Global Fire Detection and Suppression Systems Market Size, Growth & Revenue 2024-2034

Global Fire Detection and Suppression Systems Market is segmented by Product Type (Smoke Detectors, Heat Detectors, Flame Detectors, Gas Detectors, Manual Call Points), Application (Commercial Buildings, Industrial Facilities, Residential Buildings, Transportation, Data Centers), End-Use Industry (Construction, Manufacturing, Transportation & Logistics, Information Technology), Distribution Channel (Direct Sales, Distributors & Dealers, Online Sales Platforms), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The Global Fire Detection and Suppression Systems market represents a critical domain within safety and security industries, focusing on the prevention and mitigation of fire-related hazards. This market includes a diverse assortment of detection devices such as smoke, heat, flame, and gas detectors, alongside suppression technologies like sprinklers, gaseous agents, and foam systems. These integrated fire safety systems cater to a broad spectrum of applications including commercial buildings, industrial sites, residential properties, transportation sectors, and data centers, reflecting the extensive demand for fire prevention solutions. Increasing urbanization, stringent regulatory frameworks worldwide, and rising awareness regarding fire safety have been primary catalysts driving market expansion. The scope also covers both hardware and software components, including intelligent fire alarm systems and automated suppression controls, highlighting the increasing trend toward smart and connected fire safety solutions. As fire safety remains paramount, the market continues to evolve with innovations aimed at enhancing detection accuracy, reducing false alarms, and improving suppression efficiency to minimize damage and ensure occupant safety globally.

