Global Aliphatic Isocyanates Market Size, Growth & Revenue 2024-2034

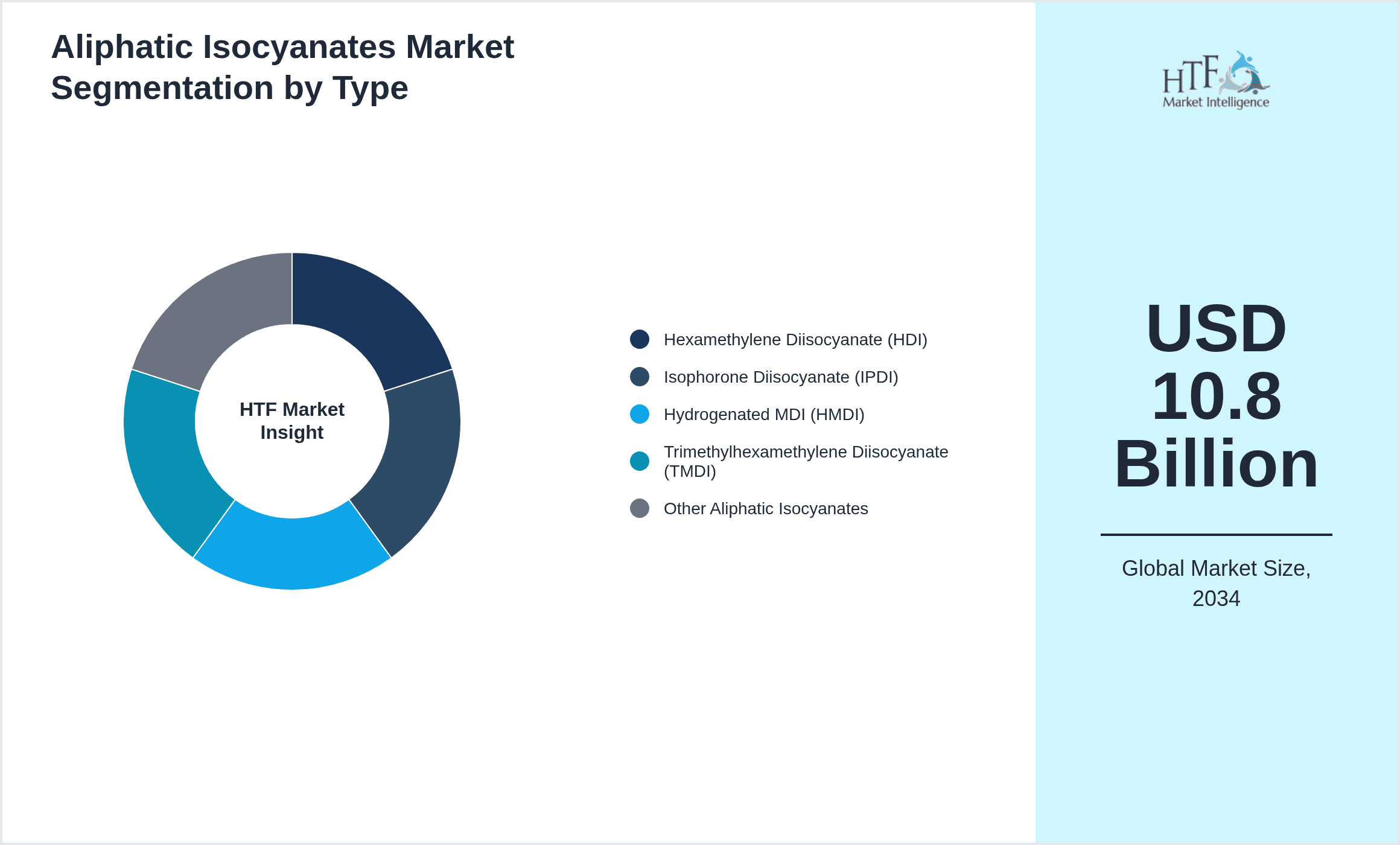

Global Aliphatic Isocyanates Market is segmented by Product Type (Hexamethylene Diisocyanate (HDI), Isophorone Diisocyanate (IPDI), Hydrogenated MDI (HMDI), Trimethylhexamethylene Diisocyanate (TMDI), Other Aliphatic Isocyanates), Application (Coatings, Adhesives & Sealants, Elastomers, Foams, Others), End-Use Industry (Automotive, Construction, Electronics, Textiles), Distribution Channel (Direct Sales, Distributors, Online Channels), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The Global Aliphatic Isocyanates Market is a dynamic and expanding chemical sector focused on the production and application of aliphatic isocyanates, essential intermediates in polyurethane manufacturing. These compounds are recognized for their superior resistance to UV radiation, moisture, and chemicals, making them indispensable in coatings, adhesives, elastomers, and foam products. Hexamethylene Diisocyanate (HDI), Isophorone Diisocyanate (IPDI), and Hydrogenated MDI represent the principal types, each with distinctive properties catering to various industrial applications. The market spans diverse end-use industries such as automotive, construction, electronics, and textiles, driven by increasing demand for durable and environmentally stable materials. Geographically, North America leads the market in terms of size, while Asia-Pacific is the fastest-growing region due to rapid industrialization and infrastructure development. Innovations in bio-based isocyanates and stricter environmental regulations are shaping the market landscape. This report offers an in-depth analysis of market segmentation, competitive landscape, growth drivers, challenges, and future opportunities through 2034.

