Global Vegetable Cutters and Dicers Market Size, Growth & Revenue 2024-2034

Global Vegetable Cutters and Dicers Market is segmented by Product Type (Manual Vegetable Cutters, Electric Vegetable Cutters, Automatic Vegetable Dicers, Handheld Vegetable Choppers, Industrial Vegetable Dicers), Application (Commercial Kitchens, Food Processing Plants, Household Use, Hospitality Sector, Retail Food Outlets), End-Use Industry (Foodservice Industry, Processed Food Industry, Hospitality Industry, Retail and Supermarkets), Distribution Channel (Direct Sales, Specialized Dealers, Online Retail), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global Vegetable Cutters and Dicers market is a vital segment of the food preparation and processing equipment industry, offering a spectrum of products designed to enhance efficiency, safety, and precision in vegetable processing. This market includes manual, electric, automatic, handheld, and industrial vegetable cutters and dicers, catering to applications ranging from household kitchens to large-scale commercial food processing plants. With increasing demand for convenience, faster food preparation, and consistent quality, manufacturers are innovating with advanced technologies such as programmable automatic dicers and multifunctional devices. The market's scope extends globally, driven by rising foodservice establishments, expanding processed food industries, and growing household adoption of kitchen automation tools. The industry also emphasizes ergonomic design, hygiene compliance, and energy efficiency, supporting diverse end-user requirements. Competitive dynamics involve established multinational corporations and emerging regional players focusing on product differentiation and strategic partnerships. Key use cases include commercial kitchens, hospitality sectors, retail food outlets, and food processing facilities, underscoring the market's wide-ranging impact on global food industry productivity and quality assurance.

