Global Floating Liquefied Natural Gas Market Size, Growth & Revenue 2024-2034

Global Floating Liquefied Natural Gas Market is segmented by Product Type (Floating Storage Regasification Unit (FSRU), Floating Liquefied Natural Gas Carrier (FLNGC), Floating Liquefied Natural Gas Production Unit, Floating Storage Unit (FSU), Others), Application (Power Generation, Industrial Use, Transportation, Residential, Commercial), End-Use Industry (Energy & Utilities, Manufacturing, Transportation & Logistics, Residential & Commercial), Distribution Channel (Direct Contracts, Third-party Distributors, Governmental Agreements), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The Global Floating Liquefied Natural Gas (FLNG) market represents an innovative segment within the energy sector, focusing on the offshore processing, liquefaction, storage, and transportation of natural gas. FLNG technology facilitates the development of offshore gas fields without the necessity for extensive onshore infrastructure, enabling more flexible and cost-effective operations. The market comprises diverse FLNG vessel types such as Floating Storage Regasification Units (FSRUs), Floating Liquefied Natural Gas Carriers, and Floating Liquefied Natural Gas Production Units, each catering to specific operational needs. Applications span power generation, industrial use, residential and commercial energy supply, and transportation fuel. The increasing global demand for cleaner energy sources and the strategic pivot towards liquefied natural gas as a transitional fuel are pivotal drivers of market expansion. Moreover, advancements in offshore engineering, environmental regulations, and the need for energy security underpin the market's growth trajectory. As the industry evolves, collaboration between energy corporations, technology providers, and regulatory bodies is crucial to address operational challenges and unlock new opportunities across key regions worldwide.

