Global Video Surveillance Systems Market Size, Growth & Revenue 2024-2034

Global Video Surveillance Systems Market is segmented by Product Type (IP Cameras, Analog Cameras, Thermal Cameras, PTZ Cameras (Pan-Tilt-Zoom), Network Video Recorders (NVRs)), Application (Residential, Commercial, Industrial, Public Safety, Transportation), End-Use Industry (Retail, Healthcare, Government & Defense, Manufacturing), Distribution Channel (Direct Sales, Distributors, Online Sales), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The Global Video Surveillance Systems Market is a dynamic and rapidly evolving sector that integrates cutting-edge video capture technologies, analytics software, and network infrastructure to provide comprehensive security and monitoring solutions worldwide. This market spans various product types including IP cameras, analog cameras, thermal imaging cameras, PTZ cameras, and network video recorders, catering to applications in residential, commercial, industrial, public safety, and transportation domains. Increasing urbanization, rising security threats, and the proliferation of smart city projects have broadened the market scope significantly. The market further encompasses services such as installation, system integration, and maintenance, supported by advancements in AI-driven analytics and cloud computing to enhance real-time surveillance and threat detection capabilities. Regulatory compliance and data privacy laws are shaping product innovation and deployment strategies. The market’s growth is fueled by technological advances, heightened demand for automation in security, and rising investment from governments and private sectors globally. These factors collectively drive substantial market expansion, making video surveillance systems an integral part of modern security infrastructure.

