Global Infrared Temperature Sensors Market Size, Growth & Revenue 2024-2034

Global Infrared Temperature Sensors Market is segmented by Product Type (Thermopile Sensors, Pyroelectric Sensors, Quantum Detectors, Bolometers, Thermographic Cameras), Application (Industrial Automation, Medical Diagnostics, Consumer Electronics, Automotive, Aerospace), End-Use Industry (Manufacturing, Healthcare, Automotive & Transportation, Aerospace & Defense), Distribution Channel (Direct Sales, Distributors, Online Sales), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

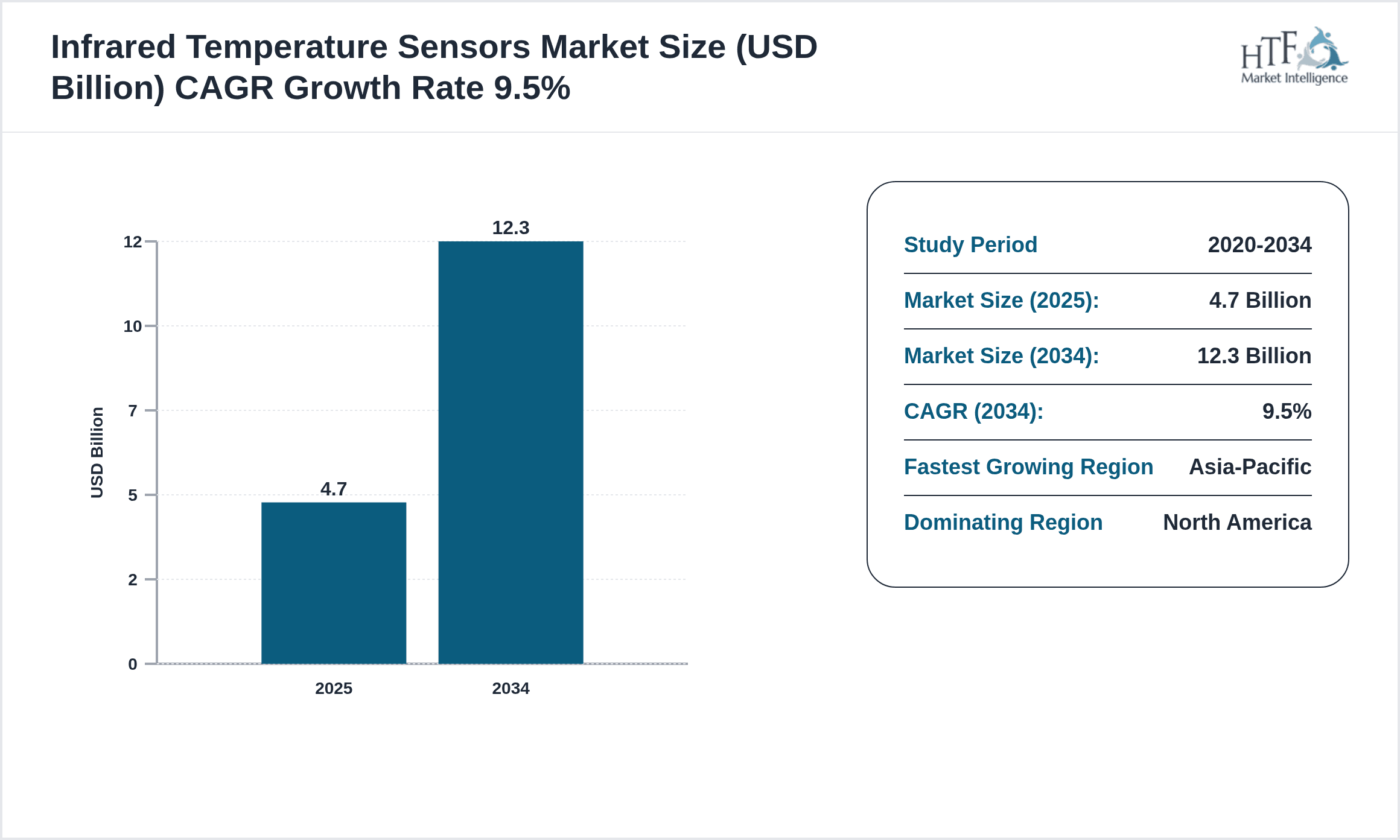

- •The Global Infrared Temperature Sensors market is defined by its provision of non-contact temperature measurement solutions using infrared radiation detection. This market spans multiple sensor technologies including thermopile sensors, pyroelectric sensors, quantum detectors, bolometers, and thermographic cameras, each tailored to specific application needs such as industrial automation, medical diagnostics, consumer electronics, automotive, and aerospace. These sensors provide critical temperature monitoring capabilities essential for process control, safety, and quality assurance across industries. The market scope encompasses research and development, manufacturing, integration with emerging technologies like IoT and artificial intelligence, and adoption across various end-use sectors worldwide. The industry is driven by increasing automation demands, healthcare innovations, and stringent regulatory standards emphasizing precision and reliability. The market's global nature reflects diverse regional growth patterns with North America dominating due to technological maturity and Asia-Pacific growing fastest owing to industrial expansion and rising healthcare infrastructure investments. Overall, infrared temperature sensors are pivotal in advancing modern thermal sensing applications with significant growth opportunities ahead.

- •Key market highlights include a robust CAGR of 9.5% projected from 2023 to 2034, with the market expanding from USD 4.7 billion in 2023 to an estimated USD 12.3 billion by 2034. Thermopile sensors currently lead the product segment due to their cost-effectiveness and broad applicability, while quantum detectors exhibit the fastest growth driven by their enhanced sensitivity and precision in specialized applications. Industrial automation remains the dominant application segment, reflecting widespread adoption in manufacturing and process control. North America holds the largest market share owing to advanced technological infrastructure and high adoption rates, whereas Asia-Pacific is the fastest-growing region fueled by rapid industrialization and healthcare sector growth. The market's growth is propelled by technological advancements, expanding application landscapes, and increasing demand for non-contact temperature measurement tools in safety-critical environments.

