Global Electronic Sphygmomanometer Market Size, Growth & Revenue 2024-2034

Global Electronic Sphygmomanometer Market is segmented by Product Type (Upper Arm Electronic Sphygmomanometer, Wrist Electronic Sphygmomanometer, Finger Electronic Sphygmomanometer, Ambulatory Electronic Sphygmomanometer, Others), Application (Home Healthcare, Hospitals, Clinics, Ambulatory Care, Telemedicine), End-Use Industry (Healthcare Facilities, Homecare Settings, Fitness & Wellness Centers, Telehealth Services), Distribution Channel (Retail Pharmacies, E-commerce Platforms, Medical Device Distributors), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global electronic sphygmomanometer market comprises advanced blood pressure monitoring devices that leverage electronic sensors and digital displays to provide accurate, convenient, and non-invasive blood pressure readings. These devices serve a broad range of users including individual consumers, healthcare professionals, and telemedicine providers. The market scope covers diverse product types such as upper arm, wrist, finger, and ambulatory monitors, integrating connectivity features and enhanced usability. The industry is propelled by the growing incidence of hypertension worldwide, increasing demand for home healthcare solutions, and advancements in digital health technologies. With expanding applications spanning hospitals, clinics, ambulatory care centers, and telemedicine, the market supports preventive healthcare and chronic disease management. Key characteristics include portability, ease of use, and integration with mobile health applications. The market also reflects evolving consumer preferences for compact, reliable, and connected monitoring systems, reinforcing its strategic importance within the global healthcare ecosystem.

