North America Solid Phase Peptide Synthesis Market Size, Growth & Revenue 2024-2034

North America Solid Phase Peptide Synthesis Market is segmented by Product Type (Fmoc Chemistry, Boc Chemistry, Hybrid Chemistry, Other Types), Application (Therapeutic Peptides, Diagnostic Peptides, Research Peptides, Cosmetic Peptides, Industrial Peptides), End-Use Industry (Pharmaceuticals, Biotechnology, Academic & Research Institutes, Cosmetics & Personal Care), Distribution Channel (Direct Sales, Distributors & Dealers, Online Platforms), and Geography (United States, Canada, Mexico)

Pricing

Report Overview

Executive Summary

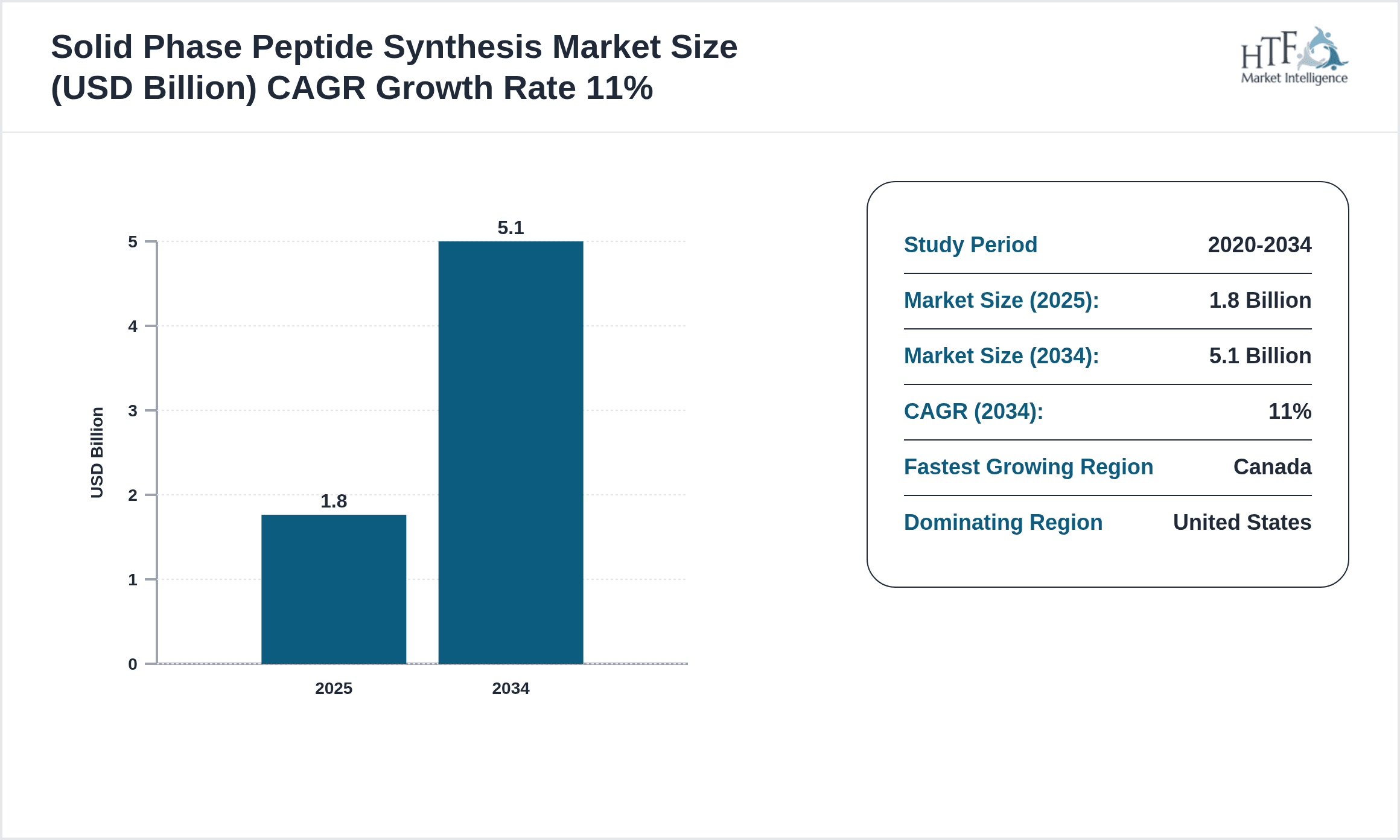

- •The North America Solid Phase Peptide Synthesis market is a specialized segment within the broader peptide manufacturing industry, focusing on the synthesis of peptides via a solid support matrix that facilitates efficient and scalable peptide chain assembly. Key chemistries such as Fmoc and Boc dominate the market, supported by emerging hybrid techniques enhancing synthesis speed and product purity. The market delivers high-value products that play a critical role in drug discovery, therapeutic development, diagnostics, cosmetics, and industrial applications. This market's scope includes raw materials like resins and reagents, automated synthesizers, and complementary technologies that enable precision peptide production. The primary geographic focus spans the United States, Canada, and Mexico, with the U.S. holding the largest share due to its advanced pharmaceutical sector and robust research infrastructure. Growth is underpinned by expanding peptide drug pipelines, increased research investments, and rising adoption of automated synthesis platforms. Challenges include high synthesis costs and complex regulatory landscapes, which are balanced by opportunities in novel peptide therapeutics and hybrid synthesis innovations.

- •The market is projected to grow from USD 1.8 billion in 2024 to USD 5.1 billion by 2034, reflecting a CAGR of approximately 11.0%. Demand for therapeutic peptides and research peptides segments is expanding rapidly, driven by the rise in chronic diseases and personalized medicine. Fmoc chemistry remains the leading synthesis type with significant market share, while hybrid chemistry is poised for fastest growth due to its enhanced efficiency. The United States dominates the regional market, accounting for the majority of revenue, with Canada exhibiting the highest growth rate. Market dynamics are shaped by technological advancements in automation, increasing peptide drug approvals, and strategic collaborations among key industry players. The growing emphasis on peptide-based diagnostics and cosmetics also contributes to diversification across applications.