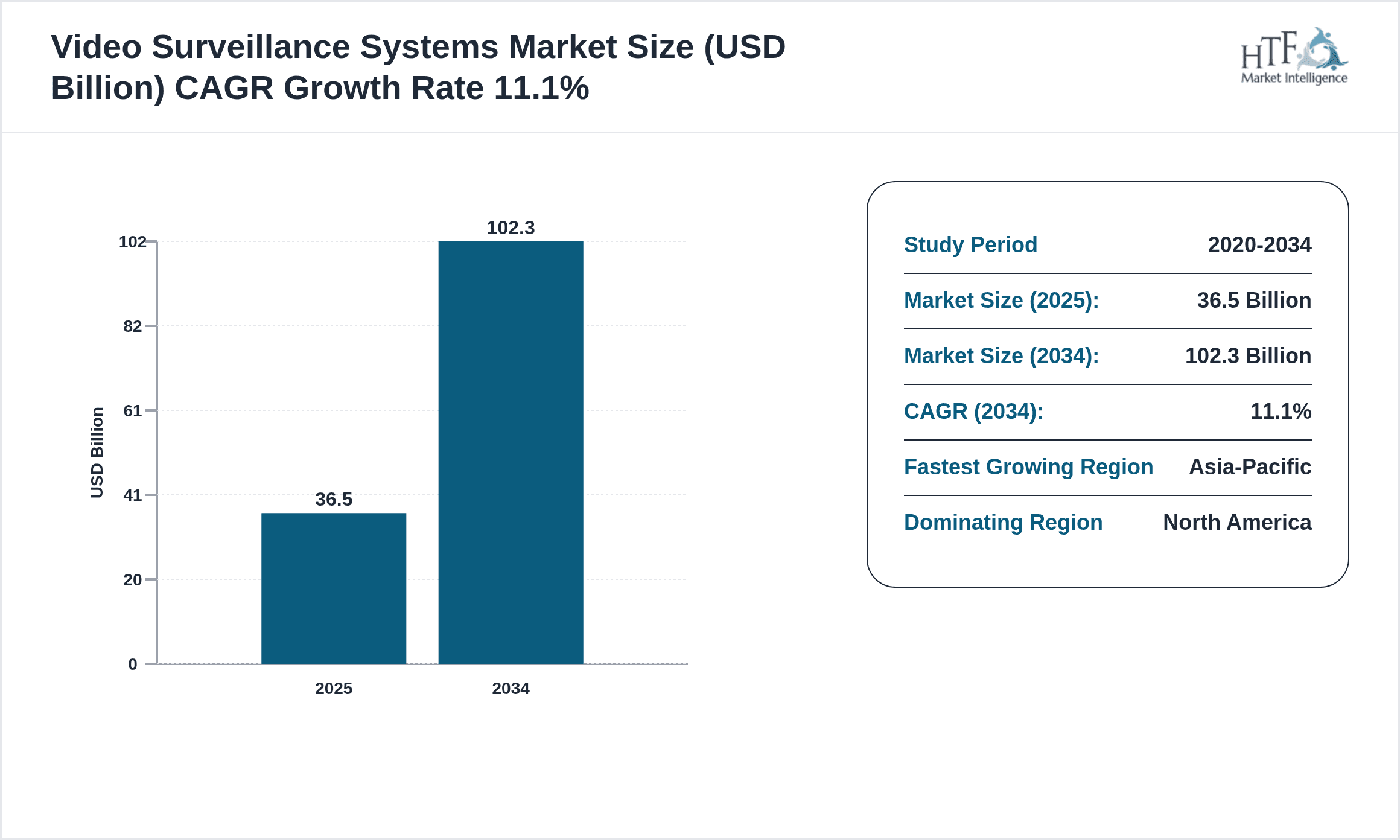

- •The Global Video Surveillance Systems Market was valued at USD 36.5 Billion in 2024 and is projected to reach USD 102.3 Billion by 2034, exhibiting a robust CAGR of 11.1% during the forecast period. Key highlights include the dominance of IP camera technology, which accounts for the largest market share, and the rapid adoption of thermal cameras driven by their effectiveness in varied environmental conditions. North America leads the market in revenue contribution, while Asia-Pacific is expected to witness the fastest growth due to increasing urbanization and infrastructure development. Emerging trends such as AI-powered video analytics, integration with IoT devices, and cloud-based surveillance solutions are reshaping market dynamics. Additionally, regulatory frameworks enforcing stringent security standards are accelerating adoption across multiple sectors. The competitive landscape is marked by continuous innovation, strategic partnerships, and mergers & acquisitions, further propelling market growth and diversification.

- •The Global Video Surveillance Systems Market holds strategic importance across diverse industries including retail, transportation, government, and manufacturing, enabling enhanced security management, operational efficiency, and risk mitigation. Its value proposition lies in offering scalable, reliable, and intelligent surveillance solutions that not only deter criminal activities but also facilitate compliance with regulatory mandates and support smart city initiatives. Stakeholders including system integrators, technology providers, and end-users benefit from continuous technological innovation, enabling real-time analytics, remote monitoring, and seamless integration with existing infrastructure. The market’s evolution supports sustainability by optimizing resource allocation and promoting safer environments. Consequently, investment in video surveillance technologies is pivotal for organizations aiming to safeguard assets, improve public safety, and leverage data-driven insights for strategic decision-making in a digitally connected world.

Competitive Landscape

The competitive environment in the Global Video Surveillance Systems Market is characterized by intense rivalry among established multinational corporations and emerging regional players, all striving to innovate and expand their market share. Market leaders leverage advanced technologies such as AI-driven analytics, cloud computing, and edge processing to differentiate their offerings and meet evolving customer demands. Strategic partnerships, acquisitions, and collaborations are common approaches to enhance product portfolios and geographic reach, while pricing strategies are calibrated to balance profitability with competitive positioning. Companies invest heavily in R&D to develop integrated solutions that offer scalability, cybersecurity features, and interoperability with IoT ecosystems. Distribution channels and after-sales services play critical roles in customer retention and brand loyalty. Barriers to entry exist due to high capital requirements and regulatory compliance complexities, fostering a competitive advantage for established players. Future trends indicate a shift toward software-centric solutions and platform-based models, intensifying competition and innovation pace globally.

