Global Aircraft Environmental Control Systems Market Size, Growth & Revenue 2025-2034

Global Aircraft Environmental Control Systems Market is segmented by Type (Air Cycle Machines, Water Separation Systems, Gas Turbine Engine, Air Conditioning Packs, Cabin Pressure Controllers), Application (Commercial Aircraft, Military Aircraft, Business Jets, Helicopters, Unmanned Aerial Vehicles), End-Use Industry (Commercial Aviation, Defense & Military, Business Aviation, Unmanned Aerial Systems), Distribution Channel (OEM, Aftermarket, Maintenance, Repair and Overhaul (MRO)), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The Aircraft Environmental Control Systems market encompasses advanced technologies and components aimed at regulating air quality, temperature, humidity, and cabin pressure in various aircraft including commercial, military, and business jets. These systems, comprising air cycle machines, water separation units, gas turbine engines, air conditioning packs, and cabin pressure controllers, play a critical role in ensuring passenger comfort, crew safety, and regulatory compliance. The market scope includes design, manufacturing, integration, and maintenance of these systems globally, addressing evolving environmental norms and technological innovations. With increasing air travel demand and stringent environmental regulations, ECS have become indispensable in modern aerospace operations, impacting fuel efficiency and operational reliability. Key applications span commercial aviation, defense sectors, and unmanned aerial vehicles, reflecting the broad industry relevance and continuous technological advancements driving market growth worldwide.

