Global Aerospace And Defense Carbon Brakes Market Size, Growth & Revenue 2025-2034

Global Aerospace And Defense Carbon Brakes Market is segmented by Product Type (Carbon-Carbon Brakes, Carbon-Silicon Carbide Brakes, Carbon-Ceramic Brakes, Hybrid Carbon Brakes, Other Composite Brakes), Application (Commercial Aircraft, Military Aircraft, Helicopters, Unmanned Aerial Vehicles (UAVs), Spacecraft), End-Use Industry (Commercial Aviation, Defense and Military, Space Exploration, Aerospace Manufacturing), Distribution Channel (Original Equipment Manufacturers (OEMs), Aftermarket Suppliers, Direct Sales), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

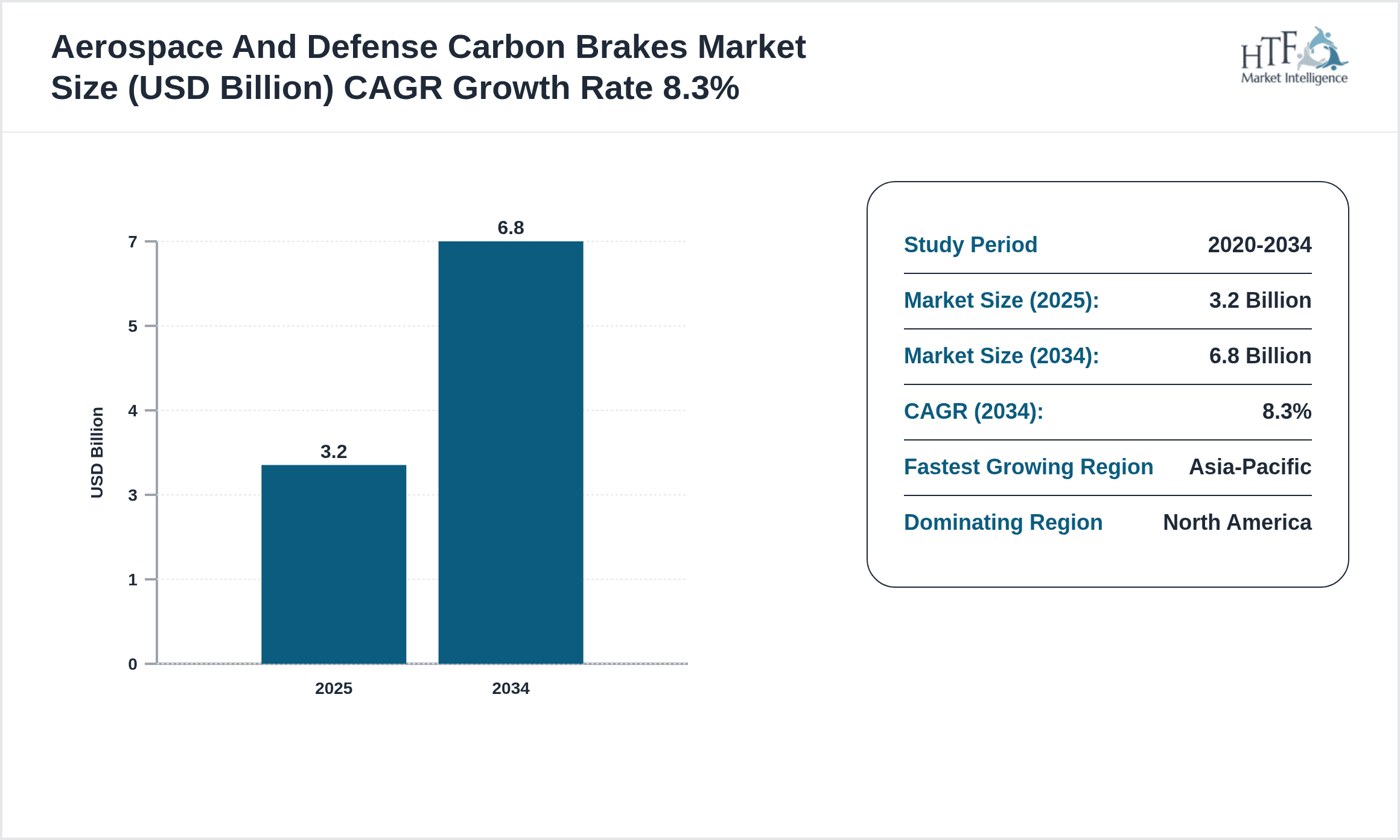

- •The global Aerospace and Defense Carbon Brakes market is a specialized segment of the braking systems industry, focusing on the design, manufacture, and integration of carbon-based composite brakes for a variety of aerospace applications. This market includes carbon-carbon, carbon-silicon carbide, and carbon-ceramic brake types, which are engineered to withstand extreme temperatures and mechanical stresses during aircraft operations. The primary applications cover commercial airliners, military fighter jets, helicopters, UAVs, and spacecraft, each requiring tailored braking systems to ensure safety and performance. The value chain comprises raw material suppliers, composite manufacturers, brake system assemblers, aerospace OEMs, and aftermarket service providers, reflecting a highly technical and regulated environment. Demand is fueled by increasing air traffic, modernization of military fleets, and the trend toward lightweight, fuel-efficient aircraft. Market growth is also supported by advancements in composite material technologies and stringent regulatory standards enforcing higher safety and environmental benchmarks across the aerospace sector. Overall, the market exhibits strong growth potential driven by innovation, sustainability efforts, and expanding aerospace production worldwide.

- •Key market highlights include a base market size of USD 3.2 Billion in 2025, growing to an estimated USD 6.8 Billion by 2034 at a CAGR of 8.3%. The Asia-Pacific region is the fastest growing market, reflecting rapid aerospace industry expansion and increased defense spending, while North America remains the dominant region due to its established aerospace manufacturing infrastructure and technological leadership. Carbon-carbon brakes retain leadership among product types due to their proven performance, but carbon-silicon carbide brakes are projected to grow fastest owing to their enhanced thermal properties and durability. Year-on-year growth averages around 8%, demonstrating sustained investment and demand in commercial and defense aviation sectors globally.