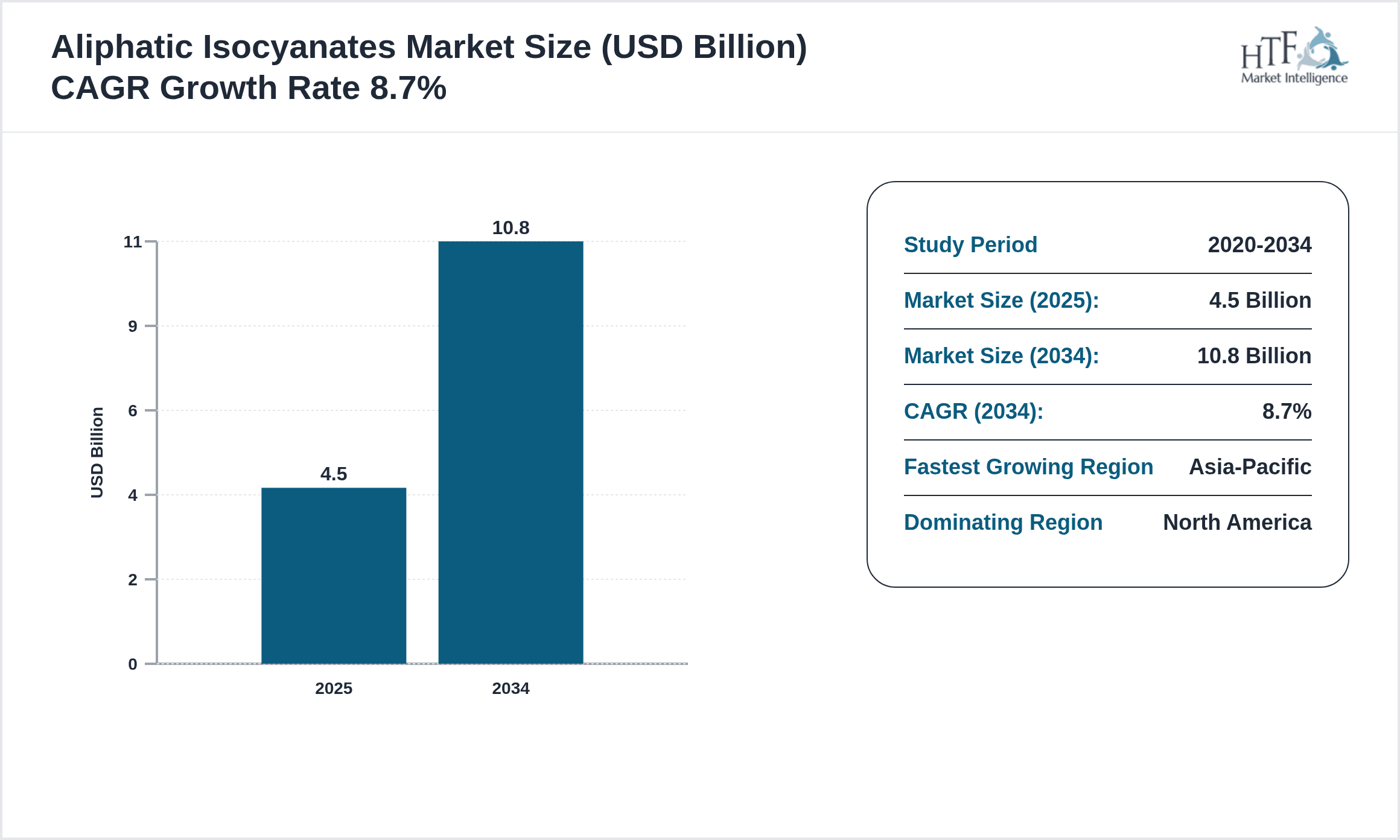

- •Key market highlights include a base market size of USD 4.5 Billion in 2024, projected to reach USD 10.8 Billion by 2034, reflecting a robust CAGR of 8.7%. Hexamethylene Diisocyanate dominates with the largest market share, propelled by extensive use in industrial coatings and automotive finishes. Meanwhile, Isophorone Diisocyanate is the fastest-growing product type owing to its versatile applications in high-performance coatings. The coatings segment leads application-wise, benefiting from increasing demand in construction and automotive sectors. North America holds the dominant regional position due to technological advancements and established chemical manufacturing infrastructure, whereas Asia-Pacific witnesses rapid growth driven by expanding manufacturing bases and rising urbanization. Key players continue investing in R&D and strategic partnerships to enhance product portfolios and expand geographic reach, positioning the market for sustained growth amid evolving regulatory landscapes and technological innovation.

- •The value proposition of aliphatic isocyanates lies in their ability to enhance durability, chemical resistance, and environmental stability of polyurethane-based products, crucial for industries demanding long-lasting performance. Their strategic importance spans automotive coatings that require UV resistance, adhesives that demand strong bonding, and elastomers with flexibility and wear resistance. Stakeholders, including chemical manufacturers, end-users, and investors, benefit from market growth driven by evolving consumer preferences for sustainable and high-performance materials. Innovations in bio-based aliphatic isocyanates and increasing emphasis on green chemistry further enhance market attractiveness. The global market’s trajectory is influenced by regulatory frameworks targeting hazardous emissions, pushing manufacturers towards safer alternatives and advanced formulations. Consequently, the aliphatic isocyanates market represents a vital segment within the broader polyurethane industry, offering substantial growth potential and technological advancement opportunities.

