Global Dual Fuel Burner Market Size, Growth & Revenue 2025-2034

Global Dual Fuel Burner Market is segmented by Product Type (Gas-Diesel Burner, Oil-Gas Burner, LPG-Diesel Burner, Natural Gas-LPG Burner, Bi-Fuel Burner), Application (Power Generation, Industrial Heating, Residential Heating, Commercial Heating, Transportation), End-Use Industry (Energy & Utilities, Manufacturing, Oil & Gas, Transportation), Distribution Channel (Direct Sales, Distributors, Online Platforms), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global dual fuel burner market represents a critical segment in the energy and combustion technology sector, providing versatile and efficient burner systems capable of utilizing two distinct fuel sources to optimize performance and reduce operational costs. These burners are widely adopted across power generation, industrial heating, residential and commercial heating, and transportation applications, where fuel flexibility is essential to meet fluctuating fuel availability and stringent environmental regulations. The market's evolution is shaped by technological advancements that enhance combustion efficiency, reduce emissions, and improve integration with smart energy management and control systems. Increasing demand for cleaner energy solutions and the need to comply with global emission standards have accelerated the adoption of dual fuel burners, particularly in regions with variable fuel supply infrastructure. The market is further influenced by the rising fuel price volatility and government incentives promoting energy-efficient combustion technologies. Industry stakeholders including manufacturers, technology providers, and end-users are investing heavily in R&D to develop innovative burner designs that offer superior fuel adaptability, lower maintenance requirements, and enhanced safety features. As a result, the dual fuel burner market is forecasted to experience robust growth through 2034, driven by both emerging economies and mature markets seeking sustainable and cost-effective heating and power generation solutions.

