Global Safety and Productivity Solutions Market Size, Growth & Revenue 2025-2034

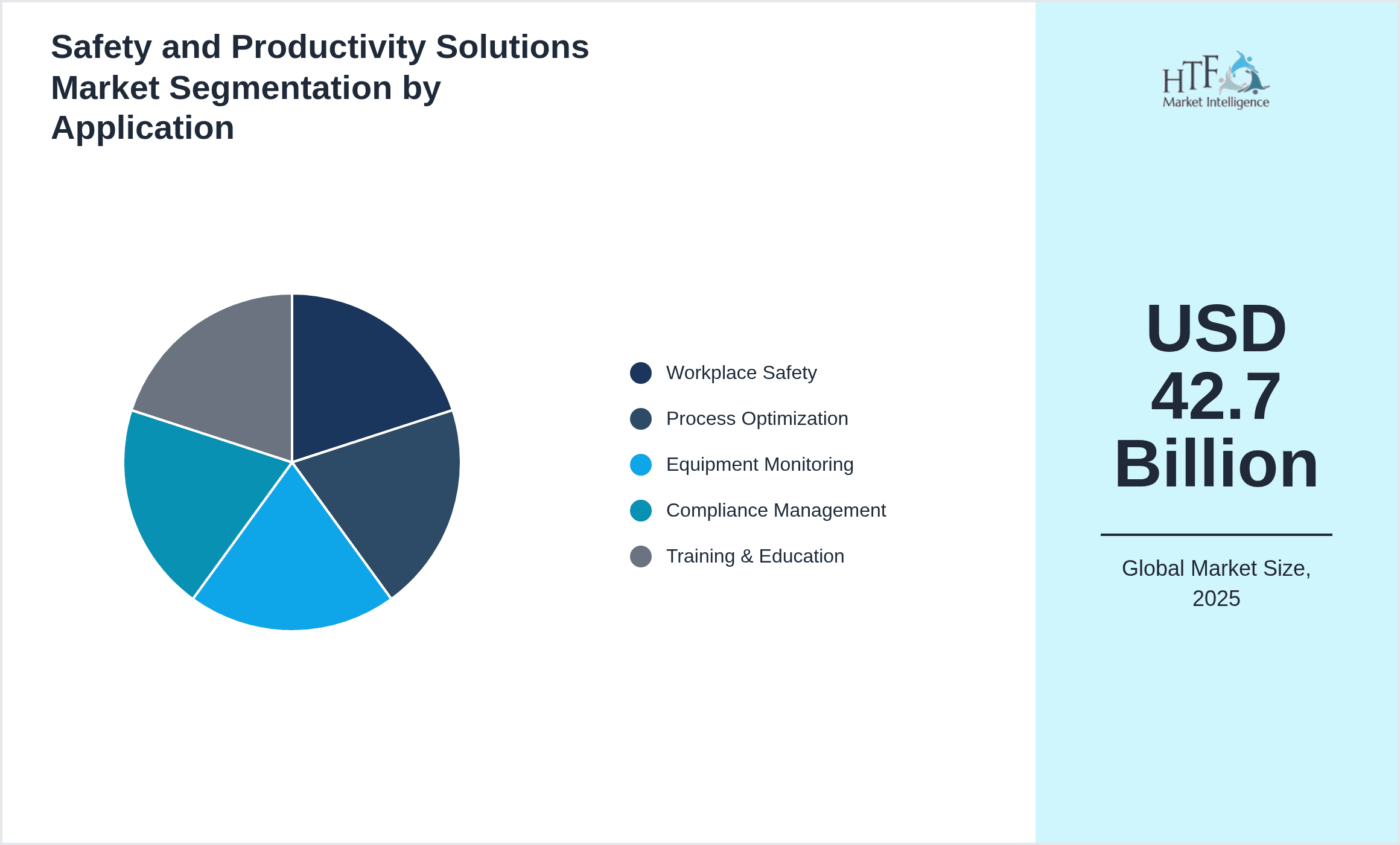

Global Safety and Productivity Solutions Market is segmented by Product Type (Software Solutions, Hardware Devices, Services, Integrated Systems, Analytics Platforms), Application (Workplace Safety, Process Optimization, Equipment Monitoring, Compliance Management, Training & Education), End-Use Industry (Manufacturing, Construction, Oil & Gas, Transportation), Distribution Channel (Direct Sales, Channel Partners, Online Platforms), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global Safety and Productivity Solutions market encompasses a broad spectrum of technologies and services aimed at enhancing workplace safety and operational efficiency across multiple industries worldwide. It includes software solutions that enable real-time risk assessment, compliance management, and process optimization, as well as hardware devices such as sensors, wearables, and automated safety equipment that monitor environmental and human factors to prevent accidents. Integrated systems combining hardware and software components provide comprehensive safety management frameworks, while analytics platforms leverage AI and machine learning to forecast potential hazards and optimize productivity. The market serves diverse applications, including workplace safety, equipment monitoring, compliance adherence, process optimization, and employee training. Key end-use industries include manufacturing, construction, oil & gas, transportation, and healthcare. Increasing regulatory mandates, technological advancements, and growing organizational focus on risk mitigation and efficiency improvements drive market growth. The rising adoption of Industry 4.0 and IoT technologies further accelerates solution deployment, enabling proactive safety management and enhanced productivity. The competitive landscape is marked by innovation, strategic partnerships, and expanding product portfolios, positioning the market for robust growth through 2034.

- •Key highlights of the market include a base size of USD 42.7 Billion in 2025, with projections reaching USD 95.4 Billion by 2034, reflecting a strong CAGR of 8.9%. North America dominates the global market due to mature regulatory frameworks and high technology adoption, while Asia-Pacific is the fastest-growing region driven by rapid industrialization and increasing safety awareness. Software solutions currently lead product segments, with analytics platforms exhibiting the fastest growth due to their capability to transform safety data into actionable insights. Market drivers include stringent safety regulations, rising workplace accidents, and the growing need for operational efficiency. Challenges such as high implementation costs and integration complexities persist, yet opportunities abound in emerging markets and through technological innovations like AI-powered predictive analytics.

