Global Intra-Oral Flat Panel Sensor Market Size, Growth & Revenue 2025-2034

Global Intra-Oral Flat Panel Sensor Market is segmented by Type (Complementary Metal-Oxide Semiconductor (CMOS) Sensors, Charge-Coupled Device (CCD) Sensors, Phosphor Storage Plate (PSP) Sensors, Wireless Sensors, Wired Sensors), Application (Dental Diagnostics, Orthodontics, Endodontics, Periodontics, Oral Surgery), End-Use Industry (Dental Clinics, Hospitals, Diagnostic Centers, Academic & Research Institutes), Distribution Channel (Direct Sales, Distributors, Online Sales), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global Intra-Oral Flat Panel Sensor market represents a transformative segment within digital dental imaging, focusing on flat panel digital sensors that acquire detailed intra-oral images with superior clarity and reduced radiation compared to conventional methods. This market covers sensor technologies including CMOS, CCD, phosphor storage plates, and wireless sensors, supporting applications across dental diagnostics, orthodontics, endodontics, periodontics, and oral surgery. Its scope extends worldwide, driven by rapid digitalization in dental practices, rising oral health awareness, and the need for precise diagnostic tools. These sensors facilitate enhanced clinical outcomes through real-time image acquisition, improved patient comfort, and integration with advanced dental software systems. The market’s importance is underscored by its contribution to more accurate treatment planning, reduced procedural times, and compliance with radiation safety standards. Growing investments in dental healthcare infrastructure and evolving regulatory frameworks further bolster adoption globally. This comprehensive analysis details market drivers, challenges, opportunities, and competitive dynamics shaping the industry’s growth trajectory from 2025 to 2034.