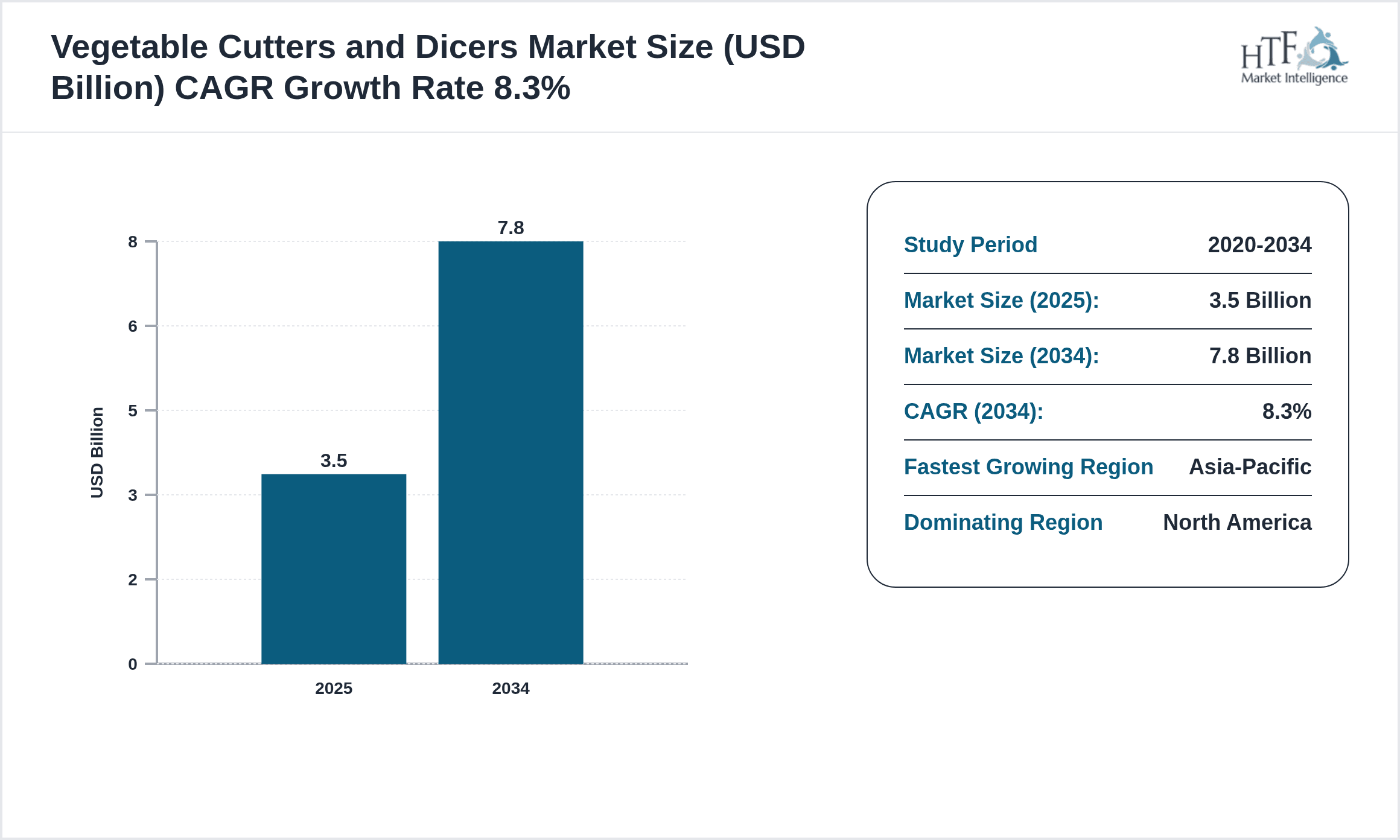

- •Significant market highlights include a base valuation of USD 3.5 billion in 2024, with projections estimating growth to USD 7.8 billion by 2034 at a CAGR of 8.3%. The electric vegetable cutters dominate the product segment due to their balance of efficiency and affordability, while automatic vegetable dicers exhibit the fastest growth owing to automation trends in food processing. North America leads the regional market, attributed to advanced foodservice infrastructures and high adoption rates of kitchen automation. Asia-Pacific is identified as the fastest-growing region, driven by expanding commercial food sectors and increasing urbanization. Key drivers include rising demand for processed foods, labor cost optimization, and technological advancements. Challenges such as high equipment costs and regulatory compliance complexities persist. Opportunities lie in emerging markets, product innovation, and expanding distribution networks.

- •The Vegetable Cutters and Dicers market holds strategic importance for the food industry by enabling faster preparation times, enhanced consistency, and reduced labor costs. Stakeholders including equipment manufacturers, distributors, food processors, and commercial kitchen operators benefit from ongoing innovations and expanding market reach. The market's growth supports food safety initiatives, waste reduction, and operational efficiency, aligning with evolving consumer preferences for convenience and quality. As global food demand rises, the market's role in supporting scalable and hygienic vegetable processing is increasingly critical. Strategic investments in technology integration, regional expansion, and customer-centric product development will shape future market trajectories and competitive positioning.

Competitive Landscape

The competitive environment within the global Vegetable Cutters and Dicers market is characterized by intense rivalry among key manufacturers focusing on innovation, product differentiation, and global distribution. Market leaders invest heavily in R&D to develop advanced features such as automation, safety enhancements, and multifunctionality that cater to diverse customer segments from household users to industrial processors. Strategic partnerships and collaborations are common to expand market reach and integrate complementary technologies. Pricing strategies vary by region and product sophistication, with premium electric and automatic dicers commanding higher margins while manual cutters compete on affordability. Barriers to entry include the need for technological expertise, compliance with food safety regulations, and establishing robust distribution networks. Regional competition is influenced by varying consumer preferences and economic factors, prompting companies to tailor offerings accordingly. The future competitive landscape is expected to be shaped by digitalization, sustainability initiatives, and increased focus on smart kitchen solutions, driving continuous evolution in market positioning and customer engagement.

