Global Cloud High Performance Computing Market Size, Growth & Revenue 2024-2034

Global Cloud High Performance Computing Market is segmented by Product Type (Infrastructure as a Service (IaaS), Platform as a Service (PaaS), Software as a Service (SaaS), Hybrid Cloud HPC, On-Demand HPC), Application (Scientific Research, Financial Modeling, Artificial Intelligence & Machine Learning, Data Analytics, Oil & Gas Exploration), End-Use Industry (Healthcare & Life Sciences, Financial Services, Energy & Utilities, Manufacturing & Automotive), Distribution Channel (Direct Sales, Channel Partners, Online Platforms), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The Global Cloud High Performance Computing (HPC) market represents an essential evolution in computational capability, delivering scalable and flexible HPC services through cloud platforms across multiple industries. This market includes diverse service models such as Infrastructure as a Service (IaaS), Platform as a Service (PaaS), Software as a Service (SaaS), hybrid cloud HPC, and on-demand HPC, enabling organizations to leverage powerful computing resources without heavy capital investment in physical infrastructure. Cloud HPC supports critical applications including scientific research simulations, financial risk modeling, artificial intelligence and machine learning workloads, advanced data analytics, and energy sector explorations like oil and gas. The market's boundaries encompass cloud service providers, hardware and software innovations, virtualization technologies, and integration with AI and big data frameworks, driving efficiency and lowering operational costs. With growing digital transformation, increased data volumes, and accelerating demand for compute-intensive tasks, the Global Cloud HPC market is poised for robust growth, transforming how enterprises deploy and utilize high-performance computing resources worldwide.