- •The aerospace and defense carbon brakes market holds significant strategic importance for aircraft manufacturers, defense contractors, and component suppliers. These braking systems contribute to flight safety, operational efficiency, and environmental sustainability by enabling weight reduction and reducing fuel consumption. Industry stakeholders leverage advancements in carbon composite technologies to differentiate product offerings and comply with evolving aerospace standards. The market also presents lucrative opportunities for investors and innovators focusing on high-performance materials and precision engineering. As air traffic and defense modernization continue, carbon brakes remain a critical enabler of next-generation aerospace capabilities, underscoring their relevance across commercial and military domains.

Competitive Landscape

The competitive environment in the global Aerospace and Defense Carbon Brakes market is characterized by the presence of a few specialized manufacturers with advanced technological capabilities and strong relationships with aerospace OEMs and defense agencies. Market dynamics include intense focus on R&D investment to develop lighter, more heat-resistant brake materials and systems that improve aircraft performance and safety. Competitive strategies often involve strategic partnerships, joint ventures, and collaborations with composite material suppliers and aerospace integrators to innovate and streamline supply chains. Mergers and acquisitions have been employed to consolidate market positions and expand geographic reach. Product differentiation is achieved through proprietary carbon composite technologies, customization for specific aircraft platforms, and integration of smart monitoring systems for predictive maintenance. Pricing strategies balance premium innovation with cost efficiency to meet rigorous budget and performance criteria. Distribution primarily occurs through OEM contracts and aftermarket service agreements. Barriers to entry are high due to stringent certification requirements, technical complexity, and established supplier networks. Regional competition varies, with North America and Europe hosting leading technology providers, while Asia-Pacific is emerging as a hub for manufacturing and innovation. Future trends indicate increasing adoption of hybrid carbon brake systems and digitalization of brake monitoring, positioning the competitive landscape for transformative evolution.