- •The value proposition of Safety and Productivity Solutions lies in their ability to significantly reduce workplace accidents, ensure regulatory compliance, and optimize operational workflows, thereby delivering both safety and economic benefits. These solutions provide strategic importance to industries by minimizing downtime, enhancing employee well-being, and enabling data-driven decision-making. Stakeholders including manufacturers, service providers, and regulators stand to benefit from the widespread adoption of these technologies, which foster safer work environments and improved productivity. The market’s trajectory is influenced by continuous innovation, growing digital transformation initiatives, and evolving regulatory landscapes, making Safety and Productivity Solutions critical to future industrial and commercial success.

Competitive Landscape

The global Safety and Productivity Solutions market is characterized by intense competition among established multinational corporations and innovative technology providers. Market dynamics are shaped by firms leveraging advanced technologies such as IoT, AI, and machine learning to develop differentiated safety and productivity offerings. Competitive strategies include product innovation, strategic partnerships, mergers and acquisitions, and geographic expansion to capture emerging market opportunities. Companies focus on enhancing solution interoperability, user experience, and integration capabilities to address complex safety challenges across diverse industries. Pricing strategies balance cost competitiveness with value-added features, while distribution channels expand through digital platforms and direct enterprise engagements. Market positioning hinges on technological leadership, regulatory compliance expertise, and service quality. Barriers to entry include high R&D costs and stringent certification requirements. Regional competition varies, with North America and Europe hosting dominant players, while Asia-Pacific witnesses rapid growth of local innovators. Future trends suggest increased collaboration within ecosystems and adoption of cloud-based safety management platforms to maintain competitive advantage.