Companies Shaping the Vegetable Cutters and Dicers Market

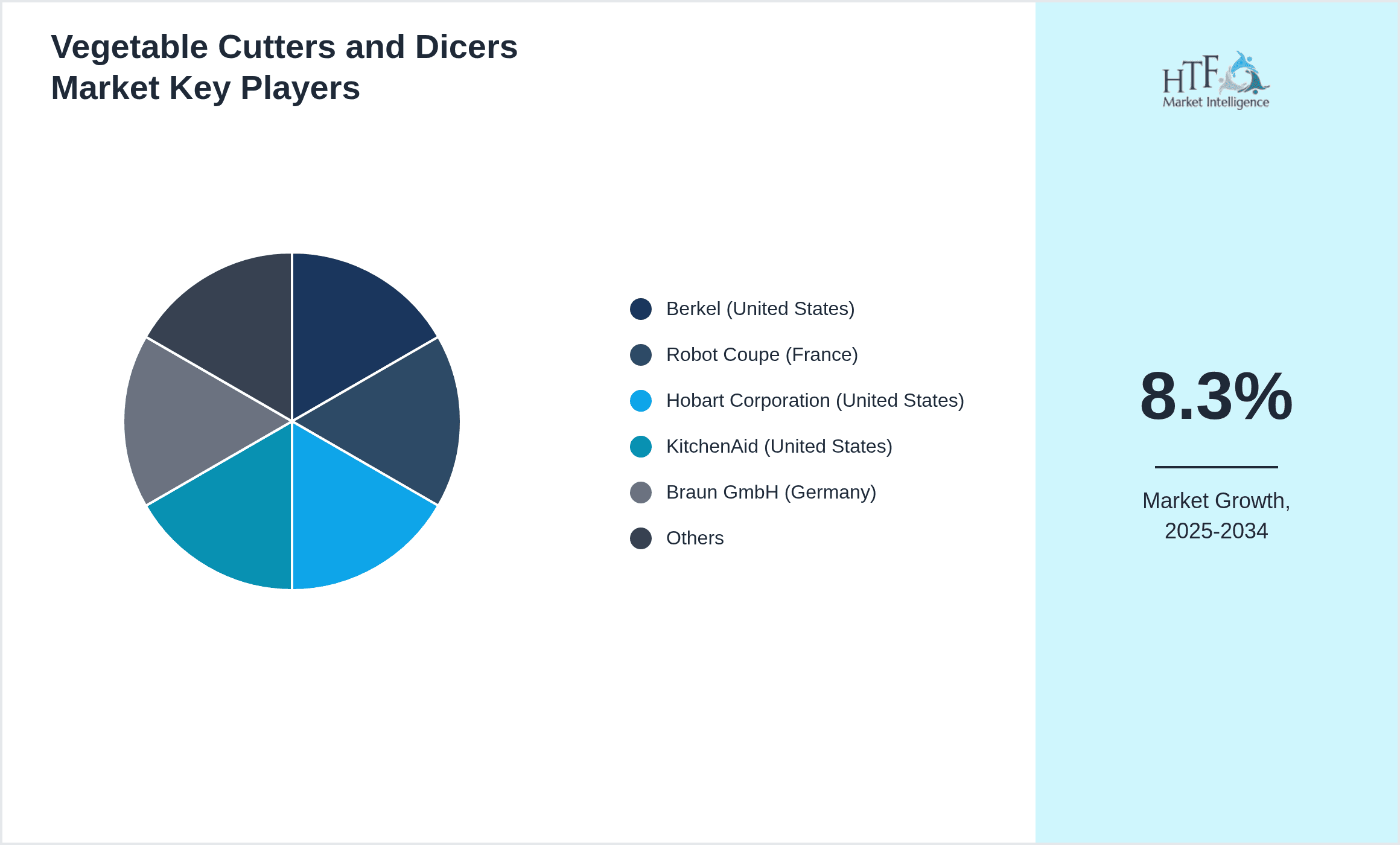

- •Berkel (United States)

- •Robot Coupe (France)

- •Hobart Corporation (United States)

- •KitchenAid (United States)

- •Braun GmbH (Germany)

- •Moulinex (France)

- •Cuisinart (United States)

- •Hamilton Beach Brands Holding Company (United States)

- •Waring Commercial (United States)

- •Weston Brands (United States)

- •Vitamix (United States)

- •Sammic (Spain)

- •Dito Sama (Belgium)

- •Bamix (Switzerland)

- •Chef'sChoice (United States)

- •Kitchenaid (United States)

- •Jaccard (Switzerland)

- •Arnica (Turkey)

- •Bosch (Germany)

- •Philips (Netherlands)

- •Morphy Richards (United Kingdom)

- •Tefal (France)

- •DeLonghi (Italy)

- •Sunbeam Products (Australia)

- •Electrolux (Sweden)

