Global Automotive Exterior Materials Market Size, Growth & Revenue 2024-2034

Global Automotive Exterior Materials Market is segmented by Product Type (Plastics (Thermoplastics, Thermosetting Plastics), Metals (Aluminum, Steel, Magnesium), Composites (Carbon Fiber Reinforced Polymers, Glass Fiber Reinforced Polymers), Glass (Tempered, Laminated), Paints & Coatings (Waterborne, Solventborne)), Application (Body Panels, Bumpers, Trim Components, Mirrors, Lighting), End-Use Industry (Passenger Cars, Commercial Vehicles, Electric Vehicles, Luxury Vehicles), Distribution Channel (OEM Supply, Aftermarket Distribution, Direct-to-Consumer), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The Global Automotive Exterior Materials market involves the design, development, and supply of materials used in the external components of vehicles such as body panels, bumpers, trim, mirrors, and lighting. This market integrates advanced plastics, lightweight metals, composites, glass, and specialized paints and coatings to address performance, safety, and aesthetic requirements. Key drivers include the automotive industry's move towards lightweight materials to improve fuel efficiency and reduce emissions, stringent environmental regulations, and growing demand for electric and autonomous vehicles. The market spans multiple vehicle segments, including passenger cars and commercial vehicles, and is influenced by technological innovation, cost optimization, and sustainability considerations. With rising global vehicle production and increased consumer focus on vehicle appearance and durability, the market is poised for robust growth through 2034.

