United States Methyl Cellulose Market Size, Growth & Revenue 2024-2034

United States Methyl Cellulose Market is segmented by Product Type (Powder Methyl Cellulose, Granules Methyl Cellulose, Flakes Methyl Cellulose, Pellets Methyl Cellulose, Other Forms), Application (Construction, Pharmaceuticals, Food & Beverages, Personal Care, Oil & Gas), End-Use Industry (Building & Construction, Healthcare & Pharmaceuticals, Food Processing, Consumer Personal Care), Distribution Channel (Direct Sales, Distributors & Wholesalers, Online Sales), and Geography (Northeast, Southwest, The South, The Midwest)

Pricing

Report Overview

Executive Summary

- •The United States methyl cellulose market is a vital segment of the chemical additives industry, serving multiple sectors including construction, pharmaceuticals, food & beverages, personal care, and oil & gas. This market includes diverse types of methyl cellulose products such as powders, granules, flakes, and pellets, each tailored to specific application needs. Methyl cellulose is prized for its water retention, binding, emulsifying, and thickening properties, making it a core ingredient in adhesive formulations, drug delivery systems, food texture enhancement, cosmetic products, and drilling fluids. The market is defined by stringent regulatory oversight, technological innovations in bio-based and sustainable derivatives, and evolving consumer preferences towards eco-friendly ingredients. Forecasts indicate a robust CAGR of 10.5% between 2024 and 2034, driven by expanding construction activities, rising pharmaceutical manufacturing, and diversified food applications. Key regional markets within the United States include the West Coast as the dominant zone and the Southeast exhibiting the fastest growth due to increasing industrial investments and infrastructure development. Competitive dynamics involve continuous product innovation and strategic partnerships among leading chemical manufacturers. The market’s growth is also supported by expanding distribution networks and rising awareness of methyl cellulose benefits across end-use applications.