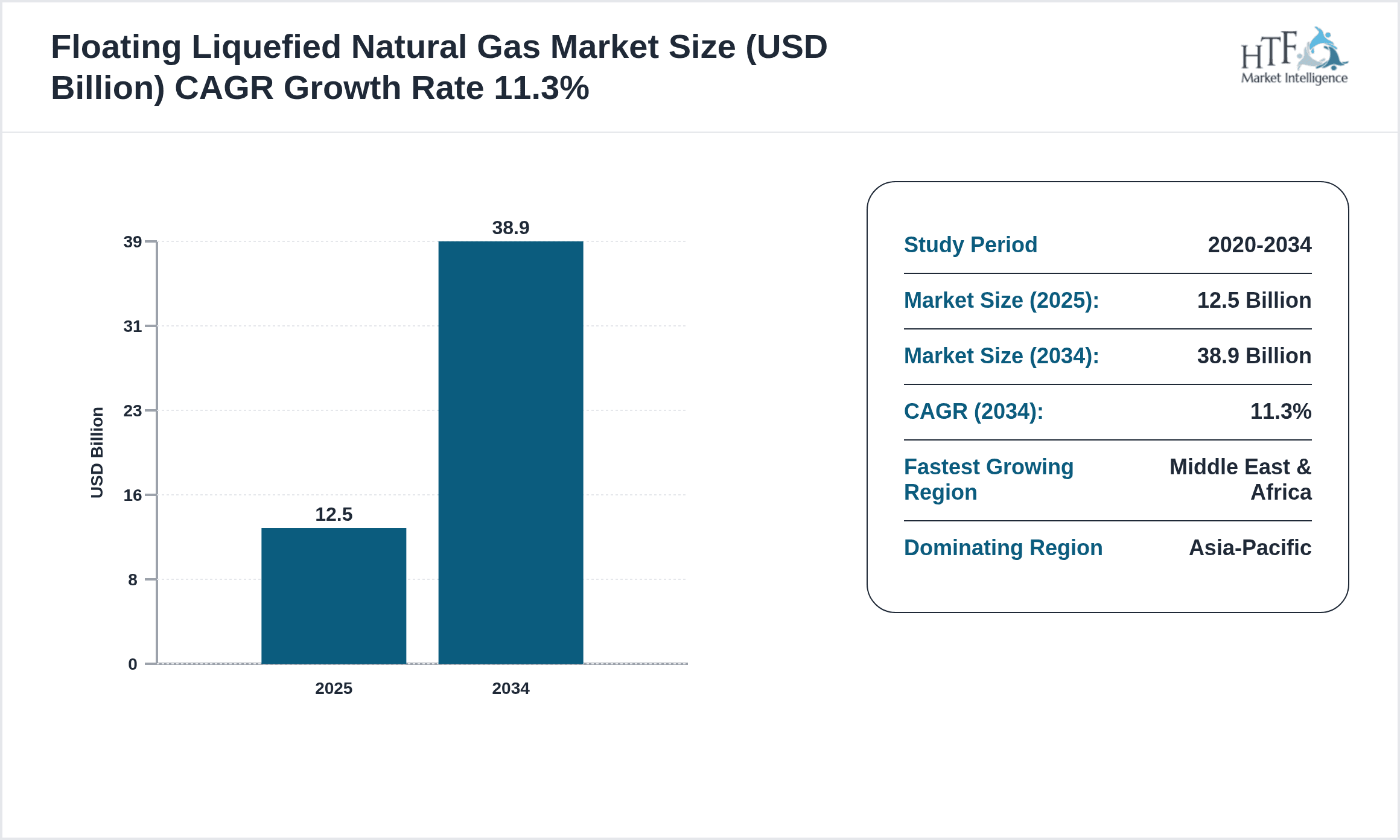

- •The FLNG market is witnessing robust growth with a compound annual growth rate (CAGR) of 11.3% projected from 2024 to 2034, expanding from USD 12.5 Billion in 2024 to an anticipated USD 38.9 Billion by 2034. Asia-Pacific dominates the market share due to significant offshore gas exploration activities and rising energy demand, while the Middle East & Africa is identified as the fastest-growing region with aggressive infrastructure investments. Floating Storage Regasification Units lead the product segment, capturing the largest market share, closely followed by Floating Liquefied Natural Gas Production Units exhibiting the highest growth rates. Power generation remains the primary application, driven by increasing adoption of natural gas as a cleaner fuel alternative. These growth indicators reflect market maturity alongside emerging regional opportunities, highlighting strategic importance for stakeholders.

- •The Global FLNG market presents significant value propositions to energy producers, technology developers, and end-users by enabling flexible, cost-efficient offshore gas monetization. It reduces dependency on onshore facilities, minimizes environmental footprint, and enhances supply chain agility, contributing to energy security and sustainability objectives worldwide. The strategic importance of FLNG technology is underscored by its role in unlocking stranded gas reserves and supporting the transition to lower-carbon energy systems. Stakeholders benefit from diversified applications across power generation, industrial fuel supply, and transportation sectors. The market's expanding footprint across key regions positions it as a critical enabler of global energy transition strategies, offering opportunities for innovation, collaboration, and long-term growth.

Competitive Landscape

The Global Floating Liquefied Natural Gas market is characterized by an intensely competitive environment driven by technological innovation, strategic partnerships, and global expansion initiatives. Leading players emphasize development of advanced FLNG technologies that offer enhanced operational efficiency, safety, and environmental compliance. Market rivalry is fueled by the need to secure lucrative offshore gas fields and deliver cost-effective solutions that reduce breakeven prices. Companies compete by investing in research and development, forming strategic alliances, and expanding service portfolios to cater to diverse regional demands. The competitive landscape also reflects consolidation trends through mergers and acquisitions aimed at enhancing market presence and technology capabilities. Pricing strategies are influenced by fluctuating raw material costs and regulatory frameworks, while distribution channels focus on direct contracts with energy producers and governmental entities. Regional competition varies, with Asia-Pacific and Middle East & Africa witnessing heightened activity due to rapid infrastructure development and growing energy consumption. Future competitive dynamics will likely revolve around sustainability integration, digitalization, and modular FLNG solutions to meet evolving market needs.