- •The infrared temperature sensors market offers significant value propositions through enabling accurate, real-time temperature monitoring essential for operational efficiency, safety, and compliance across multiple industries. For industrial users, these sensors enhance process automation and quality control, reducing downtime and improving product consistency. In healthcare, they facilitate non-invasive patient monitoring, improving diagnostics and patient comfort. Automotive and aerospace sectors benefit from improved safety and system monitoring enabled by advanced sensor integration. Stakeholders including manufacturers, system integrators, and end-users gain strategic advantages by leveraging cutting-edge sensor technologies to meet evolving regulatory requirements and consumer expectations. The market's strategic importance is underscored by ongoing innovations, increasing adoption in emerging economies, and integration with digital ecosystems, positioning infrared temperature sensors as critical components in the future of smart sensing and IoT-enabled environments.

Competitive Landscape

The competitive environment in the global infrared temperature sensors market is characterized by intense rivalry among established multinational corporations and emerging specialized players. Companies compete through continuous innovation, product differentiation, and strategic partnerships to expand their market footprint. Emphasis on research and development drives advancements in sensor accuracy, miniaturization, and integration capabilities, which serve as key competitive differentiators. Market leaders leverage their extensive distribution networks and brand recognition to maintain dominance, while new entrants focus on niche applications and cost-effective solutions to capture market share. Collaborative ventures, mergers, and acquisitions are common strategies to enhance technological capabilities and geographic reach. Pricing strategies are calibrated to balance profitability with competitive positioning, particularly in price-sensitive emerging markets. Additionally, firms invest in enhancing customer service and customization options, fostering long-term client relationships. The competitive landscape is further influenced by regulatory compliance requirements and the necessity to rapidly adapt to evolving industry standards, underscoring a dynamic and innovation-driven market atmosphere.