Market Breakdown

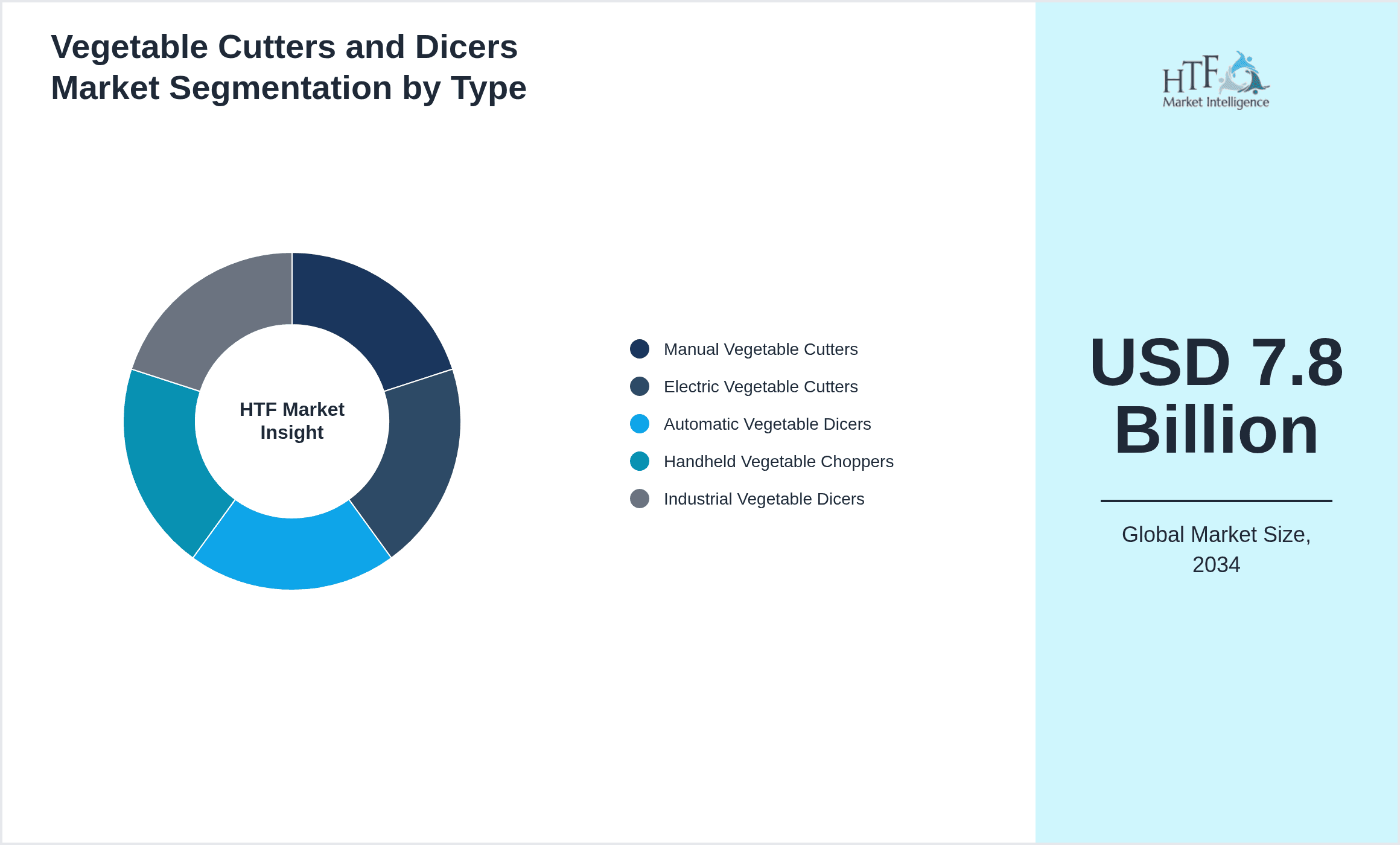

- •By Product Type

- ◦Manual Vegetable Cutters

- ◦Electric Vegetable Cutters

- ◦Automatic Vegetable Dicers

- ◦Handheld Vegetable Choppers

- ◦Industrial Vegetable Dicers

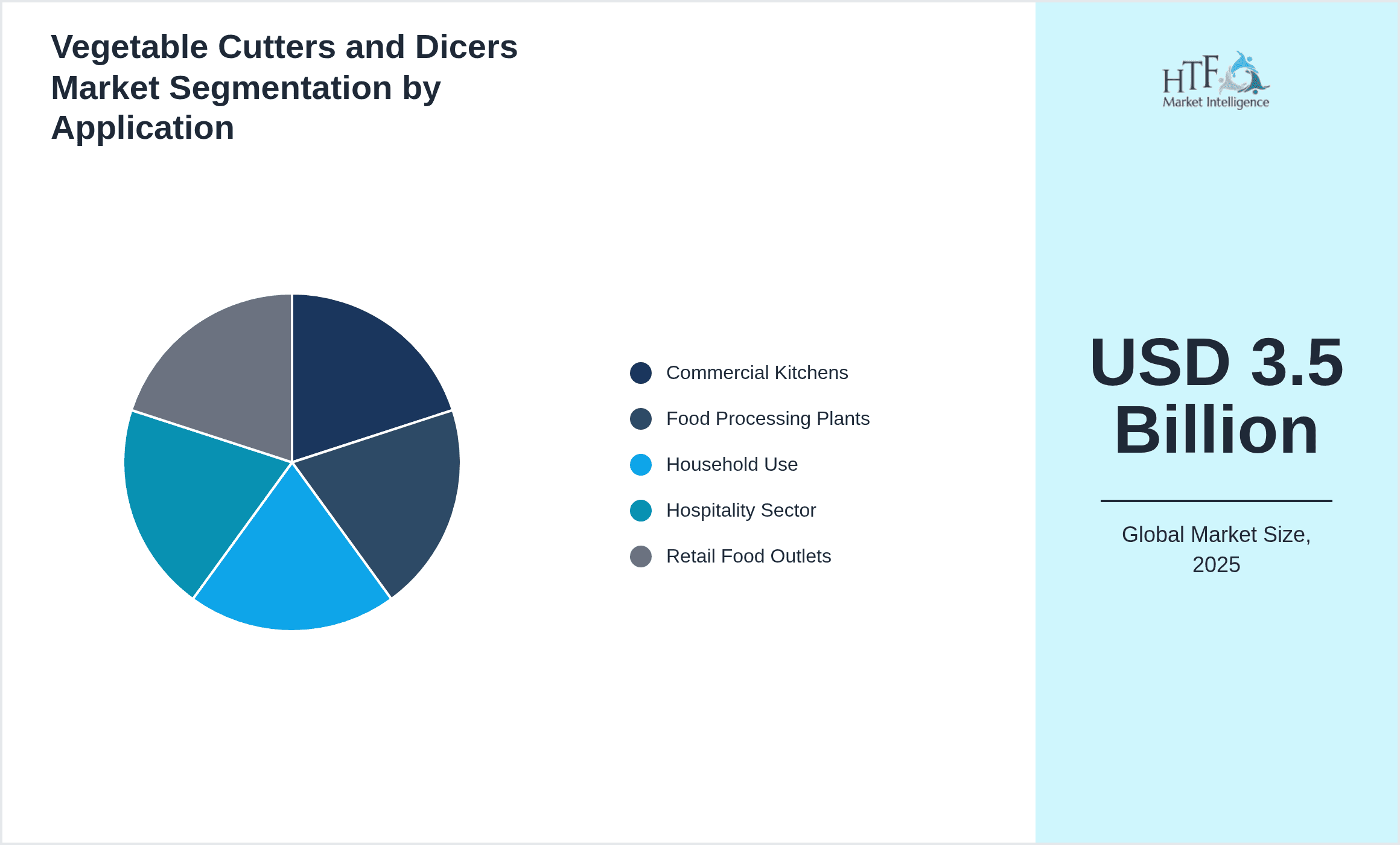

- •By Application

- ◦Commercial Kitchens

- ◦Food Processing Plants

- ◦Household Use

- ◦Hospitality Sector

- ◦Retail Food Outlets

- •By End-Use Industry

- ◦Foodservice Industry

- ◦Processed Food Industry

- ◦Hospitality Industry

- ◦Retail and Supermarkets

- •By Distribution Channel

- ◦Direct Sales

- ◦Specialized Dealers

- ◦Online Retail

Growth Dynamics

- •The global Vegetable Cutters and Dicers market is primarily propelled by the rising demand for processed and convenience foods, driving the need for efficient kitchen equipment in commercial and household settings. Increasing urbanization and changing lifestyles have intensified the adoption of electric and automatic cutting devices that reduce preparation time and ensure uniformity in food products. Innovations in automation and multifunctionality further stimulate market growth by catering to diverse operational requirements across foodservice and industrial sectors. Moreover, labor cost optimization, particularly in commercial kitchens and food processing plants, incentivizes investment in advanced cutting technologies. Government initiatives promoting food safety and hygiene standards also encourage the deployment of equipment that minimizes manual handling. These factors collectively foster robust market expansion globally, with the Asia-Pacific region experiencing accelerated growth due to expanding foodservice industries and rising disposable incomes.

- •An increasing trend toward kitchen automation and smart appliances is reshaping the Vegetable Cutters and Dicers market globally. Manufacturers are integrating IoT and programmable features to deliver precision cutting, safety, and operational convenience. The growing influence of social media and cooking shows has also heightened consumer interest in innovative kitchen tools. Furthermore, sustainability concerns have prompted the development of energy-efficient and durable products, aligning with eco-conscious consumer preferences. The rise of online retail platforms has expanded market access, facilitating global distribution and customer engagement. Collaborative efforts between manufacturers and foodservice providers to customize solutions for specific applications represent another key trend. Collectively, these trends contribute to evolving customer expectations and competitive differentiation within the market.

- •Despite positive growth outlooks, the market faces several restraints that may impede rapid expansion. High initial investment costs for advanced automatic dicers and electric cutters can deter small and medium enterprises and price-sensitive consumers. Regulatory compliance related to food safety, electrical standards, and durability adds complexity and cost to product development and market entry. Additionally, the availability of low-cost manual cutters and traditional preparation methods in certain regions limits the penetration of high-end equipment. Supply chain disruptions and raw material price volatility may also affect production costs and delivery timelines. Moreover, a lack of consumer awareness about the benefits of modern vegetable cutting equipment in emerging markets poses a challenge to widespread adoption.