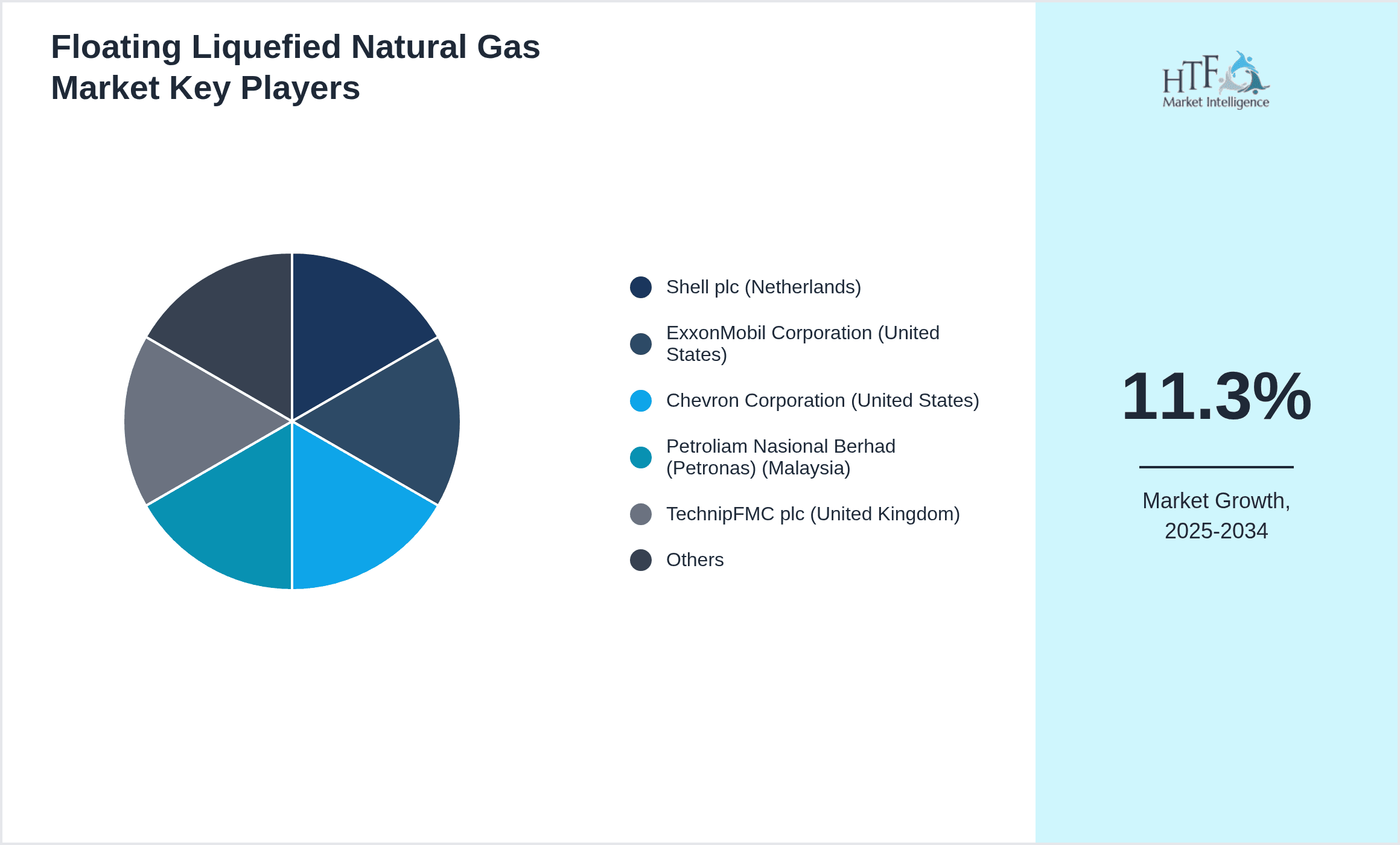

Leading Companies in Floating Liquefied Natural Gas Market

- •Shell plc (Netherlands)

- •ExxonMobil Corporation (United States)

- •Chevron Corporation (United States)

- •Petroliam Nasional Berhad (Petronas) (Malaysia)