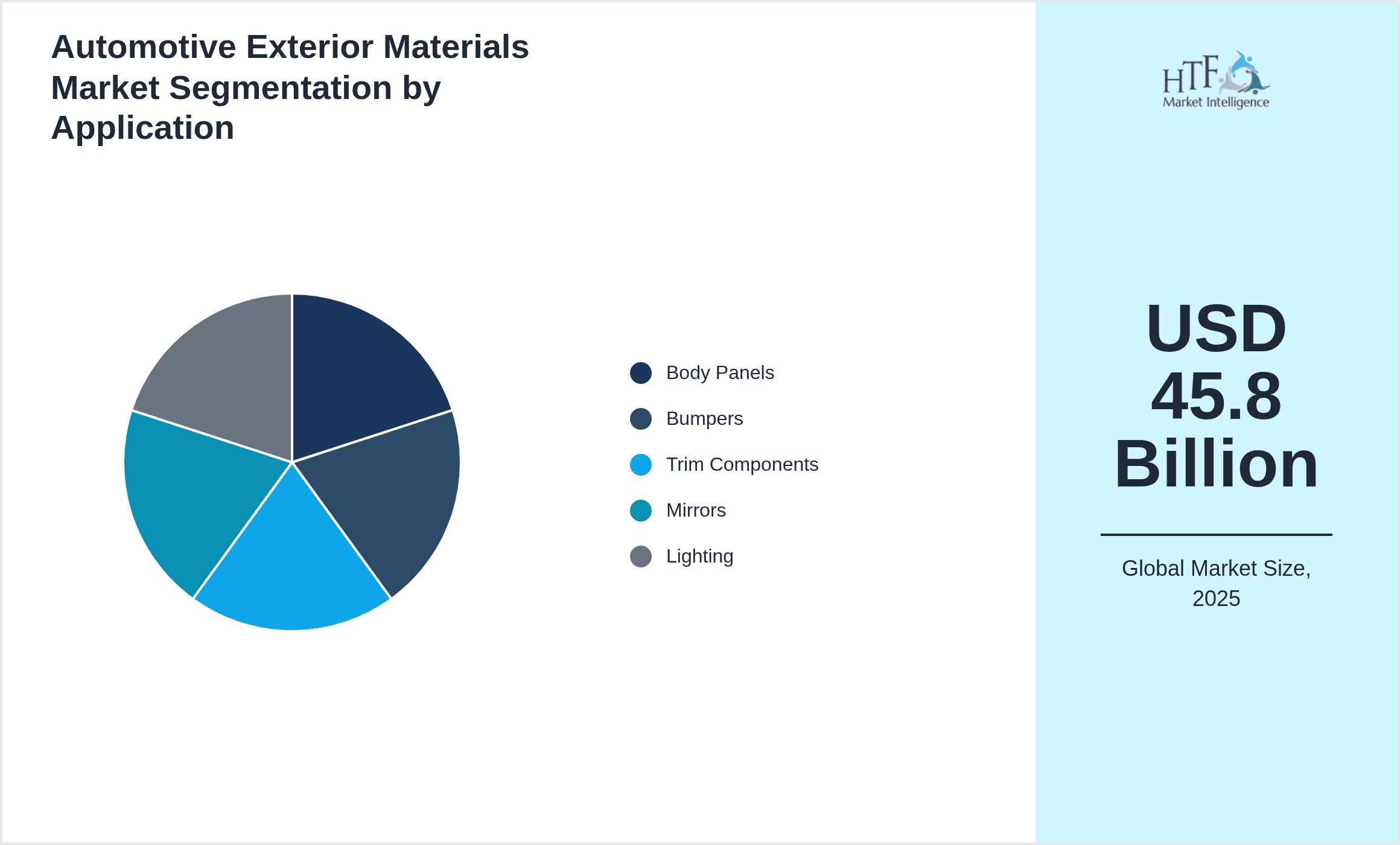

- •Market highlights indicate a 7.1% CAGR from 2024 to 2034, with the market size expected to nearly double from USD 45.8 Billion in 2024 to USD 89.7 Billion by 2034. Plastics dominate the material type segment, while composites are the fastest-growing type due to their lightweight and strength advantages. Body panels lead the application segment, followed closely by bumpers and trim components. Geographically, North America holds a dominant share driven by advanced automotive manufacturing, while Asia-Pacific is the fastest-growing region fueled by rapid industrialization and increasing vehicle production. Market growth is supported by continuous R&D investments, expansion of electric vehicle platforms, and increasing consumer preference for durable and stylish exteriors.

- •This market offers strategic value to material suppliers, automotive OEMs, and aftermarket players by enabling the development of innovative, sustainable, and cost-effective exterior solutions. It supports the automotive sector's goals of enhancing vehicle safety, reducing weight, and complying with environmental regulations. The evolving landscape also provides opportunities for partnerships and technological advancements, particularly in composite materials and advanced coatings. Stakeholders can leverage these trends to capture emerging markets, diversify product portfolios, and strengthen supply chain resilience in a competitive global environment.

Competitive Landscape

The competitive environment of the global Automotive Exterior Materials market is characterized by a blend of established multinational corporations and innovative regional suppliers striving to enhance product portfolios and geographic reach. Companies are increasingly investing in R&D to develop lightweight, durable, and eco-friendly materials that meet stringent regulatory standards and evolving consumer demands. Market rivalry is intense, with firms competing on technology innovation, production efficiency, and strategic collaborations. Mergers and acquisitions are common as players seek to consolidate capabilities and expand their material offerings. Pricing strategies and supply chain optimization also play critical roles in securing market share. The adoption of advanced composites and sustainable coatings is shaping the competitive landscape, encouraging continuous innovation and differentiation. Regional dynamics further influence competition, with Asia-Pacific emerging as a hotspot for growth due to increasing vehicle manufacturing and demand for advanced exterior materials.

Leading Companies in Automotive Exterior Materials Market

- •BASF SE (Germany)

- •3M Company (United States)

- •PPG Industries, Inc. (United States)

- •Covestro AG (Germany)

- •Dow Inc. (United States)

- •Sika AG (Switzerland)

- •Solvay S.A. (Belgium)

- •Akzo Nobel N.V. (Netherlands)

- •Toray Industries, Inc. (Japan)

- •Eastman Chemical Company (United States)

- •PPG Architectural Coatings (United States)

- •Henkel AG & Co. KGaA (Germany)

- •Bayer AG (Germany)

- •Celanese Corporation (United States)

- •Arkema S.A. (France)

- •Dupont de Nemours, Inc. (United States)

- •Mitsubishi Chemical Holdings Corporation (Japan)

- •LG Chem Ltd. (South Korea)

- •Sumitomo Chemical Co., Ltd. (Japan)

- •Clariant AG (Switzerland)

- •Celanese Limited (United Kingdom)

- •Huntsman Corporation (United States)

- •Wacker Chemie AG (Germany)

- •INEOS Group Limited (United Kingdom)

- •Lanxess AG (Germany)