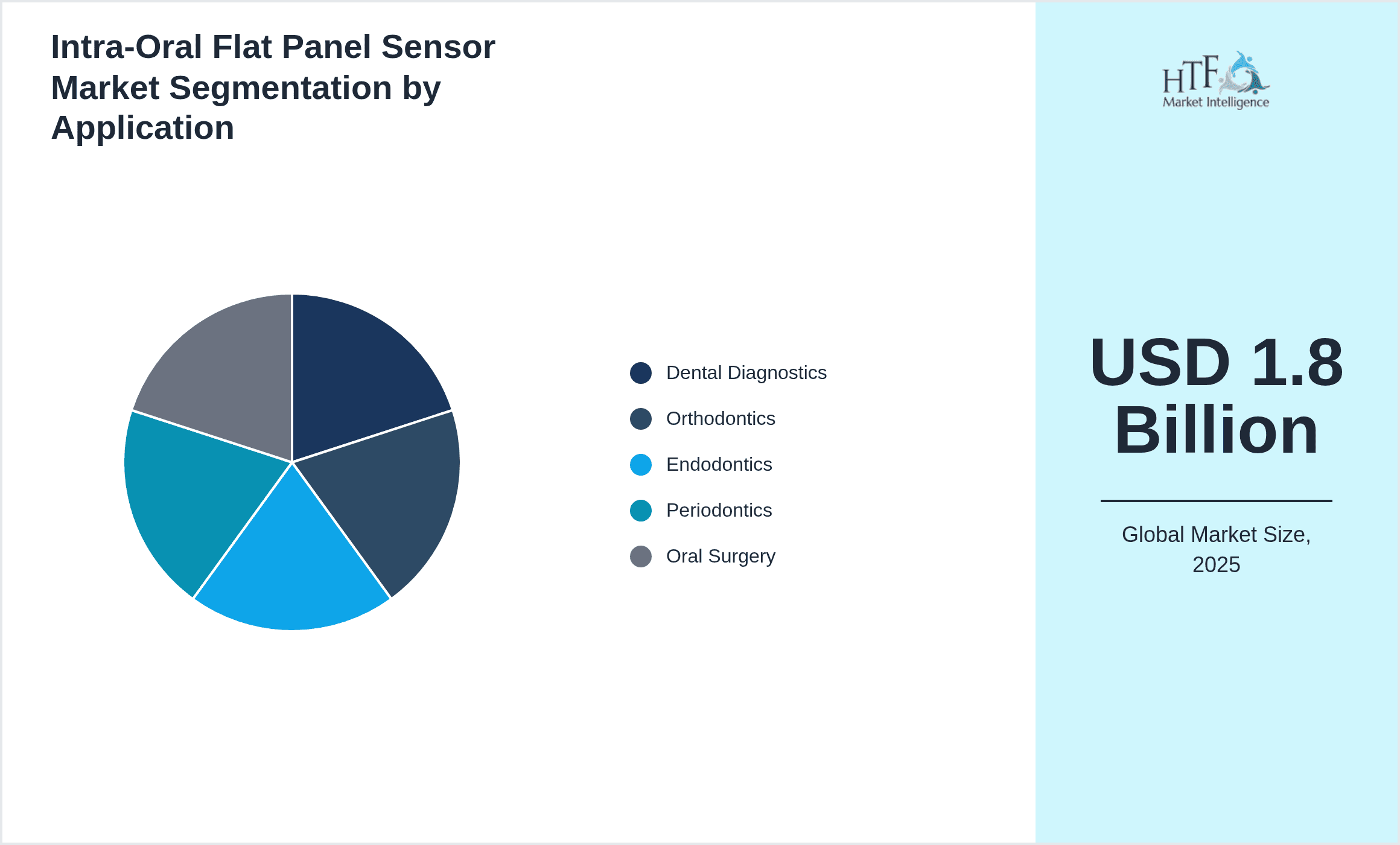

- •Key market highlights include a projected CAGR of 12.2% from 2025 to 2034, expanding the market size from USD 1.8 Billion in 2025 to USD 5.23 Billion by 2034. North America leads with the highest market share, attributed to advanced dental healthcare infrastructure and early technology adoption. Asia-Pacific exhibits the fastest growth, driven by increasing dental awareness and expanding healthcare expenditures. CMOS sensors dominate product type segments due to their high resolution and cost-effectiveness, while wireless sensors experience rapid adoption owing to ease of use and improved workflow integration. Applications in dental diagnostics hold the largest share, reflecting their critical role in routine dental examinations. Market dynamics are influenced by continuous technological innovation, increasing prevalence of dental disorders, and expanding dental service providers worldwide.

- •The market offers strategic value to dental professionals, equipment manufacturers, and healthcare providers by enabling enhanced diagnostic precision, operational efficiency, and patient safety. Development of compact, wireless, and user-friendly sensors supports seamless integration into modern dental clinics. The rising emphasis on minimally invasive dental procedures amplifies demand for high-quality imaging solutions. Additionally, regulatory initiatives to standardize digital dental imaging and radiation safety enhance market credibility. Investments in research and development foster innovation, with companies focusing on sensor sensitivity, image processing speed, and interoperability with dental practice management systems. This market’s growth significantly benefits stakeholders by driving improved patient outcomes, reducing operational costs, and expanding service capabilities across diverse geographies.

Competitive Landscape

The competitive environment in the global Intra-Oral Flat Panel Sensor market is characterized by intense innovation, strategic partnerships, and geographic expansion to maximize market penetration. Leading companies prioritize product differentiation through the development of high-resolution, wireless, and ergonomic sensor designs that enhance user experience and clinical accuracy. Emphasis on technological adoption includes integration with cloud-based dental imaging platforms and AI-driven diagnostic tools, facilitating workflow automation and improved diagnostic insights. Companies engage in collaborations with dental software providers and healthcare institutions to broaden product portfolios and accelerate adoption. Mergers and acquisitions serve as key strategies for market consolidation, enabling access to new technologies and emerging markets. Competitive pricing strategies and diversified distribution channels further strengthen market positions. Regional competition varies, with North America and Europe focusing on technological leadership while Asia-Pacific and Latin America emphasize market expansion and affordability. Future trends indicate increasing investment in R&D and sustainability initiatives to address evolving regulatory standards and environmental considerations, ensuring sustained competitive advantage.