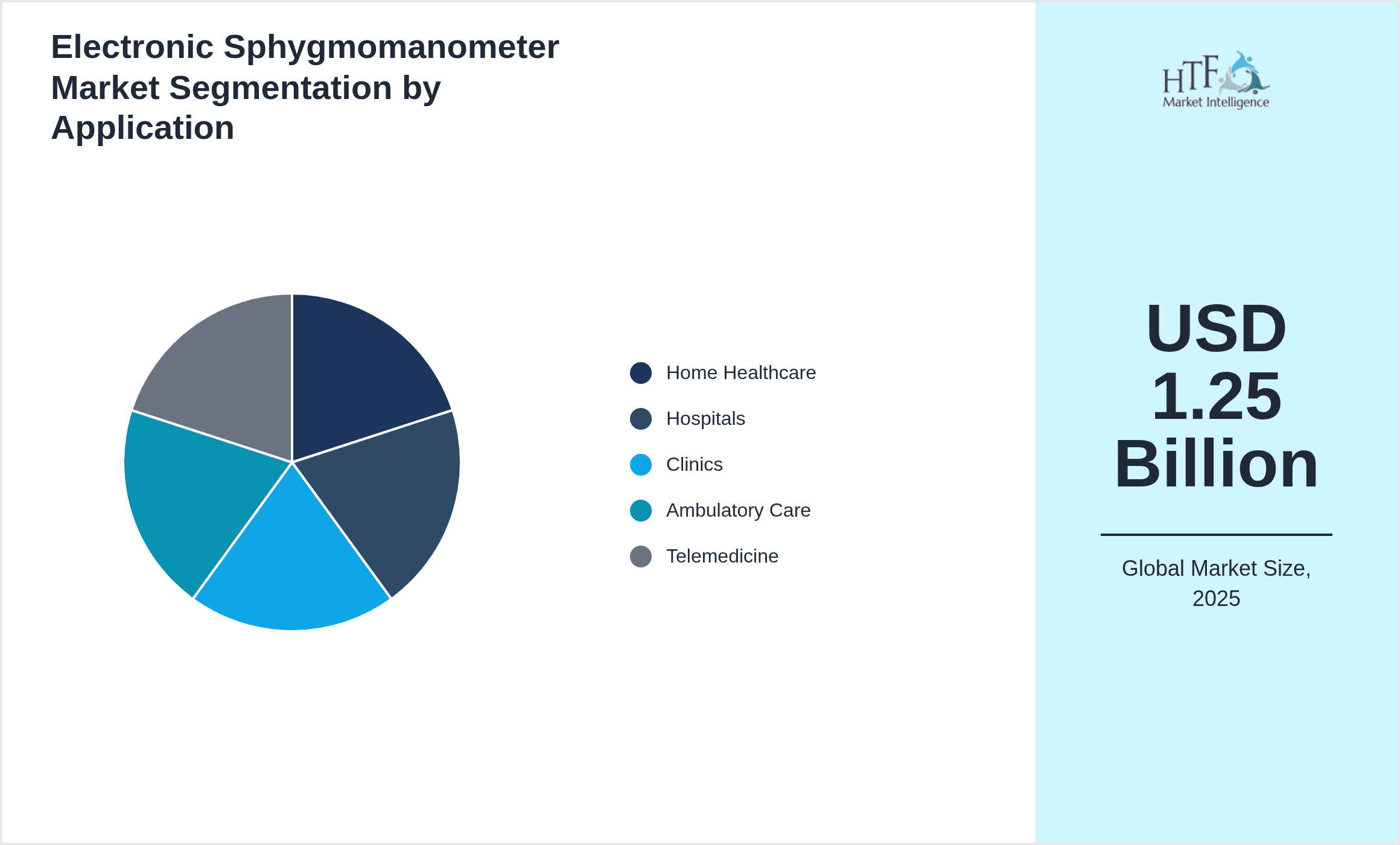

- •The market has witnessed significant growth, with a base valuation of USD 1.25 Billion in 2024 and a projected market size of USD 3.48 Billion by 2034. This growth is driven by a compound annual growth rate (CAGR) of approximately 11%, reflecting strong demand across all key regions. Key market highlights include the dominance of upper arm devices, the rapid adoption of wrist sphygmomanometers due to convenience factors, and the increasing penetration of telemedicine applications. Technological innovations such as Bluetooth-enabled devices and AI-powered analytics have enhanced product capabilities, contributing to market expansion. North America leads in market share, supported by robust healthcare infrastructure and consumer health awareness, while Asia-Pacific is the fastest-growing region due to rising healthcare expenditure and expanding middle-class populations.

- •The value proposition of electronic sphygmomanometers lies in their ability to provide accurate, user-friendly, and real-time blood pressure monitoring to diverse user groups. They play a critical role in chronic disease management, early diagnosis, and remote patient monitoring, thus reducing healthcare costs and improving patient outcomes. For healthcare providers, these devices facilitate efficient patient management and data collection, while consumers benefit from enhanced health awareness and self-monitoring capabilities. The market's strategic importance is underscored by the increasing focus on telehealth services and the rising prevalence of cardiovascular diseases globally. Stakeholders including manufacturers, distributors, healthcare institutions, and technology developers are capitalizing on the growing demand to innovate and expand their product portfolios.

Competitive Landscape

The global electronic sphygmomanometer market is highly competitive, characterized by the presence of numerous multinational corporations and regional players striving for market leadership through innovation, strategic partnerships, and aggressive marketing. Companies focus on developing technologically advanced products featuring wireless connectivity, AI integration, and enhanced user interfaces to differentiate themselves. Market rivalry intensifies with continuous product launches and expansions into emerging markets. Pricing strategies vary, with premium products targeting healthcare institutions and cost-effective models designed for home use. Distribution channels encompass direct sales, online platforms, and retail outlets, contributing to broad market penetration. Strategic collaborations and mergers & acquisitions are common to consolidate market positions and expand geographic reach. Overall, the competitive environment fosters rapid product evolution and drives adoption across both developed and developing regions.

Leading Companies in Electronic Sphygmomanometer Market

- •Omron Healthcare Inc. (Japan)

- •A&D Medical (Japan)

- •Microlife Corporation (Taiwan)

- •Beurer GmbH (Germany)

- •Welch Allyn (United States)

- •Philips Healthcare (Netherlands)

- •Nihon Kohden Corporation (Japan)

- •Withings (France)

- •iHealth Labs Inc. (United States)

- •Bosch + Sohn GmbH (Germany)

- •Andon Health Co. Ltd. (China)

- •Transtek Medical (China)

- •Rossmax International Ltd. (Switzerland)

- •Contec Medical Systems Co. Ltd. (China)

- •Citizen Systems Japan Co. Ltd. (Japan)

- •SunTech Medical, Inc. (United States)

- •Walgreens Boots Alliance Inc. (United States)

- •AcuLife (United States)

- •Beurer UK Ltd. (United Kingdom)

- •GE Healthcare (United States)

- •Nipro Corporation (Japan)

- •ForaCare Suisse AG (Switzerland)

- •Medisana AG (Germany)

- •iProvèn Medical (China)

- •ANDON Health Co., Ltd. (China)

Market Breakdown

- •By Product Type

- ◦Upper Arm Electronic Sphygmomanometer

- ◦Wrist Electronic Sphygmomanometer

- ◦Finger Electronic Sphygmomanometer

- ◦Ambulatory Electronic Sphygmomanometer

- ◦Others

- •By Application

- ◦Home Healthcare

- ◦Hospitals

- ◦Clinics

- ◦Ambulatory Care

- ◦Telemedicine

- •By End-Use Industry

- ◦Healthcare Facilities

- ◦Homecare Settings

- ◦Fitness & Wellness Centers

- ◦Telehealth Services

- •By Distribution Channel

- ◦Retail Pharmacies

- ◦E-commerce Platforms

- ◦Medical Device Distributors

Growth Dynamics

- •Increasing prevalence of hypertension worldwide is a primary driver, fueling demand for accurate and easy-to-use electronic sphygmomanometers. Rising awareness about cardiovascular health and preventive care among consumers encourages adoption of home-monitoring devices, particularly in developed regions.