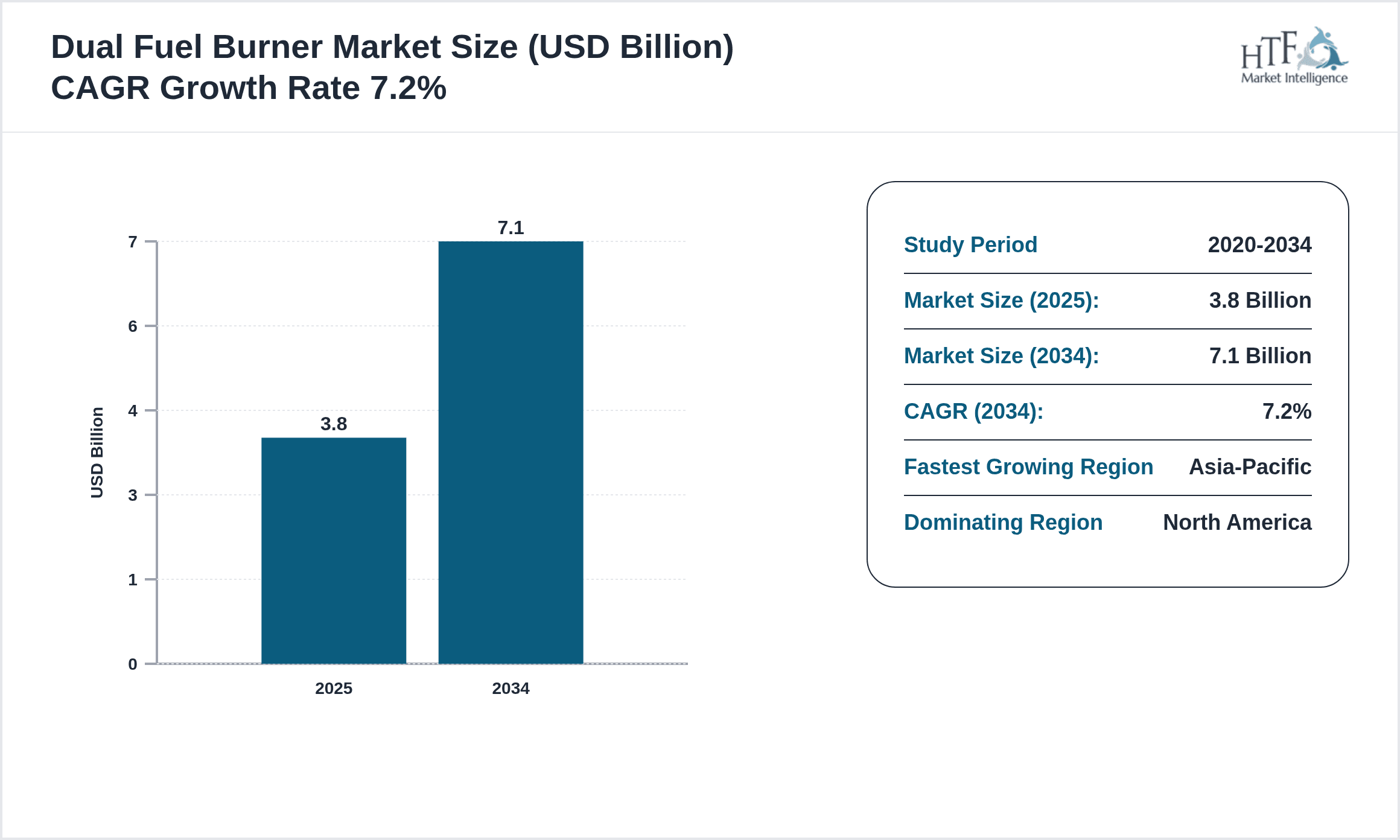

- •Key highlights of the market include a base market size of USD 3.8 Billion in 2025, expected to reach USD 7.1 Billion by 2034, with a compound annual growth rate (CAGR) of 7.2%. The year-on-year growth rate remains steady at approximately 7.0%, reflecting strong demand across all major regions. North America currently dominates the market due to early adoption of advanced burner technologies and stringent emission control mandates, while Asia-Pacific emerges as the fastest-growing region fueled by rapid industrialization and expanding energy infrastructure. Gas-Diesel burners maintain leadership in product types owing to their proven reliability and efficiency, whereas bi-fuel burners are gaining traction for their environmental benefits and fuel adaptability. The market is characterized by a dynamic competitive landscape with increasing strategic collaborations, product innovations, and regional expansions by key players to capitalize on growth opportunities.

- •The dual fuel burner market holds significant strategic importance for various industries including power generation, manufacturing, and transportation sectors as it enables operational flexibility and compliance with evolving environmental standards. Its value proposition lies in optimizing fuel utilization, reducing greenhouse gas emissions, and ensuring uninterrupted operations despite fuel supply uncertainties. For investors and stakeholders, this market offers substantial growth potential driven by technological innovation, regulatory support, and emerging applications in smart energy systems. The market also supports sustainable development goals by contributing to cleaner combustion technologies and facilitating the transition towards diversified energy portfolios across regions.

Competitive Landscape

The global dual fuel burner market is characterized by intense competition among established multinational corporations and emerging regional players, each leveraging innovation, strategic partnerships, and geographic expansion to strengthen market presence. Leading companies adopt differentiated strategies focusing on product quality, energy efficiency, and environmental compliance to meet diverse customer requirements. The competitive environment is shaped by rapid technological advancements in combustion control systems, fuel flexibility, and emission reduction technologies. Companies invest significantly in R&D to develop advanced burners that integrate IoT-enabled monitoring and predictive maintenance capabilities, enhancing operational reliability and reducing downtime. Market players also engage in mergers and acquisitions to consolidate their position, expand product portfolios, and enter new markets, thereby increasing market fragmentation. Pricing strategies are calibrated to balance profitability with competitive positioning, while distribution channels are optimized to ensure extensive market reach across industrial, commercial, and residential segments. Regulatory compliance and adaptation to region-specific standards remain critical competitive factors, influencing product development and market entry decisions. Looking ahead, the competitive landscape is expected to witness further consolidation and innovation-driven rivalry as companies aim to capitalize on the growing demand for sustainable and efficient dual fuel burner solutions worldwide.