- •This market offers strategic value to pharmaceutical, biotechnology, and research organizations by enabling rapid peptide synthesis critical for drug discovery and development workflows. The high specificity and purity achievable through solid phase synthesis support the creation of novel peptide therapeutics and targeted diagnostics. Stakeholders benefit from emerging technologies that reduce synthesis time and cost while improving scalability. Additionally, the continuous innovation in resin chemistries and automated synthesizers aligns with the increasing demand for complex peptides. The market’s growth trajectory highlights opportunities in expanding clinical trials, personalized medicine, and industrial peptide applications, positioning North America as a significant hub for peptide synthesis innovation and commercialization.

Competitive Landscape

The North America Solid Phase Peptide Synthesis market is characterized by intense competition among established global and regional players focusing on innovation, product portfolio expansion, and strategic partnerships. Market leaders invest heavily in R&D to develop advanced automated synthesizers and novel resin chemistries that enhance synthesis efficiency and purity. Companies differentiate through proprietary synthesis technologies, comprehensive reagent offerings, and integrated service models that cater to pharmaceutical, biotech, and academic customers. Competitive strategies include mergers and acquisitions to consolidate capabilities, geographic expansion to tap emerging markets within North America, and collaborations with research institutions to accelerate innovation. Pricing strategies balance premium quality with cost-effective solutions to address diverse customer needs. Distribution channels are optimized through direct sales and partnerships with specialized suppliers. Future competition will increasingly revolve around sustainability, digital integration, and the ability to meet complex peptide synthesis demands, reinforcing the competitive advantage of agile, innovation-driven organizations.