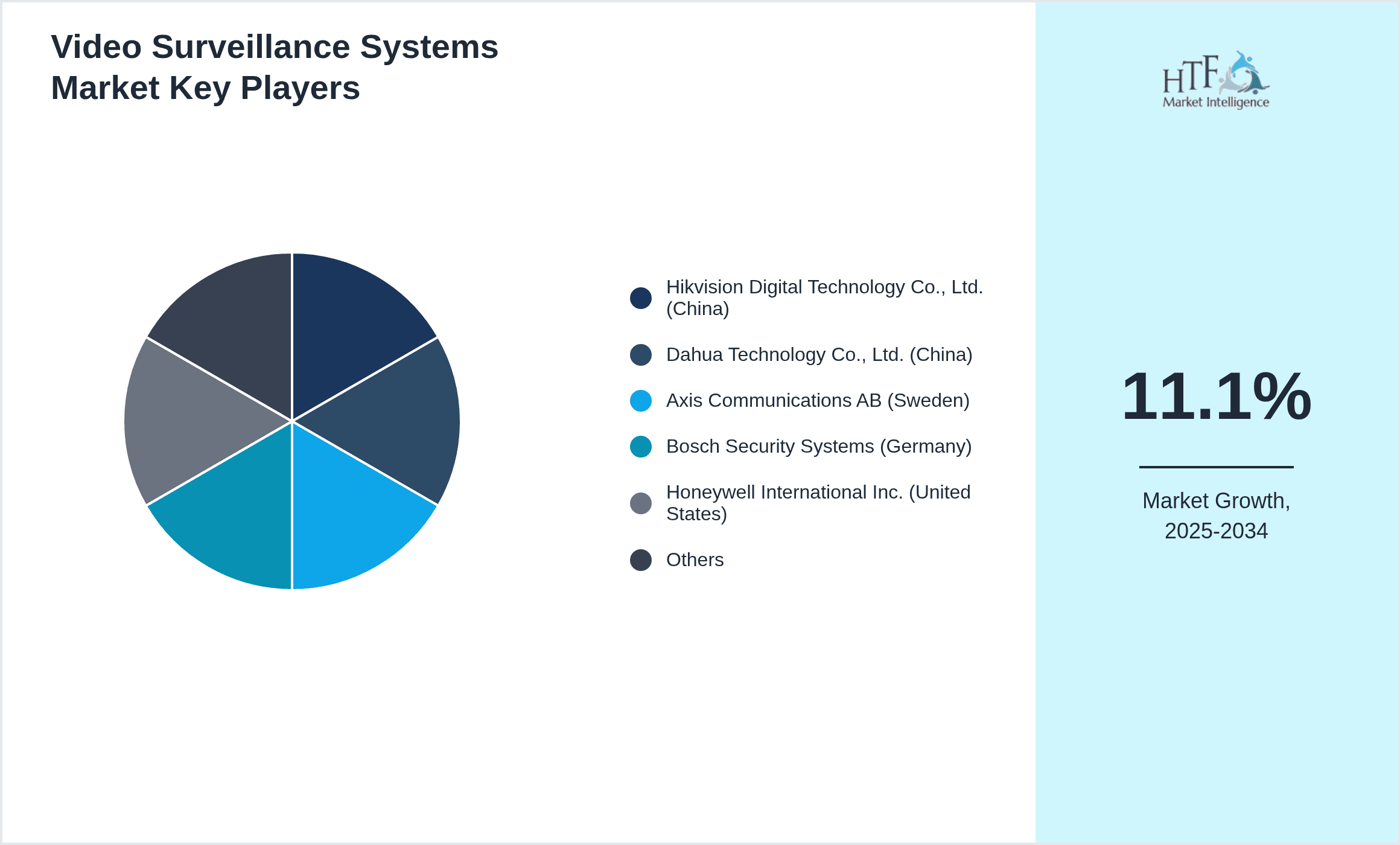

Leading Companies in Video Surveillance Systems Market

- •Hikvision Digital Technology Co., Ltd. (China)

- •Dahua Technology Co., Ltd. (China)

- •Axis Communications AB (Sweden)

- •Bosch Security Systems (Germany)

- •Honeywell International Inc. (United States)

- •Hanwha Techwin Co., Ltd. (South Korea)

- •FLIR Systems, Inc. (United States)

- •Pelco, Inc. (United States)

- •Avigilon Corporation (Canada)

- •Samsung Techwin Co., Ltd. (South Korea)

- •Canon Inc. (Japan)

- •Panasonic Corporation (Japan)

- •Tyco International plc (Ireland)

- •VIVOTEK Inc. (Taiwan)

- •Zhejiang Uniview Technologies Co., Ltd. (China)

