Asia-Pacific Software Defined Perimeter Market Size, Growth & Revenue 2024-2034

Asia-Pacific Software Defined Perimeter Market is segmented by Product Type (Gateway-based SDP, Client-based SDP, Hybrid SDP, Zero Trust Network Access, Software-only SDP), Application (Enterprise Security, Cloud Security, Data Center Security, Remote Access, Network Security), End-Use Industry (IT & Telecommunications, BFSI, Healthcare, Government & Defense), Distribution Channel (Direct Sales, Channel Partners, Managed Security Service Providers), and Geography (Japan, China, Southeast Asia, India, Australia, South Korea, Others)

Pricing

Report Overview

Executive Summary

- •The Asia-Pacific Software Defined Perimeter (SDP) market represents a critical evolution in cybersecurity, focused on creating secure, identity-centric network boundaries that dynamically adapt to user context and device posture. It encompasses a range of SDP solutions including gateway-based, client-based, hybrid, zero trust network access, and software-only implementations deployed across enterprises to safeguard data centers, cloud environments, remote access points, and network layers. Driven by heightened cyber threats, digital transformation, and stringent data privacy regulations, the market serves diverse applications like enterprise security, cloud security, data center protection, remote user access, and network security in sectors such as IT, BFSI, healthcare, and government. The market scope includes software platforms, hardware gateways, and managed services facilitating seamless, scalable, and secure connectivity. Increasing adoption of zero trust frameworks, cloud migration, and government initiatives for cyber resilience anchor the market's robust growth trajectory, positioning Asia-Pacific as a dynamic hub of cybersecurity innovation and investment.