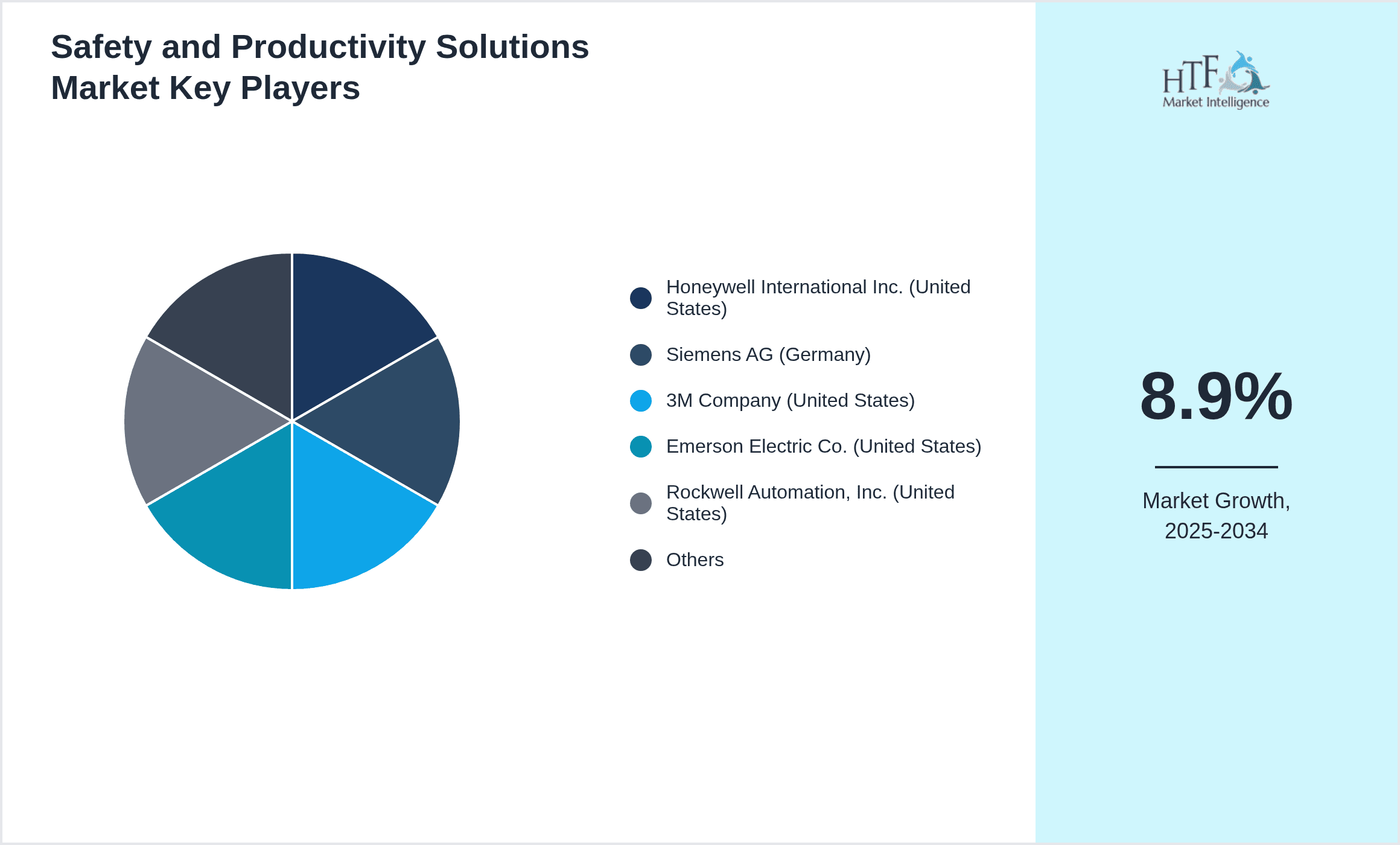

Key Players in Safety and Productivity Solutions Market

- •Honeywell International Inc. (United States)

- •Siemens AG (Germany)

- •3M Company (United States)

- •Emerson Electric Co. (United States)

- •Rockwell Automation, Inc. (United States)

- •Schneider Electric SE (France)

- •Bosch Sicherheitssysteme GmbH (Germany)

- •Johnson Controls International plc (Ireland)

- •ABB Ltd (Switzerland)