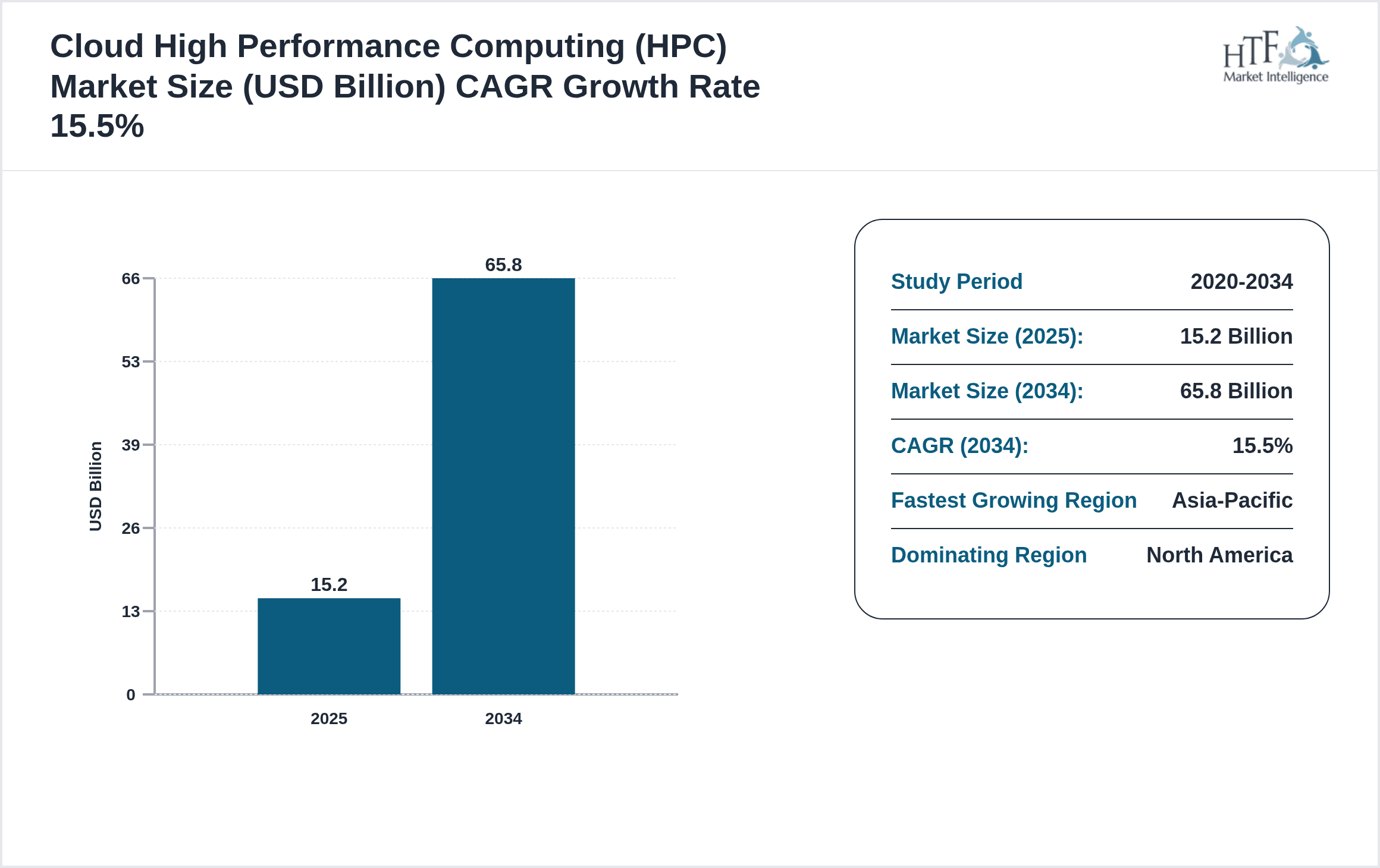

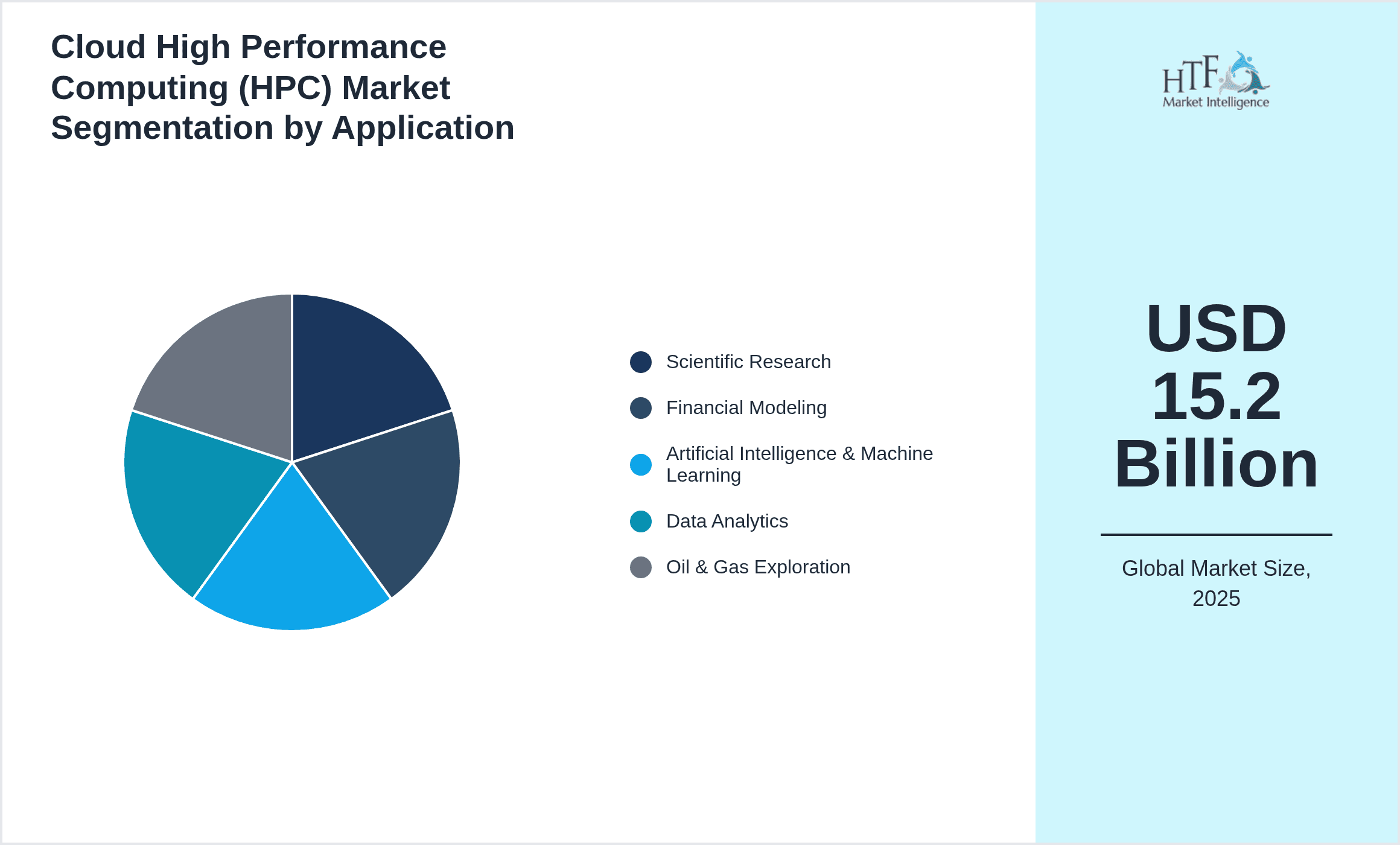

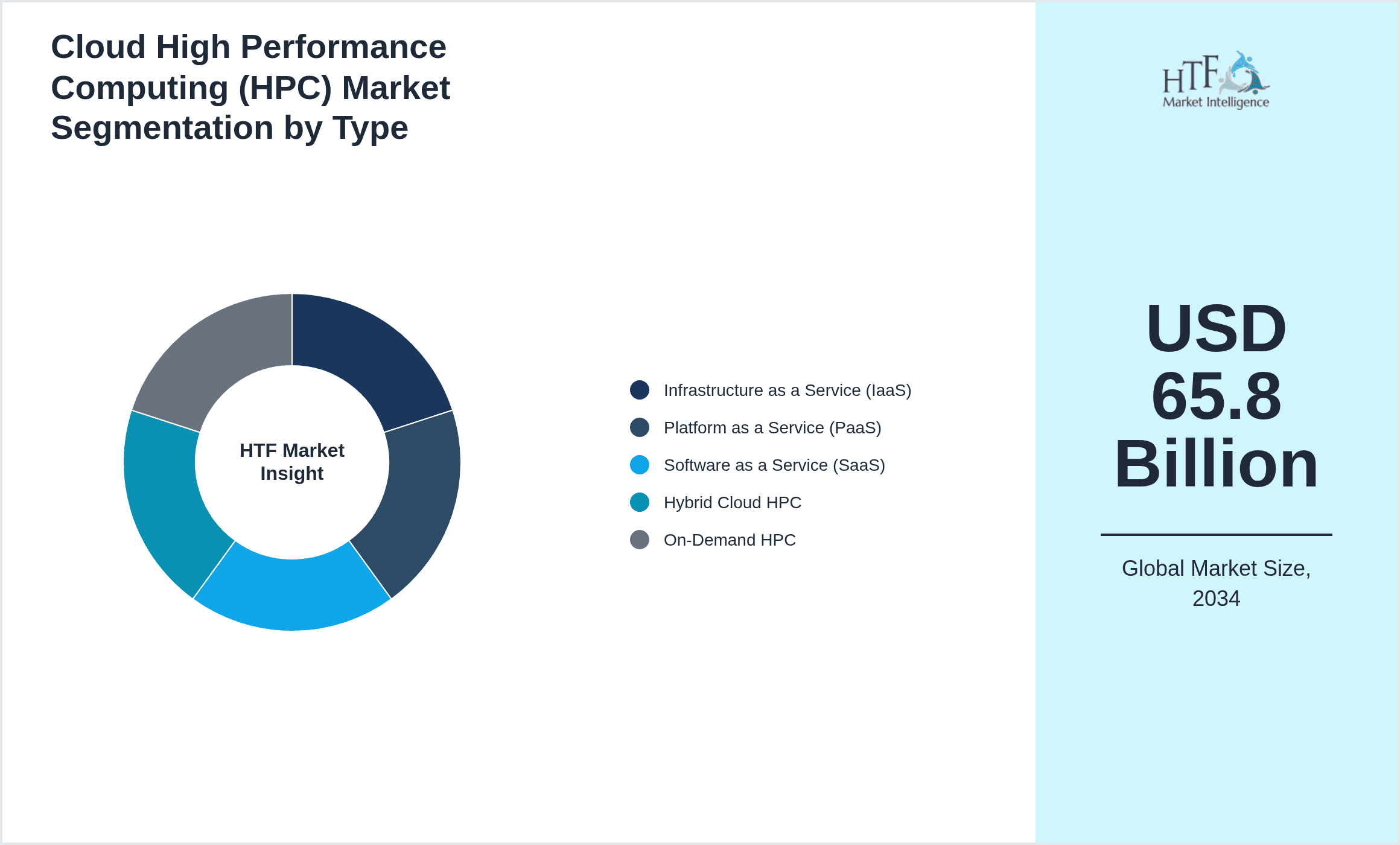

- •Key highlights of the market include a base valuation of USD 15.2 Billion in 2024 with a projected growth to USD 65.8 Billion by 2034, representing a CAGR of approximately 15.5%. The North America region currently dominates the market due to advanced cloud infrastructure and early technology adoption, while Asia-Pacific is forecasted to be the fastest growing region driven by increasing digitalization and governmental support. Infrastructure as a Service (IaaS) remains the leading product type, offering flexible and scalable compute resources, whereas Hybrid Cloud HPC is the fastest growing segment, combining on-premises and cloud resources for optimized performance. Applications such as AI and machine learning are rapidly expanding, fueling demand for high-performance cloud solutions. Market dynamics indicate strong investments in cloud HPC innovation, strategic partnerships, and expansion of data center capacities globally.

- •The value proposition of the Global Cloud HPC market lies in its ability to democratize access to supercomputing power, enabling industries and researchers to accelerate innovation and reduce time-to-insight. Cloud HPC eliminates the need for costly hardware procurement and maintenance, offering pay-as-you-go models that align with fluctuating computational needs. This strategic