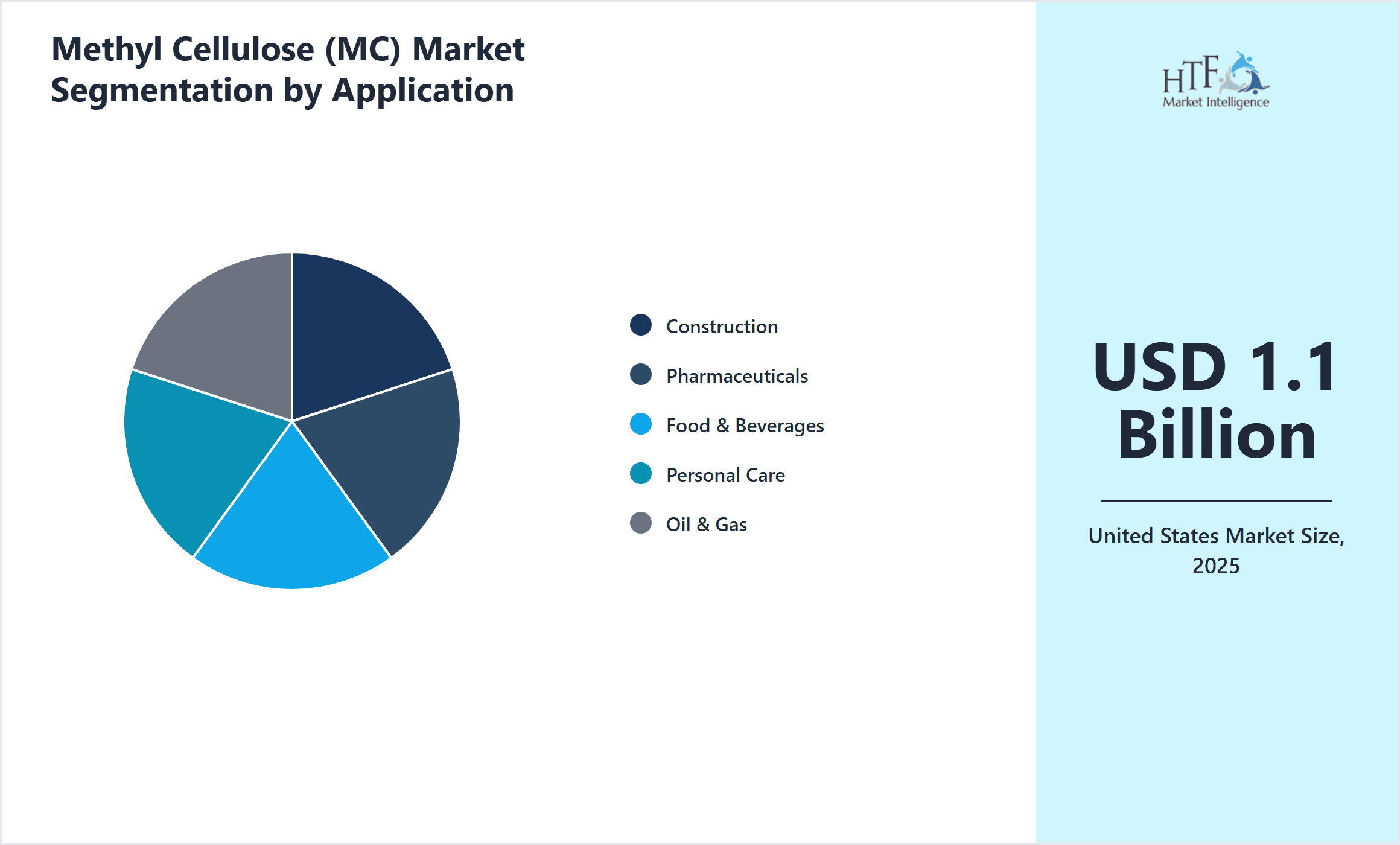

- •Market highlights include the base market size of USD 1.1 billion in 2024, projected to reach USD 2.8 billion by 2034, reflecting strong demand and expanding applications. Powder type methyl cellulose currently leads the product segment, favored for its versatility and ease of use, while pellets are rapidly gaining traction due to improved handling and dosing advantages. Construction applications dominate the usage spectrum, followed by pharmaceuticals, supported by increasing demand for sustainable construction materials and advanced drug formulations. The West Coast region holds the largest market share, driven by dense urbanization and manufacturing hubs, whereas the Southeast region's rapid growth is attributed to infrastructure expansion and favorable business climates. Year-over-year growth rates remain consistent at around 10%, underscoring the market's resilience amidst economic fluctuations. Regulatory compliance and technological advancements continue to shape product innovation and market access. The competitive landscape is marked by aggressive R&D investments and collaborations to enhance product efficacy and sustainability profiles.

- •The United States methyl cellulose market offers significant value to stakeholders across construction, pharmaceutical, food, personal care, and oil & gas industries by enabling product performance improvements and process efficiencies. Strategic importance lies in methyl cellulose's multifunctionality, which supports innovation in product formulations, enhances environmental compliance, and meets consumer demand for high-quality additives. Manufacturers benefit from expanding end-use sectors, regulatory support for sustainable materials, and technological advances in production processes. Distributors and end-users gain access to a broad portfolio of product forms and customized solutions, facilitating diverse applications. Furthermore, the market's growth trajectory presents opportunities for new entrants and established players to capitalize on emerging trends such as bio-based methyl cellulose derivatives, digital supply chain integration, and regional expansion in high-growth zones. Overall, the market underpins critical industrial processes and consumer product development, reinforcing its strategic role within the United States chemical additives ecosystem.

Competitive Landscape

The competitive environment in the United States methyl cellulose market is characterized by a blend of global chemical manufacturers and specialized domestic producers, fostering a dynamic market with intense rivalry. Companies compete on the basis of product innovation, quality, sustainability credentials, and cost efficiency. Innovation strategies focus on developing bio-based and specialty methyl cellulose variants to meet stringent regulatory standards and evolving end-user requirements, particularly in pharmaceuticals and food industries. Strategic partnerships, joint ventures, and distribution agreements are common approaches to expanding market reach and enhancing technical capabilities. The market exhibits moderate entry barriers due to regulatory compliance, capital requirements, and technological expertise. Pricing strategies reflect the balance between raw material costs and value-added product differentiation. Regional competition is pronounced, with firms leveraging proximity to key industrial hubs such as the West Coast and Southeast to optimize logistics and customer service. Future trends indicate increased consolidation through mergers and acquisitions, augmented digital transformation in supply chains, and a growing emphasis on sustainable production methods to maintain competitive advantage.