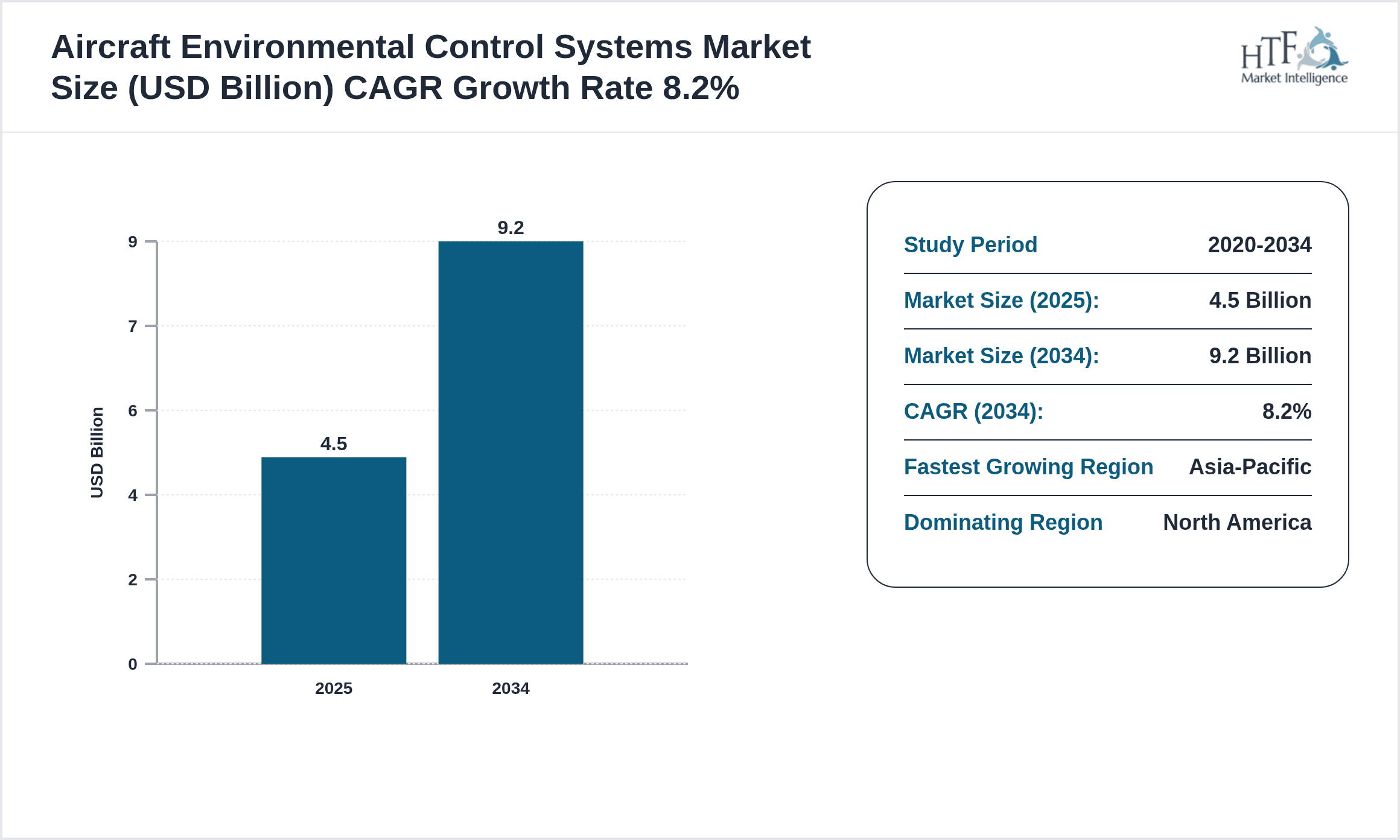

- •The global Aircraft Environmental Control Systems market is projected to grow from USD 4.5 Billion in 2025 to USD 9.2 Billion by 2034, exhibiting a robust CAGR of 8.2 percent. North America leads the market in terms of revenue share, while Asia-Pacific registers the fastest growth due to increasing aircraft manufacturing and modernization programs. Air cycle machines dominate the product segment owing to their efficiency and reliability, whereas cabin pressure controllers represent the fastest growing product type driven by enhanced safety regulations. Commercial aircraft application remains the largest segment, supported by rising passenger traffic and fleet expansion globally. These dynamics underscore the increasing strategic importance of ECS in the aerospace ecosystem, with technological innovation and regulatory compliance shaping market trajectories.

- •Aircraft Environmental Control Systems provide critical value to aerospace manufacturers, airlines, defense agencies, and maintenance providers by enhancing passenger experience, ensuring operational safety, and improving fuel efficiency. The market's growth offers strategic opportunities for technology developers and component suppliers to innovate with lightweight, energy-efficient, and digitally integrated ECS solutions. As global air travel rebounds and defense modernization accelerates, ECS manufacturers benefit from expanding aircraft fleets and retrofit demand. This market also contributes to sustainability goals by enabling reduced emissions through optimized environmental controls. Stakeholders across manufacturing, services, and aftermarket operations gain competitive advantages through advanced ECS capabilities, positioning the segment as a pivotal element of aerospace industry growth and future readiness.

Competitive Landscape

The competitive environment in the Aircraft Environmental Control Systems market is characterized by a high degree of innovation, strategic partnerships, and global expansion initiatives. Leading companies focus on developing energy-efficient, lightweight, and digitally enabled ECS components to meet rising regulatory standards and customer expectations for comfort and safety. Firms invest heavily in research and development to integrate IoT and predictive maintenance capabilities, enhancing system reliability and reducing lifecycle costs. Strategic collaborations with aircraft manufacturers and defense organizations facilitate co-development of customized ECS solutions tailored to emerging aircraft platforms. Mergers and acquisitions serve to consolidate technological expertise and expand geographic reach. Market participants adopt multi-channel distribution strategies and after-sales service networks to sustain market presence and capture aftermarket opportunities. Regional competition intensifies as Asia-Pacific manufacturers increase capabilities, prompting global players to reinforce innovation pipelines and local partnerships to maintain competitive advantages and market share.