- •Technological advancements such as Bluetooth connectivity, mobile app integration, and AI-powered analytics enable real-time monitoring and personalized health insights, enhancing user experience and clinical utility. These innovations are driving product differentiation and market expansion.

- •Growing telemedicine adoption, accelerated by the COVID-19 pandemic, expands the market significantly as remote patient monitoring becomes a standard healthcare practice. Electronic sphygmomanometers serve as essential tools for virtual consultations and continuous health tracking.

- •Demographic shifts including aging populations in North America, Europe, and Asia-Pacific increase demand for chronic disease management solutions, contributing to sustained market growth. Elderly patients prefer non-invasive, easy-to-operate devices to manage hypertension at home.

- •Government initiatives promoting digital health and reimbursement policies supporting remote monitoring devices further incentivize the adoption of electronic sphygmomanometers across various healthcare settings globally.

- •Rising disposable incomes and expanding middle-class populations in emerging markets, especially Asia-Pacific and Latin America, create new opportunities for market penetration and product affordability.

- •Increasing partnerships between device manufacturers and healthcare providers facilitate integrated monitoring solutions, fostering ecosystem development and enhancing market growth potential.

Market Trends

- •There is a notable trend towards miniaturization and portability, with manufacturers developing compact wrist and finger monitors favored by active users for convenience and mobility. These devices are increasingly equipped with smart features to sync with health apps.

- •Integration of electronic sphygmomanometers into comprehensive digital health platforms is becoming common, enabling data sharing across healthcare providers and patients, improving chronic disease management and patient engagement.

- •Sustainability and eco-friendly product designs are emerging trends, with companies focusing on reducing battery waste and using recyclable materials, aligning with global environmental concerns.

- •The rise of subscription-based models and device-as-a-service offerings is transforming the market, providing consumers with affordable access to the latest technology and continuous product upgrades.

- •Enhanced focus on user experience and ergonomic designs leads to the development of intuitive interfaces and customizable settings, catering to elderly and tech-savvy user segments alike.

- •Collaborations between tech companies and traditional medical device manufacturers are fostering innovation, combining expertise in digital health and clinical accuracy to offer next-generation sphygmomanometers.

- •Increasing adoption of wireless and cloud-based data storage solutions enables seamless remote monitoring and supports the growth of telehealth services globally.

Market Opportunities

- •Emerging markets in Asia-Pacific and Latin America present significant growth potential due to rising healthcare expenditure, increasing awareness, and growing demand for home healthcare monitoring devices, creating substantial market expansion opportunities.

- •Innovations in wearable technology and integration with smartphones and smartwatches offer opportunities for product diversification and enhanced consumer appeal, enabling continuous health monitoring beyond traditional devices.

- •Expanding telemedicine infrastructure globally opens avenues for partnerships with healthcare providers and payers to integrate electronic sphygmomanometers into remote patient management programs, driving demand and adoption.

- •Product development focusing on multi-parameter monitoring combining blood pressure with other vital signs such as heart rate and oxygen saturation enhances value propositions and broadens market reach.

- •Strategic collaborations and acquisitions aimed at technological enhancement and geographic expansion can accelerate market penetration and competitive positioning for key players.

- •Growing health consciousness and preventive healthcare trends globally create opportunities for educational campaigns and direct-to-consumer marketing, boosting product uptake.

- •Government incentives and reimbursement policies favoring digital health devices encourage innovation and market entry for new devices meeting regulatory standards.

Market Challenges

- •High cost of advanced electronic sphygmomanometers limits affordability and accessibility in low-income regions, constraining market growth despite rising demand for home healthcare solutions.

- •Lack of standardization in device accuracy and calibration across manufacturers creates concerns among healthcare professionals about reliability, impacting clinical adoption rates.

- •Regulatory complexities and lengthy approval processes in various countries delay product launches and increase development costs, posing challenges for market entrants and established players alike.

- •Data privacy and cybersecurity concerns related to connected devices and cloud data storage deter some consumers from adopting digital sphygmomanometers, requiring robust security measures.

- •Intense competition and rapid technological changes necessitate continuous R&D investment, which may strain resources for smaller manufacturers and hinder their market participation.

- •User errors in device operation and interpretation of readings, particularly among elderly or non-technical users, affect device effectiveness and market reputation.