Leading Companies in Methyl Cellulose Market

- •Dow Chemical Company (United States)

- •Ashland Global Holdings Inc. (United States)

- •The Lubrizol Corporation (United States)

- •Shandong Dongda Chemical Co., Ltd. (China)

- •CP Kelco U.S., Inc. (United States)

- •Akzo Nobel N.V. (Netherlands)

- •Celluvisc (United States)

- •Nouryon (Netherlands)

- •Lotte Fine Chemical Co., Ltd. (South Korea)

- •Ashapura Group (India)

- •MCC Biochemicals (United States)

- •Hercules Inc. (United States)

- •CPMC Group (China)

- •Jiangsu Guotai International Group (China)

- •Seppic (France)

- •FMC Corporation (United States)

- •Lamberti S.p.A. (Italy)

- •Ashland Specialty Ingredients (United States)

- •Mitsubishi Chemical Corporation (Japan)

- •BASF SE (Germany)

- •DuPont de Nemours, Inc. (United States)

- •Hubei Xingfa Chemicals Group Co., Ltd. (China)

- •Domo Chemicals (Belgium)

- •Jungbunzlauer Suisse AG (Switzerland)

- •Sekisui Chemical Co., Ltd. (Japan)

Market Breakdown

- •By Product Type

- ◦Powder Methyl Cellulose

- ◦Granules Methyl Cellulose

- ◦Flakes Methyl Cellulose

- ◦Pellets Methyl Cellulose

- ◦Other Forms

- •By Application

- ◦Construction

- ◦Pharmaceuticals

- ◦Food & Beverages

- ◦Personal Care

- ◦Oil & Gas

- •By End-Use Industry

- ◦Building & Construction

- ◦Healthcare & Pharmaceuticals

- ◦Food Processing

- ◦Consumer Personal Care

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors & Wholesalers

- ◦Online Sales

Growth Dynamics

- •The United States methyl cellulose market's growth is primarily driven by expanding construction activities fueled by urbanization and infrastructure development, increasing the demand for high-performance adhesives and binders. Additionally, growth in pharmaceutical manufacturing, particularly for controlled-release drug formulations, supports market expansion. The food & beverage industry’s rising incorporation of methyl cellulose as a stabilizer and emulsifier enhances textural attributes in gluten-free and low-fat products, further boosting consumption. Technological advancements in producing bio-based and environmentally friendly methyl cellulose variants align with regulatory trends and consumer preferences, reinforcing demand. Regional industrial growth, especially in the West Coast and Southeast zones, provides localized market stimulation, supported by favorable business climates and investment incentives. Overall, these drivers contribute to a robust compound annual growth rate, positioning the market for sustained expansion through 2034.

- •Market trends indicate a growing focus on sustainability, with manufacturers investing in green chemistry approaches to produce methyl cellulose from renewable cellulose sources, reducing environmental footprint. Digitalization of supply chains and e-commerce platforms is facilitating more efficient distribution channels and customer engagement. The demand for specialty methyl cellulose grades tailored for pharmaceutical and personal care applications is rising, reflecting innovation in formulation science. Moreover, integration of methyl cellulose in novel food products such as plant-based meat alternatives exemplifies evolving consumer preferences. Collaborative R&D efforts between chemical producers and end-use industries accelerate product development cycles and market responsiveness. These trends collectively enhance market resilience and adaptability amid changing regulatory and economic landscapes.

- •Market restraints include the volatility of raw material prices, particularly cellulose derivatives sourced from wood pulp, which can impact production costs and pricing stability. Regulatory challenges, especially stringent food safety and pharmaceutical compliance requirements, impose additional costs and limit product flexibility. The presence of alternative additives and substitutes such as hydroxypropyl methylcellulose (HPMC) and other cellulose ethers creates competitive pressure, potentially reducing methyl cellulose market share. Furthermore, supply chain disruptions, including logistics constraints and import-export restrictions, may hamper consistent market supply. Lastly, the high capital investment needed for advanced manufacturing facilities limits entry for smaller players, consolidating market power among established companies.

- •Opportunities in the United States methyl cellulose market arise from expanding applications in emerging sectors such as plant-based food products, advanced drug delivery systems, and eco-friendly personal care formulations. Geographic expansion within high-growth regional zones like the Southeast enables companies to tap into underserved markets and benefit from regional incentives. Innovations in product forms such as pellets and specialty blends offer enhanced handling and performance benefits, opening new customer segments. Strategic acquisitions and partnerships to access novel technologies and broaden product portfolios provide competitive advantages. Furthermore, increasing consumer awareness about sustainable and safe ingredients fosters demand for methyl cellulose, particularly in clean-label food and natural cosmetic markets.

- •Challenges confronting the methyl cellulose market include navigating complex regulatory frameworks that differ across federal and state levels, requiring substantial compliance investments. Maintaining consistent product quality amid raw material variability poses operational hurdles. Market penetration in price-sensitive segments is difficult due to competition from lower-cost substitutes. Additionally, the need for continuous innovation to meet evolving application requirements demands significant R&D expenditure. Supply chain disruptions and fluctuating demand patterns amid economic uncertainties present risks to stable growth. Addressing these challenges requires strategic planning, investment in quality assurance, and agile market strategies to sustain competitive positioning.