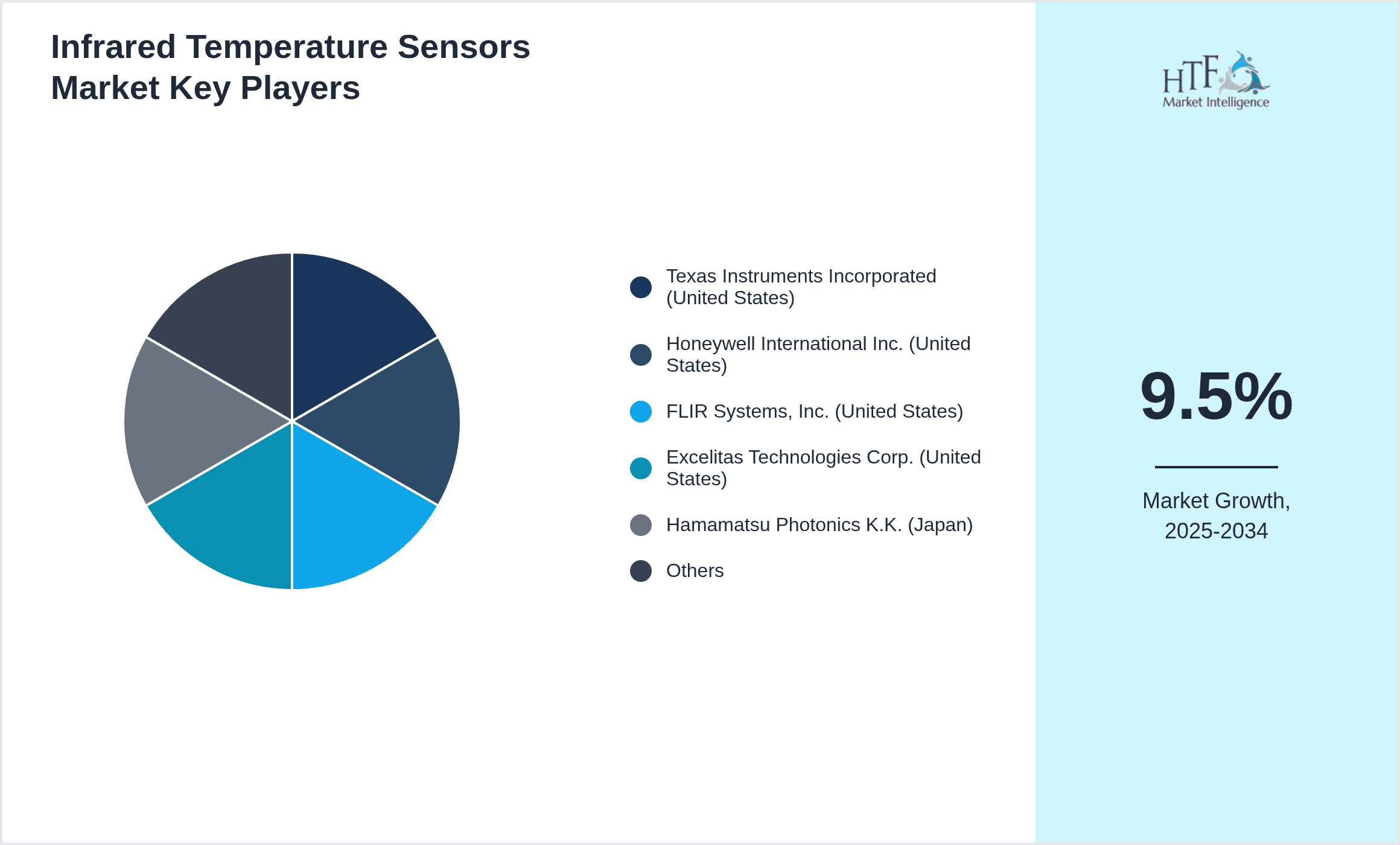

Leading Companies in Infrared Temperature Sensors Market

- •Texas Instruments Incorporated (United States)

- •Honeywell International Inc. (United States)

- •FLIR Systems, Inc. (United States)

- •Excelitas Technologies Corp. (United States)

- •Hamamatsu Photonics K.K. (Japan)

- •Murata Manufacturing Co., Ltd. (Japan)

- •LumaSense Technologies, Inc. (United States)

- •Vishay Intertechnology, Inc. (United States)

- •Raytheon Technologies Corporation (United States)

- •FLUKE Corporation (United States)

- •Sensirion AG (Switzerland)

- •Omron Corporation (Japan)

- •Amphenol Advanced Sensors (United States)

- •Nippon Ceramic Co., Ltd. (Japan)

- •Siemens AG (Germany)

- •Panasonic Corporation (Japan)

- •STMicroelectronics N.V. (Switzerland)

- •DENSO Corporation (Japan)

- •Analog Devices, Inc. (United States)

- •Infineon Technologies AG (Germany)

- •OSRAM Licht AG (Germany)

- •TE Connectivity Ltd. (Switzerland)