Competitive Landscape

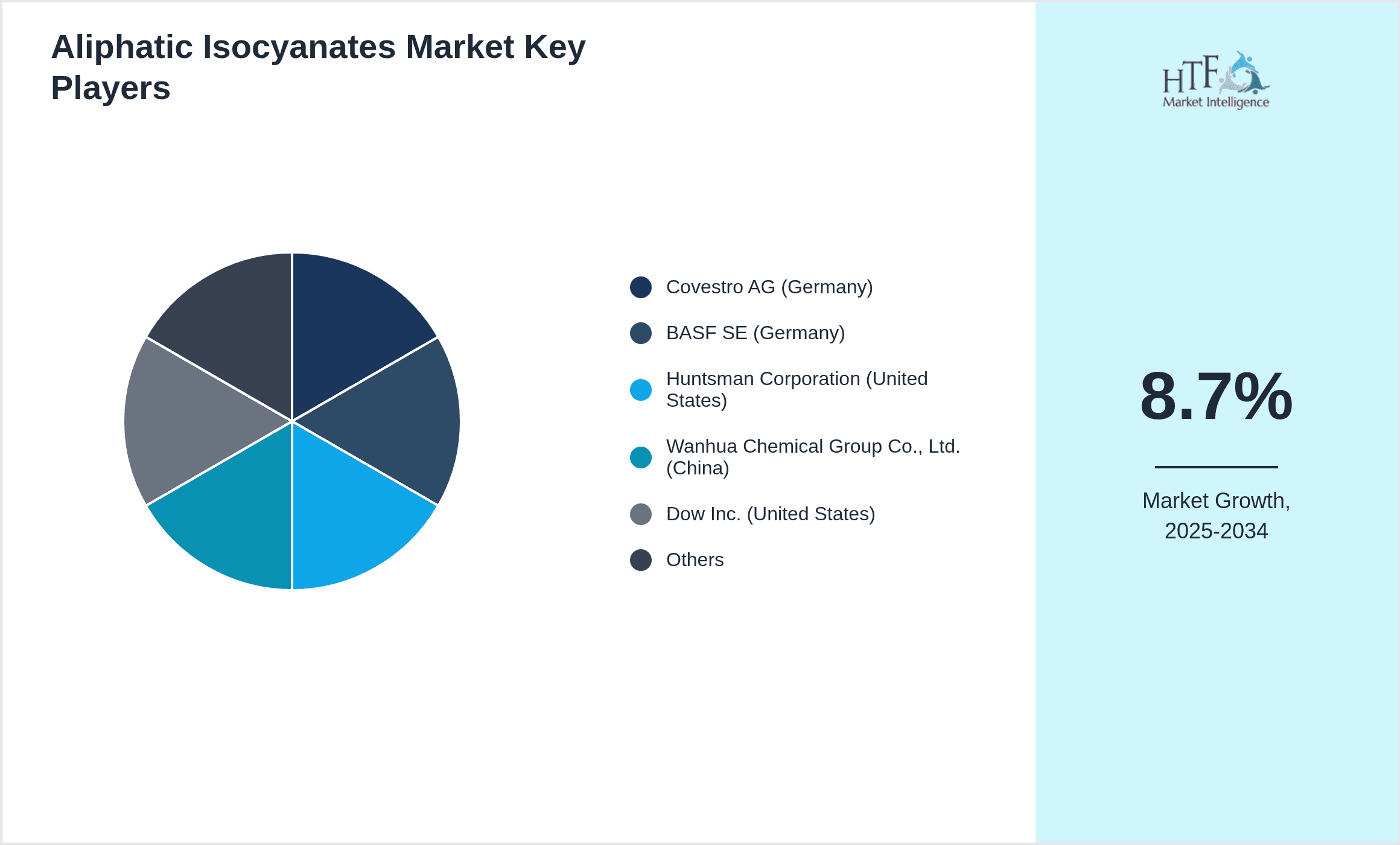

The competitive environment in the Global Aliphatic Isocyanates Market is characterized by a mix of established multinational chemical corporations and agile regional players. Market leaders employ diverse strategies such as product innovation, capacity expansions, and strategic partnerships to maintain and enhance their market positions. Innovation is centered on developing bio-based and low-VOC isocyanates to comply with environmental regulations and meet sustainability goals. Companies invest heavily in R&D to improve product performance and develop customized solutions for specific end-use applications, thereby driving differentiation. The rivalry is intensified by the need to expand geographic presence, especially in emerging markets like Asia-Pacific and Latin America. Pricing strategies balance raw material cost fluctuations with the demand for high-quality products. Mergers and acquisitions have also shaped market dynamics by enabling portfolio diversification and strengthening supply chains. Overall, competitive success hinges on technological leadership, regulatory compliance, and the ability to address evolving customer needs globally.