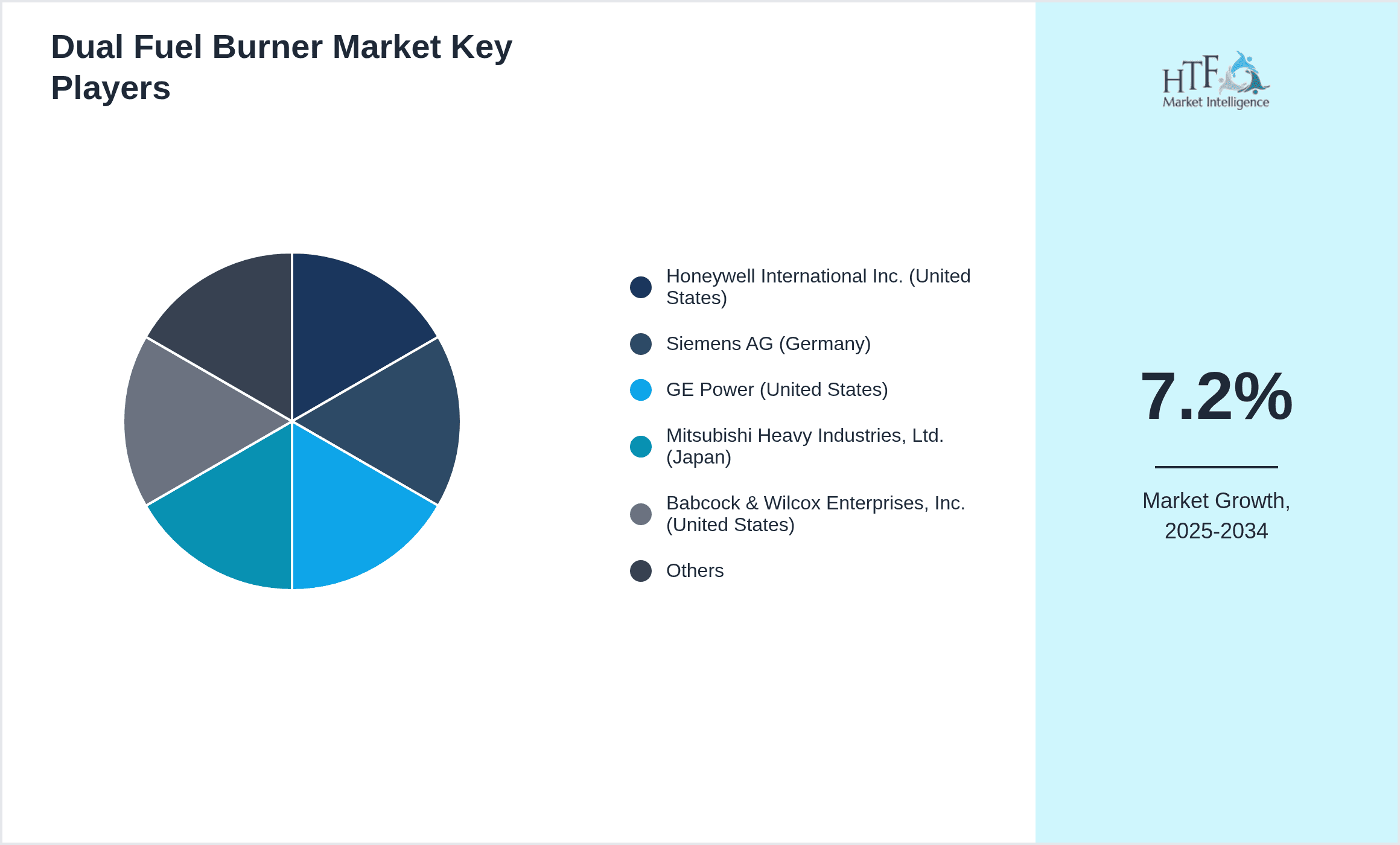

Prominent Players in Dual Fuel Burner Market

- •Honeywell International Inc. (United States)

- •Siemens AG (Germany)

- •GE Power (United States)

- •Mitsubishi Heavy Industries, Ltd. (Japan)

- •Babcock & Wilcox Enterprises, Inc. (United States)

- •Fives Group (France)

- •Coen Company (United States)

- •Eclipse, Inc. (United States)

- •Riello Burners Group (Italy)

