Global Light and Heavy Duty Natural Gas Vehicle Market Size, Growth & Revenue 2025-2034

Global Light and Heavy Duty Natural Gas Vehicle Market is segmented by Type (Compressed Natural Gas Vehicles, Liquefied Natural Gas Vehicles, Dual Fuel Vehicles, Bi-Fuel Vehicles, Others), Application (Light Duty Vehicles, Heavy Duty Vehicles, Commercial Transportation, Public Transport, Logistics), End-Use Industry (Transportation & Logistics, Public Sector & Government, Commercial Fleets, Private Consumers), Distribution Channel (OEMs, Aftermarket, Fleet Operators), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global Light and Heavy Duty Natural Gas Vehicle market includes a comprehensive range of vehicles powered by natural gas fuels such as compressed natural gas and liquefied natural gas. This market spans light-duty passenger vehicles, heavy-duty trucks, buses, and commercial transport vehicles, including dual fuel and bi-fuel variants. Natural gas vehicles provide significant environmental benefits by reducing carbon emissions and particulate matter compared to conventional diesel and gasoline-powered vehicles. The market also addresses economic concerns by offering cost-effective fuel alternatives amid fluctuating oil prices. Technological improvements in fuel storage, engine efficiency, and infrastructure development support increasing adoption worldwide. Government policies promoting cleaner transportation fuels, alongside rising urbanization and demand for sustainable logistics solutions, underscore the market's strategic importance. The expanding global focus on reducing carbon footprints and adhering to stringent emission standards further accelerates market growth, making natural gas vehicles a critical player in the transition to greener mobility solutions.

