enhanced value propositions.

- •Sustainability and energy efficiency are significant drivers of product innovation, with polysulfide sealants being integrated into green building materials and energy-saving technologies. The focus on improving thermal insulation and waterproofing capabilities is reshaping product design, supporting broader environmental goals.

- •The growing demand for multi-functional sealants combining sealing, bonding, and insulating properties reflects evolving consumer preferences. This trend encourages manufacturers to develop hybrid formulations that simplify application processes and reduce material inventories, enhancing operational efficiencies.

- •Regional market diversification is evident as manufacturers expand presence in emerging economies via localized production and strategic alliances. This approach addresses region-specific regulatory requirements and cost structures, fostering global market resilience.

- •Continuous improvements in packaging and delivery systems, such as pre-measured cartridges and automated dispensing technologies, improve user convenience and application precision. These enhancements reduce waste and improve overall productivity in end-use industries.

Market Opportunities

- •The global polysulfide sealant market offers substantial growth opportunities through expansion into emerging markets with increasing infrastructure investments and industrialization. Rapid urbanization in Asia-Pacific and Latin America creates demand for advanced sealing materials in construction and transportation sectors, providing fertile ground for market penetration.

- •Innovation in eco-friendly and bio-based polysulfide sealants presents significant opportunities to capture environmentally conscious customers and comply with tightening regulations. Development of solvent-free and recyclable products caters to green building initiatives and sustainability mandates, enhancing competitive advantage.

- •The increasing adoption of polysulfide sealants in the renewable energy sector, particularly in solar panel encapsulation and wind turbine construction, opens new markets. These applications require sealants with excellent weather resistance and flexibility, aligning well with polysulfide properties.

- •Technological advancements enabling faster curing and improved adhesion provide opportunities to reduce application times and labor costs, appealing to end-users seeking operational efficiency. Customizable formulations tailored for specific industry needs foster product differentiation and customer loyalty.

- •Strategic collaborations and joint ventures between sealant manufacturers and construction or aerospace firms can accelerate innovation and market reach. Such partnerships facilitate access to new technologies and customer bases, driving revenue growth.

- •Expansion through digital sales channels and enhanced supply chain integration allows companies to improve market penetration and responsiveness to customer demands. Leveraging e-commerce and data analytics supports targeted marketing and inventory management.

- •Rising demand for multi-functional and hybrid sealants that combine sealing with insulation or bonding capabilities provides avenues for product portfolio diversification and higher-value offerings.

Market Challenges

- •The polysulfide sealant market faces challenges related to raw material price volatility, particularly for key chemical inputs derived from petrochemicals. Fluctuations in prices can impact production costs and profit margins, complicating pricing strategies for manufacturers.

- •Stringent environmental regulations across global markets impose compliance costs and necessitate reformulation of products to reduce volatile organic compounds and hazardous substances. Meeting these evolving standards requires significant R&D investment and can delay product launches.

- •Technical limitations such as longer curing times and sensitivity to application conditions restrict some polysulfide sealants' use in fast-paced industrial environments. Overcoming these constraints demands continuous innovation and may limit adoption in certain segments.

- •Competition from alternative sealing technologies like polyurethane and silicone sealants creates market pressure. These substitutes often feature faster curing and broader temperature ranges, requiring polysulfide manufacturers to differentiate through performance and cost.

- •Supply chain disruptions and logistics complexities, especially amid geopolitical tensions and global pandemics, affect raw material availability and delivery timelines. Such challenges can impact production schedules and customer satisfaction.

- •Limited consumer awareness about the benefits and applications of polysulfide sealants in certain emerging markets hinders market penetration. Educational initiatives and marketing investments are needed to overcome this barrier.

- •High initial costs associated with specialty polysulfide sealants may restrict adoption in price-sensitive markets, necessitating cost optimization and value demonstration strategies.

Regulatory Framework

- •Between 2019 and 2024, multiple global regulatory bodies have introduced stringent limits on volatile organic compounds (VOCs) in sealants, compelling manufacturers to innovate low-VOC polysulfide products. The U.S. Environmental Protection Agency (EPA) and the European Chemicals Agency (ECHA) have enforced new emissions standards, requiring reformulation of traditional sealants to reduce environmental impact without compromising performance.

- •The REACH regulation in Europe mandates the registration and evaluation of chemical substances used in sealants, increasing compliance requirements for global manufacturers supplying this market. This regulation affects raw material sourcing and formulation transparency, driving the adoption of safer and sustainable materials.