Prominent Players in Intra-Oral Flat Panel Sensor Market

- •Carestream Health (United States)

- •Dentsply Sirona (United States)

- •Planmeca Oy (Finland)

- •Vatech Co. Ltd. (South Korea)

- •Sirona Dental Systems (Germany)

- •Gendex Dental Systems (United States)

- •Acteon Group (France)

- •Satelec (France)

- •Kodak Dental Systems (United States)

- •Owandy Radiology (France)

- •Schick Technologies (United States)

- •MyRay (Italy)

- •DEXIS (United States)

- •Sirona Dental (Germany)

- •Instrumentarium Dental (Finland)

- •Morita Corporation (Japan)

- •Carestream Dental (United States)

- •XDR Radiology (United States)

- •Suni Medical Imaging (United States)

- •Air Techniques (United States)

- •ImageWorks (United States)

- •Genoray Co. Ltd. (South Korea)

- •Esaote S.p.A. (Italy)

- •Dürr Dental AG (Germany)

- •Owandy Radiology (France)

Market Breakdown

- •By Type

- ◦Complementary Metal-Oxide Semiconductor (CMOS) Sensors

- ◦Charge-Coupled Device (CCD) Sensors

- ◦Phosphor Storage Plate (PSP) Sensors

- ◦Wireless Sensors

- ◦Wired Sensors

- •By Application

- ◦Dental Diagnostics

- ◦Orthodontics

- ◦Endodontics

- ◦Periodontics

- ◦Oral Surgery

- •By End-Use Industry

- ◦Dental Clinics

- ◦Hospitals

- ◦Diagnostic Centers

- ◦Academic & Research Institutes

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors

- ◦Online Sales

Growth Dynamics

The global Intra-Oral Flat Panel Sensor market demonstrates robust growth fueled by technological advancements such as the integration of wireless CMOS sensors that enhance imaging quality and patient comfort. Increasing global dental healthcare expenditure, especially in emerging markets, propels demand for advanced diagnostic tools. The rising prevalence of dental diseases including caries and periodontal disorders underscores the need for precise imaging solutions. Regulatory emphasis on reducing radiation exposure fosters adoption of flat panel sensors over traditional radiography. Furthermore, growing awareness of digital dentistry benefits among practitioners accelerates market penetration. Strategic collaborations between sensor manufacturers and dental software providers improve workflow efficiency. For instance, recent launches of AI-enabled imaging software integrated with flat panel sensors enable real-time diagnostics, enhancing clinical decision-making. COVID-19 pandemic-induced tele-dentistry trends have further increased demand for digital imaging technologies facilitating remote consultations. Collectively, these factors sustain CAGR above 12%, positioning the market for significant expansion through 2034.

Market Trends

Emerging trends in the Intra-Oral Flat Panel Sensor market include the rapid adoption of wireless sensor technologies that eliminate cumbersome cables, improving ergonomics and reducing infection risks. Integration of artificial intelligence and machine learning algorithms with imaging systems enhances diagnostic accuracy by automating anomaly detection and treatment planning. Manufacturers increasingly focus on developing compact, lightweight sensors with higher pixel density to deliver superior image resolution. The growing trend of personalized dental care drives demand for precise three-dimensional imaging capabilities. Additionally, adoption of cloud-based dental imaging platforms facilitates data storage, remote access, and collaborative diagnostics. Recent product launches emphasize compatibility with mobile devices, enabling portable and chair-side imaging. Sustainability initiatives prompt development of energy-efficient sensors with longer lifespans. Expansion of dental service providers in Asia-Pacific and Latin America supports market growth. These trends collectively transform clinical workflows, improve patient outcomes, and open new avenues for market innovation and expansion.