- •TechnipFMC plc (United Kingdom)

- •Samsung Heavy Industries Co., Ltd. (South Korea)

- •MODEC, Inc. (Japan)

- •BW Group (Singapore)

- •McDermott International, Inc. (United States)

- •Mitsubishi Heavy Industries, Ltd. (Japan)

- •JGC Corporation (Japan)

- •KBR, Inc. (United States)

- •Saipem S.p.A. (Italy)

- •Samsung Engineering Co., Ltd. (South Korea)

- •China State Shipbuilding Corporation (China)

- •Daewoo Shipbuilding & Marine Engineering Co., Ltd. (South Korea)

- •Hyundai Heavy Industries Co., Ltd. (South Korea)

- •Wood Group (United Kingdom)

- •Technip Energies (France)

- •Fluor Corporation (United States)

- •Petrofac Limited (United Kingdom)

- •Samsung C&T Corporation (South Korea)

- •Linde plc (Ireland)

- •Air Products and Chemicals, Inc. (United States)

- •McDermott International, Inc. (United States)

Market Breakdown

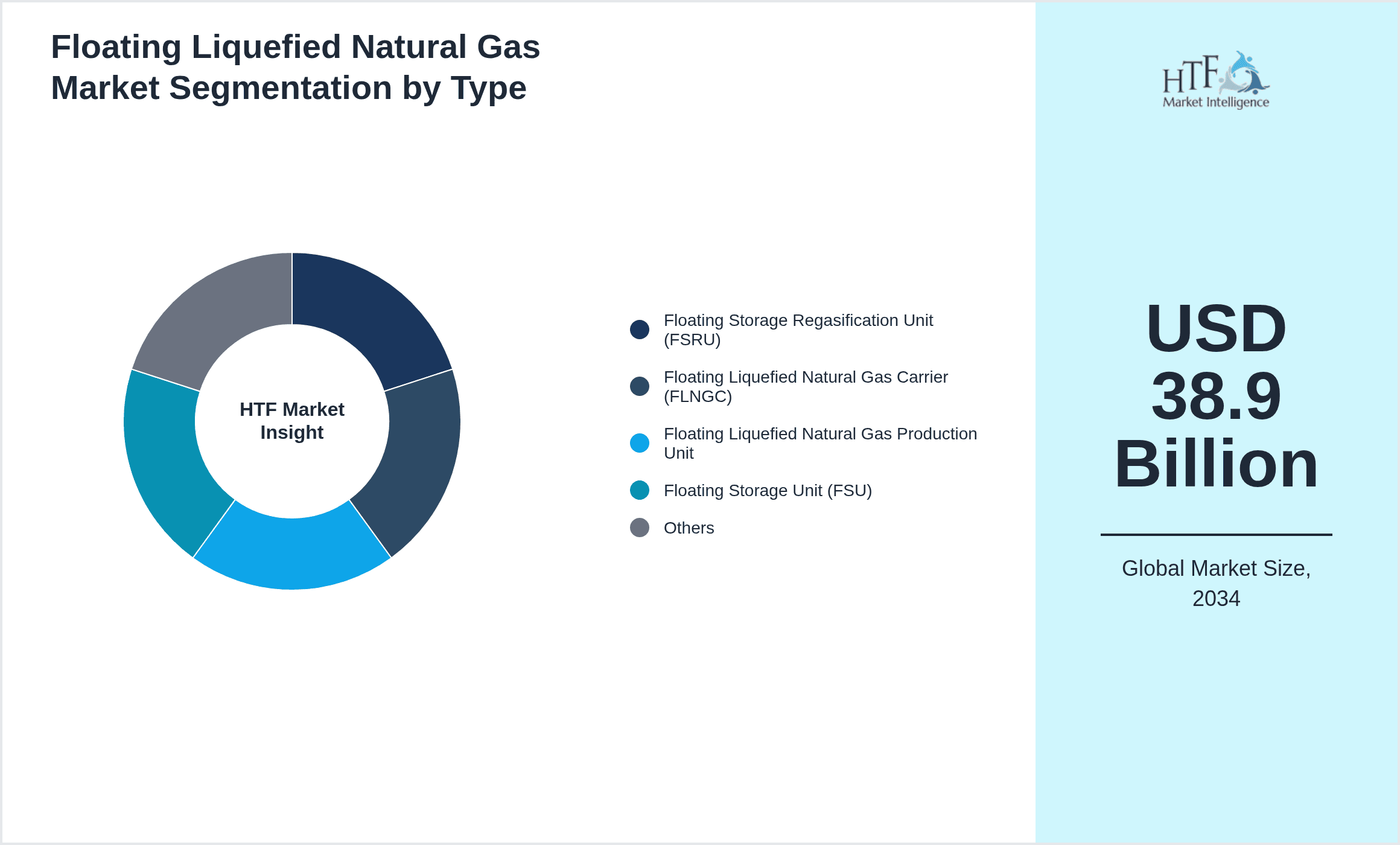

- •By Product Type

- ◦Floating Storage Regasification Unit (FSRU)

- ◦Floating Liquefied Natural Gas Carrier (FLNGC)

- ◦Floating Liquefied Natural Gas Production Unit

- ◦Floating Storage Unit (FSU)