- •The global Vegetable Cutters and Dicers market presents extensive opportunities for product innovation, regional expansion, and strategic collaborations. Emerging economies with growing foodservice and processed food sectors offer untapped potential for market penetration. Developing multifunctional, compact, and user-friendly devices tailored for household consumers can capture new segments. Integration of digital technologies such as IoT-enabled smart cutters enhances product differentiation and customer value. Partnerships with food processing companies and hospitality chains can facilitate customized solutions and bulk sales. Additionally, expanding e-commerce channels provides direct access to a broader customer base. Investment in sustainability-driven product designs, including energy-efficient motors and recyclable materials, aligns with global environmental priorities and consumer preferences, creating further growth avenues.

- •Key challenges confronting the Vegetable Cutters and Dicers market include intense price competition, rapid technological changes, and stringent regulatory landscapes. Manufacturers must continuously innovate to maintain competitive advantage, balancing cost and feature enhancements. Ensuring compliance with diverse international standards related to food safety, electrical certification, and environmental regulations requires significant resource allocation. Market fragmentation with numerous regional players complicates global brand recognition and distribution. Furthermore, educating consumers and commercial buyers about advanced product benefits remains a hurdle, particularly in developing regions reliant on traditional methods. Supply chain disruptions and fluctuating raw material costs add operational risks. Addressing these challenges demands strategic investments in R&D, marketing, and regulatory expertise to sustain growth and market relevance.

Market Trends

- •A prominent trend in the Vegetable Cutters and Dicers market is the increasing incorporation of automation and digital controls, enabling precise, consistent cutting with reduced manual intervention. This shift enhances productivity in commercial kitchens and food processing plants, driving demand for sophisticated automatic dicers. Additionally, manufacturers are focusing on compact, multifunctional devices catering to space-constrained households, reflecting consumer preferences for convenience and versatility. Sustainability considerations are influencing product design, favoring energy-efficient motors and recyclable materials. The growth of online retail platforms facilitates direct consumer engagement and customized offerings. These developments collectively influence purchasing decisions and competitive strategies across regions.