Market Breakdown

- •By Product Type

- ◦Plastics (Thermoplastics, Thermosetting Plastics)

- ◦Metals (Aluminum, Steel, Magnesium)

- ◦Composites (Carbon Fiber Reinforced Polymers, Glass Fiber Reinforced Polymers)

- ◦Glass (Tempered, Laminated)

- ◦Paints & Coatings (Waterborne, Solventborne)

- •By Application

- ◦Body Panels

- ◦Bumpers

- ◦Trim Components

- ◦Mirrors

- ◦Lighting

- •By End-Use Industry

- ◦Passenger Cars

- ◦Commercial Vehicles

- ◦Electric Vehicles

- ◦Luxury Vehicles

- •By Distribution Channel

- ◦OEM Supply

- ◦Aftermarket Distribution

- ◦Direct-to-Consumer

Growth Dynamics

- •Rising demand for lightweight automotive materials is a primary growth driver, as manufacturers seek to improve fuel efficiency and reduce emissions in response to global environmental regulations.

- •Technological advancements in composite materials and coatings enable enhanced durability and aesthetics, fostering adoption among OEMs focused on vehicle performance and style.

- •Growth in electric vehicle production globally is driving demand for specialized exterior materials that balance weight reduction with safety and design flexibility.

- •Increasing consumer preference for customized and premium vehicle exteriors is fueling innovation in paints, coatings, and trim materials, expanding market opportunities.

- •Expansion of automotive manufacturing in emerging markets, particularly in Asia-Pacific and Latin America, is creating substantial demand for exterior materials.

- •Stringent regulatory frameworks on emissions and recyclability are encouraging the adoption of sustainable and eco-friendly exterior materials in vehicle production.

- •Investment in R&D and collaborations between material suppliers and automakers are driving continuous innovation and market expansion.

Market Trends

- •The shift towards lightweight composites is accelerating, with manufacturers increasingly replacing traditional metals with carbon fiber and glass fiber reinforced polymers to improve vehicle efficiency.

- •Sustainable and bio-based materials are gaining traction as regulatory pressures and consumer environmental awareness increase, promoting green alternatives in exterior components.

- •Integration of smart coatings with self-healing and anti-scratch properties is emerging as a key innovation, enhancing exterior durability and reducing maintenance costs.

- •Digitalization in manufacturing processes, including 3D printing and automated application of coatings, is improving precision, reducing waste, and speeding up production cycles.

- •Collaboration between chemical companies and automakers is increasing to co-develop tailored materials that meet bespoke vehicle design and performance requirements.

- •Consumer demand for aesthetic customization is leading to a rise in specialty paints and finishes, including matte, metallic, and color-shifting coatings.

- •Regulatory emphasis on recyclability and circular economy principles is influencing material selection and end-of-life vehicle processing strategies.

Market Opportunities

- •Expanding electric and autonomous vehicle markets present opportunities for developing lightweight, multifunctional exterior materials that enhance safety and range.

- •Emerging economies in Asia-Pacific and Latin America offer untapped potential due to rising vehicle production and demand for modern exterior components.

- •Innovations in nanotechnology and smart coatings can create value-added exterior materials with enhanced properties, opening new application segments.

- •Strategic partnerships between material suppliers and OEMs can accelerate adoption of advanced composites and sustainable materials in mainstream vehicle models.

- •Growth in aftermarket personalization and repair segments provides avenues for specialized paints, coatings, and trim materials.

- •Government incentives for green manufacturing and sustainable materials development can boost investments and innovation in this sector.

- •Adoption of Industry 4.0 technologies in production and supply chain management can enhance efficiency and reduce costs for exterior material providers.

Market Challenges

- •High costs associated with advanced composite materials and innovative coatings limit widespread adoption, especially in cost-sensitive vehicle segments.

- •Complex regulatory compliance across different regions creates challenges for global material suppliers in ensuring product approvals and certifications.

- •Supply chain disruptions, including raw material shortages and logistics constraints, affect the timely delivery and pricing stability of exterior materials.

- •Technical limitations related to recycling and end-of-life processing of composite and multi-material components pose environmental and economic hurdles.

- •Intense competition leads to pricing pressures and necessitates continuous innovation investments to maintain market position.