importance extends to sectors like pharmaceuticals, automotive, finance, and energy, where complex simulations and big data processing are critical. Stakeholders including cloud service providers, technology vendors, and end-users benefit from enhanced operational agility, reduced capital expenditure, and collaboration opportunities across geographies. The market's growth is further stimulated by advancements in AI integration, edge computing, and security protocols, establishing cloud HPC as a cornerstone of next-generation computing infrastructure globally.

Competitive Landscape

Competition in the Global Cloud High Performance Computing market is intensifying as service providers invest heavily in innovation, infrastructure expansion, and strategic partnerships to capture growing demand. Market players differentiate themselves through advanced cloud architectures offering superior scalability, low latency, and integrated AI capabilities. Competitive strategies include enhancing security features, optimizing cost-efficiency, and expanding global data centers to ensure compliance with regional regulations and to reduce latency. The rivalry is characterized by rapid technological advancements such as containerization and hybrid cloud integration, fostering collaboration through ecosystem development and open-source initiatives. Mergers and acquisitions are common to consolidate expertise and broaden service portfolios, while pricing strategies focus on pay-per-use models to attract diverse customer bases. Barriers to entry are significant due to high capital investment and technical complexity, sustaining dominance of established players and regional champions. Future trends point to increased competition around customized HPC solutions, sustainability, and edge computing integration.

Leading Companies in Cloud High Performance Computing Market

- •Amazon Web Services (United States)

- •Microsoft Corporation (United States)

- •Google LLC (United States)

- •IBM Corporation (United States)

- •NVIDIA Corporation (United States)

- •Oracle Corporation (United States)

- •Alibaba Group Holding Limited (China)

- •Hewlett Packard Enterprise (United States)

- •Fujitsu Limited (Japan)

- •Dell Technologies Inc. (United States)

- •Cisco Systems, Inc. (United States)

- •Atos SE (France)

- •Lenovo Group Limited (China)

- •Huawei Technologies Co., Ltd. (China)

- •Tencent Holdings Limited (China)

- •SAP SE (Germany)

- •Hitachi, Ltd. (Japan)

- •Rackspace Technology, Inc. (United States)

- •Equinix, Inc. (United States)

- •Google Cloud Platform (United States)

- •Oracle Cloud (United States)

- •DigitalOcean, LLC (United States)

- •OVHcloud (France)

- •Tencent Cloud (China)

- •SAP Cloud Platform (Germany)

Market Breakdown

- •By Product Type

- ◦Infrastructure as a Service (IaaS)

- ◦Platform as a Service (PaaS)

- ◦Software as a Service (SaaS)