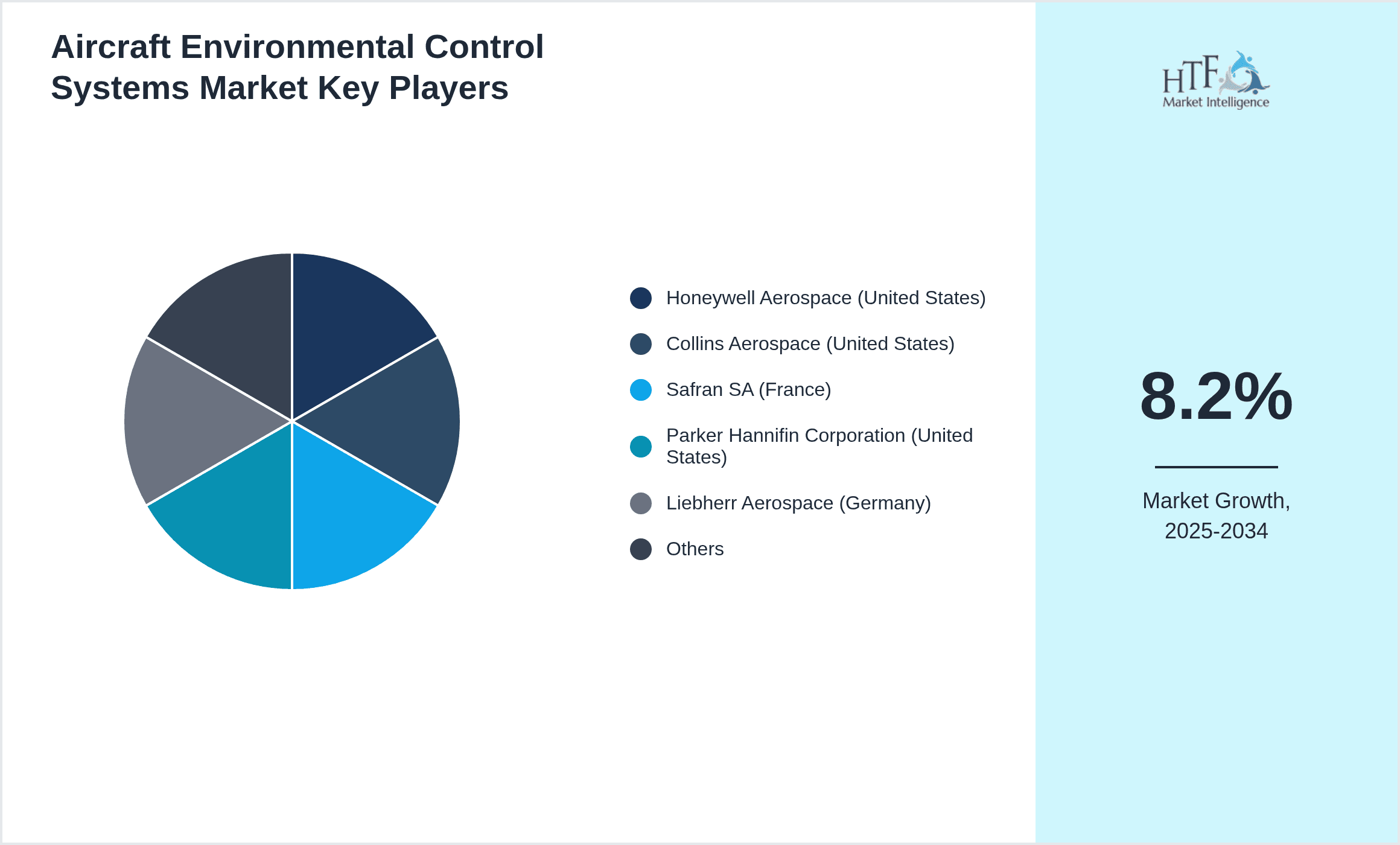

Key Players in Aircraft Environmental Control Systems Market

- •Honeywell Aerospace (United States)

- •Collins Aerospace (United States)

- •Safran SA (France)

- •Parker Hannifin Corporation (United States)

- •Liebherr Aerospace (Germany)

- •MTU Aero Engines (Germany)

- •Eaton Corporation (United States)

- •UTC Aerospace Systems (United States)

- •B/E Aerospace (United States)

- •GKN Aerospace (United Kingdom)

- •Triumph Group, Inc. (United States)

- •Moog Inc. (United States)

- •Avio Aero (Italy)

- •Meggitt PLC (United Kingdom)

- •SAFRAN Electrical & Power (France)

- •Thales Group (France)

- •CIRCOR Aerospace (United States)

- •General Electric Aviation (United States)

- •Woodward, Inc. (United States)

- •Kongsberg Defence & Aerospace (Norway)