- ◦Others

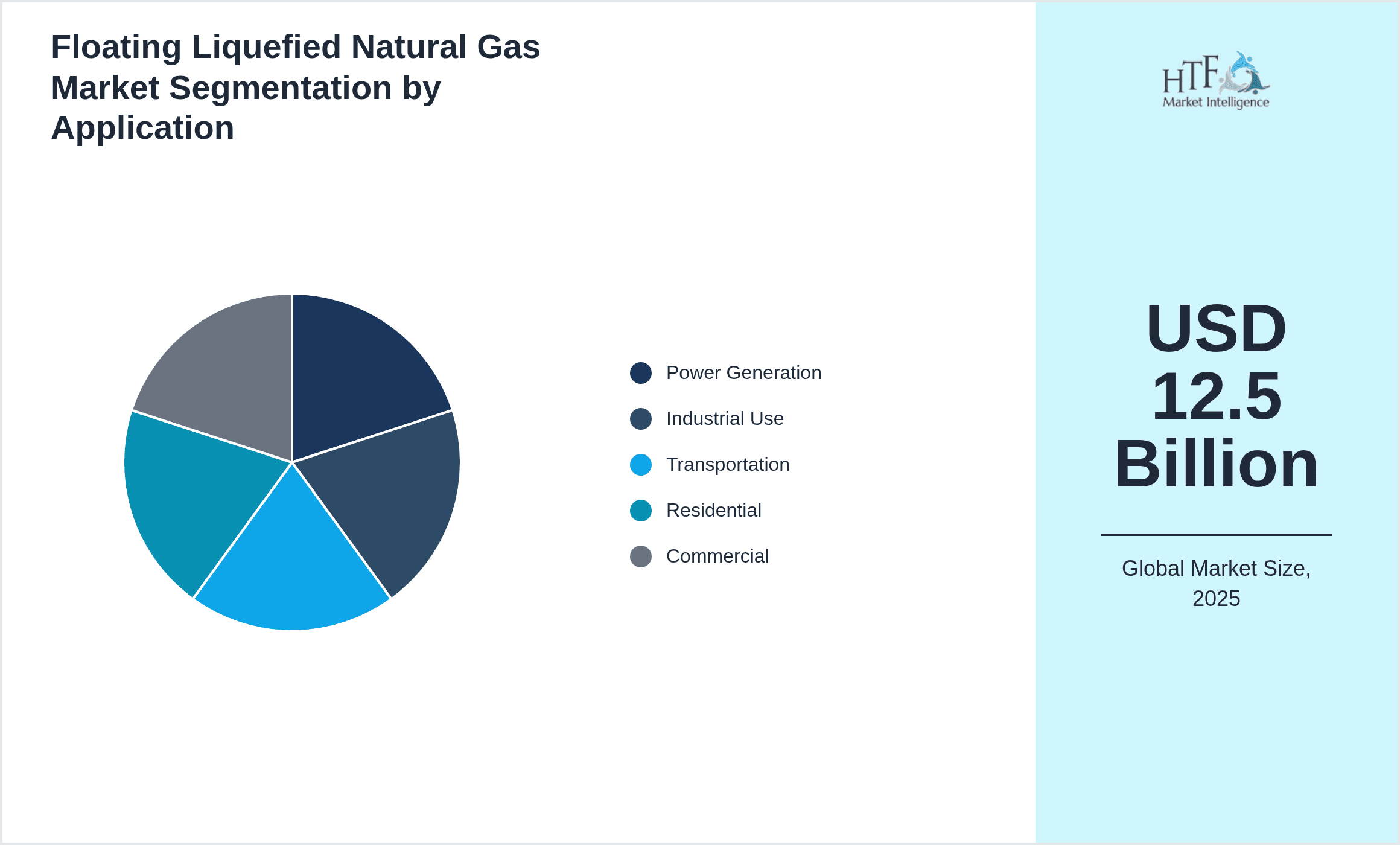

- •By Application

- ◦Power Generation

- ◦Industrial Use

- ◦Transportation

- ◦Residential

- ◦Commercial

- •By End-Use Industry

- ◦Energy & Utilities

- ◦Manufacturing

- ◦Transportation & Logistics

- ◦Residential & Commercial

- •By Distribution Channel

- ◦Direct Contracts

- ◦Third-party Distributors

- ◦Governmental Agreements

Growth Dynamics

The Global Floating Liquefied Natural Gas market is propelled by escalating demand for cleaner energy sources as governments and industries aim to reduce carbon emissions. FLNG technology enables monetization of remote and offshore gas reserves that were previously uneconomical, facilitating energy supply diversification. Rising investments in offshore infrastructure development, coupled with technological advancements improving operational efficiency and safety, stimulate market growth. Additionally, the flexibility offered by FLNG units in transportation and storage reduces logistical constraints, attracting energy producers. The integration of digital technologies such as IoT and AI for remote monitoring and predictive maintenance further enhances operational reliability. The growing industrialization in emerging economies, especially in Asia-Pacific, amplifies natural gas consumption, bolstering FLNG adoption. Furthermore, regulatory incentives promoting LNG use in transportation and power sectors underscore the market’s expansion potential. Collectively, these factors create a robust growth environment for the FLNG market globally.

Market Trends