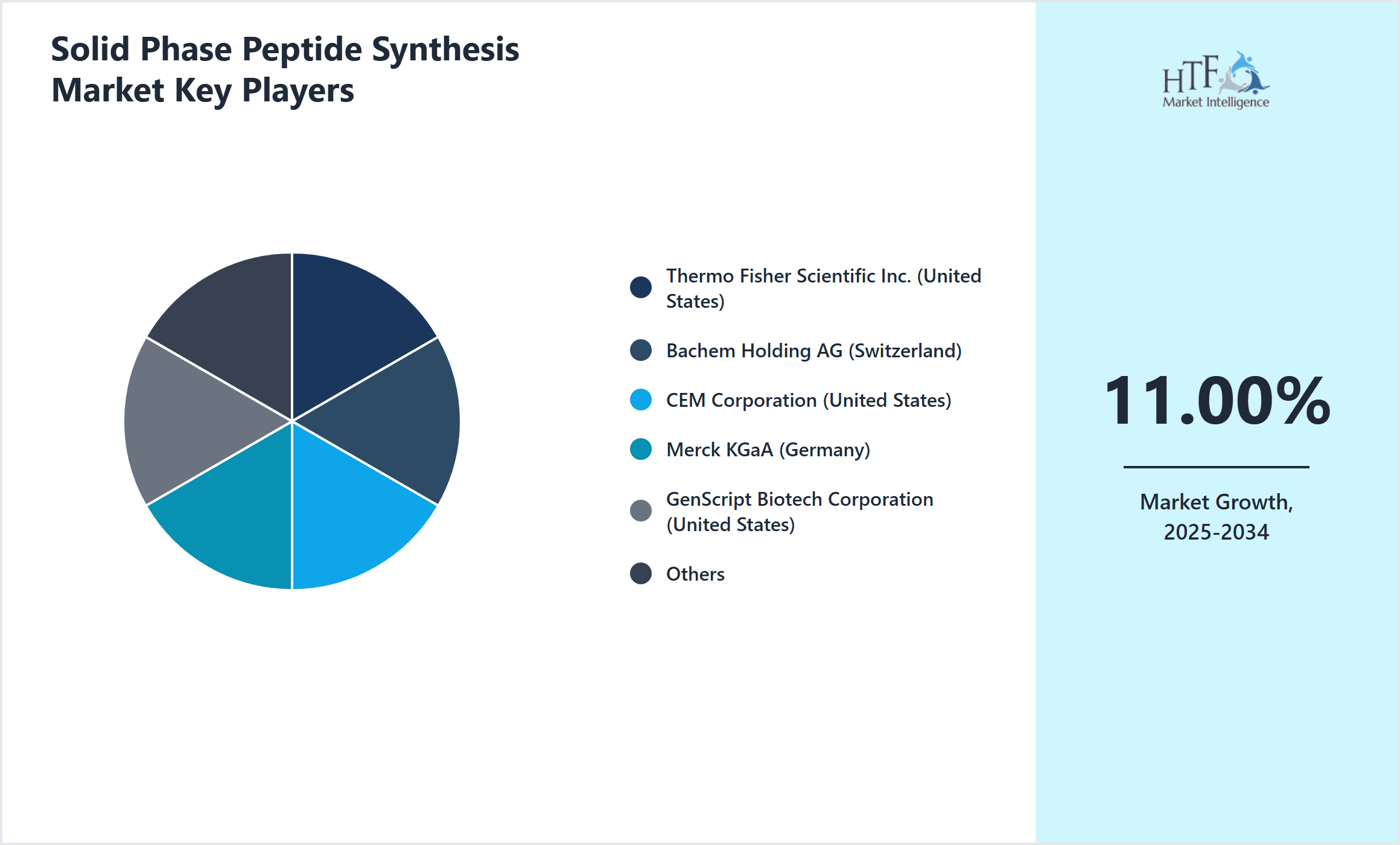

Leading Companies in Solid Phase Peptide Synthesis Market

- •Thermo Fisher Scientific Inc. (United States)

- •Bachem Holding AG (Switzerland)

- •CEM Corporation (United States)

- •Merck KGaA (Germany)

- •GenScript Biotech Corporation (United States)

- •Peptides International, Inc. (United States)

- •PolyPeptide Group (Sweden)

- •CSBio, Inc. (United States)

- •Iris Biotech GmbH (Germany)

- •Aapptec (United States)

- •Bachem Americas, Inc. (United States)