- •Panasonic Corporation (Japan)

- •Samsung Electronics Co., Ltd. (South Korea)

- •Bosch Sensortec GmbH (Germany)

Market Breakdown

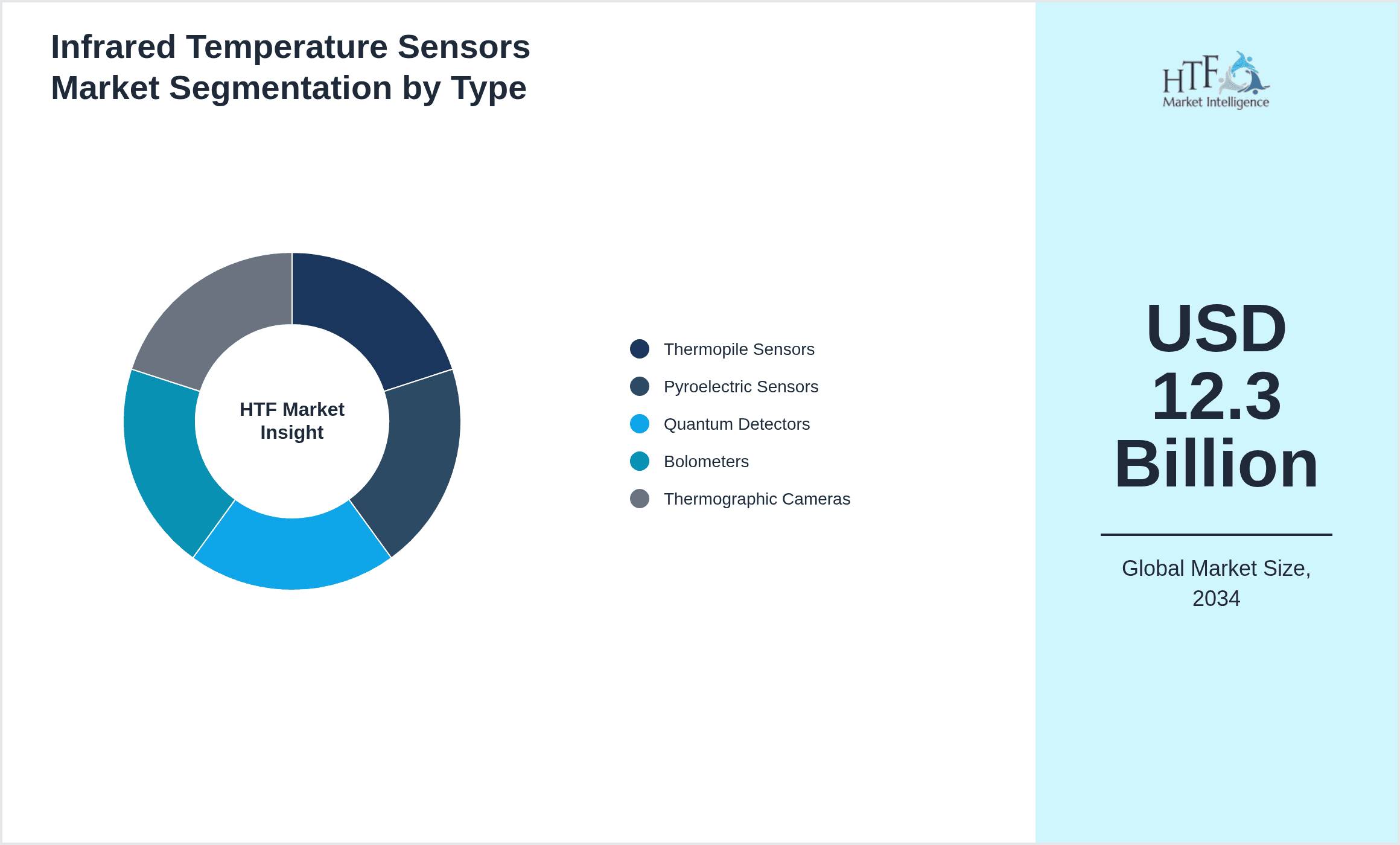

- •By Product Type

- ◦Thermopile Sensors

- ◦Pyroelectric Sensors

- ◦Quantum Detectors

- ◦Bolometers

- ◦Thermographic Cameras

- •By Application

- ◦Industrial Automation

- ◦Medical Diagnostics

- ◦Consumer Electronics

- ◦Automotive

- ◦Aerospace

- •By End-Use Industry

- ◦Manufacturing

- ◦Healthcare

- ◦Automotive & Transportation

- ◦Aerospace & Defense

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors

- ◦Online Sales

Growth Dynamics

The global infrared temperature sensors market growth is primarily driven by escalating demand for automation across manufacturing and industrial sectors, where precise, non-contact temperature measurement enhances process efficiency and safety. Increasing adoption of Industry 4.0 and smart factory initiatives accelerates sensor integration into automated systems. Additionally, the expanding healthcare sector's focus on non-invasive temperature monitoring techniques propels market growth, as infrared sensors enable accurate diagnostics and patient monitoring. Technological innovations leading to enhanced sensor sensitivity, miniaturization, and integration capabilities further stimulate adoption across diverse applications. Growing consumer electronics demand for thermal management solutions in devices also contributes significantly. The rising need for energy-efficient and reliable automotive safety systems utilizing infrared sensors fosters market expansion. Finally, regional industrialization and infrastructure development in Asia-Pacific and other emerging economies provide substantial growth opportunities, creating a favorable environment for market stakeholders to capitalize on expanding applications and technological advancements.

Market Trends

Recent trends in the infrared temperature sensors market include increased adoption of IoT-enabled sensors facilitating real-time temperature monitoring and data analytics across industries. Integration of artificial intelligence algorithms with sensor systems enables predictive maintenance and enhanced process optimization. The shift towards miniaturized and flexible sensor designs caters to wearable medical devices and compact consumer electronics. Sustainability considerations promote development of energy-efficient sensors with lower power consumption profiles. Companies are diversifying product portfolios to include multi-spectral and multi-point sensing capabilities, improving accuracy and application versatility. Collaborations between sensor manufacturers and technology firms foster innovation ecosystems accelerating product development. Additionally, the automotive sector is witnessing increased use of infrared sensors for advanced driver-assistance systems (ADAS) and occupant monitoring, reflecting a convergence of safety and comfort trends shaping market evolution globally.

Market Opportunities