Market Breakdown

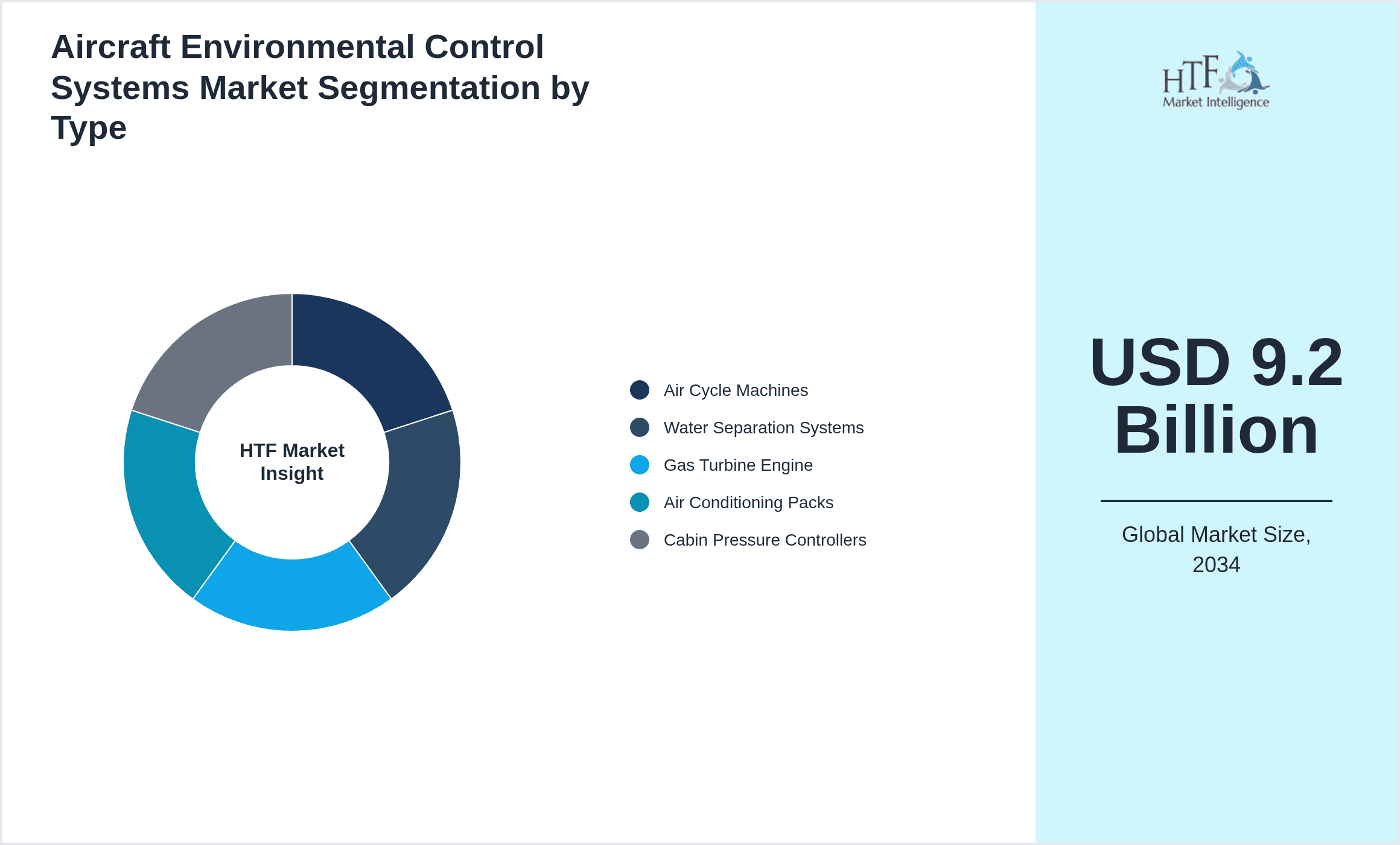

- •By Type

- ◦Air Cycle Machines

- ◦Water Separation Systems

- ◦Gas Turbine Engine

- ◦Air Conditioning Packs

- ◦Cabin Pressure Controllers

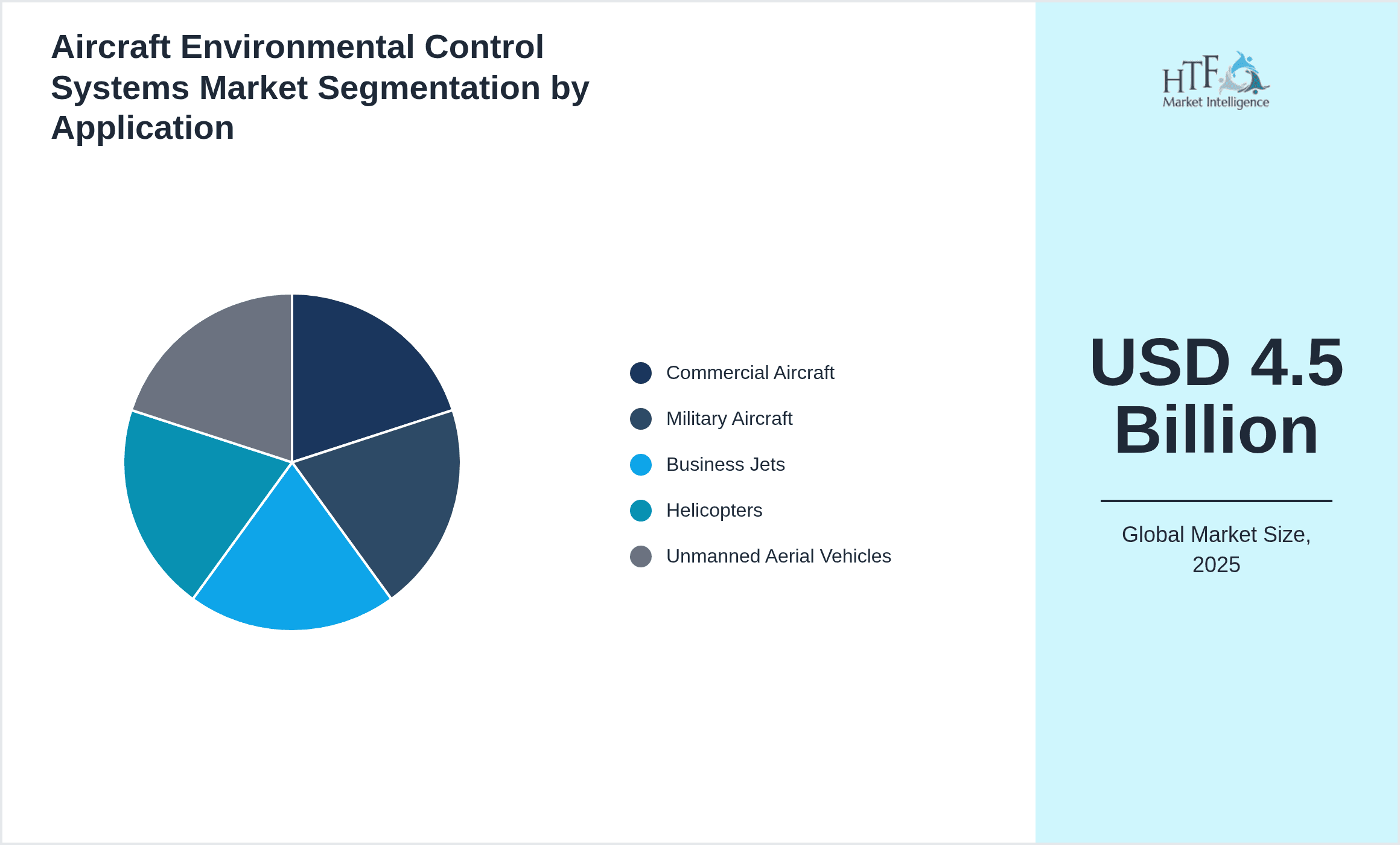

- •By Application

- ◦Commercial Aircraft

- ◦Military Aircraft

- ◦Business Jets

- ◦Helicopters

- ◦Unmanned Aerial Vehicles

- •By End-Use Industry

- ◦Commercial Aviation

- ◦Defense & Military

- ◦Business Aviation

- ◦Unmanned Aerial Systems

- •By Distribution Channel

- ◦OEM

- ◦Aftermarket

- ◦Maintenance, Repair and Overhaul (MRO)

Growth Dynamics

The Aircraft Environmental Control Systems market exhibits strong growth momentum driven by expanding global air traffic and fleet modernization across commercial and defense sectors. Increasing demand for fuel-efficient and environmentally compliant ECS solutions propelled by stringent international aviation emissions regulations enhances market expansion. Technological advancements in lightweight materials and digital integration facilitate improved system performance, reducing operational costs and enhancing passenger comfort. Development of electric and hybrid aircraft platforms further stimulates ECS innovation. Recent contracts awarded to leading manufacturers for next-generation commercial aircraft programs demonstrate escalating market investment. Additionally, retrofitting aging aircraft with advanced ECS modules provides significant aftermarket growth opportunities. These factors collectively underpin the sustained CAGR of over 8 percent forecasted through 2034, positioning ECS as a critical growth segment within aerospace technologies.