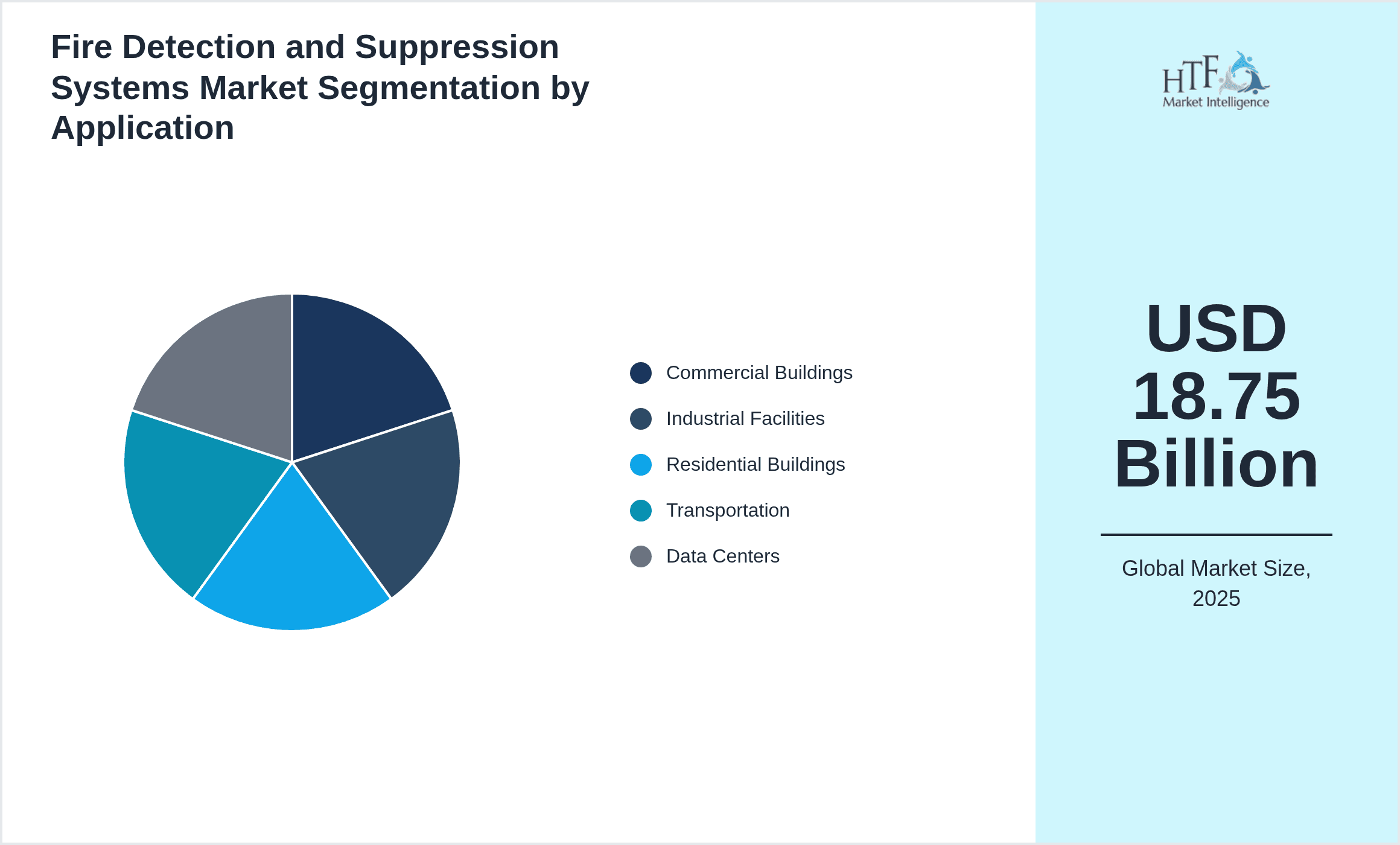

- •Key market highlights indicate a robust CAGR of 8.3% projected from 2024 to 2034, with the base market size estimated at USD 18.75 Billion in 2024 and a forecasted market valuation of USD 42.65 Billion by 2034. North America currently dominates the global market, attributed to early adoption of advanced technologies and stringent fire safety regulations. The Asia-Pacific region is identified as the fastest-growing market due to rapid industrialization and infrastructural development. Smoke detectors maintain the largest product segment share, while gas detectors are expected to witness the highest growth rate, driven by increasing demand in industrial and hazardous environments. Key applications such as commercial buildings and industrial facilities remain pivotal in market penetration, supported by ongoing urban development and safety compliance.

- •The fire detection and suppression systems market holds strategic importance across diverse sectors including construction, manufacturing, transportation, and IT infrastructure. Its value proposition encompasses enhanced safety, regulatory compliance, operational continuity, and risk mitigation. Stakeholders ranging from manufacturers and system integrators to end-users benefit from evolving technologies that include IoT-enabled detectors, AI-driven analytics for early fire prediction, and environmentally friendly suppression agents. The market’s evolution supports government safety mandates and helps reduce economic losses due to fire incidents, making it indispensable for ensuring safety and resilience in critical infrastructure worldwide.

Competitive Landscape

The competitive landscape of the global Fire Detection and Suppression Systems market is characterized by intense rivalry among established multinational corporations and agile regional players. Market participants focus on innovation, strategic partnerships, and mergers & acquisitions to strengthen their market position and broaden product portfolios. Emphasis on research and development has led to the introduction of smart fire detection technologies and integrated systems that combine detection with automated suppression. Competitive strategies also include expanding distribution networks and enhancing customer service to meet diverse industry requirements. Pricing strategies are influenced by technology sophistication and compliance with regional safety standards. The competition is further intensified by the growing demand for environmentally sustainable suppression agents and the incorporation of IoT and AI in fire safety solutions. Barriers to entry remain significant due to the stringent regulatory environment and the necessity for certification, which favors established players with robust compliance and innovation capabilities. Looking forward, the market is expected to witness consolidation trends alongside increased focus on digital transformation and customized solutions.

Companies Shaping the Fire Detection and Suppression Systems Market

- •Johnson Controls International (United States)

- •Honeywell International Inc. (United States)

- •Siemens AG (Germany)

- •Tyco International (United States)

- •UTC Climate, Controls & Security (United States)

- •Bosch Security Systems (Germany)

- •United Technologies Corporation (United States)

- •Schneider Electric (France)

- •Chubb Fire & Security (United Kingdom)

- •Carrier Global Corporation (United States)

- •Fike Corporation (United States)

- •Minimax Viking Group (Germany)

- •Nohmi Bosai Ltd. (Japan)

- •Kidde (United States)

- •Apollo Fire Detectors Ltd. (United Kingdom)

- •Argus Security Systems (United Kingdom)

- •Cerberus Pyrotronics (Germany)

- •EST Fire & Security (Denmark)

- •Notifier (United States)

- •Tyco SimplexGrinnell (United States)

- •Honeywell Analytics (United States)

- •Bosch Building Technologies (Germany)

- •Siemens Building Technologies (Germany)

- •Schneider Electric Buildings (France)

- •Panasonic Corporation (Japan)