Market Opportunities

Significant opportunities arise from expanding dental healthcare infrastructure in developing regions, where increasing awareness and affordability drive demand for digital imaging solutions. The rising adoption of minimally invasive dental procedures necessitates high-precision imaging, creating opportunities for advanced flat panel sensors. Integration with tele-dentistry and remote consultation platforms offers potential for market growth by extending dental care access to underserved populations. Technological innovations in wireless sensor designs and AI-powered diagnostics provide avenues for product differentiation and competitive advantage. Collaborations between sensor manufacturers and dental equipment companies enable bundled offerings that enhance market reach. Furthermore, government initiatives promoting oral health and digital dentistry adoption facilitate market penetration. Expanding applications beyond traditional dentistry into maxillofacial surgery and implantology further diversify revenue streams. Strategic investments in R&D focusing on sensor sensitivity, image processing speed, and interoperability with emerging dental software platforms are poised to unlock new growth horizons in the forecast period.

Market Challenges

Challenges constraining the Intra-Oral Flat Panel Sensor market include high initial investment costs for advanced digital imaging systems, limiting adoption among small dental practices in price-sensitive regions. Technical complexities related to wireless sensor connectivity and compatibility with existing dental software impede seamless integration. Concerns regarding data security and patient privacy in cloud-based imaging platforms present regulatory and operational hurdles. Market fragmentation and the presence of low-cost, lower-quality sensor alternatives affect pricing and brand differentiation. Additionally, regulatory compliance with radiation safety standards varies across regions, complicating product approvals and market entry. Supply chain disruptions, as experienced during the COVID-19 pandemic, have impacted component availability and production timelines. Skilled workforce shortages in emerging markets hinder optimal utilization of sophisticated imaging technologies. Companies face challenges balancing innovation with cost-effectiveness while addressing diverse customer requirements, necessitating strategic focus on product customization and after-sales support to overcome market barriers.

Regulatory Framework

Recent regulatory developments from 2020 to 2025 emphasize stringent compliance with radiation safety and digital data protection standards impacting the Intra-Oral Flat Panel Sensor market. The European Union’s Medical Device Regulation mandates enhanced clinical evaluation and post-market surveillance for dental imaging devices, ensuring product safety and efficacy. In the United States, FDA guidance updates focus on cybersecurity requirements for connected medical devices, including wireless dental sensors, to protect patient data integrity. Additionally, HIPAA regulations reinforce confidentiality and security protocols for digital dental records. China’s National Medical Products Administration has introduced accelerated approval pathways for innovative dental imaging technologies, fostering market entry while maintaining safety standards. These regulations collectively influence product design, manufacturing processes, and market access strategies, compelling manufacturers to invest in compliance infrastructure and quality management systems. Adherence to these evolving regulatory frameworks ensures market credibility, patient safety, and sustained competitive positioning globally.

Market Intelligence

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

- •Source: Official company announcements, Industry reports, Regulatory agency publications

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.8 Billion |

| Forecast Year Market Size | USD 5.23 Billion |

| CAGR | 12.2% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 12.2% |

| Scope of Report | Market is segmented by Type (Complementary Metal-Oxide Semiconductor (CMOS) Sensors, Charge-Coupled Device (CCD) Sensors, Phosphor Storage Plate (PSP) Sensors, Wireless Sensors, Wired Sensors), Application (Dental Diagnostics, Orthodontics, Endodontics, Periodontics, Oral Surgery), End-Use Industry (Dental Clinics, Hospitals, Diagnostic Centers, Academic & Research Institutes), Distribution Channel (Direct Sales, Distributors, Online Sales) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Carestream Health (United States), Dentsply Sirona (United States), Planmeca Oy (Finland), Vatech Co. Ltd. (South Korea), Sirona Dental Systems (Germany) |

Global Intra-Oral Flat Panel Sensor Market Size, Growth & Revenue 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.