- •AnaSpec, Inc. (United States)

- •SynPeptide Co., Ltd. (China)

- •Peptidream Inc. (Japan)

- •Peptide Synthetics Ltd. (United Kingdom)

- •Sigma-Aldrich Corporation (United States)

- •Almac Group (United Kingdom)

- •AAPPTec (United States)

- •GL Biochem (China)

- •CSBio, Inc. (United States)

- •Peptide International, Inc. (United States)

- •Polypeptide Group (Sweden)

- •AmbioPharm Inc. (United States)

- •Bachem Americas Inc. (United States)

- •AAPPTec (United States)

Market Breakdown

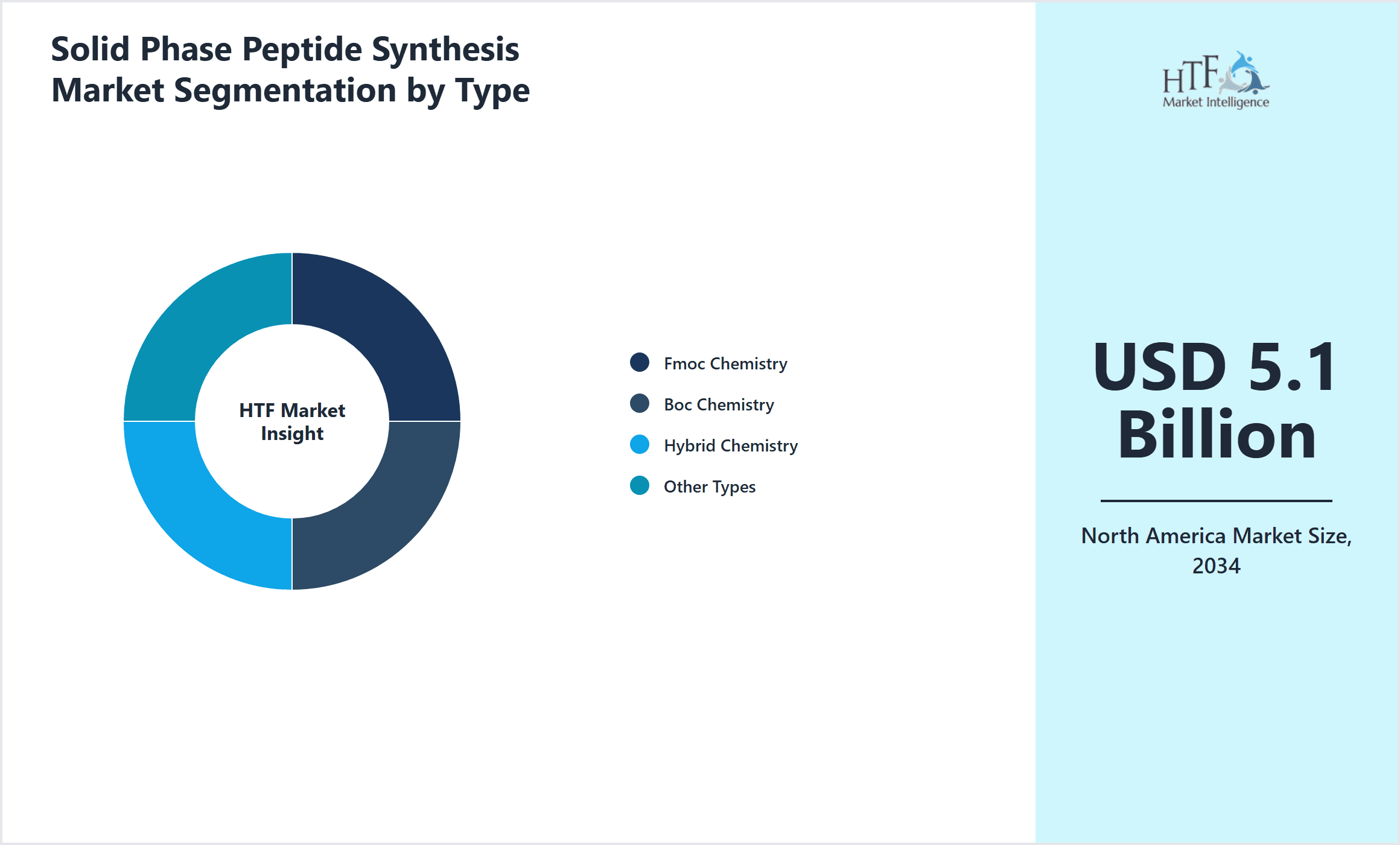

- •By Product Type

- ◦Fmoc Chemistry

- ◦Boc Chemistry

- ◦Hybrid Chemistry

- ◦Other Types

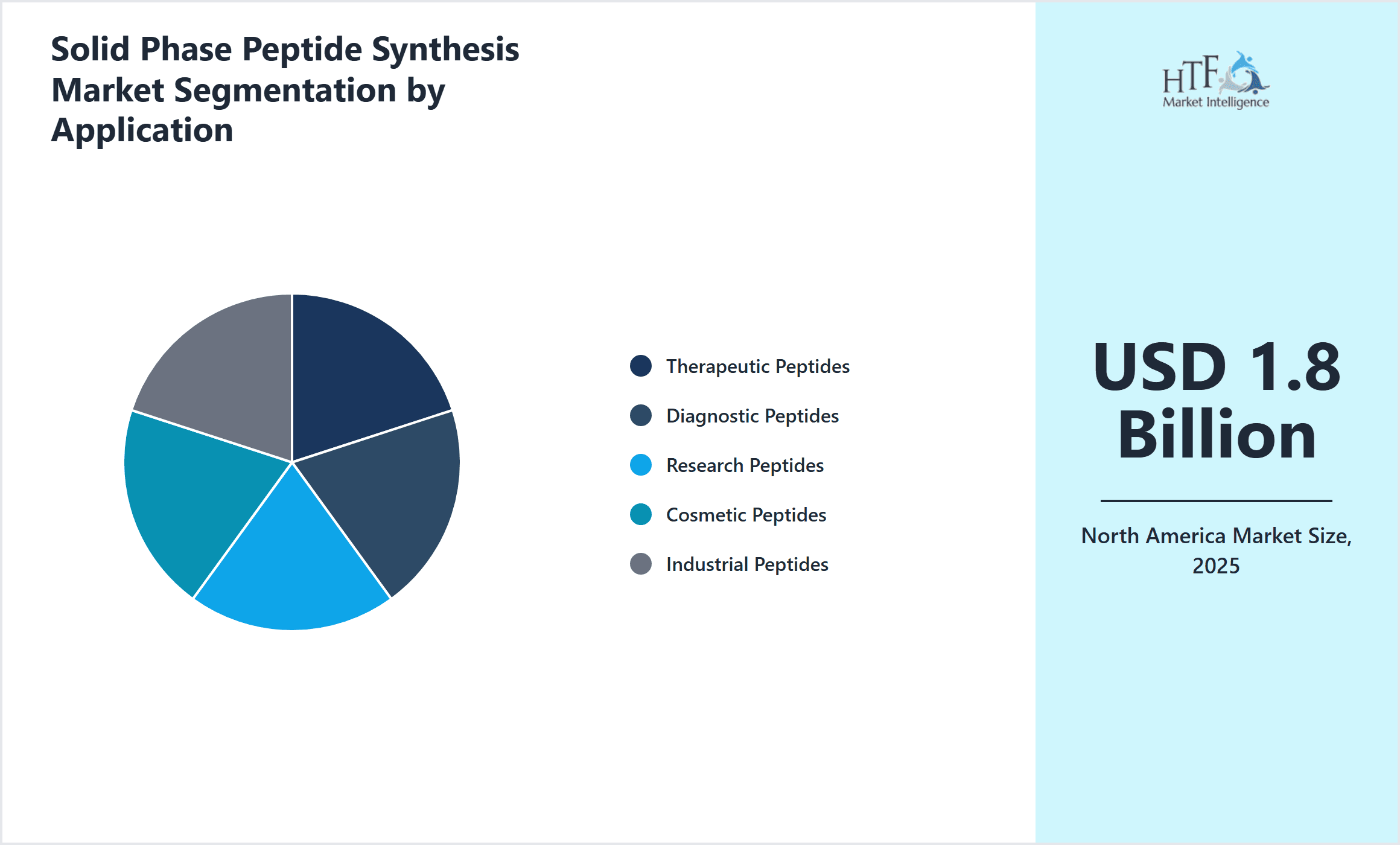

- •By Application

- ◦Therapeutic Peptides

- ◦Diagnostic Peptides

- ◦Research Peptides

- ◦Cosmetic Peptides

- ◦Industrial Peptides

- •By End-Use Industry

- ◦Pharmaceuticals

- ◦Biotechnology

- ◦Academic & Research Institutes

- ◦Cosmetics & Personal Care

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors & Dealers

- ◦Online Platforms

Growth Dynamics

The North America Solid Phase Peptide Synthesis market's growth is fueled by increasing demand for peptide-based therapeutics to address chronic and rare diseases, with pharmaceutical companies investing heavily in peptide drug development pipelines. Advances in automated synthesis technologies, such as high-throughput synthesizers and improved resin chemistries, enhance synthesis efficiency and scalability, reducing production timelines and costs. The rising prevalence of personalized medicine and peptide vaccines further propels market expansion. Additionally, expanding applications in diagnostics and cosmetics diversify revenue streams. Government funding and favorable regulatory frameworks