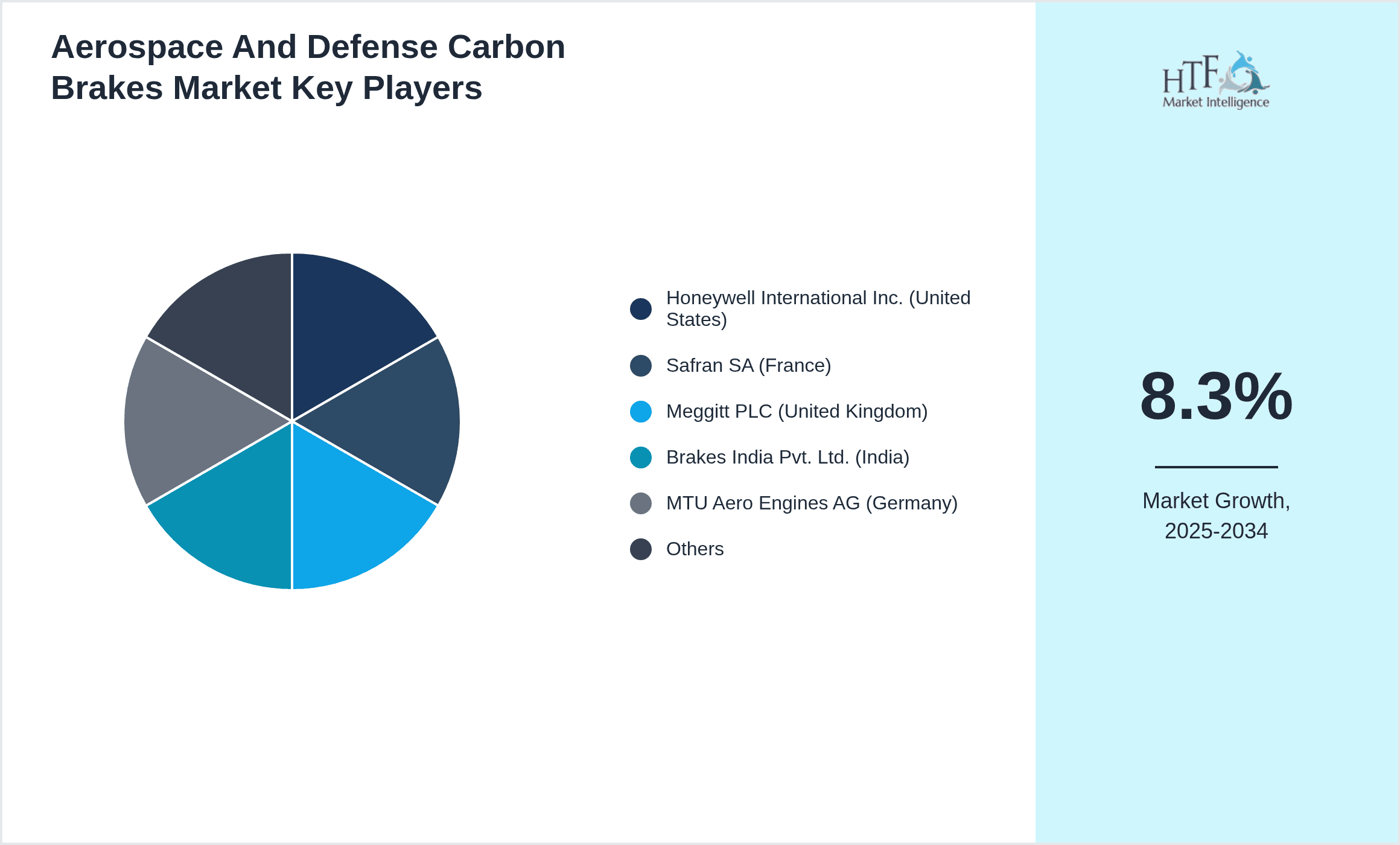

Leading Companies in Aerospace And Defense Carbon Brakes Market

- •Honeywell International Inc. (United States)

- •Safran SA (France)

- •Meggitt PLC (United Kingdom)

- •Brakes India Pvt. Ltd. (India)

- •MTU Aero Engines AG (Germany)

- •Collins Aerospace (United States)

- •Kaman Corporation (United States)

- •Zhejiang Hongli Brake Systems Co., Ltd. (China)

- •Aerospace Industrial Development Corporation (Taiwan)

- •Hankook Carbon Co., Ltd. (South Korea)

- •Avio Aero (Italy)

- •Sumitomo Electric Industries, Ltd. (Japan)

- •Tata Advanced Systems Limited (India)

- •Rolls-Royce Holdings plc (United Kingdom)