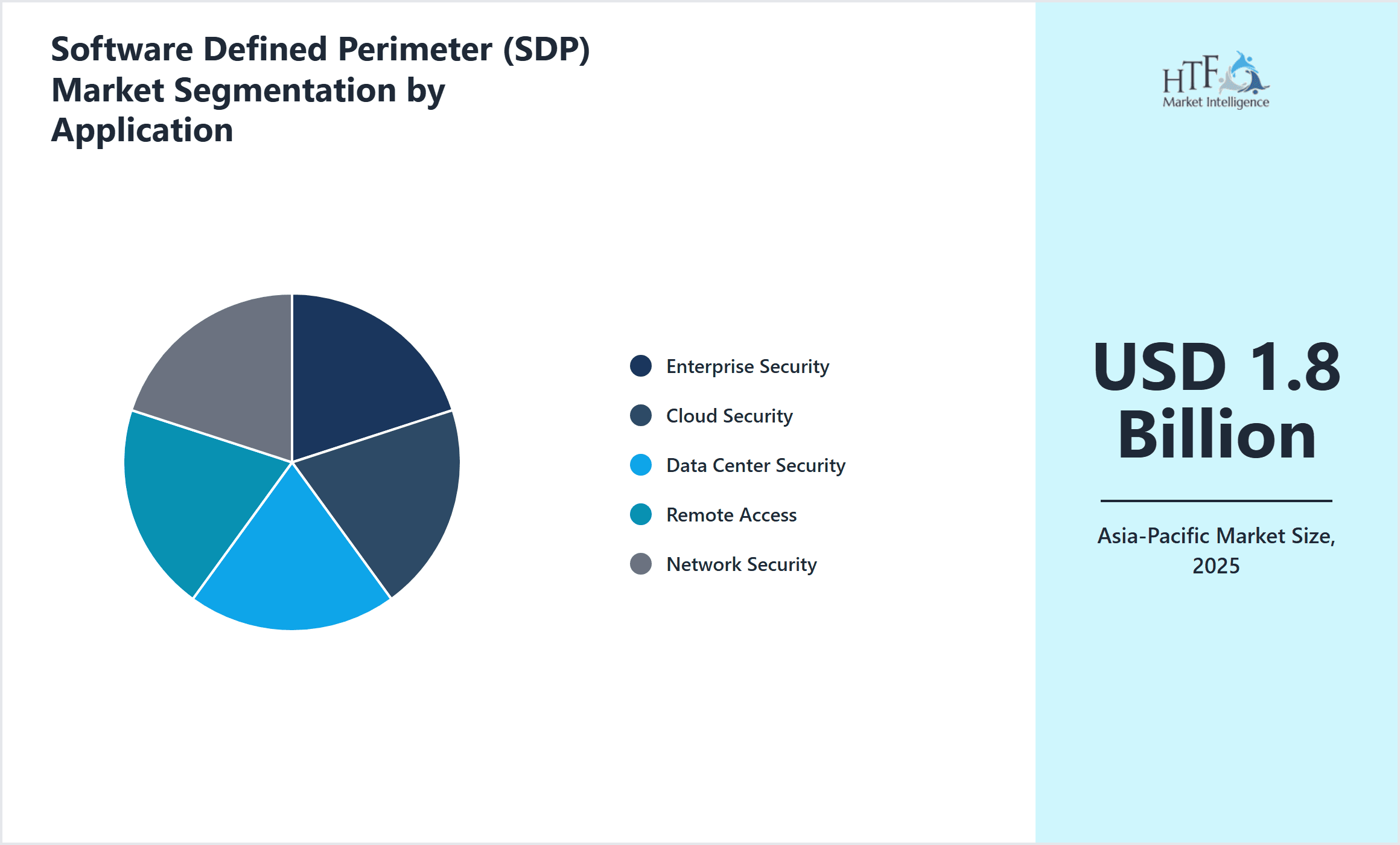

- •Key highlights of the Asia-Pacific SDP market include a forecasted compound annual growth rate (CAGR) of 20.1% from 2024 to 2034, with market size expected to expand from USD 1.8 billion in 2024 to USD 11.4 billion by 2034. China dominates the regional market share owing to its advanced digital infrastructure and stringent cybersecurity mandates, while India exhibits the fastest growth driven by rapid digital adoption and increasing cyber threat awareness. Gateway-based SDP solutions currently lead product type adoption, but zero trust network access models are emerging rapidly due to their enhanced security postures. The enterprise security application segment holds the largest share, followed closely by cloud security, reflecting shifting enterprise priorities towards cloud-native architectures and remote work security.

- •The Asia-Pacific SDP market offers strategic value to cybersecurity vendors, enterprises, cloud service providers, and governmental bodies by enabling a transformative approach to network security that aligns with zero trust principles. It empowers organizations to protect critical assets from sophisticated cyberattacks while ensuring compliance with evolving data protection laws across the region. Investment in SDP technologies enhances operational agility, reduces attack surfaces, and supports hybrid and multi-cloud environments, thereby fostering digital resilience. Stakeholders benefit from increased market opportunities driven by collaborative innovation, regulatory compliance demands, and the surge in cloud adoption, positioning SDP as a cornerstone technology in the region's cybersecurity ecosystem.

Competitive Landscape

The Asia-Pacific Software Defined Perimeter market is characterized by intense competition among established global cybersecurity vendors and emerging regional players. Market participants differentiate themselves through continuous innovation in zero trust architectures, integration capabilities with cloud platforms, and advanced authentication mechanisms. Strategic investments in research and development, coupled with partnerships and alliances, enable companies to enhance their product portfolios and expand regional footprints. Competitive dynamics are further influenced by pricing strategies tailored to diverse customer segments and the ability to provide managed security services. Regional nuances such as local compliance requirements and technological maturity shape market positioning. Mergers and acquisitions remain a significant trend to consolidate market share and acquire complementary technologies, while the focus on scalable, user-centric, and AI-driven SDP solutions continues to drive competitive differentiation and future market trajectories.

Key Players in Software Defined Perimeter Market

- •Cisco Systems, Inc. (United States)

- •Palo Alto Networks, Inc. (United States)

- •Zscaler, Inc. (United States)

- •Akamai Technologies, Inc. (United States)

- •Fortinet, Inc. (United States)

- •IBM Corporation (United States)

- •Nokia Corporation (Finland)

- •Check Point Software Technologies Ltd. (Israel)

- •Cloudflare, Inc. (United States)

- •Symantec Corporation (United States)

- •Huawei Technologies Co., Ltd. (China)

- •Tenable Holdings, Inc. (United States)

- •Juniper Networks, Inc. (United States)

- •Citrix Systems, Inc. (United States)

- •VMware, Inc. (United States)

- •Okta, Inc. (United States)

- •SonicWall Inc. (United States)

- •Dell Technologies Inc. (United States)

- •Radware Ltd. (Israel)

- •Netskope, Inc. (United States)

- •A10 Networks, Inc. (United States)

- •Barracuda Networks, Inc. (United States)

- •Trend Micro Incorporated (Japan)

- •F5 Networks, Inc. (United States)

- •CyberArk Software Ltd. (Israel)

Market Breakdown

- •By Product Type

- ◦Gateway-based SDP

- ◦Client-based SDP

- ◦Hybrid SDP

- ◦Zero Trust Network Access

- ◦Software-only SDP

- •By Application

- ◦Enterprise Security

- ◦Cloud Security

- ◦Data Center Security

- ◦Remote Access

- ◦Network Security

- •By End-Use Industry

- ◦IT & Telecommunications

- ◦BFSI

- ◦Healthcare

- ◦Government & Defense

- •By Distribution Channel

- ◦Direct Sales

- ◦Channel Partners

- ◦Managed Security Service Providers

Growth Dynamics

- •Rising cyber threats and sophisticated attack vectors across Asia-Pacific enterprises are propelling the adoption of SDP solutions, as organizations seek enhanced perimeter security aligned with zero trust principles. The increasing migration to cloud services and hybrid IT environments necessitates dynamic, identity-based access controls, driving market demand.