Market Breakdown

- •By Product Type

- ◦Smoke Detectors

- ◦Heat Detectors

- ◦Flame Detectors

- ◦Gas Detectors

- ◦Manual Call Points

- •By Application

- ◦Commercial Buildings

- ◦Industrial Facilities

- ◦Residential Buildings

- ◦Transportation

- ◦Data Centers

- •By End-Use Industry

- ◦Construction

- ◦Manufacturing

- ◦Transportation & Logistics

- ◦Information Technology

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors & Dealers

- ◦Online Sales Platforms

Growth Dynamics

- •Increasing urbanization and industrialization worldwide have significantly driven demand for advanced fire detection and suppression systems, particularly in rapidly developing regions such as Asia-Pacific. The expansion of commercial and residential infrastructure necessitates enhanced fire safety compliance, fueling market growth.

- •Technological advancements such as IoT-enabled fire detection devices and AI-powered analytics enable faster and more accurate fire detection, reducing false alarms and improving response times, which boosts adoption and market expansion.

- •Stringent government regulations and international safety standards across developed and developing countries have mandated the installation of sophisticated fire safety systems, thereby creating sustained demand and encouraging modernization of legacy systems.

- •Rising awareness among businesses and homeowners about fire hazards and insurance benefits linked to fire safety compliance is leading to increased investment in fire detection and suppression technologies across multiple sectors.

- •Growing integration of fire detection systems with building management and security solutions is enhancing operational efficiency and fire safety, promoting market growth through cross-sector adoption and smart infrastructure development.

- •Government incentives and subsidies for upgrading fire safety infrastructure, especially in emerging economies, are encouraging market penetration and technological adoption among small and medium enterprises.

- •The rising frequency of fire incidents and natural disasters worldwide underscores the critical need for reliable fire safety systems, prompting stakeholders to prioritize investment in advanced detection and suppression solutions.

Market Trends

- •The adoption of wireless and battery-operated fire detection systems is gaining momentum, offering flexible installation and lower maintenance costs, especially in retrofit projects and remote locations.

- •Integration of fire detection systems with smart building technologies and IoT platforms is enabling real-time monitoring, predictive maintenance, and automated emergency response, reshaping the market landscape.

- •Environmental sustainability trends are driving the development of eco-friendly fire suppression agents that minimize ozone depletion and environmental impact, aligning with global climate action initiatives.

- •The increasing use of multi-sensor detectors combining smoke, heat, and gas detection capabilities enhances accuracy and reduces false alarms, becoming a preferred choice in high-risk industries.

- •Collaborations and partnerships between technology providers and fire safety companies are fostering innovation, enabling rapid deployment of integrated fire safety solutions tailored to sector-specific needs.

- •The rise of cloud-based fire safety management platforms allows centralized control and analytics, improving fire risk assessment and compliance reporting across large enterprises and multi-site operations.

- •Emerging markets in Latin America and the Middle East are witnessing increased fire safety investments driven by infrastructure development and regulatory reforms, presenting new growth avenues.

Market Opportunities

- •There is significant potential to expand fire detection and suppression solutions in emerging economies where urbanization and industrial growth are accelerating, yet fire safety infrastructure remains underdeveloped.

- •Development of AI and machine learning-based fire detection algorithms offers opportunities for creating highly adaptive and predictive fire safety systems that can revolutionize incident prevention.

- •Integration of fire safety solutions with renewable energy and smart grid infrastructures presents new market opportunities, especially in regions focusing on sustainable urban development.

- •Expanding aftermarket services such as system upgrades, maintenance, and monitoring create recurring revenue streams and foster customer loyalty in the fire safety ecosystem.

- •Collaborations with insurance companies to offer premium discounts for installations of advanced fire safety systems can drive adoption among residential and commercial customers.

- •Innovations in miniaturized and portable fire detection devices enable penetration into niche applications such as transportation and small-scale industrial setups, broadening market reach.

- •Government-backed smart city initiatives emphasizing integrated safety solutions provide a platform for large-scale deployment of next-generation fire detection and suppression technologies.

Market Challenges

- •High initial installation and integration costs of advanced fire detection and suppression systems remain a barrier for small and medium enterprises, limiting widespread adoption in price-sensitive markets.

- •Complexity in complying with diverse regulatory standards across different regions poses challenges for manufacturers and system integrators in ensuring universal market acceptance.