- •Innovation in smart kitchen appliances is transforming the Vegetable Cutters and Dicers landscape, with companies integrating IoT capabilities for remote operation and maintenance alerts. This advancement supports user convenience and proactive equipment management, reducing downtime. The rise of health-conscious consumers drives demand for devices that enable quick preparation of fresh vegetables, encouraging innovations in safety features and hygiene compliance. Collaborative product development between manufacturers and commercial foodservice operators is enhancing application-specific solutions. Furthermore, the COVID-19 pandemic accelerated interest in contactless and easy-to-clean equipment, shaping design priorities and consumer expectations.

- •Strategic partnerships and acquisitions have become common to expand product portfolios and geographic reach. Companies are leveraging collaborations to integrate complementary technologies and enhance market penetration. For instance, alliances between kitchen appliance manufacturers and technology firms facilitate the adoption of automation and smart features. Market players are also investing in local manufacturing facilities to reduce costs and improve supply chain resilience. Such strategies contribute to competitive differentiation and responsiveness to regional market demands, reinforcing leadership positions in key geographies.

- •Digitalization and e-commerce growth are reshaping distribution channels for vegetable cutters and dicers globally. Online platforms enable manufacturers to reach diverse customer segments directly, offering customization options and competitive pricing. This trend also empowers consumers with detailed product information and peer reviews, influencing buying behavior. Companies are enhancing digital marketing efforts and after-sales support services to build brand loyalty and customer engagement. The omnichannel approach combining traditional dealers with online sales optimizes market coverage and responsiveness to emerging consumer trends.

- •Sustainability is gaining traction as a critical trend, with manufacturers focusing on eco-friendly materials, energy-efficient designs, and reduced waste production during manufacturing. Consumers increasingly prefer products aligned with environmental values, prompting companies to obtain certifications and adopt green manufacturing processes. This trend is expected to influence regulatory policies and purchasing decisions, fostering long-term market transformation towards sustainable kitchen equipment solutions.

Market Opportunities

- •The burgeoning processed food industry in emerging economies offers significant growth opportunities for vegetable cutters and dicers, with increased demand for industrial-grade and semi-automatic equipment. Expanding urban populations and rising disposable incomes fuel the need for efficient food preparation solutions in both commercial and household contexts. Market entrants can capitalize on this by tailoring products to local preferences and price sensitivities. Additionally, investing in R&D to develop compact, multifunctional devices for small kitchens can address unmet consumer needs. The growing online retail penetration provides a scalable channel for market expansion and customer engagement, facilitating direct-to-consumer sales and customized offerings. Strategic partnerships with foodservice operators and retail chains can unlock bulk procurement opportunities, further boosting market reach.

- •Technological advancements present opportunities to innovate with smart, IoT-enabled vegetable cutters and dicers that offer remote monitoring, predictive maintenance, and usage analytics. Such features enhance operational efficiency, particularly for large-scale food processing plants and commercial kitchens, supporting premium pricing and brand differentiation. Sustainability-driven product development focusing on energy efficiency and recyclable materials aligns with increasing regulatory pressures and consumer preferences. Geographic expansion into untapped regions with growing foodservice sectors, such as Latin America and Middle East & Africa, can diversify revenue streams and mitigate regional risks. Furthermore, developing modular designs that allow easy upgrades and repairs can improve product lifecycle value and customer satisfaction.

- •Collaborations with culinary institutes, food processors, and hospitality chains for co-developing specialized cutting solutions offer opportunities to address specific operational challenges. Customizing equipment for ethnic cuisines and regional food preparation techniques can enhance product relevance and adoption. Leveraging digital marketing and e-commerce platforms to educate consumers about product benefits and usage techniques can accelerate market penetration, especially in household segments. Additionally, expanding after-sales services including maintenance, training, and warranty programs can create competitive advantages and recurring revenue streams. These strategic initiatives collectively underpin sustained growth and market leadership.

- •Government initiatives promoting food safety, hygiene, and mechanization in food processing sectors provide a supportive framework for market growth. Incentives and subsidies for modern kitchen equipment adoption encourage investments by commercial establishments and food processors. Aligning product development with regulatory standards and certifications can facilitate market access and customer trust. Educational campaigns highlighting benefits of mechanized vegetable cutting in reducing contamination and labor dependency can further stimulate demand. Such policy-driven opportunities enable manufacturers to expand customer base and reinforce compliance-driven product differentiation.

- •The rising trend of home cooking and meal prepping, exacerbated by recent global events, creates a lucrative opportunity for manufacturers to innovate user-friendly, safe, and multifunctional vegetable cutters targeting household consumers. Incorporating ergonomic designs and easy-clean features addresses consumer convenience and safety concerns. Subscription-based models for replacement blades and accessories can establish continuous revenue streams. Collaborations with recipe platforms and culinary content creators can enhance brand visibility and customer engagement. Capitalizing on these lifestyle shifts through targeted marketing and product development strategies can significantly expand market share in the consumer segment.