- ◦Hybrid Cloud HPC

- ◦On-Demand HPC

- •By Application

- ◦Scientific Research

- ◦Financial Modeling

- ◦Artificial Intelligence & Machine Learning

- ◦Data Analytics

- ◦Oil & Gas Exploration

- •By End-Use Industry

- ◦Healthcare & Life Sciences

- ◦Financial Services

- ◦Energy & Utilities

- ◦Manufacturing & Automotive

- •By Distribution Channel

- ◦Direct Sales

- ◦Channel Partners

- ◦Online Platforms

Growth Dynamics

- •Rapid adoption of artificial intelligence and machine learning technologies is driving demand for cloud HPC services, as these applications require extensive compute power to process large datasets efficiently and accelerate model training cycles.

- •Advancements in cloud infrastructure and virtualization technologies enable scalable and flexible HPC offerings, reducing costs and complexity for enterprises seeking high-performance computing without capital-intensive hardware investments.

- •Growing digital transformation initiatives across industries such as healthcare, finance, and energy increase the need for real-time data analytics and simulation, further fueling cloud HPC market growth globally.

- •Government investments and support for cloud computing infrastructure and HPC research, particularly in Asia-Pacific and North America, are significant contributors to market expansion and innovation acceleration.

- •The rising shift towards hybrid cloud architectures allows organizations to combine on-premises HPC resources with cloud capabilities, enhancing performance flexibility and attracting new market segments.

- •Increasing collaboration between cloud service providers and technology vendors fosters innovation in HPC software optimization and resource management, driving broader market adoption.

- •Growing awareness of environmental sustainability motivates deployment of energy-efficient HPC cloud solutions, aligning with corporate social responsibility objectives and regulatory requirements.

Market Trends

- •The integration of AI accelerators such as GPUs and TPUs into cloud HPC platforms is enhancing computational capabilities, enabling more complex and faster processing for AI and scientific workloads.

- •Emergence of edge computing combined with cloud HPC is facilitating low-latency processing for time-sensitive applications in IoT, autonomous vehicles, and real-time analytics.

- •Providers are increasingly offering customizable HPC solutions tailored to specific industry verticals, improving efficiency and addressing unique computational challenges.

- •Sustainability initiatives are leading to adoption of green data centers powered by renewable energy sources, reducing the carbon footprint of cloud HPC operations.

- •Collaboration ecosystems between cloud providers, academia, and research institutions are growing, driving innovation and shared resource utilization in HPC projects.

- •Subscription-based pricing models and on-demand HPC resource allocation are becoming standard, enhancing customer flexibility and cost management.

- •Open-source HPC software and frameworks are gaining traction, fostering community-driven development and reducing vendor lock-in for users.

Market Opportunities

- •Expanding HPC adoption in emerging markets presents significant growth potential, especially in Asia-Pacific and Latin America where digital infrastructure is rapidly evolving and demand for cloud services is increasing.

- •Development of industry-specific HPC applications, such as genomics in healthcare and risk analytics in finance, opens new avenues for tailored cloud HPC solutions and value-added services.

- •Investment in hybrid cloud HPC models offers opportunities to capture customers seeking flexible compute solutions balancing on-premises security with cloud scalability.

- •Advancements in quantum computing integration with cloud HPC platforms could revolutionize computational capabilities, attracting high-value research and enterprise customers.

- •Partnerships and acquisitions targeting HPC software optimization and AI acceleration technologies can enhance competitive positioning and service differentiation.

- •Increasing demand for sustainable and energy-efficient HPC solutions allows providers to innovate around green technologies and attract environmentally conscious clients.

- •Expansion of multi-cloud HPC strategies enables customers to avoid vendor lock-in and optimize workloads across diverse cloud environments, creating new service offerings.

Market Challenges

- •High initial costs associated with upgrading legacy systems and integrating cloud HPC solutions pose a barrier for small and medium enterprises seeking adoption.

- •Data security and privacy concerns remain critical challenges, especially for regulated industries requiring stringent compliance with international standards and data residency laws.

- •Complexity in managing hybrid and multi-cloud HPC environments demands skilled personnel and advanced tools, limiting accessibility for organizations with limited IT resources.

- •Latency and bandwidth limitations in certain regions impact performance of cloud HPC applications requiring real-time or near-real-time processing capabilities.