- •Parker Hannifin Corporation (United States)

- •Brembo S.p.A. (Italy)

- •Magneti Marelli S.p.A. (Italy)

- •HEG Carbon Fibers (India)

- •Friction Materials (China)

- •Ducommun Incorporated (United States)

- •Precision Castparts Corp. (United States)

- •Nexcelle LLC (United States)

- •ATE Brake Technologies GmbH (Germany)

- •GKN Aerospace (United Kingdom)

- •Miba AG (Austria)

Market Breakdown

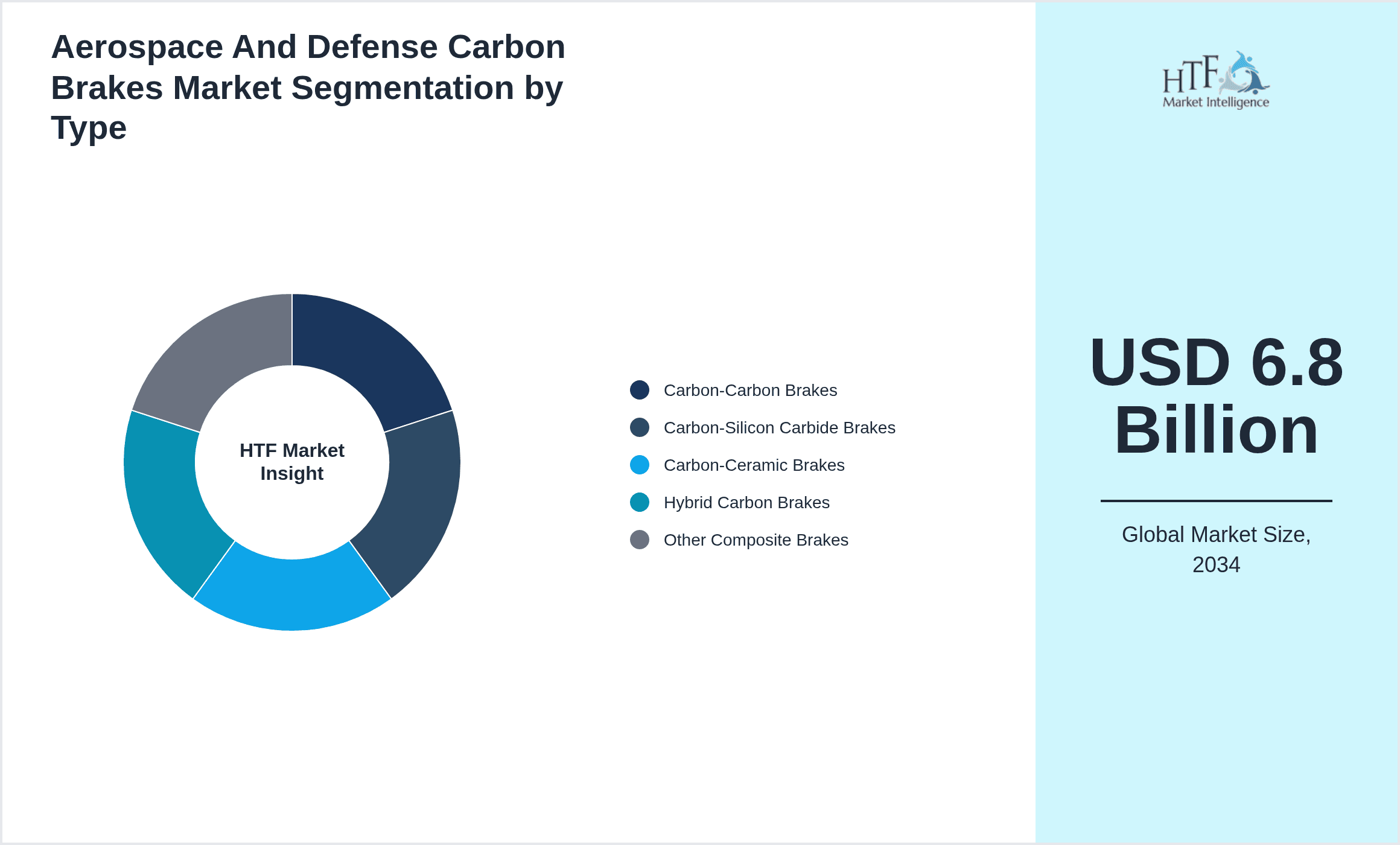

- •By Product Type

- ◦Carbon-Carbon Brakes

- ◦Carbon-Silicon Carbide Brakes

- ◦Carbon-Ceramic Brakes

- ◦Hybrid Carbon Brakes

- ◦Other Composite Brakes

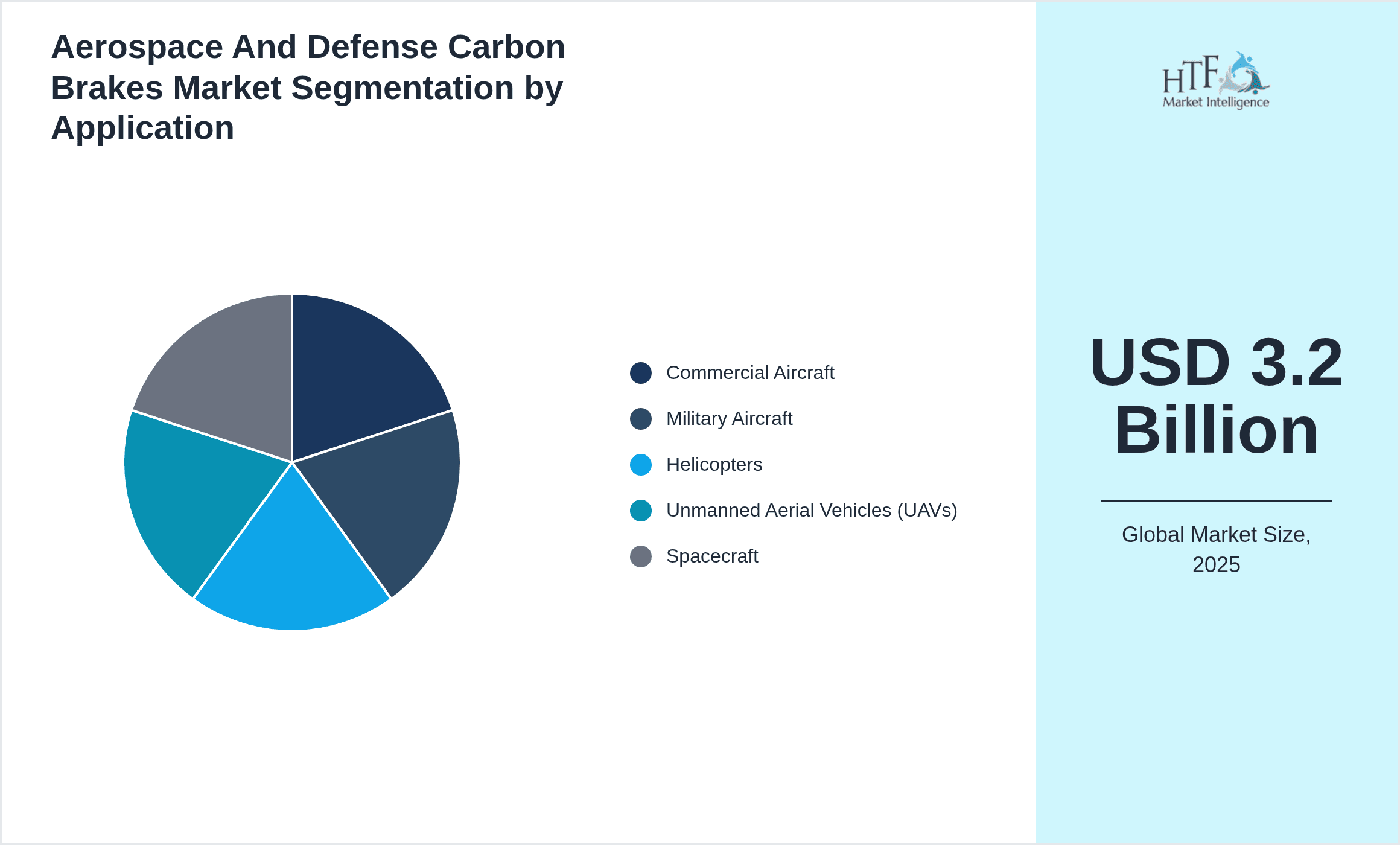

- •By Application

- ◦Commercial Aircraft

- ◦Military Aircraft

- ◦Helicopters

- ◦Unmanned Aerial Vehicles (UAVs)