- •Balancing durability, aesthetics, and environmental sustainability in exterior materials requires complex R&D and testing, extending product development cycles.

- •Evolving consumer preferences and rapid technological changes demand agile manufacturing and supply chain strategies.

Regulatory Framework

- •Between 2019 and 2024, the European Union implemented the End-of-Life Vehicles Directive (2000/53/EC) revisions requiring higher recycling rates and restrictions on hazardous substances in automotive materials, compelling manufacturers to adopt eco-friendly exterior materials.

- •The U.S. Environmental Protection Agency (EPA) enhanced volatile organic compound (VOC) emission limits for automotive coatings in 2021, requiring advanced low-VOC paints and coatings to reduce environmental impact and comply with air quality standards.

- •China introduced the Automotive Lightweight Materials Policy in 2022, incentivizing the use of advanced composites and aluminum alloys in vehicle exteriors to reduce fuel consumption and emissions, catalyzing market growth in the Asia-Pacific region.

- •Japan enforced stricter chemical substance regulations in automotive materials in 2023, aligning with global standards to improve vehicle recyclability and reduce environmental hazards, impacting material formulations and supply chains.

- •Global mandates under the United Nations Economic Commission for Europe (UNECE) concerning vehicle safety and environmental performance, updated in 2020, also influence exterior material standards, ensuring harmonization across major automotive markets.

Market Intelligence

- •15th January 2025, BASF SE launched a next-generation lightweight composite material specifically designed for automotive exterior panels, featuring enhanced durability and recyclability. This innovation targets electric vehicle manufacturers aiming to reduce vehicle weight and improve driving range. The product integrates bio-based resins and advanced fiber reinforcements, aligning with sustainable manufacturing goals and regulatory compliance in major markets. BASF SE's strategic objective is to establish leadership in eco-friendly automotive materials and capture growing demand in Asia-Pacific and Europe. Source: Official BASF press release.

- •10th March 2025, 3M Company introduced an innovative automotive coating technology with self-healing and scratch-resistant properties for exterior surfaces. The new coating leverages nanotechnology to provide long-lasting protection while maintaining aesthetic appeal. Target applications include body panels and bumpers across passenger and commercial vehicles. 3M aims to enhance vehicle longevity and reduce maintenance costs, responding to rising consumer expectations. The product launch is backed by partnerships with leading automakers in North America and Europe. Source: 3M official announcement.

- •22nd May 2025, Covestro AG announced a strategic partnership with a major European automotive OEM to co-develop sustainable plastic exterior components using recycled raw materials. This collaboration focuses on reducing carbon footprints and advancing circular economy principles in vehicle manufacturing. The initiative encompasses research, production scale-up, and market introduction scheduled for late 2026. Covestro AG’s investment underscores commitment to sustainability and innovation leadership in the automotive materials sector. Source: Covestro corporate news.

- •5th July 2025, PPG Industries, Inc. completed expansion of its automotive coatings manufacturing facility in Asia-Pacific to meet growing demand from electric vehicle producers. The enhanced capacity includes advanced environmentally friendly paint lines adhering to local regulations and global standards. PPG’s strategic move aims to strengthen supply chain resilience and service excellence in the fastest-growing automotive region worldwide. The facility upgrade supports PPG’s vision for sustainable growth and technological advancement. Source: PPG Industries press release.

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 45.8 Billion |

| Forecast Year Market Size | USD 89.7 Billion |

| CAGR | 7.1% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7% |

| Scope of Report | Market is segmented by Product Type (Plastics (Thermoplastics, Thermosetting Plastics), Metals (Aluminum, Steel, Magnesium), Composites (Carbon Fiber Reinforced Polymers, Glass Fiber Reinforced Polymers), Glass (Tempered, Laminated), Paints & Coatings (Waterborne, Solventborne)), Application (Body Panels, Bumpers, Trim Components, Mirrors, Lighting), End-Use Industry (Passenger Cars, Commercial Vehicles, Electric Vehicles, Luxury Vehicles), Distribution Channel (OEM Supply, Aftermarket Distribution, Direct-to-Consumer) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | BASF SE (Germany), 3M Company (United States), PPG Industries, Inc. (United States), Covestro AG (Germany), Dow Inc. (United States) |

Global Automotive Exterior Materials Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.