Market Trends

- •Sustainability has become a central trend with manufacturers increasingly adopting bio-based cellulose sources and eco-friendly production processes to meet regulatory and consumer demands for greener products. This shift is influencing product development and marketing strategies significantly.

- •The rise of digital transformation in distribution channels enables improved supply chain transparency and efficiency, allowing manufacturers and distributors to respond swiftly to fluctuating market demands and optimize inventory management.

- •Increasing demand for specialty methyl cellulose grades in pharmaceuticals and cosmetics is fostering niche product innovation, driven by the need for customized rheological properties and enhanced functional performance.

- •Integration of methyl cellulose in emerging food products, such as plant-based meat alternatives and gluten-free formulations, reflects shifting consumer preferences towards health-conscious and sustainable diets.

- •Collaborative partnerships between chemical producers and end-use industries are accelerating innovation pipelines, facilitating faster commercialization of advanced methyl cellulose formulations.

- •Consumer focus on clean-label and natural ingredients is driving market segmentation and product differentiation, emphasizing transparency and ingredient safety in methyl cellulose applications.

- •Emerging technologies in cellulose modification and processing are enabling the development of multifunctional methyl cellulose products with improved performance and sustainability profiles, shaping future market directions.

Market Opportunities

- •Expanding applications in plant-based and alternative protein food products present significant growth potential, allowing methyl cellulose to serve as a functional ingredient for texture and stability in novel formulations.

- •Geographic expansion into rapidly growing regions like the Southeast United States offers access to new industrial hubs and consumer markets, supported by favorable economic policies and infrastructure development.

- •Investment in specialty product development, including pellets and customized viscosity grades, can unlock new customer segments and improve product usability across varied applications.

- •Strategic partnerships and acquisitions enable companies to enhance technological capabilities, diversify portfolios, and expand market presence effectively.

- •Increasing consumer demand for natural and sustainable personal care products creates avenues for methyl cellulose to be utilized as a bio-based thickener and stabilizer in cosmetics and toiletries.

- •Regulatory incentives promoting sustainable chemical production offer opportunities for early movers adopting green manufacturing processes in methyl cellulose production.

- •Future-focused R&D on multifunctional methyl cellulose derivatives can address unmet needs in pharmaceuticals and advanced material applications, positioning companies as innovation leaders.

Market Challenges

- •Regulatory complexity across federal and state agencies requires substantial compliance efforts, increasing operational costs and extending product approval timelines for methyl cellulose manufacturers.

- •Raw material price volatility, particularly for cellulose pulp, impacts production costs and pricing stability, challenging manufacturers to maintain competitive margins.

- •Competition from alternative additives such as hydroxypropyl methylcellulose and synthetic polymers limits market share growth, necessitating continuous product differentiation.

- •High capital investments for advanced production technologies and quality control systems create barriers to entry and expansion for smaller market participants.

- •Supply chain disruptions, including transportation delays and import-export restrictions, affect timely product availability and customer satisfaction.

- •Maintaining consistent product quality amid variability in raw material sources demands rigorous quality assurance protocols and supplier management.

- •Rapidly evolving customer requirements and application standards require ongoing R&D investment, posing financial and operational challenges.

Regulatory Framework

- •Between 2019 and 2024, the US Food and Drug Administration (FDA) updated guidelines on food additive approvals, including methyl cellulose, emphasizing purity, safety, and labeling requirements to ensure consumer protection in food and pharmaceutical products.

- •The Environmental Protection Agency (EPA) introduced stricter emission and waste management standards for chemical manufacturing facilities in 2021, impacting methyl cellulose producers by mandating cleaner production technologies and reducing environmental footprint.

- •Occupational Safety and Health Administration (OSHA) enhanced workplace safety regulations in 2022, focusing on handling and storage of chemical powders like methyl cellulose to minimize occupational hazards and improve employee safety.

- •State-level regulations, notably in California under Proposition 65, require disclosure of certain chemical components, influencing labeling and compliance strategies for methyl cellulose products marketed within the state.

- •Federal initiatives promoting sustainable chemical production, including tax incentives and grants introduced in 2023, encourage manufacturers to adopt green technologies in methyl cellulose production, fostering innovation and market competitiveness.