- •Mobotix AG (Germany)

- •Pelco by Schneider Electric (United States)

- •IDIS Co., Ltd. (South Korea)

- •Milestone Systems A/S (Denmark)

- •Axis Communications (Sweden)

- •Vicon Industries, Inc. (United States)

- •Digital Watchdog (United States)

- •Bosch Sicherheitssysteme GmbH (Germany)

- •Honeywell Security Group (United States)

- •Avigilon Corporation (Canada)

Market Breakdown

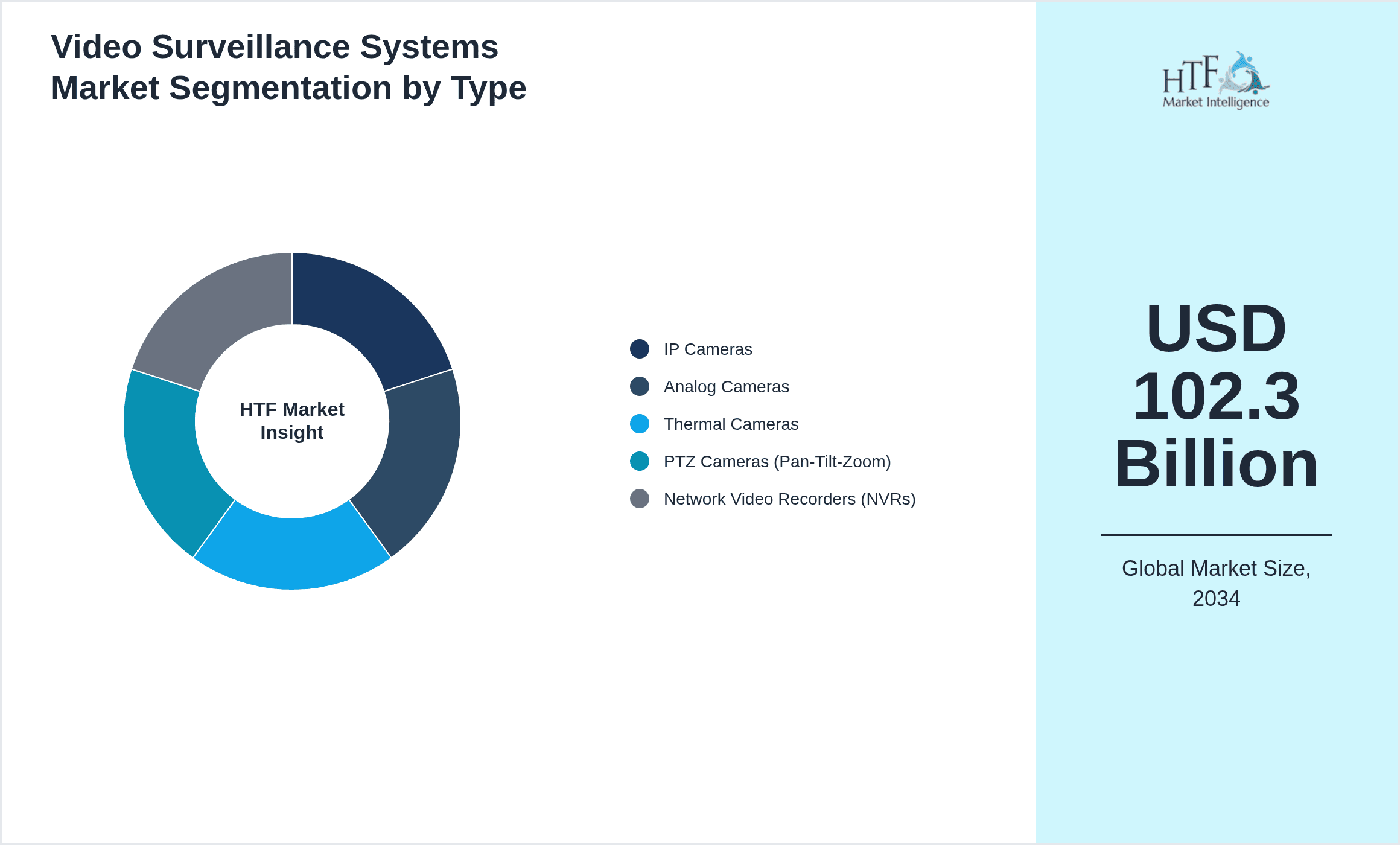

- •By Product Type

- ◦IP Cameras

- ◦Analog Cameras

- ◦Thermal Cameras

- ◦PTZ Cameras (Pan-Tilt-Zoom)