Leading Companies in Aliphatic Isocyanates Market

- •Covestro AG (Germany)

- •BASF SE (Germany)

- •Huntsman Corporation (United States)

- •Wanhua Chemical Group Co., Ltd. (China)

- •Dow Inc. (United States)

- •Mitsubishi Chemical Holdings Corporation (Japan)

- •Evonik Industries AG (Germany)

- •Bayer AG (Germany)

- •Asahi Kasei Corporation (Japan)

- •Yantai Wanhua Polyurethane Co., Ltd. (China)

- •Nippon Polyurethane Industry Co., Ltd. (Japan)

- •Huntsman Advanced Materials (United States)

- •MITSUI Chemicals, Inc. (Japan)

- •W. R. Grace & Co. (United States)

- •Covestro Chemicals Asia Pacific Pte. Ltd. (Singapore)

- •Tronox Holdings plc (United States)

- •Kumho Mitsui Chemicals, Inc. (South Korea)

- •Evonik Japan Co., Ltd. (Japan)

- •Shell Chemicals Ltd. (United Kingdom)

- •LG Chem Ltd. (South Korea)

- •Sumitomo Chemical Co., Ltd. (Japan)

- •Celanese Corporation (United States)

- •Lanxess AG (Germany)

- •INEOS Group AG (Switzerland)