Market Challenges

- •High initial costs of advanced vegetable cutters and dicers, especially automatic and industrial-grade models, represent a significant barrier to adoption among small and medium enterprises and price-sensitive consumers. This limits market penetration in developing regions where traditional manual methods are prevalent. Manufacturers face the challenge of balancing technological sophistication with affordability to broaden appeal. Additionally, the fragmented nature of the market with numerous regional players complicates brand recognition and distribution efficiencies. The complexity of complying with diverse international regulatory standards related to food safety, electrical safety, and environmental impact imposes additional operational burdens. These factors collectively constrain rapid market expansion and necessitate strategic approaches to product positioning and market entry.

- •Supply chain disruptions, including shortages of raw materials and logistical challenges, have impacted production schedules and cost structures in recent years. Volatility in the prices of metals, plastics, and electronic components affects profitability and pricing strategies. Manufacturers must invest in supply chain resilience and alternative sourcing to mitigate risks. Furthermore, educating consumers and commercial buyers on the benefits of mechanized vegetable cutting equipment remains a challenge, particularly in regions with strong cultural preferences for manual food preparation. Addressing these issues requires targeted marketing, training programs, and after-sales support to build trust and awareness.

- •Competition from low-cost, unbranded manual cutters and counterfeit products undermines market value and consumer confidence. Ensuring product quality and authenticity is critical but difficult to enforce globally. Additionally, rapid technological advancements require continuous R&D investments, which may strain smaller manufacturers. The need for skilled technicians and maintenance infrastructure to support advanced equipment, especially in emerging markets, poses operational challenges. Environmental regulations demanding reduction in energy consumption and waste generation necessitate redesigns and compliance costs. Navigating these multifaceted challenges is essential for sustained competitiveness and market growth.

- •Market saturation in developed regions, where penetration of electric and automatic vegetable cutters is already high, limits growth potential. Companies must innovate to create differentiation through features, design, and customer experience to retain market share. The evolving consumer preference towards multifunctional kitchen appliances intensifies competition from broader kitchen equipment categories, requiring strategic portfolio management. Furthermore, integration with smart home ecosystems introduces compatibility and cybersecurity considerations. Adapting to these dynamic market conditions demands agility and forward-looking strategies.

- •The COVID-19 pandemic highlighted vulnerabilities in supply chains and shifted consumer behavior unpredictably. While accelerating interest in home cooking, it also disrupted commercial foodservice demand temporarily. Recovery trajectories vary across regions, affecting market forecasts and investment decisions. Manufacturers must remain adaptable to fluctuating demand patterns, regulatory changes, and health safety requirements. Balancing short-term operational challenges with long-term growth strategies is a persistent challenge in the evolving global landscape.

Regulatory Framework

- •Between 2020 and 2024, several key regulations impacted the global Vegetable Cutters and Dicers market. The implementation of updated food safety standards such as ISO 22000 and HACCP protocols mandated stricter hygiene and material compliance for cutting equipment, requiring manufacturers to enhance product designs and materials. Electrical safety regulations including IEC 60335 standards were revised to ensure user safety in kitchen appliances, influencing certification procedures globally. The European Union introduced the EcoDesign Directive updates promoting energy efficiency and recyclability for electrical devices, affecting product development cycles. In the United States, FDA guidelines emphasized contamination prevention in food processing equipment, driving innovation in easy-to-clean surfaces and antimicrobial materials. Additionally, regional mandates on waste reduction and extended producer responsibility encouraged manufacturers to adopt sustainable manufacturing practices. These regulatory frameworks collectively shaped market dynamics by elevating product quality, safety, and environmental responsibility, fostering greater consumer confidence and compliance complexity across global markets.

- •In 2022, the U.S. Consumer Product Safety Commission (CPSC) intensified enforcement of electrical appliance safety standards, compelling manufacturers to enhance insulation, grounding, and overload protection in vegetable cutters and dicers. Concurrently, the EU General Product Safety Directive revisions required comprehensive risk assessments and traceability measures. Several countries in Asia-Pacific introduced national standards aligned with international norms to facilitate export opportunities, increasing compliance requirements for domestic producers. These developments necessitated investment in testing infrastructure and certification processes, impacting time-to-market and operational costs. Manufacturers responded by integrating safety features such as automatic shut-off mechanisms and child-lock functions to meet regulatory expectations. Overall, evolving regulations underscore the critical importance of safety, hygiene, and environmental sustainability in shaping product innovation and market access.

- •Food contact material regulations enacted between 2020 and 2024 globally required the use of non-toxic, corrosion-resistant, and durable materials in vegetable cutters and dicers. Standards such as the EU Regulation No 1935/2004 and FDA’s CFR Title 21 mandated rigorous testing for chemical migration and allergen prevention, influencing material selection and supplier audits. Compliance with these regulations ensures consumer safety and reduces liability risks, but also presents challenges in sourcing and cost management. Manufacturers have increasingly adopted stainless steel, BPA-free plastics, and antimicrobial coatings to meet these requirements. The regulatory emphasis on product traceability and recall mechanisms has also increased, compelling companies to enhance supply chain transparency and documentation.