The infrared temperature sensors market offers significant growth opportunities in emerging economies where industrial modernization and healthcare infrastructure investments are rapidly increasing. Expansion into untapped applications such as smart homes, environmental monitoring, and precision agriculture presents new revenue streams. Advancements in quantum detector technology open avenues for ultra-sensitive thermal imaging and scientific research applications. Strategic partnerships and collaborations between sensor manufacturers and IoT platform providers can facilitate entry into integrated solutions markets. The rising demand for contactless temperature measurement in pandemic and post-pandemic healthcare settings further accelerates opportunities for innovative product development. Additionally, leveraging artificial intelligence and machine learning for enhanced sensor data interpretation can create competitive advantages. Geographic expansion focusing on Asia-Pacific, Latin America, and the Middle East & Africa regions with growing industrial and consumer markets is poised to unlock substantial value for market participants.

Market Challenges

The infrared temperature sensors market faces several challenges including high manufacturing costs of advanced sensor types such as quantum detectors, which may limit adoption in cost-sensitive segments. Technical limitations related to sensor accuracy under varying environmental conditions and interference pose reliability concerns. The market also confronts intense competition leading to pricing pressures impacting profitability. Regulatory compliance complexities across different regions increase operational challenges for manufacturers. Additionally, supply chain disruptions and shortages of critical raw materials affect production continuity. Integration complexities with existing systems and the need for skilled personnel to manage sophisticated sensor technologies can hinder widespread deployment. Furthermore, rapid technological obsolescence requires continual investment in research and development, posing financial burdens on smaller players. Addressing these challenges is critical for sustainable market growth and maintaining competitive advantage amidst evolving industry dynamics.

Regulatory Framework

Between 2018 and 2023, regulatory frameworks impacting the infrared temperature sensors market have evolved to emphasize product safety, electromagnetic compatibility, and environmental sustainability. Key regulations include the EU's RoHS directive limiting hazardous substances in electronic components, and REACH regulations governing chemical usage affecting sensor manufacturing. The IEC 60751 standards prescribe performance and calibration requirements for temperature sensors, ensuring measurement accuracy and safety compliance. Additionally, FDA guidelines for medical device sensors mandate rigorous testing and approval processes to safeguard patient safety. Regional mandates in North America and Asia-Pacific focus on energy efficiency and emissions, influencing sensor design and deployment. Governments have introduced incentives to promote adoption of smart sensing technologies aligned with Industry 4.0 initiatives. Compliance with these evolving regulations necessitates continuous innovation and quality assurance, shaping market entry strategies and product development pipelines across geographies.