Market Trends

The Aircraft Environmental Control Systems market trends emphasize integration of smart sensors and IoT-enabled monitoring for predictive maintenance and real-time system diagnostics. Adoption of additive manufacturing techniques accelerates lightweight component production, enhancing ECS efficiency and reducing costs. Digital twin technologies facilitate virtual testing and optimization of ECS performance across different aircraft models. Growing focus on sustainable aviation fuels and electric propulsion systems influences ECS design adaptations to new thermal management requirements. Furthermore, partnerships between aerospace OEMs and technology firms promote innovation in cabin air quality and pressure control systems. Increased investments in hybrid-electric and unmanned aerial vehicles also drive customized ECS solutions addressing unique operational environments. These trends reflect the industry's commitment to advancing safety, comfort, and environmental sustainability through continuous ECS innovations.

Market Opportunities

Emerging markets in Asia-Pacific and Latin America offer substantial growth avenues for Aircraft Environmental Control Systems due to expanding commercial aircraft production and increasing defense modernization programs. Retrofit opportunities for legacy fleets present significant potential for aftermarket ECS upgrades focused on enhancing energy efficiency and cabin comfort. Development of next-generation electric and hybrid aircraft platforms opens pathways for innovative ECS designs tailored to novel propulsion systems. Collaborations between ECS manufacturers and avionics suppliers enable integrated environmental and flight control solutions, improving operational efficiency. Growing emphasis on passenger health and air quality post-pandemic encourages adoption of advanced filtration and humidity control technologies. These factors, combined with supportive government policies and investments in aerospace infrastructure, provide a fertile environment for ECS market expansion and technology diversification globally.

Market Challenges

Stringent regulatory compliance requirements across multiple jurisdictions impose significant technical and certification challenges for Aircraft Environmental Control Systems manufacturers, increasing development timelines and costs. High capital investment in R&D to develop lightweight, energy-efficient, and digitally integrated ECS products poses barriers for new entrants and smaller players. Supply chain disruptions and raw material price volatility impact production schedules and cost structures, complicating market stability. Integration complexities with evolving aircraft architectures and emerging propulsion technologies require continuous innovation and adaptation. Additionally, the COVID-19 pandemic's impact on global air travel temporarily reduced aircraft production and retrofit activities, affecting short-term ECS demand. Companies face pressure to balance performance, safety, and environmental sustainability while managing competitive pricing, making market penetration and profitability challenging in this evolving landscape.

Regulatory Framework

Recent regulations from 2020 to 2025 such as the International Civil Aviation Organization’s (ICAO) Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA) have mandated stringent emission reductions, impacting Aircraft Environmental Control Systems design to enhance fuel efficiency and reduce environmental footprints. The European Union’s Environmental Standards for Aviation released in 2021 require ECS manufacturers to comply with noise and emission limits, promoting development of quieter and cleaner systems. The Federal Aviation Administration (FAA) updated certification protocols for ECS components in 2023, emphasizing safety, reliability, and integration with next-gen aircraft systems. These regulations have enforced rigorous testing standards and documentation requirements, driving innovation and ensuring alignment with global environmental and safety objectives. Compliance with these evolving mandates remains a critical factor influencing ECS market strategies and technology roadmaps worldwide.

Market Intelligence

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

- •Source: Industry Reports, Official Company Releases, Aviation Regulatory Bodies

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 4.5 Billion |

| Forecast Year Market Size | USD 9.2 Billion |

| CAGR | 8.2% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 8% |

| Scope of Report | Market is segmented by Type (Air Cycle Machines, Water Separation Systems, Gas Turbine Engine, Air Conditioning Packs, Cabin Pressure Controllers), Application (Commercial Aircraft, Military Aircraft, Business Jets, Helicopters, Unmanned Aerial Vehicles), End-Use Industry (Commercial Aviation, Defense & Military, Business Aviation, Unmanned Aerial Systems), Distribution Channel (OEM, Aftermarket, Maintenance, Repair and Overhaul (MRO)) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Honeywell Aerospace (United States), Collins Aerospace (United States), Safran SA (France), Parker Hannifin Corporation (United States), Liebherr Aerospace (Germany), MTU Aero Engines (Germany), Eaton Corporation (United States), UTC Aerospace Systems (United States), B/E Aerospace (United States), GKN Aerospace (United Kingdom), Triumph Group, Inc. (United States), Moog Inc. (United States), Avio Aero (Italy), Meggitt PLC (United Kingdom), SAFRAN Electrical & Power (France), Thales Group (France), CIRCOR Aerospace (United States), General Electric Aviation (United States), Woodward, Inc. (United States), Kongsberg Defence & Aerospace (Norway) |

Global Aircraft Environmental Control Systems Market Size, Growth & Revenue 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.