- ◦Spacecraft

- •By End-Use Industry

- ◦Commercial Aviation

- ◦Defense and Military

- ◦Space Exploration

- ◦Aerospace Manufacturing

- •By Distribution Channel

- ◦Original Equipment Manufacturers (OEMs)

- ◦Aftermarket Suppliers

- ◦Direct Sales

Growth Dynamics

- •Rising global air traffic and increasing demand for fuel-efficient aircraft have propelled the adoption of lightweight carbon brake systems, which significantly reduce aircraft weight and improve fuel economy.

- •Defense sector modernization programs across key regions are increasing procurement of advanced carbon brakes to enhance performance and safety in military aircraft and helicopters.

- •Technological advancements in carbon composite materials, such as improved heat resistance and durability, are expanding the application scope of carbon brakes to new aerospace platforms including UAVs and spacecraft.

- •Stringent environmental regulations encouraging reduction of carbon emissions are driving the aerospace industry toward lighter braking solutions that contribute to overall aircraft weight reduction and lower fuel consumption.

- •Increasing investments by aerospace OEMs in research and development to innovate hybrid and multi-material carbon brakes are fueling market growth and product differentiation.

- •Growing aftermarket demand for carbon brake maintenance and refurbishment services is creating recurring revenue streams and expanding the market beyond initial equipment sales.

- •Expansion of commercial aircraft fleets in emerging economies, particularly in Asia-Pacific, is boosting regional demand for carbon brake systems and driving global market growth.

Market Trends

- •Integration of smart sensor technologies into carbon brake systems enables real-time monitoring of brake wear and performance, enhancing predictive maintenance capabilities and operational safety.

- •Adoption of hybrid carbon brake materials combining carbon-carbon and carbon-ceramic composites is gaining traction to optimize performance characteristics such as heat dissipation and weight savings.

- •Increasing collaboration between aerospace OEMs and advanced material suppliers is accelerating innovation cycles and reducing time-to-market for next-generation carbon brakes.

- •Sustainability initiatives in aerospace manufacturing are leading to the use of recyclable and environmentally friendly composite materials in carbon brake production.

- •Rising demand for UAVs in defense and commercial applications is opening new market segments for compact, high-performance carbon brake systems tailored to smaller platforms.

- •Digital twin technology adoption in aerospace component design is optimizing carbon brake system development and testing, reducing costs and improving reliability.

- •Global supply chain diversification is prompting manufacturers to establish regional production hubs for carbon brakes to mitigate risks and enhance responsiveness.

Market Opportunities

- •Emerging aerospace markets in Asia-Pacific present significant opportunities for carbon brake manufacturers to expand their footprint and capitalize on increasing aircraft deliveries.

- •Development of next-generation hypersonic and space exploration vehicles creates demand for highly advanced carbon brake systems capable of withstanding extreme conditions.

- •Investment in research focused on hybrid and multifunctional carbon composites offers potential for product innovation and competitive advantage.

- •Growing aftermarket services including maintenance, repair, and overhaul (MRO) for carbon brakes provide recurring revenue and customer retention opportunities.

- •Strategic partnerships with aerospace OEMs and defense agencies to co-develop customized carbon brake solutions can enhance market penetration and brand recognition.

- •Adoption of digitalization and smart monitoring technologies in brake systems opens avenues for value-added services and enhanced operational efficiencies.

- •Expansion into adjacent applications such as urban air mobility and electric vertical takeoff and landing (eVTOL) aircraft presents new growth frontiers.

Market Challenges

- •High manufacturing costs and complex production processes for advanced carbon composite brakes limit accessibility for cost-sensitive aerospace segments.

- •Stringent regulatory and certification requirements impose lengthy approval cycles, delaying product launches and increasing compliance costs.

- •Supply chain disruptions for specialized raw materials such as carbon fibers and silicon carbide can impact production schedules and increase lead times.

- •Technical challenges related to brake system integration with diverse aircraft platforms require extensive customization and testing efforts.