Market Intelligence

- •15th January 2024, Honeywell International Inc. launched an advanced thermopile infrared temperature sensor series featuring enhanced accuracy and reduced power consumption tailored for medical and industrial applications. The new sensors integrate seamlessly with IoT platforms, enabling real-time temperature monitoring and predictive analytics to improve operational efficiency and patient outcomes. Honeywell’s strategic focus on miniaturization and reliability positions the product line as a market leader for next-generation sensing solutions, addressing growing demand for non-contact temperature measurement technologies globally. Source: Honeywell Official Press Release

- •10th June 2023, FLIR Systems, Inc. introduced a cutting-edge thermographic camera with high-resolution imaging and AI-driven anomaly detection capabilities. Designed for industrial inspection and security applications, the camera enhances thermal visualization accuracy and operational safety. FLIR’s innovation reflects the increasing convergence of sensor technology with artificial intelligence, targeting enhanced decision-making and automation across sectors. This launch strengthens FLIR’s competitive position in the global infrared temperature sensors market amid rising demand for intelligent thermal sensing solutions. Source: FLIR Systems Corporate News

- •22nd September 2023, Texas Instruments Incorporated announced a strategic partnership with a leading IoT platform provider to develop integrated sensor modules combining infrared temperature sensing with wireless connectivity. This collaboration aims to accelerate deployment in smart manufacturing and healthcare monitoring, leveraging TI’s sensor expertise and the partner’s cloud analytics capabilities. The initiative is expected to enhance data accuracy, reduce latency, and enable scalable sensor networks addressing diverse industry needs. Source: Texas Instruments Press Release

- •7th November 2024, Excelitas Technologies Corp. completed the acquisition of a niche infrared sensor manufacturer specializing in quantum detectors, aiming to expand its product portfolio and technological capabilities. This acquisition enhances Excelitas’ market reach in high-sensitivity sensing applications including scientific research and aerospace, positioning the company for accelerated growth in emerging segments. The consolidation supports innovation-driven expansion strategies amid intensifying market competition. Source: Excelitas Technologies Corporate Announcement

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 4.7 Billion |

| Forecast Year Market Size | USD 12.3 Billion |

| CAGR | 9.5% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 9.1% |

| Scope of Report | Market is segmented by Product Type (Thermopile Sensors, Pyroelectric Sensors, Quantum Detectors, Bolometers, Thermographic Cameras), Application (Industrial Automation, Medical Diagnostics, Consumer Electronics, Automotive, Aerospace), End-Use Industry (Manufacturing, Healthcare, Automotive & Transportation, Aerospace & Defense), Distribution Channel (Direct Sales, Distributors, Online Sales) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Texas Instruments Incorporated (United States), Honeywell International Inc. (United States), FLIR Systems, Inc. (United States), Excelitas Technologies Corp. (United States), Hamamatsu Photonics K.K. (Japan), Murata Manufacturing Co., Ltd. (Japan), LumaSense Technologies, Inc. (United States), Vishay Intertechnology, Inc. (United States), Raytheon Technologies Corporation (United States), FLUKE Corporation (United States), Sensirion AG (Switzerland), Omron Corporation (Japan), Amphenol Advanced Sensors (United States), Nippon Ceramic Co., Ltd. (Japan), Siemens AG (Germany), Panasonic Corporation (Japan), STMicroelectronics N.V. (Switzerland), DENSO Corporation (Japan), Analog Devices, Inc. (United States), Infineon Technologies AG (Germany), OSRAM Licht AG (Germany), TE Connectivity Ltd. (Switzerland), Panasonic Corporation (Japan), Samsung Electronics Co., Ltd. (South Korea), Bosch Sensortec GmbH (Germany) |

Global Infrared Temperature Sensors Market Size, Growth & Revenue 2024-2034 - Table of Contents

Multidisciplinary researcher with 10+ years of experience uncovering insights across diverse domains focused on uncovering insights that drive informed decisions.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.