- •Honeywell Analytics (United States)

- •Fluke Corporation (United States)

- •Draegerwerk AG & Co. KGaA (Germany)

- •Fanuc Corporation (Japan)

- •General Electric Company (United States)

- •Mitsubishi Electric Corporation (Japan)

- •Pilz GmbH & Co. KG (Germany)

- •Siemens Healthineers AG (Germany)

- •Trimble Inc. (United States)

- •Yokogawa Electric Corporation (Japan)

- •Hexagon AB (Sweden)

- •Emerson Process Management (United States)

- •Bentley Systems, Incorporated (United States)

- •Zebra Technologies Corporation (United States)

- •Honeywell Process Solutions (United States)

- •Siemens Digital Industries Software (Germany)

Market Breakdown

- •By Product Type

- ◦Software Solutions

- ◦Hardware Devices

- ◦Services

- ◦Integrated Systems

- ◦Analytics Platforms

- •By Application

- ◦Workplace Safety

- ◦Process Optimization

- ◦Equipment Monitoring

- ◦Compliance Management

- ◦Training & Education

- •By End-Use Industry

- ◦Manufacturing

- ◦Construction

- ◦Oil & Gas

- ◦Transportation

- •By Distribution Channel

- ◦Direct Sales

- ◦Channel Partners

- ◦Online Platforms

Growth Dynamics

The global Safety and Productivity Solutions market growth is primarily driven by increasingly stringent workplace safety regulations worldwide, compelling organizations to adopt advanced safety technologies. The integration of IoT and AI in these solutions enables real-time hazard detection and predictive analytics, significantly reducing workplace incidents. Additionally, rising industrial automation and digital transformation initiatives create demand for comprehensive productivity solutions that enhance operational efficiency. Growing awareness of employee well-being and the financial impact of accidents further incentivizes investments in safety technologies. Furthermore, the expansion of end-use industries such as manufacturing and construction in emerging economies fuels market growth, supported by government initiatives promoting industrial safety standards. These dynamics create a favorable environment for innovation and adoption of integrated safety management platforms globally.

Market Trends

A significant trend in the Safety and Productivity Solutions market is the increasing adoption of cloud-based safety management systems that offer scalability, remote access, and real-time data analytics. Companies are investing in wearable safety devices equipped with sensors to monitor worker health and environmental conditions, enhancing proactive hazard prevention. The convergence of AI and machine learning technologies facilitates advanced predictive maintenance and risk assessment capabilities. Sustainability and environmental safety are becoming integral to solution design, aligning with global ESG initiatives. Collaborative platforms enabling workforce training and compliance tracking are gaining prominence, fostering a culture of safety and continuous improvement across industries.

Market Opportunities

Opportunities in the Safety and Productivity Solutions market arise from untapped emerging markets where industrialization is accelerating, and safety infrastructure is developing. Advancements in AI-driven analytics and IoT connectivity offer avenues for innovative product development that can deliver predictive and prescriptive safety interventions. Expansion into small and medium-sized enterprises presents growth potential due to increasing awareness and affordability of safety solutions. Strategic partnerships between technology providers and industry players can enhance solution customization and adoption. Additionally, the growing emphasis on remote monitoring and workforce safety post-pandemic creates demand for contactless and automated safety management tools.

Market Challenges

The market faces challenges including high initial investment costs for advanced safety and productivity solutions, which can deter small and medium enterprises from adoption. Integration complexities with existing legacy systems pose operational hurdles and require substantial customization. Data privacy and cybersecurity concerns emerge due to increased connectivity of safety devices and platforms. Regulatory diversity across regions complicates compliance and solution standardization. Furthermore, lack of skilled personnel to manage and interpret sophisticated safety technologies limits effective deployment. These challenges necessitate focused strategies to enhance affordability, interoperability, and workforce training to sustain market growth.