- •Rapid technological evolution necessitates continuous investment in infrastructure and software upgrades, creating financial and operational challenges for providers.

- •Market fragmentation and lack of standardized HPC cloud protocols complicate interoperability and integration efforts across diverse platforms and vendors.

- •Competition from on-premises HPC solutions and specialized hardware can slow migration to cloud-based HPC for certain applications with stringent latency or security needs.

Regulatory Framework

- •Between 2019 and 2024, the introduction of data protection regulations such as the EU’s GDPR and similar frameworks in North America and Asia-Pacific have required cloud HPC providers to enhance data security and privacy compliance measures.

- •Regulatory mandates on data residency and cross-border data transfer have influenced the architecture of global HPC cloud services, pushing providers to establish localized data centers and regional compliance programs.

- •Emerging standards for cloud service certifications, including ISO/IEC 27017 and 27018, have been adopted by leading providers to assure customers of security and privacy best practices in HPC environments.

- •Environmental regulations targeting energy consumption and carbon emissions have led to increased adoption of sustainable data center practices within cloud HPC infrastructure, particularly in Europe and North America.

- •Government initiatives such as the US CHIPS Act and similar policies in Asia-Pacific support HPC research and cloud infrastructure expansion, encouraging innovation and investment in high-performance cloud technologies.

Market Intelligence

- •15th February 2025, Amazon Web Services announced the launch of its new HPC optimized instances featuring enhanced GPU capabilities and lower latency networking, targeting AI and scientific research sectors to accelerate complex simulations and machine learning workloads. This initiative aims to expand AWS’s HPC market share by providing scalable, cost-effective solutions with integrated AI acceleration and improved data throughput. The offering is expected to meet increasing customer demand for high-performance cloud computing that supports next-generation applications globally. Source: AWS Official Press Release

- •8th March 2025, Microsoft Corporation introduced Azure HPC Mesh, a platform integrating hybrid cloud HPC with edge computing to deliver seamless, low-latency compute power for industries such as automotive and healthcare. The platform combines on-premises resources with Azure cloud services, enabling flexible workload distribution and enhanced security controls. This innovation supports real-time data processing and complex simulation workloads, aligning with growing hybrid cloud adoption trends. Microsoft’s strategic focus on HPC integration is expected to strengthen its competitive positioning in the cloud HPC market worldwide. Source: Microsoft Newsroom

- •22nd April 2025, Google Cloud expanded its TPU-based HPC offerings by launching the AI Supercomputing Platform, designed to accelerate machine learning workloads across research and enterprise applications. The platform provides scalable TPU pods with optimized networking and storage, targeting sectors demanding extensive AI training capabilities. Google Cloud’s move reflects increasing investment in specialized hardware for HPC in the cloud, aiming to capture growing demand for AI-powered HPC solutions globally. This launch is a strategic step to enhance Google’s presence in the competitive cloud HPC landscape. Source: Google Cloud Blog

- •10th January 2025, IBM Corporation completed the acquisition of a leading HPC software startup specializing in workload orchestration and AI-driven resource optimization. This acquisition expands IBM’s cloud HPC portfolio by integrating advanced software tools that improve efficiency and scalability of HPC workloads on hybrid cloud environments. The strategic move is poised to bolster IBM’s market share and innovation capabilities, catering to enterprises seeking sophisticated HPC management solutions. IBM’s enhanced service offerings are expected to accelerate adoption of cloud HPC across multiple industries. Source: IBM Corporate Announcement

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 15.2 Billion |

| Forecast Year Market Size | USD 65.8 Billion |

| CAGR | 15.5% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 15.5% |

| Scope of Report | Market is segmented by Product Type (Infrastructure as a Service (IaaS), Platform as a Service (PaaS), Software as a Service (SaaS), Hybrid Cloud HPC, On-Demand HPC), Application (Scientific Research, Financial Modeling, Artificial Intelligence & Machine Learning, Data Analytics, Oil & Gas Exploration), End-Use Industry (Healthcare & Life Sciences, Financial Services, Energy & Utilities, Manufacturing & Automotive), Distribution Channel (Direct Sales, Channel Partners, Online Platforms) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Amazon Web Services (United States), Microsoft Corporation (United States), Google LLC (United States), IBM Corporation (United States), NVIDIA Corporation (United States) |

Global Cloud High Performance Computing Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.