- •Government initiatives and regulatory mandates across countries like China, India, and Australia to strengthen cybersecurity frameworks are fostering investments in SDP technologies. Policies emphasizing data privacy, critical infrastructure protection, and secure remote access are key enablers of market growth.

- •Advancements in AI and machine learning are being integrated into SDP platforms for real-time threat detection and adaptive security enforcement, enhancing solution efficacy and attracting enterprise adoption.

- •The rise of remote work culture triggered by the COVID-19 pandemic has accelerated the need for secure, scalable remote access solutions provided by SDP architectures, significantly expanding the addressable market.

- •Strategic collaborations between cybersecurity vendors and cloud service providers enable seamless integration of SDP solutions, boosting customer confidence and accelerating deployment in complex IT environments.

- •Cost optimization and operational efficiency gains through software-defined, centrally managed security models motivate enterprises to replace traditional perimeter controls with SDP frameworks.

- •Increasing awareness and training about zero trust security models among IT decision-makers in Asia-Pacific contribute to growing interest and procurement of SDP solutions.

Market Trends

- •A significant trend is the adoption of zero trust network access (ZTNA) within SDP deployments, emphasizing least-privilege access and continuous verification, which enhances security posture against insider and external threats.

- •Integration of SDP with cloud-native security platforms and containerized environments is gaining traction, enabling granular access control in microservices architectures and multi-cloud deployments.

- •Emergence of AI-powered behavioral analytics within SDP solutions is enabling proactive threat detection and automated response, reducing reliance on manual security operations.

- •Increasing preference for software-only SDP models that offer flexibility and ease of deployment in diverse IT environments is reshaping vendor product strategies.

- •Collaborations between telecom operators and cybersecurity firms to embed SDP capabilities in 5G networks are emerging, supporting secure and low-latency connectivity for IoT and edge computing use cases.

- •The rapid growth of managed security service providers (MSSPs) offering SDP-as-a-service reflects a shift toward subscription-based, scalable security consumption models in the region.

- •Focus on compliance-driven SDP deployments in regulated industries like BFSI and healthcare is increasing, driven by stringent data protection and privacy laws across Asia-Pacific countries.

Market Opportunities

- •Expanding digital transformation initiatives in emerging Asia-Pacific economies present vast opportunities for SDP vendors to cater to SMBs and mid-market enterprises seeking cost-effective, scalable security solutions.

- •The growing adoption of hybrid cloud and multi-cloud strategies across enterprises creates demand for interoperable SDP solutions that can unify security policies across heterogeneous environments.

- •Increasing investments in critical infrastructure protection by governments offer prospects for specialized SDP solutions tailored for sectors like energy, transportation, and utilities.

- •Rising demand for secure remote access in educational institutions and public sector organizations fuels market expansion, particularly with the proliferation of digital learning platforms.

- •Integration of SDP with emerging technologies such as edge computing and IoT security opens new avenues for product innovation and market penetration.

- •Strategic partnerships and alliances between SDP vendors and cloud service providers can accelerate market reach and solution adoption across the Asia-Pacific region.

- •Customization and localization of SDP offerings to address region-specific regulatory and language requirements can differentiate vendors and enhance market acceptance.

Market Challenges

- •Lack of awareness and understanding of SDP technologies among certain enterprise segments in Asia-Pacific hampers broader adoption and slows market penetration.

- •Complexity in integrating SDP solutions with legacy IT infrastructure and diverse cloud environments poses technical challenges for organizations.

- •High initial deployment costs and perceived operational overheads deter small and medium enterprises from investing in SDP frameworks despite long-term benefits.

- •Shortage of skilled cybersecurity professionals trained in zero trust and SDP architectures limits effective implementation and ongoing management.

- •Regulatory fragmentation and evolving data privacy laws across Asia-Pacific countries create compliance complexities for multinational enterprises deploying SDP solutions.

- •Resistance to change from traditional perimeter security models to software-defined approaches among IT leadership slows transformation initiatives.

- •Security concerns related to SDP vendor lock-in and interoperability with other security products may impact customer confidence and procurement decisions.

Regulatory Framework

- •Between 2019 and 2024, several Asia-Pacific countries implemented stringent data protection regulations requiring enhanced network security controls; for instance, China’s Cybersecurity Law (2017, enforced through 2019-2024) mandates critical infrastructure operators to deploy advanced access controls, benefiting SDP adoption.