supporting peptide research create a conducive environment for market growth. The growing biotechnology sector and collaborations among key players stimulate innovation. Furthermore, the rising awareness of peptide benefits among end-users and increased adoption in research institutions contribute to sustained demand. Overall, these drivers synergize to maintain a robust CAGR approaching 11% through 2034.

Market Trends

A prominent trend in the North America Solid Phase Peptide Synthesis market is the integration of AI and machine learning to optimize peptide design and synthesis processes, improving yield and reducing errors. The adoption of hybrid synthesis techniques combining Fmoc and Boc chemistries enables the production of complex peptides with enhanced stability. Custom peptide synthesis services are gaining traction, supported by online platforms offering rapid turnaround and flexible order sizes. Sustainability initiatives are influencing resin and reagent development toward greener chemistries with reduced environmental impact. Additionally, increasing use of peptides in personalized medicine and immunotherapy fuels innovation in targeted peptide drug development. Strategic partnerships between peptide manufacturers and pharmaceutical companies accelerate commercialization of novel therapeutics. These evolving trends are reshaping market offerings and competitive dynamics within the region.

Market Opportunities

The North America Solid Phase Peptide Synthesis market presents significant opportunities in expanding clinical applications, including peptide-based vaccines and immunotherapies addressing unmet medical needs. Emerging hybrid chemistries and automated synthesis platforms offer avenues for cost reduction and