- ◦Network Video Recorders (NVRs)

- •By Application

- ◦Residential

- ◦Commercial

- ◦Industrial

- ◦Public Safety

- ◦Transportation

- •By End-Use Industry

- ◦Retail

- ◦Healthcare

- ◦Government & Defense

- ◦Manufacturing

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors

- ◦Online Sales

Growth Dynamics

The Global Video Surveillance Systems Market is driven by rising concerns over security and safety in public and private sectors, leading to increased demand for sophisticated monitoring solutions. Technological advancements such as AI-enabled video analytics and cloud integration are enabling real-time threat detection and remote monitoring, enhancing system efficiency and scalability. Growing investments in smart city projects and infrastructure development across emerging economies are further accelerating market growth. Additionally, stringent government regulations mandating surveillance for public safety and crime prevention are propelling adoption across various industries. The integration of IoT devices with video surveillance systems is fostering smarter, interconnected security ecosystems. Increasing awareness about asset protection and demand for automated security solutions in commercial and residential applications also contribute significantly to market expansion. Together, these factors are transforming traditional surveillance into intelligent, data-driven systems, driving sustained growth globally.

Market Trends

The video surveillance market is witnessing a significant shift towards IP-based camera systems due to their superior image quality, scalability, and integration capabilities with network infrastructure. AI and machine learning technologies are being increasingly embedded within surveillance software to enable facial recognition, behavior analysis, and anomaly detection, thereby enhancing proactive security measures. Cloud-based storage solutions are gaining traction for their flexibility and cost-effectiveness, allowing remote access and scalability. Furthermore, thermal imaging cameras are experiencing rising adoption in critical infrastructure and industrial applications for their ability to perform in low-visibility conditions. Sustainability trends are also influencing product development, with manufacturers focusing on energy-efficient devices. The convergence of video surveillance with analytics and IoT platforms is fostering the creation of smart surveillance ecosystems tailored for diverse industry needs, marking a paradigm shift in security technology.

Market Opportunities

Emerging economies present vast opportunities for video surveillance market expansion due to rapid urbanization, increasing crime rates, and growing governmental focus on public safety infrastructure. The integration of AI and deep learning in video analytics opens avenues for innovative applications such as crowd management, traffic control, and predictive security, creating new market segments. Expansion into untapped sectors like agriculture and energy facilities offers growth potential for customized surveillance solutions. The rising adoption of cloud-based and mobile surveillance platforms provides opportunities for service providers to offer subscription-based models, enhancing revenue streams. Additionally, strategic collaborations between technology vendors and system integrators can facilitate market penetration and solution diversification. The increasing need for cybersecurity in surveillance systems also fosters innovation in secure video transmission and storage technologies, representing a significant growth frontier.

Market Challenges

Despite robust growth, the video surveillance systems market faces challenges such as concerns over data privacy and the ethical use of surveillance technologies, leading to regulatory complexities and potential adoption hesitations. High initial capital expenditure for advanced IP-based systems and integration costs hinder small and medium enterprises from widespread deployment. Technical limitations such as bandwidth constraints, interoperability issues among heterogeneous devices, and cybersecurity vulnerabilities pose operational risks. Additionally, the need for continuous software updates and skilled workforce to manage sophisticated systems can escalate maintenance costs. Market fragmentation with multiple regional standards and the presence of low-cost counterfeit products also affect market stability and customer trust. Addressing these challenges requires harmonized regulations, enhanced data protection mechanisms, and investment in user education and system robustness.