The FLNG market is experiencing a trend towards modular and scalable floating units enabling faster deployment and cost optimization. Industry players are increasingly integrating digital twin technologies and advanced analytics for enhanced operational efficiency and risk mitigation. There is a rising focus on environmental sustainability, with companies adopting greener technologies and designs to reduce emissions and marine impact. Strategic collaborations between energy firms and shipbuilders are becoming prevalent to accelerate innovation and project execution. Additionally, the shift towards hybrid fuel solutions incorporating LNG as a transition fuel in maritime and power sectors is influencing market dynamics. Regional diversification is evident with increased FLNG activities in the Middle East & Africa and Latin America, driven by untapped gas reserves and supportive policies. These trends highlight the market’s evolution towards flexibility, sustainability, and technological sophistication.

Market Opportunities

Emerging offshore gas discoveries in underexplored regions present substantial opportunities for FLNG deployment to access stranded reserves cost-effectively. The increasing global emphasis on energy transition offers growth avenues through LNG's role as a cleaner alternative fuel in power and transportation sectors. Expansion of LNG bunkering infrastructure to support maritime decarbonization creates new application segments. Moreover, advancements in floating production technologies and integration with renewable energy systems open innovative pathways for hybrid energy solutions. Strategic partnerships and joint ventures between upstream and midstream players enable market expansion and risk sharing. Additionally, government incentives and regulatory frameworks promoting LNG adoption in emerging economies stimulate investment. These factors collectively create a fertile environment for market participants to capitalize on evolving demand and technological advancements.