Regulatory Framework

Between 2020 and 2025, key regulations such as the Occupational Safety and Health Administration (OSHA) updates in the United States mandated stricter workplace safety protocols, driving solution adoption. The European Union’s Machinery Directive revisions enforced rigorous compliance for industrial equipment safety, impacting manufacturers and solution developers. Asia-Pacific countries implemented new industrial safety standards aligned with international norms, enhancing market potential. Environmental regulations including REACH and RoHS influenced hardware device manufacturing to ensure sustainability compliance. Government incentives and certification requirements in major regions facilitated technology integration, compelling enterprises to adopt certified safety and productivity solutions to meet regulatory expectations and avoid penalties.

Market Intelligence

- •15th March 2025, Honeywell International Inc. launched an innovative AI-powered safety analytics platform targeting the manufacturing sector, designed to integrate with existing IoT infrastructures and provide predictive risk assessments. This solution enables real-time monitoring of workplace hazards and automates compliance reporting, significantly reducing incident response times. Honeywell aims to expand its footprint in emerging markets by offering scalable subscription models. This launch positions the company at the forefront of digital transformation in safety management, expected to accelerate adoption globally and drive substantial revenue growth. Source: Honeywell Official Press Release.

- •22nd July 2025, Siemens AG introduced a next-generation integrated safety and productivity system that combines hardware sensors with cloud-based software analytics to optimize industrial workflows while ensuring compliance with global safety standards. This system supports remote monitoring and predictive maintenance, reducing downtime and enhancing worker safety. Siemens is targeting key industrial segments including oil & gas, automotive, and construction. The innovation reflects Siemens' strategy to leverage digitalization for competitive advantage in the global safety market. Source: Siemens Corporate Communications.

- •10th October 2025, Schneider Electric SE announced a strategic partnership with a leading AI startup to co-develop advanced safety solutions incorporating machine learning algorithms for real-time hazard detection and automated corrective actions. This collaboration aims to enhance Schneider Electric's existing portfolio by integrating cutting-edge analytics capabilities, enabling clients to achieve higher safety and productivity standards. The partnership is expected to accelerate innovation cycles and open new market opportunities in Asia-Pacific and Europe. Source: Schneider Electric Press Release.

- •5th December 2024, Rockwell Automation, Inc. completed the acquisition of a niche safety software provider specializing in compliance management and workforce training platforms. This acquisition expands Rockwell’s digital offerings and strengthens its position in the integrated safety solutions market. The combined capabilities facilitate end-to-end safety lifecycle management, from risk assessment to employee certification. This strategic move is anticipated to drive market consolidation and enhance Rockwell’s competitive edge amid growing demand for comprehensive safety solutions. Source: Rockwell Automation Investor Relations.

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 42.7 Billion |

| Forecast Year Market Size | USD 95.4 Billion |

| CAGR | 8.9% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 8.5% |

| Scope of Report | Market is segmented by Product Type (Software Solutions, Hardware Devices, Services, Integrated Systems, Analytics Platforms), Application (Workplace Safety, Process Optimization, Equipment Monitoring, Compliance Management, Training & Education), End-Use Industry (Manufacturing, Construction, Oil & Gas, Transportation), Distribution Channel (Direct Sales, Channel Partners, Online Platforms) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Honeywell International Inc. (United States), Siemens AG (Germany), 3M Company (United States), Emerson Electric Co. (United States), Rockwell Automation, Inc. (United States), Schneider Electric SE (France), Bosch Sicherheitssysteme GmbH (Germany), Johnson Controls International plc (Ireland), ABB Ltd (Switzerland), Honeywell Analytics (United States), Fluke Corporation (United States), Draegerwerk AG & Co. KGaA (Germany), Fanuc Corporation (Japan), General Electric Company (United States), Mitsubishi Electric Corporation (Japan), Pilz GmbH & Co. KG (Germany), Siemens Healthineers AG (Germany), Trimble Inc. (United States), Yokogawa Electric Corporation (Japan), Hexagon AB (Sweden), Emerson Process Management (United States), Bentley Systems, Incorporated (United States), Zebra Technologies Corporation (United States), Honeywell Process Solutions (United States), Siemens Digital Industries Software (Germany) |

Global Safety and Productivity Solutions Market Size, Growth & Revenue 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.