- •Zeeco, Inc. (United States)

- •Baltur S.p.A. (Italy)

- •John Zink Hamworthy Combustion (United States)

- •Saacke GmbH (Germany)

- •Weishaupt GmbH (Germany)

- •Elster Group SE (Germany)

- •Maxon Corporation (United States)

- •Beijing Huayuan Group (China)

- •Atlas Copco AB (Sweden)

- •Chongqing Boiler Group (China)

- •Lattner Energy Solutions (United States)

- •Toshiba Corporation (Japan)

- •Andritz AG (Austria)

- •John Wood Group PLC (United Kingdom)

- •Viessmann Group (Germany)

- •Caterpillar Inc. (United States)

Market Breakdown

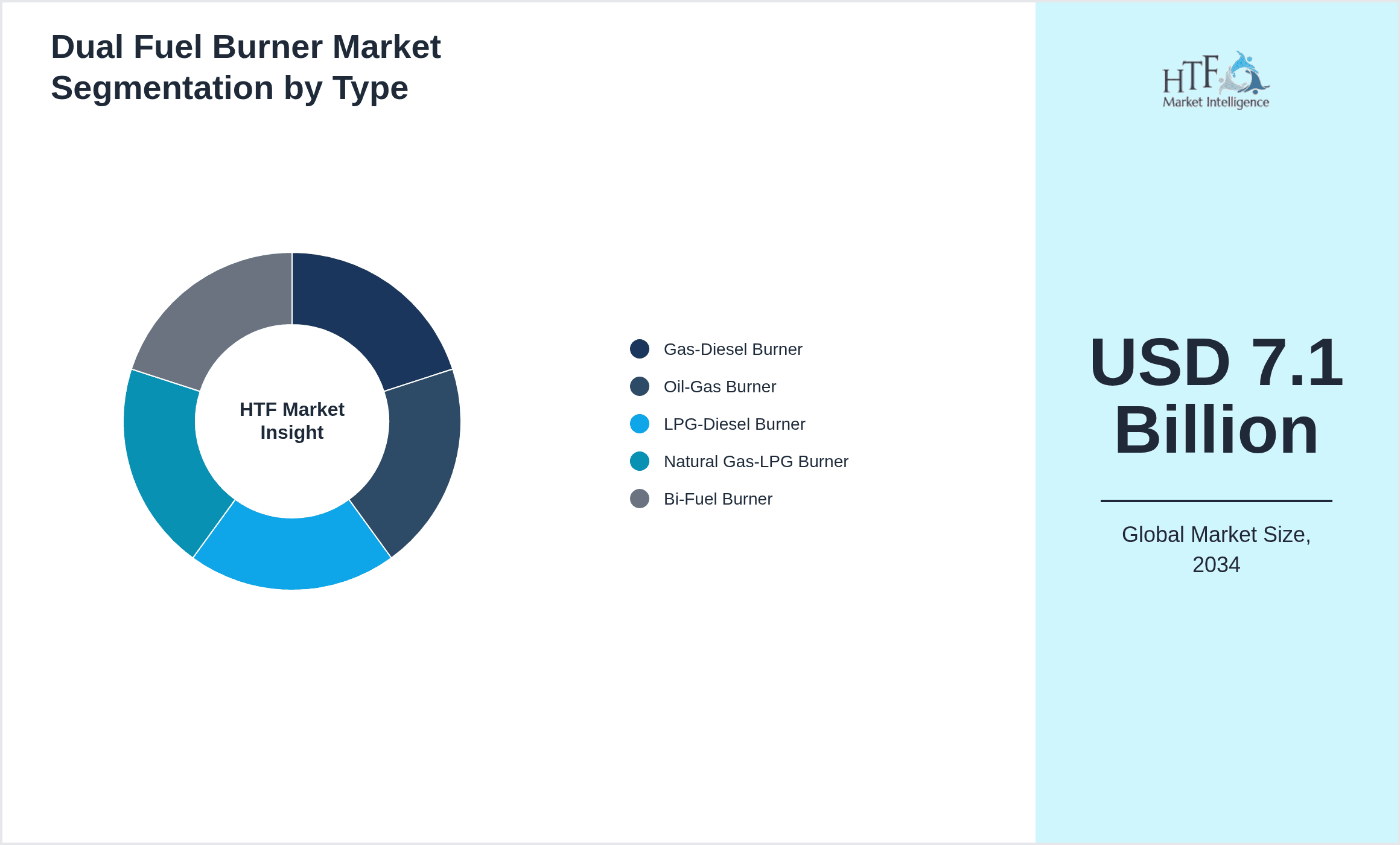

- •By Product Type

- ◦Gas-Diesel Burner

- ◦Oil-Gas Burner

- ◦LPG-Diesel Burner

- ◦Natural Gas-LPG Burner

- ◦Bi-Fuel Burner

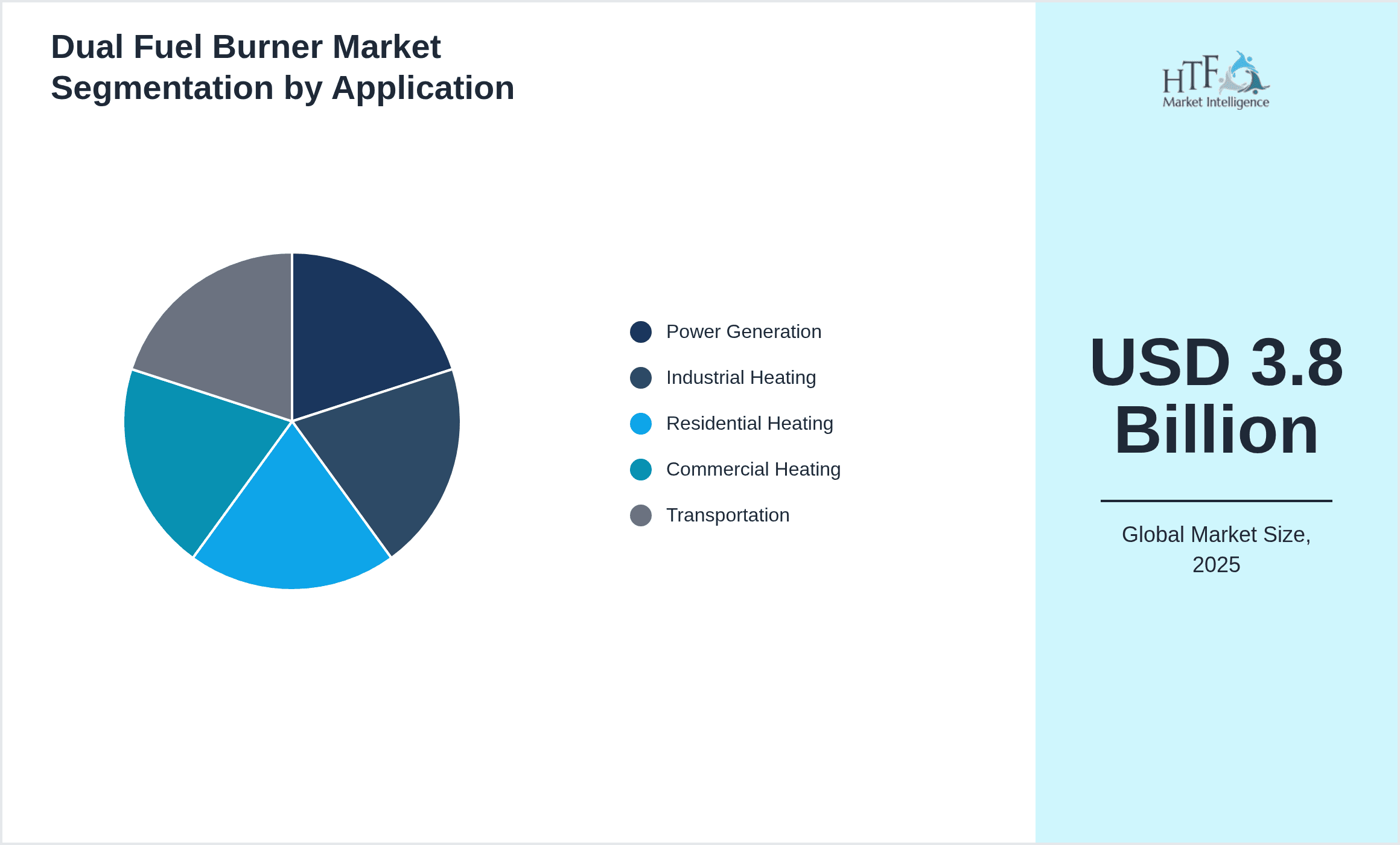

- •By Application

- ◦Power Generation

- ◦Industrial Heating

- ◦Residential Heating

- ◦Commercial Heating

- ◦Transportation

- •By End-Use Industry

- ◦Energy & Utilities

- ◦Manufacturing

- ◦Oil & Gas

- ◦Transportation

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors

- ◦Online Platforms

Growth Dynamics

The global dual fuel burner market growth is primarily driven by the increasing demand for fuel flexibility and efficiency across various sectors, including power generation and industrial heating. The ability to switch between gaseous and liquid fuels enables end-users to optimize operational costs amid fluctuating fuel prices and availability. Additionally, stringent environmental regulations worldwide are compelling industries to adopt combustion technologies that reduce emissions, positioning dual fuel burners as a preferred solution. Technological advancements such as integration with smart control systems and