- •In emerging markets, governments implemented incentives to modernize food processing infrastructure, including subsidies and tax benefits for acquiring certified vegetable cutting equipment. These policies aimed to improve food safety standards and operational efficiency in commercial kitchens and processing plants. However, regulatory heterogeneity across countries necessitates localized compliance strategies. Several regions established mandatory registration and labeling requirements to ensure equipment authenticity and consumer information. These frameworks promote market formalization and consumer protection but increase administrative burdens for manufacturers and importers.

- •Environmental regulations such as the Restriction of Hazardous Substances (RoHS) directive and Waste Electrical and Electronic Equipment (WEEE) directive influenced the disposal and recycling processes for vegetable cutters and dicers in Europe and other territories. Manufacturers are required to minimize hazardous substances in components and facilitate product take-back programs. These mandates encourage circular economy practices and responsible end-of-life management. Compliance entails design adjustments and collaboration with recycling entities, impacting cost structures and corporate social responsibility initiatives. Such regulatory developments are expected to continue shaping sustainable product innovation and lifecycle management within the market.

Market Intelligence

- •15th March 2024, Berkel launched its latest automatic vegetable dicer model featuring advanced programmable settings designed to optimize cutting speed and precision for commercial kitchens. The new model incorporates IoT connectivity for remote monitoring and predictive maintenance, enhancing operational uptime and reducing manual oversight. Targeted at large food processing plants and hospitality sectors, this product aims to improve workflow efficiency while maintaining strict hygiene standards through easy disassembly and cleaning. Berkel’s strategic objective is to expand its footprint in Asia-Pacific, leveraging automation trends and growing foodservice demands in the region. This launch underscores the company’s commitment to integrating technology and innovation to meet evolving industry requirements. Source: Official Berkel Press Release

- •22nd September 2023, Robot Coupe introduced a compact, multifunctional electric vegetable cutter tailored for household consumers seeking convenience and versatility. The device combines slicing, dicing, and shredding functionalities in a single unit with enhanced safety features such as automatic shut-off and non-slip base. Marketed towards urban households with limited kitchen space, this product aligns with rising consumer interest in meal prepping and health-conscious cooking. Robot Coupe’s innovation emphasizes ergonomic design and energy efficiency, contributing to its competitive positioning in the consumer segment. The launch is part of the company’s broader strategy to diversify its product portfolio and strengthen e-commerce presence globally. Source: Robot Coupe Official Website

- •10th November 2024, Hobart Corporation announced a strategic partnership with a leading food processing technology firm to co-develop smart vegetable cutting solutions integrating AI for quality control and operational analytics. This collaboration aims to enhance the efficiency and traceability of food preparation processes in industrial settings, reducing waste and ensuring consistent product quality. The joint initiative focuses on leveraging data-driven insights to optimize cutting parameters, maintenance schedules, and inventory management. Hobart plans to pilot these solutions in North America and Europe, targeting large-scale food processors and commercial kitchens. This move reflects increasing industry emphasis on digital transformation and sustainability. Source: Hobart Corporate Announcement

- •5th June 2023, KitchenAid expanded its product line with the introduction of a handheld vegetable chopper featuring modular blades and cordless operation. Designed for home cooks seeking ease of use and portability, the device enhances chopping efficiency without compromising safety. KitchenAid’s innovation responds to growing consumer demand for compact, versatile kitchen tools that support diverse culinary needs. The launch also involved a digital marketing campaign leveraging influencer partnerships, driving strong initial sales in North America and Europe. This strategic expansion into handheld devices complements KitchenAid’s core offerings and targets the fast-growing meal prep market segment. Source: KitchenAid Press Release

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 3.5 Billion |

| Forecast Year Market Size | USD 7.8 Billion |

| CAGR | 8.3% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7.9% |

| Scope of Report | Market is segmented by Product Type (Manual Vegetable Cutters, Electric Vegetable Cutters, Automatic Vegetable Dicers, Handheld Vegetable Choppers, Industrial Vegetable Dicers), Application (Commercial Kitchens, Food Processing Plants, Household Use, Hospitality Sector, Retail Food Outlets), End-Use Industry (Foodservice Industry, Processed Food Industry, Hospitality Industry, Retail and Supermarkets), Distribution Channel (Direct Sales, Specialized Dealers, Online Retail) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Berkel (United States), Robot Coupe (France), Hobart Corporation (United States), KitchenAid (United States), Braun GmbH (Germany), Moulinex (France), Cuisinart (United States), Hamilton Beach Brands Holding Company (United States), Waring Commercial (United States), Weston Brands (United States), Vitamix (United States), Sammic (Spain), Dito Sama (Belgium), Bamix (Switzerland), Chef'sChoice (United States), Kitchenaid (United States), Jaccard (Switzerland), Arnica (Turkey), Bosch (Germany), Philips (Netherlands), Morphy Richards (United Kingdom), Tefal (France), DeLonghi (Italy), Sunbeam Products (Australia), Electrolux (Sweden) |

Global Vegetable Cutters and Dicers Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.