enhanced peptide complexity, enabling novel therapeutic modalities. Geographic expansion into underserved markets within Canada and Mexico can capture untapped demand. Growth in cosmetic peptides and industrial applications diversifies market potential beyond pharmaceuticals. Integration with digital technologies and bioinformatics tools to streamline peptide development pipelines creates value-added services. Strategic alliances and mergers offer pathways to broaden product portfolios and accelerate innovation. Additionally, the increasing focus on personalized medicine and rare disease therapies provides a fertile ground for tailored peptide synthesis solutions, positioning companies to capitalize on evolving healthcare trends.

Market Challenges

Despite strong growth prospects, the North America Solid Phase Peptide Synthesis market faces challenges including high production costs associated with complex peptide synthesis and expensive raw materials such as specialized resins and reagents. Regulatory complexities, including stringent quality standards and lengthy approval processes for therapeutic peptides, pose barriers to market entry and expansion. Technical challenges related to synthesizing long or cyclic peptides with high purity limit scalability. Supply chain disruptions and dependence on key chemical suppliers impact production continuity. Market fragmentation and intense competition pressure pricing and profit margins. Furthermore, environmental concerns around solvent use and waste generation necessitate investments in greener technologies, increasing operational costs. Addressing these challenges requires innovation in synthesis methods, regulatory harmonization, and strategic investments to maintain competitiveness.