- •Competition from alternative braking technologies such as electric and regenerative braking may affect market share in the long term.

- •Limited availability of skilled workforce for advanced composite manufacturing and maintenance constrains market scalability.

- •Environmental concerns regarding disposal and recycling of composite brake materials necessitate development of sustainable end-of-life solutions.

Regulatory Framework

- •The Federal Aviation Administration (FAA) updated brake system certification standards between 2020 and 2025, imposing stricter testing protocols for carbon composite brake materials to enhance safety and performance in commercial and military aircraft.

- •European Union Aviation Safety Agency (EASA) introduced new environmental regulations during 2021-2025, encouraging lightweight brake technologies to reduce aircraft fuel consumption and emissions, impacting design and manufacturing practices.

- •International Civil Aviation Organization (ICAO) established guidelines in 2023 focused on sustainable material use and lifecycle management for aerospace components, requiring compliance from manufacturers of carbon brakes globally.

- •China's Civil Aviation Administration (CAAC) implemented region-specific mandates from 2022 to 2025 to promote adoption of advanced carbon brakes in domestic aerospace manufacturing, fostering local industry growth and technology adoption.

- •Defense procurement policies across major regions between 2020 and 2025 increasingly prioritize carbon composite brake systems for military aircraft modernization programs, necessitating compliance with stringent reliability and durability standards.

Market Intelligence

- •15th January 2025, Honeywell International Inc. launched its next-generation carbon-silicon carbide brake system designed for commercial aircraft, featuring enhanced heat dissipation and reduced weight by 15%. The product targets major aerospace OEMs aiming to improve aircraft fuel efficiency and operational safety. This innovation leverages proprietary composite manufacturing techniques and integrates smart sensors for real-time brake condition monitoring, enabling predictive maintenance and reducing downtime. Honeywell’s strategic objective is to solidify its position as a leading supplier of advanced aerospace braking technologies amid growing global air traffic. Source: Honeywell Official Press Release

- •22nd March 2025, Safran SA introduced a hybrid carbon brake solution combining carbon-carbon and carbon-ceramic composites to optimize thermal resistance and durability for military fighter jets. The product is engineered to withstand high-speed landing stresses and offers a 20% longer service life compared to traditional brakes. Safran's innovation focuses on meeting evolving defense requirements for lightweight yet robust braking systems and is expected to be integrated into upcoming aircraft platforms. The launch reinforces Safran’s commitment to innovation in aerospace safety and performance. Source: Safran Corporate News

- •5th June 2025, Meggitt PLC announced a strategic collaboration with a leading carbon fiber supplier to co-develop advanced composite materials for aerospace brake applications. This partnership aims to accelerate the development of next-generation carbon composite brakes with improved mechanical properties and sustainability characteristics. The initiative is aligned with Meggitt's vision to enhance product performance while reducing environmental impact, targeting both commercial and defense aerospace sectors globally. The companies plan joint R&D efforts and pilot production trials over the next two years. Source: Meggitt Press Release

- •Market Intelligence: Recent developments and industry insights are being monitored. For latest updates, consult official company announcements and industry publications.

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 3.2 Billion |

| Forecast Year Market Size | USD 6.8 Billion |

| CAGR | 8.3% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 8% |

| Scope of Report | Market is segmented by Product Type (Carbon-Carbon Brakes, Carbon-Silicon Carbide Brakes, Carbon-Ceramic Brakes, Hybrid Carbon Brakes, Other Composite Brakes), Application (Commercial Aircraft, Military Aircraft, Helicopters, Unmanned Aerial Vehicles (UAVs), Spacecraft), End-Use Industry (Commercial Aviation, Defense and Military, Space Exploration, Aerospace Manufacturing), Distribution Channel (Original Equipment Manufacturers (OEMs), Aftermarket Suppliers, Direct Sales) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Honeywell International Inc. (United States), Safran SA (France), Meggitt PLC (United Kingdom), Brakes India Pvt. Ltd. (India), MTU Aero Engines AG (Germany) |

Global Aerospace And Defense Carbon Brakes Market Size, Growth & Revenue 2025-2034 - Table of Contents

Research enthusiast focused on transforming data uncovering into actionable insights through data-driven decision-making.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.