IoT-enabled monitoring further enhance burner performance and reliability, stimulating market expansion. The rising focus on reducing carbon footprints and improving energy efficiency in emerging economies, especially in Asia-Pacific, is creating substantial demand. Moreover, government incentives promoting cleaner fuel technologies and infrastructure modernization are catalyzing adoption. These factors collectively contribute to a robust CAGR forecast and sustained year-on-year market growth through 2034.

Market Trends

A prominent market trend is the increasing integration of automation and digital monitoring technologies into dual fuel burners, enabling real-time performance tracking, predictive maintenance, and enhanced fuel management. This trend supports operational efficiency and reduces downtime for end-users. Additionally, the adoption of bi-fuel burners combining renewable fuels with conventional sources reflects the market's move towards sustainability. Strategic collaborations among burner manufacturers and technology providers are fostering innovation and accelerating product development. Furthermore, the expansion of dual fuel burner applications into emerging sectors such as transportation and smart buildings illustrates market diversification. Regulatory pressures continue to drive advancements in low-emission burner designs, while regional growth disparities highlight the importance of localized solutions tailored to specific fuel availability and environmental norms.

Market Opportunities

Significant opportunities exist in expanding dual fuel burner adoption within emerging economies undergoing rapid industrialization and infrastructure development, particularly in Asia-Pacific and Latin America. The growing focus on energy efficiency and emission reductions creates demand for advanced burner technologies that can operate on alternative and renewable fuels. Additionally, retrofitting existing single-fuel burner installations with dual fuel systems presents a lucrative market segment. Technological innovations enabling seamless fuel switching and enhanced combustion control offer prospects for differentiation and premium product offerings. Strategic partnerships with regional distributors and service providers can facilitate market penetration. Furthermore, increasing investments in smart energy management systems present integration opportunities, enabling manufacturers to offer comprehensive energy solutions beyond traditional burner products.

Market Challenges

The dual fuel burner market faces challenges including high initial capital expenditure for advanced burner systems and integration with digital controls, which can deter adoption among cost-sensitive end-users. Variability in fuel quality and supply infrastructure across regions complicates burner design and operation, necessitating robust customization. Regulatory compliance requires continuous product innovation to meet evolving emission standards, increasing R&D costs. Moreover, competition from alternative heating technologies such as electric heating and renewable energy sources poses a threat to market share. Supply chain disruptions and raw material price volatility can impact manufacturing costs and delivery timelines. Additionally, lack of skilled workforce for installation and maintenance of sophisticated dual fuel systems in certain regions presents operational challenges.