Regulatory Framework

Between 2019 and 2024, several key regulatory measures have shaped the Global Video Surveillance Systems Market, focusing on data protection, privacy, and operational standards. The General Data Protection Regulation (GDPR) enacted in the European Union mandates strict controls on video data collection, storage, and sharing, influencing product design and deployment globally. Similarly, the U.S. has implemented state-level regulations requiring transparency and limitations on surveillance in public spaces. International standards such as ISO/IEC 27001 for information security management are increasingly adopted by vendors to ensure cybersecurity compliance. Additionally, government mandates in various regions have accelerated the integration of video surveillance in public safety and critical infrastructure projects, requiring adherence to technical and ethical guidelines. These frameworks have compelled manufacturers and service providers to enhance data encryption, implement privacy-by-design principles, and ensure lawful use of surveillance technologies, fostering trust and compliance across markets.

Market Intelligence

- •15th January 2025, Hikvision Digital Technology Co., Ltd. launched its next-generation AI-enabled thermal and IP camera lineup designed for enhanced perimeter security and low-light environments. The new products feature integrated deep learning algorithms for advanced facial and behavior recognition, aimed at high-security zones and smart city projects. This launch underscores the company’s commitment to innovation and expanding its footprint in emerging markets, leveraging cloud-based analytics and edge computing to deliver real-time actionable insights. The product suite enhances scalability and cybersecurity features, addressing growing concerns over data protection. This initiative positions Hikvision to capitalize on rising demand for intelligent surveillance solutions globally. Source: Official Hikvision Press Release

- •22nd March 2025, Axis Communications AB announced a strategic partnership with a leading cloud services provider to offer integrated cloud-based video management solutions tailored for commercial and public safety sectors. The collaboration focuses on delivering scalable, subscription-based surveillance services with enhanced data encryption and remote accessibility. This move aims to address evolving customer preferences for flexible deployment models and reduced upfront investments. The partnership also includes joint research on AI-driven analytics to improve threat detection accuracy and operational efficiency. This strategic initiative bolsters Axis Communications’ market position in the cloud surveillance domain and expands its global service ecosystem. Source: Axis Communications Official Website

- •30th April 2025, FLIR Systems, Inc. completed the acquisition of a cybersecurity firm specializing in securing IoT devices used in surveillance networks. This acquisition enhances FLIR’s portfolio by integrating advanced cybersecurity solutions to protect video data transmission and storage against emerging cyber threats. The combined expertise aims to address vulnerabilities in connected surveillance devices, promoting safer and more resilient security infrastructures. This strategic move reflects FLIR’s focus on holistic security solutions that combine physical and cybersecurity, responding to increasing market demands for comprehensive protection in video surveillance systems. The acquisition is expected to accelerate innovation and open new market opportunities in secure surveillance solutions. Source: FLIR Systems Press Release

- •10th February 2025, Avigilon Corporation announced the launch of an AI-powered video analytics platform designed to integrate seamlessly with existing surveillance systems across retail and transportation sectors. The platform offers real-time object detection, crowd analytics, and anomaly alerts, significantly enhancing situational awareness and operational efficiency. The company emphasized data privacy compliance and user-friendly interfaces to facilitate broad adoption. This launch marks a significant step in democratizing advanced analytics capabilities, enabling businesses to leverage intelligent insights without extensive infrastructure overhaul. The platform supports cloud and edge deployment, catering to diverse customer needs globally. Source: Avigilon Official Announcement

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 36.5 Billion |

| Forecast Year Market Size | USD 102.3 Billion |

| CAGR | 11.1% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 11% |

| Scope of Report | Market is segmented by Product Type (IP Cameras, Analog Cameras, Thermal Cameras, PTZ Cameras (Pan-Tilt-Zoom), Network Video Recorders (NVRs)), Application (Residential, Commercial, Industrial, Public Safety, Transportation), End-Use Industry (Retail, Healthcare, Government & Defense, Manufacturing), Distribution Channel (Direct Sales, Distributors, Online Sales) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Hikvision Digital Technology Co., Ltd. (China), Dahua Technology Co., Ltd. (China), Axis Communications AB (Sweden), Bosch Security Systems (Germany), Honeywell International Inc. (United States) |

Global Video Surveillance Systems Market Size, Growth & Revenue 2024-2034 - Table of Contents

Research enthusiast focused on transforming data uncovering into actionable insights through data-driven decision-making.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.