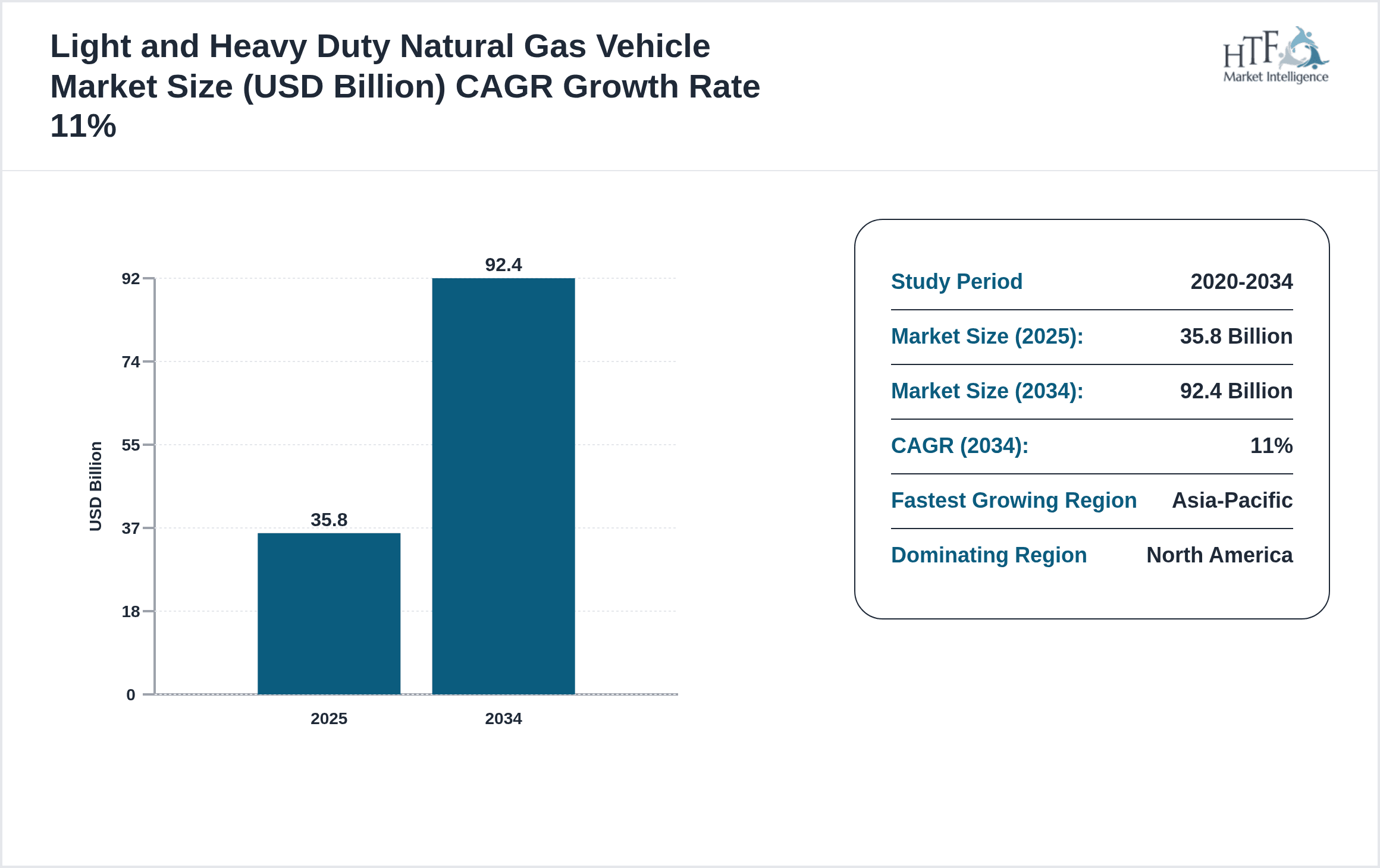

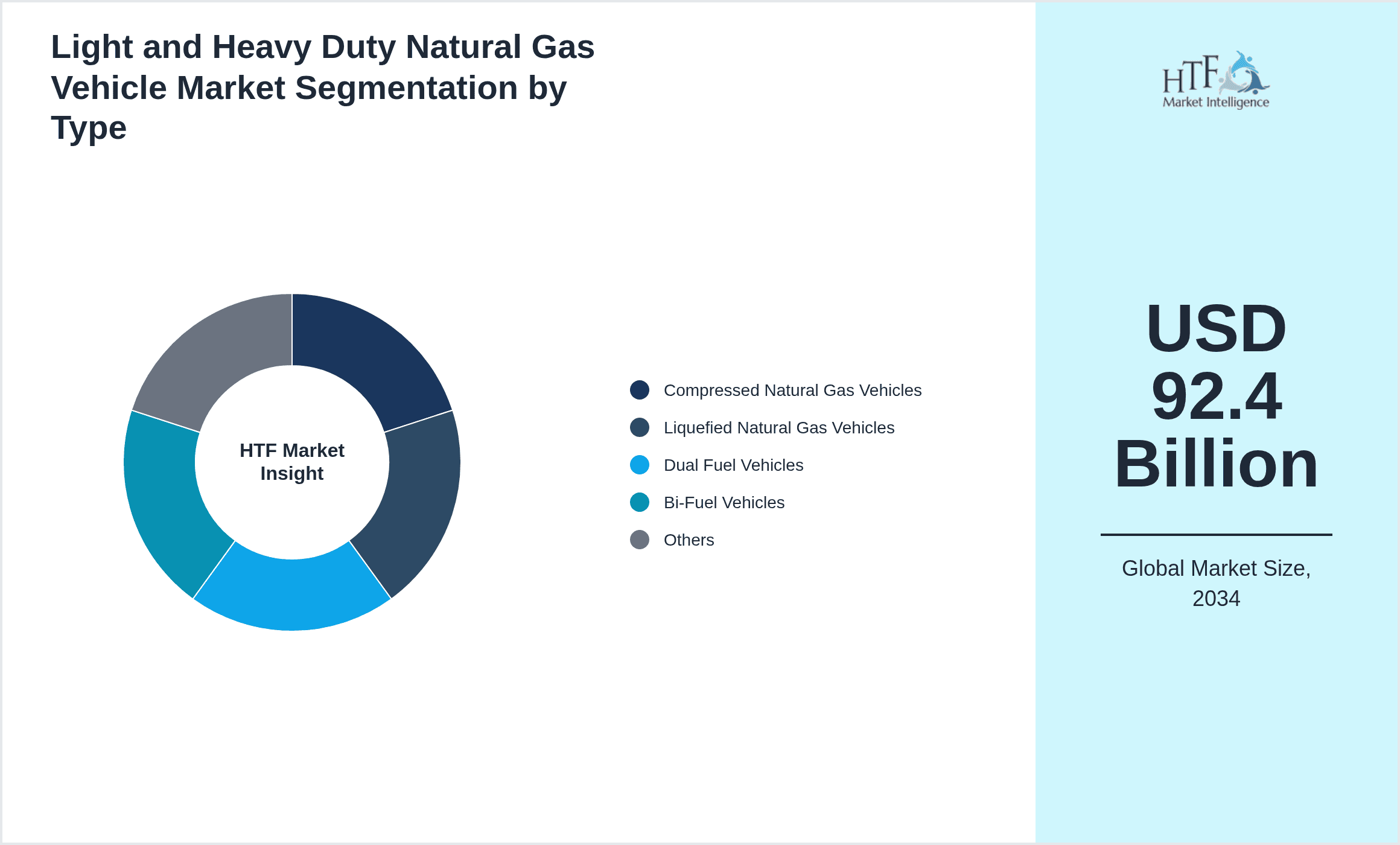

- •Key highlights of the global Light and Heavy Duty Natural Gas Vehicle market include a base market size of USD 35.8 Billion in 2025, forecasted to reach USD 92.4 Billion by 2034, reflecting a compound annual growth rate of 11.0%. North America dominates the market with a 34.2% share, while Asia-Pacific exhibits the fastest growth fueled by infrastructure expansion and increasing demand in emerging economies. Compressed Natural Gas Vehicles hold the leading product type position, whereas Liquefied Natural Gas Vehicles register the highest growth rate due to their suitability for heavy-duty and long-haul applications. Light duty and heavy duty applications serve distinct market demands, with commercial transportation and public transport sectors driving significant volume. Market consolidation, technological innovations, and supportive regulatory frameworks contribute to sustained growth momentum.

- •The global Light and Heavy Duty Natural Gas Vehicle market presents strategic value to automotive manufacturers, fuel suppliers, fleet operators, and policymakers focused on sustainability. Its growth offers opportunities for innovation in vehicle design, fuel storage solutions, and refueling infrastructure. Stakeholders benefit from government subsidies and emission regulations incentivizing cleaner fuel adoption. The market’s expansion enhances energy security by reducing dependency on crude oil and diversifies fuel sources. Enhanced public transport systems and logistics efficiency supported by natural gas vehicles contribute to economic development and environmental protection. The convergence of technological advancements, policy support, and increasing consumer awareness solidifies the market’s role in shaping the future of transportation ecosystems.

Competitive Landscape

Companies operating in the global Light and Heavy Duty Natural Gas Vehicle market employ multifaceted strategies to maintain and strengthen their market positions. Key approaches include establishing strategic partnerships with fuel infrastructure providers and technology firms to enhance vehicle performance and refueling accessibility. Global expansion into emerging markets is driven by rising demand and favorable regulations, with manufacturers tailoring product portfolios to regional requirements. Innovation focuses on improving engine efficiency, fuel storage technologies, and vehicle range. Investments in R&D and collaborations with governmental agencies facilitate compliance with evolving emission standards. Competitive pricing, product differentiation, and after-sales services are leveraged to capture fleet operators and public transport agencies. Mergers and acquisitions enable consolidation of technological capabilities and market reach. Adoption of digital solutions for fleet management and telematics further differentiates companies. These combined strategies foster sustainable growth and competitive advantage amidst increasing market competition and regulatory complexity.