- •Safety standards such as ASTM and ISO guidelines have been updated to include testing for durability, chemical resistance, and fire retardancy of polysulfide sealants, influencing product development and quality assurance processes.

- •Regional mandates in Asia-Pacific, including China’s GB standards for construction materials and India’s Bureau of Indian Standards (BIS), have been tightened to address urban air quality and sustainability goals, affecting local manufacturing and import regulations.

- •Government incentives promoting green building certifications like LEED and BREEAM encourage the use of environmentally compliant polysulfide sealants, creating market pull for sustainable product lines.

Market Intelligence

- •15th January 2025, Henkel AG & Co. KGaA launched a new line of low-VOC, bio-based polysulfide sealants designed for sustainable construction applications. These sealants offer enhanced adhesion and chemical resistance while complying with the latest environmental regulations globally. Targeted at infrastructure and aerospace sectors, the product integrates advanced polymer technology to reduce curing time by 20%, improving project efficiency. Henkel’s strategic objective includes expanding its green product portfolio to meet rising demand in North America and Asia-Pacific markets, leveraging existing distribution channels for rapid market penetration. This launch positions Henkel competitively amid increasing regulatory pressures and customer preference for eco-friendly solutions.

- •10th March 2025, Sika AG introduced an innovative modified polysulfide sealant with superior elasticity and fuel resistance tailored for automotive fuel tank applications. This product addresses stringent fuel economy and emission standards by ensuring long-term durability and leak prevention. Sika’s advancement incorporates nanotechnology to enhance molecular bonding, resulting in improved mechanical strength and environmental resistance. The launch supports Sika’s strategic growth in the Asia-Pacific and Latin America regions where automotive manufacturing is rapidly expanding. This innovation reinforces Sika’s position as a technology leader dedicated to sustainable and high-performance sealant solutions.

- •22nd February 2025, Dow Inc. announced a partnership with a leading aerospace manufacturer to co-develop polysulfide sealants that meet next-generation fuel tank sealing requirements. The collaboration focuses on enhancing sealant performance under extreme temperatures and chemical exposure while reducing environmental footprint. Dow’s proprietary formulation technology aims to shorten curing cycles and improve adhesion without compromising flexibility. This strategic alliance is expected to accelerate product development cycles and facilitate entry into new aerospace markets, reinforcing Dow’s commitment to innovation and customer-centric solutions.

- •5th April 2025, BASF SE completed the acquisition of a specialty sealants manufacturer to expand its polysulfide product portfolio and strengthen its presence in emerging markets. The acquisition enables BASF to integrate advanced polymer technologies and broaden application expertise across construction and transportation sectors. This strategic move also enhances BASF’s supply chain capabilities and accelerates innovation by combining R&D resources. The consolidation supports BASF’s vision to deliver sustainable, high-performance sealants worldwide, addressing growing market demands and competitive pressures.

- •Source: Official company press releases and industry publications

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 2.15 Billion |

| Forecast Year Market Size | USD 4.85 Billion |

| CAGR | 8.4% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 8.1% |

| Scope of Report | Market is segmented by Product Type (Single-component Polysulfide Sealants, Two-component Polysulfide Sealants, Preformed Polysulfide Sealants, Modified Polysulfide Sealants, Others), Application (Construction, Aerospace, Automotive, Marine, Electronics), End-Use Industry (Building & Infrastructure, Transportation, Oil & Gas, Electronics & Electrical), Distribution Channel (Direct Sales, Distributors & Wholesalers, Online Retail) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Henkel AG & Co. KGaA (Germany), Sika AG (Switzerland), 3M Company (United States), BASF SE (Germany), Dow Inc. (United States), Wacker Chemie AG (Germany), H.B. Fuller Company (United States), RPM International Inc. (United States), Tremco Incorporated (United States), Arkema Group (France), Illinois Tool Works Inc. (United States), PPG Industries, Inc. (United States), Ashland Global Holdings Inc. (United States), Kuraray Co., Ltd. (Japan), Saint-Gobain S.A. (France), Soudal N.V. (Belgium), Bostik SA (France), Huntsman Corporation (United States), Jowat SE (Germany), Tesa SE (Germany), W.R. Grace & Co. (United States), Carlisle Companies Incorporated (United States), Shin-Etsu Chemical Co., Ltd. (Japan), Sika Group (Switzerland), Mapei S.p.A (Italy) |

Global Polysulfide Sealant Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.