- •Hexion Inc. (United States)

Market Breakdown

- •By Product Type

- ◦Hexamethylene Diisocyanate (HDI)

- ◦Isophorone Diisocyanate (IPDI)

- ◦Hydrogenated MDI (HMDI)

- ◦Trimethylhexamethylene Diisocyanate (TMDI)

- ◦Other Aliphatic Isocyanates

- •By Application

- ◦Coatings

- ◦Adhesives & Sealants

- ◦Elastomers

- ◦Foams

- ◦Others

- •By End-Use Industry

- ◦Automotive

- ◦Construction

- ◦Electronics

- ◦Textiles

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors

- ◦Online Channels

Growth Dynamics

- •Increasing demand for durable and UV-resistant coatings across automotive and construction industries is a primary growth driver. Aliphatic isocyanates offer superior weather resistance, appealing to manufacturers seeking long-lasting finishes. This trend is supported by rising vehicle production and infrastructure development globally.

- •Technological advancements in bio-based aliphatic isocyanates are fostering sustainable product development, attracting eco-conscious consumers and complying with stringent environmental regulations. Companies investing in green chemistry innovations are gaining competitive advantages.

- •Growth in emerging economies, particularly in Asia-Pacific, due to rapid urbanization and industrialization is expanding the market footprint. Increasing middle-class populations and infrastructure projects stimulate demand for high-performance coatings and adhesives.

- •Stringent regulatory frameworks on VOC emissions and hazardous chemicals drive the adoption of aliphatic isocyanates as safer alternatives to aromatic counterparts. This regulatory push accelerates product innovation and market acceptance globally.

- •Rising application of aliphatic isocyanates in electronics for protective coatings and adhesives is opening new growth avenues, driven by the expanding consumer electronics and renewable energy sectors. Enhanced product formulations improve electrical insulation and durability.

Market Trends

- •There is a growing trend toward the development and commercialization of bio-based aliphatic isocyanates, reducing reliance on petrochemical feedstocks and enhancing sustainability credentials. This shift is gaining momentum among leading manufacturers seeking environmental compliance.

- •Manufacturers are increasingly adopting digitalization and automation in production processes to improve product consistency and operational efficiency, reducing costs and enhancing supply chain responsiveness.

- •Strategic collaborations between chemical companies and end-user industries are becoming prevalent, facilitating tailored product development and faster market penetration, particularly in automotive and electronics sectors.

- •The trend of product diversification to include low-VOC and solvent-free aliphatic isocyanates is gaining traction, addressing environmental regulations and consumer demand for safer products.

- •Emerging applications in flexible foams and elastomers for wearable electronics and medical devices are driving innovation and expanding the market scope beyond traditional segments.

Market Opportunities

- •Expanding infrastructure development in emerging markets presents significant opportunities for growth in coatings and adhesives applications, driven by government investments and urbanization.

- •Innovation in bio-based and sustainable aliphatic isocyanates offers potential for product differentiation and entry into environmentally regulated markets worldwide.

- •Development of specialty aliphatic isocyanates tailored for electronics and renewable energy applications opens new revenue streams and market segments.

- •Strategic alliances and joint ventures with regional manufacturers can facilitate market penetration in high-growth regions such as Asia-Pacific and Latin America.

- •Investment in digital supply chain management enables improved distribution efficiency and customer engagement, fostering competitive advantages.

Market Challenges

- •Volatility in raw material prices, especially petrochemical derivatives, poses cost challenges for manufacturers, impacting pricing strategies and profit margins.

- •Stringent environmental regulations require significant compliance efforts and investments in safer production technologies, increasing operational complexities.

- •High capital expenditure for setting up advanced manufacturing facilities limits market entry for smaller players and constrains capacity expansion.

- •Competition from alternative materials and technologies, such as waterborne coatings and non-isocyanate polyurethanes, challenges market growth and product adoption.

- •Supply chain disruptions due to geopolitical tensions and global logistics complexities affect raw material availability and delivery schedules.

Regulatory Framework

- •The REACH regulation implemented between 2019 and 2024 in Europe mandates strict registration and evaluation of isocyanates, enhancing safety standards and limiting hazardous substances in the market.