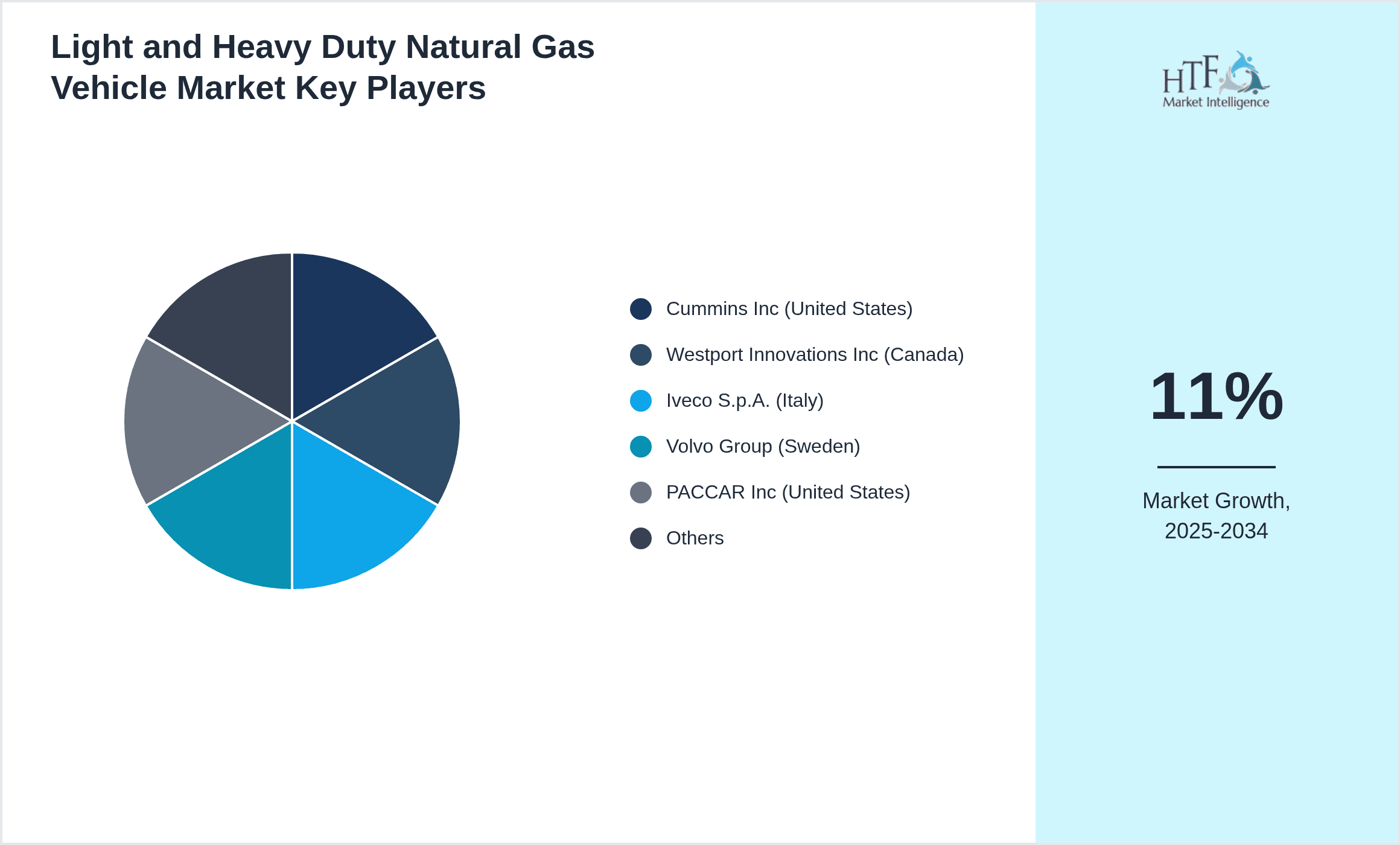

Leading Companies in Light and Heavy Duty Natural Gas Vehicle Market

- •Cummins Inc (United States)