- •False alarms from sensitive detection devices can lead to operational disruptions and increased maintenance expenses, affecting end-user confidence and system reputation.

- •Limited awareness and lack of trained personnel to operate and maintain sophisticated fire safety systems hinder effective deployment, particularly in developing regions.

- •Supply chain disruptions and raw material price volatility impact manufacturing costs and delivery timelines, challenging market stability and profitability.

- •Rapid technological evolution demands continuous product innovation and upgrades, imposing significant R&D investment burdens on market participants and complicating legacy system compatibility.

- •Environmental concerns over certain chemical suppression agents and disposal issues necessitate costly compliance measures and alternative technology development.

Regulatory Framework

- •Between 2019 and 2024, several key regulations have shaped the fire detection and suppression systems market globally. The NFPA (National Fire Protection Association) codes have been updated with enhanced requirements for detector sensitivity and system integration, significantly influencing North American market standards. These regulations mandate periodic system testing and certification, ensuring higher reliability and safety compliance.

- •The European Union introduced the Construction Products Regulation (CPR) updates in 2020, emphasizing the performance and safety of fire detection devices in building materials and systems. This has driven manufacturers to align products with harmonized standards to facilitate pan-European market access.

- •In Asia-Pacific, countries like Japan and Australia have revised their fire safety codes to incorporate modern fire suppression technologies and IoT-based monitoring systems, fostering innovation and regulatory compliance in the region.

- •Environmental regulations such as the Montreal Protocol have impacted the use of halon-based suppression agents, pushing the market towards eco-friendly alternatives and compliance with global environmental safety standards.

- •Government initiatives promoting smart city and critical infrastructure security include mandates for integrated fire detection and suppression systems, supported by subsidies and incentives to accelerate adoption and ensure public safety.

Market Intelligence

- •15th February 2025, Johnson Controls International launched a next-generation IoT-enabled fire detection system designed for commercial and industrial applications. This system integrates AI-powered analytics for real-time fire risk prediction, reducing false alarms by over 30%, and features wireless connectivity for seamless monitoring and maintenance. The launch aims to enhance fire safety in smart buildings and critical infrastructure, supporting regulatory compliance and operational efficiency globally. This innovation positions the company as a leader in the evolving fire safety technology landscape. Source: Johnson Controls Official Press Release.

- •10th April 2025, Honeywell International Inc. introduced an eco-friendly gaseous fire suppression agent compliant with the latest environmental regulations under the Montreal Protocol. The product offers high efficiency in extinguishing fires without ozone depletion or global warming potential, targeting data centers and industrial plants requiring sustainable fire suppression solutions. Honeywell’s strategic objective is to capture growing demand in regions enforcing strict environmental standards, consolidating its market presence in the Asia-Pacific and European markets. Source: Honeywell Corporate News.

- •22nd January 2025, Siemens AG announced a strategic partnership with a leading AI software provider to develop integrated fire detection platforms that leverage machine learning for early fire detection and predictive maintenance. This collaboration focuses on enhancing system accuracy and reducing response times, targeting commercial and transportation sectors worldwide. The initiative is part of Siemens’ broader digital transformation strategy to expand smart infrastructure solutions and strengthen market competitiveness. Source: Siemens Press Release.

- •8th March 2025, Tyco International completed the acquisition of a regional fire safety solutions provider specializing in wireless detection technologies. This acquisition expands Tyco’s product portfolio and regional footprint in Latin America and the Middle East. The deal is expected to generate synergies through combined R&D efforts and broadened distribution channels, accelerating growth in emerging markets with increasing fire safety infrastructure investments. Source: Tyco International News.

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 18.75 Billion |

| Forecast Year Market Size | USD 42.65 Billion |

| CAGR | 8.3% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7.97% |

| Scope of Report | Market is segmented by Product Type (Smoke Detectors, Heat Detectors, Flame Detectors, Gas Detectors, Manual Call Points), Application (Commercial Buildings, Industrial Facilities, Residential Buildings, Transportation, Data Centers), End-Use Industry (Construction, Manufacturing, Transportation & Logistics, Information Technology), Distribution Channel (Direct Sales, Distributors & Dealers, Online Sales Platforms) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Johnson Controls International (United States), Honeywell International Inc. (United States), Siemens AG (Germany), Tyco International (United States), UTC Climate, Controls & Security (United States) |

Global Fire Detection and Suppression Systems Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.