- •The U.S. EPA's National Emission Standards for Hazardous Air Pollutants (NESHAP) updated in 2021 imposes stringent VOC emission limits affecting aliphatic isocyanate manufacturing and application processes.

- •China’s Ministry of Ecology and Environment introduced mandatory environmental impact assessments for chemical producers in 2020, requiring compliance with pollution control norms for isocyanates.

- •Japan’s Chemical Substances Control Law (CSCL) revision in 2022 focuses on enhancing chemical safety and promoting green chemistry, influencing product formulations and manufacturing practices.

- •Global initiatives like the United Nations’ Globally Harmonized System (GHS) for classification and labeling of chemicals have standardized safety data sheet requirements and hazard communication for aliphatic isocyanates since 2019.

Market Intelligence

- •15th January 2025, Covestro AG launched a new line of bio-based Hexamethylene Diisocyanate products designed to reduce carbon footprint in automotive coatings. These products offer enhanced UV resistance and durability while aligning with sustainability targets of leading automakers. The launch supports Covestro’s strategic focus on green chemistry and expands its portfolio in high-performance polyurethane raw materials, aiming to capture growing demand in Europe and Asia-Pacific.

- •10th March 2025, BASF SE introduced an innovative solvent-free Isophorone Diisocyanate (IPDI) variant optimized for adhesives and sealants applications. This product reduces VOC emissions and enhances bonding strength, catering to evolving regulatory standards globally. BASF’s development underscores its commitment to sustainable product innovation and aims to strengthen its market position across North America and Latin America.

- •22nd June 2025, Wanhua Chemical Group Co., Ltd. announced a strategic partnership with a leading electronics manufacturer to develop specialized aliphatic isocyanate-based elastomers for flexible electronics. The collaboration focuses on tailored formulations providing enhanced flexibility and thermal stability, targeting the rapidly growing wearable technology market in Asia-Pacific. This initiative reflects Wanhua’s strategy to diversify applications and enhance technological capabilities.

- •5th October 2025, Huntsman Corporation completed the acquisition of a regional polyurethane chemicals producer to expand its manufacturing capacity for hydrogenated MDI in North America. This acquisition supports Huntsman’s growth strategy by increasing supply chain efficiency and product availability amid rising demand in construction and automotive sectors. The move strengthens Huntsman’s competitive edge in the aliphatic isocyanates market and broadens its customer base.

- •Source: Official company press releases, Industry publications

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 4.5 Billion |

| Forecast Year Market Size | USD 10.8 Billion |

| CAGR | 8.7% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 8.4% |

| Scope of Report | Market is segmented by Product Type (Hexamethylene Diisocyanate (HDI), Isophorone Diisocyanate (IPDI), Hydrogenated MDI (HMDI), Trimethylhexamethylene Diisocyanate (TMDI), Other Aliphatic Isocyanates), Application (Coatings, Adhesives & Sealants, Elastomers, Foams, Others), End-Use Industry (Automotive, Construction, Electronics, Textiles), Distribution Channel (Direct Sales, Distributors, Online Channels) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Covestro AG (Germany), BASF SE (Germany), Huntsman Corporation (United States), Wanhua Chemical Group Co., Ltd. (China), Dow Inc. (United States), Mitsubishi Chemical Holdings Corporation (Japan), Evonik Industries AG (Germany), Bayer AG (Germany), Asahi Kasei Corporation (Japan), Yantai Wanhua Polyurethane Co., Ltd. (China), Nippon Polyurethane Industry Co., Ltd. (Japan), Huntsman Advanced Materials (United States), MITSUI Chemicals, Inc. (Japan), W. R. Grace & Co. (United States), Covestro Chemicals Asia Pacific Pte. Ltd. (Singapore), Tronox Holdings plc (United States), Kumho Mitsui Chemicals, Inc. (South Korea), Evonik Japan Co., Ltd. (Japan), Shell Chemicals Ltd. (United Kingdom), LG Chem Ltd. (South Korea), Sumitomo Chemical Co., Ltd. (Japan), Celanese Corporation (United States), Lanxess AG (Germany), INEOS Group AG (Switzerland), Hexion Inc. (United States) |

Global Aliphatic Isocyanates Market Size, Growth & Revenue 2024-2034 - Table of Contents

Research enthusiast focused on transforming data uncovering into actionable insights through data-driven decision-making.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.