- •Westport Innovations Inc (Canada)

- •Iveco S.p.A. (Italy)

- •Volvo Group (Sweden)

- •PACCAR Inc (United States)

- •Toyota Motor Corporation (Japan)

- •Tata Motors Limited (India)

- •Scania AB (Sweden)

- •Ford Motor Company (United States)

- •Hino Motors, Ltd. (Japan)

- •Daimler AG (Germany)

- •MAN SE (Germany)

- •FPT Industrial (Italy)

- •CNH Industrial N.V. (Netherlands)

- •Navistar International Corporation (United States)

- •FAW Jiefang Automotive Co., Ltd. (China)

- •Dongfeng Motor Corporation (China)

- •BAIC Group (China)

- •Nikola Corporation (United States)

- •Ballard Power Systems Inc. (Canada)

Market Breakdown

- •By Type

- ◦Compressed Natural Gas Vehicles

- ◦Liquefied Natural Gas Vehicles

- ◦Dual Fuel Vehicles

- ◦Bi-Fuel Vehicles

- ◦Others

- •By Application

- ◦Light Duty Vehicles

- ◦Heavy Duty Vehicles

- ◦Commercial Transportation

- ◦Public Transport

- ◦Logistics

- •By End-Use Industry

- ◦Transportation & Logistics

- ◦Public Sector & Government

- ◦Commercial Fleets

- ◦Private Consumers

- •By Distribution Channel

- ◦OEMs

- ◦Aftermarket

- ◦Fleet Operators

Growth Dynamics

The global Light and Heavy Duty Natural Gas Vehicle market experiences accelerated growth fueled by increasing environmental regulations mandating reduced emissions from transport sectors. Recent policy frameworks promoting clean energy vehicles, such as subsidies and tax incentives in North America and Europe, drive fleet conversions and new vehicle sales. Technological advancements in fuel storage systems and engine optimization improve vehicle range and performance, expanding adoption in heavy-duty logistics and public transport. For instance, Cummins Inc recently introduced next-generation LNG engines enhancing fuel efficiency and lowering operational costs. Rising fuel price volatility encourages fleet operators to switch to cost-effective natural gas vehicles, exemplified by growing LNG truck fleets in the Asia-Pacific region. Infrastructure development, including expanded CNG and LNG refueling stations, mitigates range anxiety and logistical challenges. Increasing urbanization and smart city initiatives further contribute by integrating natural gas vehicles into public transit, reducing urban pollution. These combined factors create a robust environment for sustained market expansion globally.

Market Trends

Emerging trends in the global Light and Heavy Duty Natural Gas Vehicle market include rapid adoption of liquefied natural gas vehicles tailored for heavy-duty and long-haul transportation, offering superior energy density and extended range. Integration of digital technologies such as IoT-enabled fleet management systems optimizes fuel consumption and maintenance scheduling, enhancing operational efficiency. Strategic collaborations between vehicle manufacturers and fuel infrastructure providers facilitate seamless refueling networks, notably in Europe and North America. Increased focus on bi-fuel and dual-fuel vehicle technologies provides flexibility for operators amid fluctuating fuel availability. Additionally, governments in Asia-Pacific are implementing stringent emission norms and incentivizing natural gas vehicle purchases, accelerating regional market growth. The rise of hydrogen blended with natural gas as a future fuel source marks a paradigm shift toward decarbonization. Market leaders invest heavily in R&D to innovate engine designs and after-treatment solutions, ensuring compliance and performance. These trends collectively position natural gas vehicles as a viable alternative in the evolving sustainable transport ecosystem.