Market Challenges

The FLNG market faces challenges including high capital expenditure and complex offshore engineering requirements which can delay project timelines and impact profitability. Regulatory compliance across multiple jurisdictions introduces operational complexities and cost variability. Technical challenges related to harsh marine environments and safety risks require continuous innovation and stringent standards, raising operational costs. Market volatility in natural gas prices affects investment decisions and project viability. Limited availability of skilled workforce and specialized equipment constrains capacity expansion. Environmental concerns and stakeholder opposition may impact project approvals. Additionally, competition from alternative energy sources such as renewables and pipeline gas infrastructure poses long-term market risks. Addressing these challenges necessitates collaborative efforts among stakeholders, innovation, and adaptive strategic planning.

Regulatory Framework

Between 2019 and 2024, several international and regional regulatory developments have shaped the FLNG market landscape. The International Maritime Organization (IMO) has implemented stricter emissions standards, including the 2020 sulfur cap, compelling FLNG operators to adopt cleaner fuel technologies. Environmental protection regulations concerning marine biodiversity and pollution control have become more stringent, requiring enhanced operational safeguards. Many jurisdictions have introduced licensing frameworks for offshore gas exploitation and FLNG operations to ensure safety and environmental compliance. Energy transition policies promoting LNG as a bridge fuel have incentivized infrastructure investments through subsidies and tax benefits. Additionally, cross-border trade regulations and natural gas tariff structures have evolved, impacting market logistics and pricing. These regulatory changes collectively influence project feasibility, investment attractiveness, and operational protocols across major global regions.

Market Intelligence

- •15th March 2024, Shell plc announced the launch of its latest Floating Liquefied Natural Gas Production Unit featuring enhanced liquefaction capacity and reduced emissions technology. The innovative FLNG vessel integrates advanced modular design and digital monitoring systems aimed at improving operational reliability and reducing environmental footprint. This development targets expanding offshore gas fields in the Asia-Pacific region, supporting Shell's strategic growth in cleaner energy solutions. The new unit aligns with global energy transition goals by enabling cost-effective access to remote gas reserves while minimizing carbon emissions. Shell’s initiative is expected to strengthen its market position and set new industry benchmarks for sustainability and efficiency in FLNG operations. Source: Shell Official Press Release

- •22nd August 2023, BW Group announced a strategic partnership with Samsung Heavy Industries to co-develop next-generation Floating Storage Regasification Units (FSRU) incorporating energy-efficient regasification technology. This collaboration aims to enhance LNG import capacity in emerging markets, particularly in the Middle East & Africa, by delivering scalable and rapid-deployment solutions. The partnership focuses on integrating digital twin technology for remote asset management and predictive maintenance to optimize uptime and reduce operating costs. This initiative reflects growing industry trends towards technological innovation and market expansion in underserved regions. The combined expertise of BW Group and Samsung Heavy Industries positions them competitively within the global FLNG market. Source: BW Group Corporate Announcement

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Regional Outlook

The Asia-Pacific currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Middle East & Africa is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 12.5 Billion |

| Forecast Year Market Size | USD 38.9 Billion |

| CAGR | 11.3% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 11.3% |

| Scope of Report | Market is segmented by Product Type (Floating Storage Regasification Unit (FSRU), Floating Liquefied Natural Gas Carrier (FLNGC), Floating Liquefied Natural Gas Production Unit, Floating Storage Unit (FSU), Others), Application (Power Generation, Industrial Use, Transportation, Residential, Commercial), End-Use Industry (Energy & Utilities, Manufacturing, Transportation & Logistics, Residential & Commercial), Distribution Channel (Direct Contracts, Third-party Distributors, Governmental Agreements) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Shell plc (Netherlands), ExxonMobil Corporation (United States), Chevron Corporation (United States), Petroliam Nasional Berhad (Petronas) (Malaysia), TechnipFMC plc (United Kingdom) |

Global Floating Liquefied Natural Gas Market Size, Growth & Revenue 2024-2034 - Table of Contents

Multidisciplinary researcher with 10+ years of experience uncovering insights across diverse domains focused on uncovering insights that drive informed decisions.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.