Regulatory Framework

Between 2019 and 2024, North American regulatory agencies such as the FDA have implemented stricter guidelines for peptide drug manufacturing, emphasizing Good Manufacturing Practices (GMP) compliance and validation of synthesis processes to ensure product safety and efficacy. The introduction of updated USP monographs for peptide purity and identity testing has increased quality control requirements for solid phase peptide synthesis. Additionally, environmental regulations targeting solvent emissions and waste disposal have mandated greener synthesis protocols and solvent recycling initiatives. The Biologics Price Competition and Innovation Act has influenced the approval pathway for peptide biosimilars, impacting market competition. Regulatory frameworks also encourage innovation by streamlining expedited review processes for breakthrough peptide therapies. Collectively, these regulations shape manufacturing standards, quality assurance, and market access strategies within the North America peptide synthesis industry.

Market Intelligence

- •15th July 2023, Thermo Fisher Scientific Inc. launched an advanced automated solid phase peptide synthesizer featuring increased synthesis speed, enhanced purity, and integration with digital monitoring tools aimed at pharmaceutical and biotech customers in North America. This innovation supports rapid peptide drug development by reducing synthesis cycle times and enabling real-time process control, thus improving productivity and lowering costs. The new platform addresses growing demand for complex peptides in therapeutic and research applications and strengthens Thermo Fisher's position in the automated synthesis market. Source: Thermo Fisher Scientific Official Press Release

- •22nd November 2022, Bachem Holding AG introduced a novel hybrid peptide synthesis technology combining Fmoc and Boc chemistries to improve yield and purity for long-chain peptides used in oncology therapeutics. This advancement enhances manufacturing efficiency and supports the growing pipeline of complex peptide drugs requiring stringent quality standards. Bachem’s innovation is expected to accelerate commercialization timelines and expand contract manufacturing opportunities within the North America region. Source: Bachem Corporate News

- •10th March 2024, CEM Corporation announced a strategic partnership with a leading U.S. biotech firm to co-develop custom peptide synthesis solutions tailored for personalized medicine applications. The collaboration focuses on integrating automated synthesis with AI-driven design tools to optimize peptide sequences and accelerate clinical trial readiness. This initiative strengthens CEM’s market presence and addresses rising demand for bespoke peptide therapeutics in North America. Source: CEM Corporation Press Release

- •5th January 2023, Merck KGaA expanded its peptide synthesis reagent manufacturing facility in the United States, increasing capacity and introducing greener solvent technologies to comply with enhanced environmental regulations. This investment aims to meet rising domestic demand for high-quality synthesis materials and supports Merck’s sustainability objectives. The facility expansion is projected to improve supply chain resilience and reinforce Merck’s competitive edge in the North American peptide synthesis market. Source: Merck Official Statement

Regional Outlook

The United States currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Canada is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- United States

- Canada

- Mexico

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.8 Billion |

| Forecast Year Market Size | USD 5.1 Billion |

| CAGR | 11% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 11% |

| Scope of Report | Market is segmented by Product Type (Fmoc Chemistry, Boc Chemistry, Hybrid Chemistry, Other Types), Application (Therapeutic Peptides, Diagnostic Peptides, Research Peptides, Cosmetic Peptides, Industrial Peptides), End-Use Industry (Pharmaceuticals, Biotechnology, Academic & Research Institutes, Cosmetics & Personal Care), Distribution Channel (Direct Sales, Distributors & Dealers, Online Platforms) |

| Regions Covered | United States, Canada, Mexico |

| Key Companies | Thermo Fisher Scientific Inc. (United States), Bachem Holding AG (Switzerland), CEM Corporation (United States), Merck KGaA (Germany), GenScript Biotech Corporation (United States) |

North America Solid Phase Peptide Synthesis Market Size, Growth & Revenue 2024-2034 - Table of Contents

Multidisciplinary researcher with 10+ years of experience uncovering insights across diverse domains focused on uncovering insights that drive informed decisions.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.