- •Supply chain disruptions and component shortages, as witnessed during recent global events, impact production schedules and product availability, affecting market stability.

Regulatory Framework

- •Between 2019 and 2024, the FDA updated its guidance on digital health devices, emphasizing stringent accuracy and safety standards for electronic sphygmomanometers marketed in the United States. Compliance with these regulations ensures device reliability and consumer protection, influencing product design and testing protocols.

- •The European Union implemented the Medical Device Regulation (MDR) in 2021, which introduced more rigorous clinical evaluation requirements and post-market surveillance obligations for sphygmomanometer manufacturers. This regulatory shift requires enhanced transparency and traceability in product lifecycle management.

- •In China, the National Medical Products Administration (NMPA) mandated updated certification processes for electronic medical devices in 2022, streamlining approvals but increasing documentation and testing requirements to align with international standards.

- •Several countries have introduced data privacy laws impacting connected sphygmomanometers, requiring manufacturers to implement robust encryption and data protection measures to safeguard patient information during transmission and storage.

- •Government initiatives promoting telehealth and remote patient monitoring have resulted in revised reimbursement policies supporting the inclusion of electronic sphygmomanometers in healthcare plans, facilitating broader market access and adoption.

Market Intelligence

- •15th January 2025, Omron Healthcare Inc. launched its latest wrist electronic sphygmomanometer featuring enhanced Bluetooth connectivity, a mobile app with AI-driven health analytics, and a compact design targeted at active users seeking convenience and precision. This product aims to strengthen Omron’s market position in the wearable health device segment, responding to growing consumer demand for integrated digital health solutions. The launch aligns with global trends emphasizing remote patient monitoring and real-time health data accessibility, supporting clinical and personal health management.

- •10th March 2025, Microlife Corporation introduced an innovative upper arm sphygmomanometer with multi-parameter vital sign monitoring, including blood pressure, heart rate, and arrhythmia detection. The device incorporates wireless data transmission capabilities compatible with telehealth platforms, facilitating remote patient management. This launch enhances Microlife’s portfolio by offering comprehensive monitoring solutions for both clinical and home settings, meeting rising demand for integrated digital health tools.

- •22nd May 2025, Philips Healthcare announced a strategic partnership with a leading telemedicine provider to integrate its electronic sphygmomanometers into virtual care platforms. This collaboration aims to enhance remote patient monitoring capabilities by combining Philips’ accurate devices with telehealth services, expanding accessibility and improving chronic disease management. The initiative reflects industry-wide shifts towards connected healthcare ecosystems and patient-centric service models.

- •5th September 2025, Beurer GmbH completed the acquisition of a wearable health tech startup specializing in AI-driven blood pressure monitoring solutions. This acquisition expands Beurer’s technological capabilities and accelerates development of intelligent sphygmomanometers with predictive health analytics. The move strengthens Beurer’s competitive position and innovation pipeline in the increasingly digitalized healthcare market.

- •Source: Official company press releases, Industry publications

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.25 Billion |

| Forecast Year Market Size | USD 3.48 Billion |

| CAGR | 10.98% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 10.48% |

| Scope of Report | Market is segmented by Product Type (Upper Arm Electronic Sphygmomanometer, Wrist Electronic Sphygmomanometer, Finger Electronic Sphygmomanometer, Ambulatory Electronic Sphygmomanometer, Others), Application (Home Healthcare, Hospitals, Clinics, Ambulatory Care, Telemedicine), End-Use Industry (Healthcare Facilities, Homecare Settings, Fitness & Wellness Centers, Telehealth Services), Distribution Channel (Retail Pharmacies, E-commerce Platforms, Medical Device Distributors) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Omron Healthcare Inc. (Japan), A&D Medical (Japan), Microlife Corporation (Taiwan), Beurer GmbH (Germany), Welch Allyn (United States), Philips Healthcare (Netherlands), Nihon Kohden Corporation (Japan), Withings (France), iHealth Labs Inc. (United States), Bosch + Sohn GmbH (Germany), Andon Health Co. Ltd. (China), Transtek Medical (China), Rossmax International Ltd. (Switzerland), Contec Medical Systems Co. Ltd. (China), Citizen Systems Japan Co. Ltd. (Japan), SunTech Medical, Inc. (United States), Walgreens Boots Alliance Inc. (United States), AcuLife (United States), Beurer UK Ltd. (United Kingdom), GE Healthcare (United States), Nipro Corporation (Japan), ForaCare Suisse AG (Switzerland), Medisana AG (Germany), iProvèn Medical (China), ANDON Health Co., Ltd. (China) |

Global Electronic Sphygmomanometer Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.