Regulatory Framework

Between 2020 and 2025, key regulatory developments worldwide have shaped the dual fuel burner market landscape by imposing stringent emission limits and efficiency standards. The US Environmental Protection Agency (EPA) tightened regulations on nitrogen oxides (NOx) and sulfur oxides (SOx) emissions from combustion equipment, compelling manufacturers to innovate lower-emission burners. Similarly, the European Union’s Industrial Emissions Directive (IED) established strict limits on industrial burner emissions, promoting adoption of best available technologies (BAT). In Asia-Pacific, countries such as China and India introduced policies incentivizing energy-efficient and cleaner fuel combustion systems to reduce urban pollution. These regulations mandate compliance with safety, environmental, and operational standards, affecting burner design and certification processes. Governments also introduced subsidies and tax incentives to encourage adoption of advanced dual fuel burners that support energy transition goals. Regulatory frameworks continue to evolve, requiring manufacturers to maintain compliance agility and invest in continuous product improvements to meet regional mandates.

Market Intelligence

- •15th January 2025, Honeywell International Inc. launched a next-generation dual fuel burner featuring IoT-enabled combustion control and real-time emissions monitoring designed for industrial heating applications. The product integrates advanced sensors and AI algorithms to optimize fuel mix and reduce emissions by up to 20%, targeting energy-intensive sectors seeking compliance with evolving environmental standards. Honeywell aims to expand its market share in North America and Asia-Pacific through this innovative offering, enhancing operational efficiency and predictive maintenance capabilities for end-users. This launch underscores the growing importance of digital transformation in burner technology and positions Honeywell as a leader in sustainable combustion solutions. Source: Honeywell Official Press Release

- •22nd March 2025, Siemens AG introduced its latest bi-fuel burner model capable of seamless switching between natural gas and hydrogen-enriched fuels, catering to the growing demand for low-carbon energy solutions. The burner’s design supports retrofitting existing systems with minimal downtime and offers enhanced safety features compliant with international standards. Siemens targets markets in Europe and Asia-Pacific where hydrogen adoption is accelerating as part of energy transition strategies. The innovation aligns with regulatory efforts to reduce carbon footprints and demonstrates Siemens' commitment to advancing sustainable industrial technologies. Source: Siemens Corporate Announcement

- •5th July 2024, GE Power announced a strategic partnership with a leading renewable energy provider to develop hybrid dual fuel burner systems integrating biofuels and conventional fuels for power generation plants. This collaboration aims to facilitate cleaner energy production and support decarbonization targets in North America and Europe. The joint initiative focuses on R&D, pilot projects, and commercialization of advanced burner technologies that improve fuel efficiency and reduce greenhouse gas emissions. The partnership enhances GE’s market competitiveness and broadens its product portfolio to address evolving energy demands. Source: GE Power Industry News

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 3.8 Billion |

| Forecast Year Market Size | USD 7.1 Billion |

| CAGR | 7.2% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7% |

| Scope of Report | Market is segmented by Product Type (Gas-Diesel Burner, Oil-Gas Burner, LPG-Diesel Burner, Natural Gas-LPG Burner, Bi-Fuel Burner), Application (Power Generation, Industrial Heating, Residential Heating, Commercial Heating, Transportation), End-Use Industry (Energy & Utilities, Manufacturing, Oil & Gas, Transportation), Distribution Channel (Direct Sales, Distributors, Online Platforms) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Honeywell International Inc. (United States), Siemens AG (Germany), GE Power (United States), Mitsubishi Heavy Industries, Ltd. (Japan), Babcock & Wilcox Enterprises, Inc. (United States), Fives Group (France), Coen Company (United States), Eclipse, Inc. (United States), Riello Burners Group (Italy), Zeeco, Inc. (United States), Baltur S.p.A. (Italy), John Zink Hamworthy Combustion (United States), Saacke GmbH (Germany), Weishaupt GmbH (Germany), Elster Group SE (Germany), Maxon Corporation (United States), Beijing Huayuan Group (China), Atlas Copco AB (Sweden), Chongqing Boiler Group (China), Lattner Energy Solutions (United States), Toshiba Corporation (Japan), Andritz AG (Austria), John Wood Group PLC (United Kingdom), Viessmann Group (Germany), Caterpillar Inc. (United States) |

Global Dual Fuel Burner Market Size, Growth & Revenue 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.