Market Opportunities

Significant growth opportunities arise from expanding natural gas vehicle infrastructure in emerging economies within Asia-Pacific and Latin America, where rising urbanization and freight demand necessitate cleaner transport solutions. Increasing government initiatives offering subsidies and regulatory mandates for fleet modernization create favorable conditions for market penetration. Technological innovations targeting enhanced LNG storage and dual-fuel engine efficiency open new avenues for heavy-duty vehicle applications. The logistics sector’s growing emphasis on sustainability presents opportunities for natural gas vehicle deployment in last-mile delivery and long-haul transportation. Collaborations between OEMs and fuel suppliers facilitate integrated solutions, reducing adoption barriers. Additionally, retrofitting existing diesel fleets with natural gas systems offers a cost-effective pathway for emission reduction. The convergence of digital fleet management and natural gas vehicle adoption enhances operational transparency and efficiency, attracting commercial operators. These factors collectively provide a broad landscape for investment, product development, and market expansion globally.

Market Challenges

Challenges in the global Light and Heavy Duty Natural Gas Vehicle market include limited refueling infrastructure in key regions, particularly in Latin America and parts of the Middle East & Africa, which restricts vehicle adoption and operational flexibility. High initial costs of natural gas vehicles compared to conventional diesel or petrol counterparts pose financial barriers for fleet operators, despite lower fuel costs over the vehicle lifecycle. Technological complexities related to fuel storage, vehicle range limitations, and engine durability require continuous innovation and investment. Regulatory discrepancies across regions complicate compliance efforts for manufacturers and operators. Additionally, competition from electric vehicles and alternative fuel technologies intensifies market pressure. Recent reports highlight supply chain disruptions and raw material price volatility impacting vehicle production schedules. For example, certain OEMs have delayed product launches due to component shortages. These challenges necessitate coordinated efforts among stakeholders to enhance infrastructure, reduce costs, and streamline regulations to achieve broader market adoption.

Regulatory Framework

In the last five years, several key regulations have shaped the global Light and Heavy Duty Natural Gas Vehicle market. The European Union’s Clean Vehicle Directive mandates public procurement of low and zero-emission vehicles, boosting natural gas vehicle deployment in public transport. The United States Environmental Protection Agency introduced stricter emission standards for heavy-duty engines, encouraging cleaner fuel adoption. China’s New Energy Vehicle policy includes incentives for natural gas vehicles alongside electric alternatives, facilitating market growth. India implemented the National Bio-Energy Mission, promoting CNG adoption in commercial fleets. Additionally, international agreements like the Paris Accord have intensified commitments to reduce transport sector emissions, indirectly benefiting natural gas vehicle markets. Compliance with these regulations requires manufacturers to invest in advanced engine and after-treatment technologies. These frameworks collectively drive innovation, infrastructure development, and market expansion by setting clear emission reduction targets and supporting financial incentives for natural gas vehicle adoption worldwide.

Market Intelligence

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 35.8 Billion |

| Forecast Year Market Size | USD 92.4 Billion |

| CAGR | 11% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 10.5% |

| Scope of Report | Market is segmented by Type (Compressed Natural Gas Vehicles, Liquefied Natural Gas Vehicles, Dual Fuel Vehicles, Bi-Fuel Vehicles, Others), Application (Light Duty Vehicles, Heavy Duty Vehicles, Commercial Transportation, Public Transport, Logistics), End-Use Industry (Transportation & Logistics, Public Sector & Government, Commercial Fleets, Private Consumers), Distribution Channel (OEMs, Aftermarket, Fleet Operators) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Cummins Inc (United States), Westport Innovations Inc (Canada), Iveco S.p.A. (Italy), Volvo Group (Sweden), PACCAR Inc (United States), Toyota Motor Corporation (Japan), Tata Motors Limited (India), Scania AB (Sweden), Ford Motor Company (United States), Hino Motors, Ltd. (Japan), Daimler AG (Germany), MAN SE (Germany), FPT Industrial (Italy), CNH Industrial N.V. (Netherlands), Navistar International Corporation (United States), FAW Jiefang Automotive Co., Ltd. (China), Dongfeng Motor Corporation (China), BAIC Group (China), Nikola Corporation (United States), Ballard Power Systems Inc. (Canada) |

Global Light and Heavy Duty Natural Gas Vehicle Market Size, Growth & Revenue 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.