- •India’s Personal Data Protection Bill, introduced in 2019 and evolving through 2024, emphasizes the need for robust data access frameworks, incentivizing enterprises to adopt zero trust and SDP solutions to comply effectively.

- •Australia’s Security of Critical Infrastructure Act, updated in 2021 with enforcement mechanisms through 2024, requires operators to implement cybersecurity best practices including identity-based access management, aligning with SDP principles.

- •The ASEAN Cybersecurity Cooperation Strategy, developed between 2019 and 2023, provides a regional framework promoting collaborative security measures which foster cross-border adoption of SDP technology among member nations.

- •Regulatory bodies across Asia-Pacific have introduced compliance mandates on cloud security and remote access protections, including multi-factor authentication and continuous monitoring, which directly support the deployment and growth of SDP solutions.

Market Intelligence

- •15th February 2025, Cisco Systems, Inc. announced the launch of its latest Gateway-based SDP platform optimized for hybrid cloud environments, featuring AI-driven threat detection and seamless integration with leading cloud providers. The platform is designed to enhance secure access for enterprises in Asia-Pacific, supporting rapid scalability and compliance with regional data privacy regulations. This launch underscores Cisco’s commitment to advancing zero trust security architectures and addresses growing demand for flexible, software-defined network perimeters in the region. Source: Cisco Official Press Release

- •28th April 2025, Palo Alto Networks, Inc. introduced an enhanced Zero Trust Network Access (ZTNA) solution integrated with its Prisma Access cloud service, aimed at securing remote workforces across Asia-Pacific. The product features real-time user behavior analytics and automated policy enforcement, enabling enterprises to mitigate insider threats and advanced cyberattacks. This innovation supports multi-cloud deployment scenarios and aligns with evolving regulatory requirements in key Asia-Pacific markets such as India and Australia. Source: Palo Alto Networks Corporate Announcement

- •10th March 2025, Zscaler, Inc. completed strategic expansion into Southeast Asia by establishing a new regional headquarters in Singapore, enhancing local support and service delivery for its software-only SDP offerings. This move facilitates faster deployment cycles and tailored solutions for the growing cloud security market in ASEAN countries. The expansion is part of Zscaler’s broader growth strategy to capitalize on increasing digital transformation initiatives and cybersecurity investments in Asia-Pacific. Source: Zscaler Press Release

- •5th January 2025, Fortinet, Inc. announced a partnership with a leading telecom operator in South Korea to integrate SDP capabilities into 5G network infrastructure, providing secure and low-latency access for enterprise IoT applications. This collaboration aims to accelerate the adoption of secure network architectures leveraging zero trust principles within the Asia-Pacific region’s rapidly evolving telecommunications landscape. Source: Fortinet Corporate News

Regional Outlook

The China currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, India is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Japan

- China

- Southeast Asia

- India

- Australia

- South Korea

- Others

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.8 Billion |

| Forecast Year Market Size | USD 11.4 Billion |

| CAGR | 20.1% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 18.6% |

| Scope of Report | Market is segmented by Product Type (Gateway-based SDP, Client-based SDP, Hybrid SDP, Zero Trust Network Access, Software-only SDP), Application (Enterprise Security, Cloud Security, Data Center Security, Remote Access, Network Security), End-Use Industry (IT & Telecommunications, BFSI, Healthcare, Government & Defense), Distribution Channel (Direct Sales, Channel Partners, Managed Security Service Providers) |

| Regions Covered | Japan, China, Southeast Asia, India, Australia, South Korea, Others |

| Key Companies | Cisco Systems, Inc. (United States), Palo Alto Networks, Inc. (United States), Zscaler, Inc. (United States), Akamai Technologies, Inc. (United States), Fortinet, Inc. (United States), IBM Corporation (United States), Nokia Corporation (Finland), Check Point Software Technologies Ltd. (Israel), Cloudflare, Inc. (United States), Symantec Corporation (United States), Huawei Technologies Co., Ltd. (China), Tenable Holdings, Inc. (United States), Juniper Networks, Inc. (United States), Citrix Systems, Inc. (United States), VMware, Inc. (United States), Okta, Inc. (United States), SonicWall Inc. (United States), Dell Technologies Inc. (United States), Radware Ltd. (Israel), Netskope, Inc. (United States), A10 Networks, Inc. (United States), Barracuda Networks, Inc. (United States), Trend Micro Incorporated (Japan), F5 Networks, Inc. (United States), CyberArk Software Ltd. (Israel) |

Asia-Pacific Software Defined Perimeter Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.