Market Intelligence

- •15th January 2025, Dow Chemical Company launched a new bio-based methyl cellulose powder aimed at the construction industry, featuring enhanced water retention and sustainability credentials. This product targets eco-conscious builders and manufacturers seeking high-performance additives with reduced environmental impact. The launch aligns with increasing demand for green building materials in the United States, especially in the West Coast and Southeast regions. Dow’s strategic focus on renewable raw materials and advanced manufacturing processes underscores its commitment to innovation and market leadership. The new product is expected to capture significant market share in sustainable construction applications by 2027. Source: Dow Chemical Official Press Release

- •7th March 2025, Ashland Global Holdings Inc. introduced a specialty methyl cellulose grade designed for pharmaceutical controlled-release formulations. This innovation offers improved viscosity control and drug release profiles, addressing critical needs in oral and topical drug delivery systems. The product launch supports Ashland’s strategy to expand its pharmaceutical excipient portfolio and cater to increasing demand from US pharmaceutical manufacturers focusing on generic and novel drug products. The formulation enhances patient compliance and therapeutic efficacy, positioning Ashland as a key player in advanced pharmaceutical ingredients. Market analysts anticipate accelerated adoption in the Midwest and Northeast pharmaceutical hubs. Source: Ashland Global Holdings Official Announcement

- •22nd June 2025, The Lubrizol Corporation announced a strategic partnership with a leading personal care brand to develop methyl cellulose-based natural thickeners for cosmetic applications. This collaboration aims to innovate sustainable and effective ingredients for skincare and haircare products, responding to consumer demand for clean-label formulations. The partnership includes co-development of customized methyl cellulose grades with superior sensory attributes and stability. The initiative is expected to strengthen Lubrizol’s position in the personal care additives market and expand its customer base in the Southeast and West Coast regions. The joint venture also focuses on scaling production capabilities to meet growing market needs. Source: The Lubrizol Corporation Press Release

- •10th October 2025, CP Kelco U.S., Inc. expanded its methyl cellulose production facility in Texas to increase capacity and enhance supply chain efficiency for the food and beverage sector. The expansion supports rising demand for methyl cellulose as a stabilizer and emulsifier in plant-based food products and gluten-free items. CP Kelco’s investment reflects confidence in the sustained growth of these segments within the United States and aims to reduce lead times for major clients across the Southeast and Southwest regions. The upgraded facility incorporates energy-efficient technologies and adheres to stringent quality standards, reinforcing CP Kelco’s commitment to sustainability and product excellence. Source: CP Kelco Official Company Statement

Regional Outlook

The West Coast currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Southeast is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Northeast

- Southwest

- The South

- The Midwest

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.1 Billion |

| Forecast Year Market Size | USD 2.8 Billion |

| CAGR | 10.5% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 10% |

| Scope of Report | Market is segmented by Product Type (Powder Methyl Cellulose, Granules Methyl Cellulose, Flakes Methyl Cellulose, Pellets Methyl Cellulose, Other Forms), Application (Construction, Pharmaceuticals, Food & Beverages, Personal Care, Oil & Gas), End-Use Industry (Building & Construction, Healthcare & Pharmaceuticals, Food Processing, Consumer Personal Care), Distribution Channel (Direct Sales, Distributors & Wholesalers, Online Sales) |

| Regions Covered | Northeast, Southwest, The South, The Midwest |

| Key Companies | Dow Chemical Company (United States), Ashland Global Holdings Inc. (United States), The Lubrizol Corporation (United States), Shandong Dongda Chemical Co., Ltd. (China), CP Kelco U.S., Inc. (United States), Akzo Nobel N.V. (Netherlands), Celluvisc (United States), Nouryon (Netherlands), Lotte Fine Chemical Co., Ltd. (South Korea), Ashapura Group (India), MCC Biochemicals (United States), Hercules Inc. (United States), CPMC Group (China), Jiangsu Guotai International Group (China), Seppic (France), FMC Corporation (United States), Lamberti S.p.A. (Italy), Ashland Specialty Ingredients (United States), Mitsubishi Chemical Corporation (Japan), BASF SE (Germany), DuPont de Nemours, Inc. (United States), Hubei Xingfa Chemicals Group Co., Ltd. (China), Domo Chemicals (Belgium), Jungbunzlauer Suisse AG (Switzerland), Sekisui Chemical Co., Ltd. (Japan) |

United States Methyl Cellulose Market Size, Growth & Revenue 2024-2034 - Table of Contents

Multidisciplinary researcher with 10+ years of experience uncovering insights across diverse domains focused on uncovering insights that drive informed decisions.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.