Global Rotational Molding Products Market Size, Growth & Revenue 2025-2034

Global Rotational Molding Products Market is segmented by Type (Polyethylene, Polypropylene, Polyvinyl Chloride, Nylon, Other Polymers), Application (Automotive, Storage Tanks, Industrial Containers, Marine, Consumer Goods), End-Use Industry (Automotive Manufacturing, Agriculture, Chemical Processing, Marine Industry), Distribution Channel (Direct Sales, Distributors, Online Platforms), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global rotational molding products market includes manufacturing hollow plastic components using a rotational molding process that heats and rotates polymer materials inside molds to produce uniform, seamless parts. Key products range from automotive components and industrial containers to marine products and consumer goods, utilizing polymers such as polyethylene, polypropylene, PVC, and nylon. This market serves diverse industries including automotive, industrial manufacturing, storage solutions, and marine applications. Rotational molding is critical due to its ability to produce complex shapes with consistent wall thickness and cost-effectiveness for low to medium production volumes. The technology's flexibility, combined with growing demand for lightweight and durable plastic products globally, positions rotational molding as a vital manufacturing method. Increasing environmental regulations and material innovations further expand its applications. The market is characterized by steady growth driven by industrialization, infrastructure development, and rising consumer demand across major global regions.

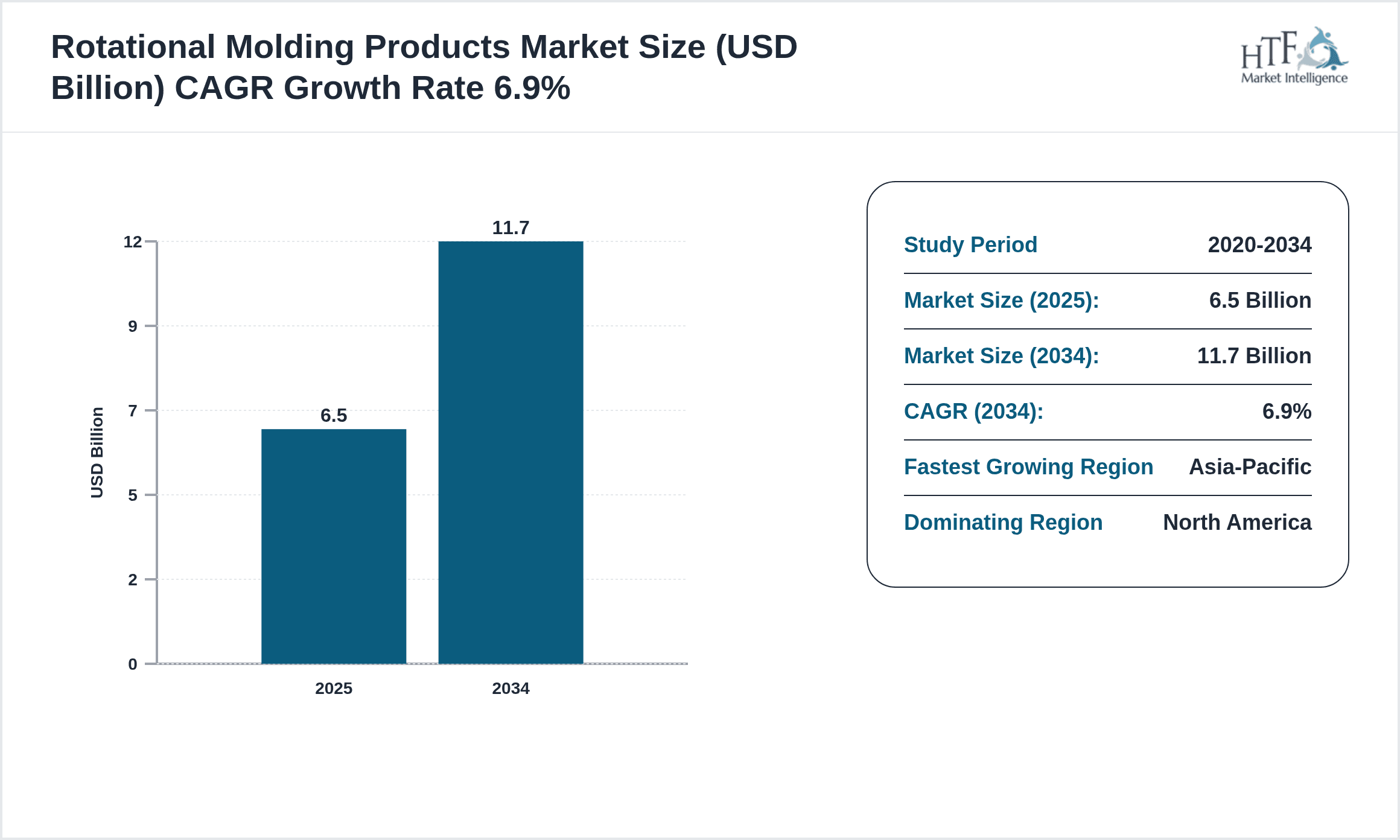

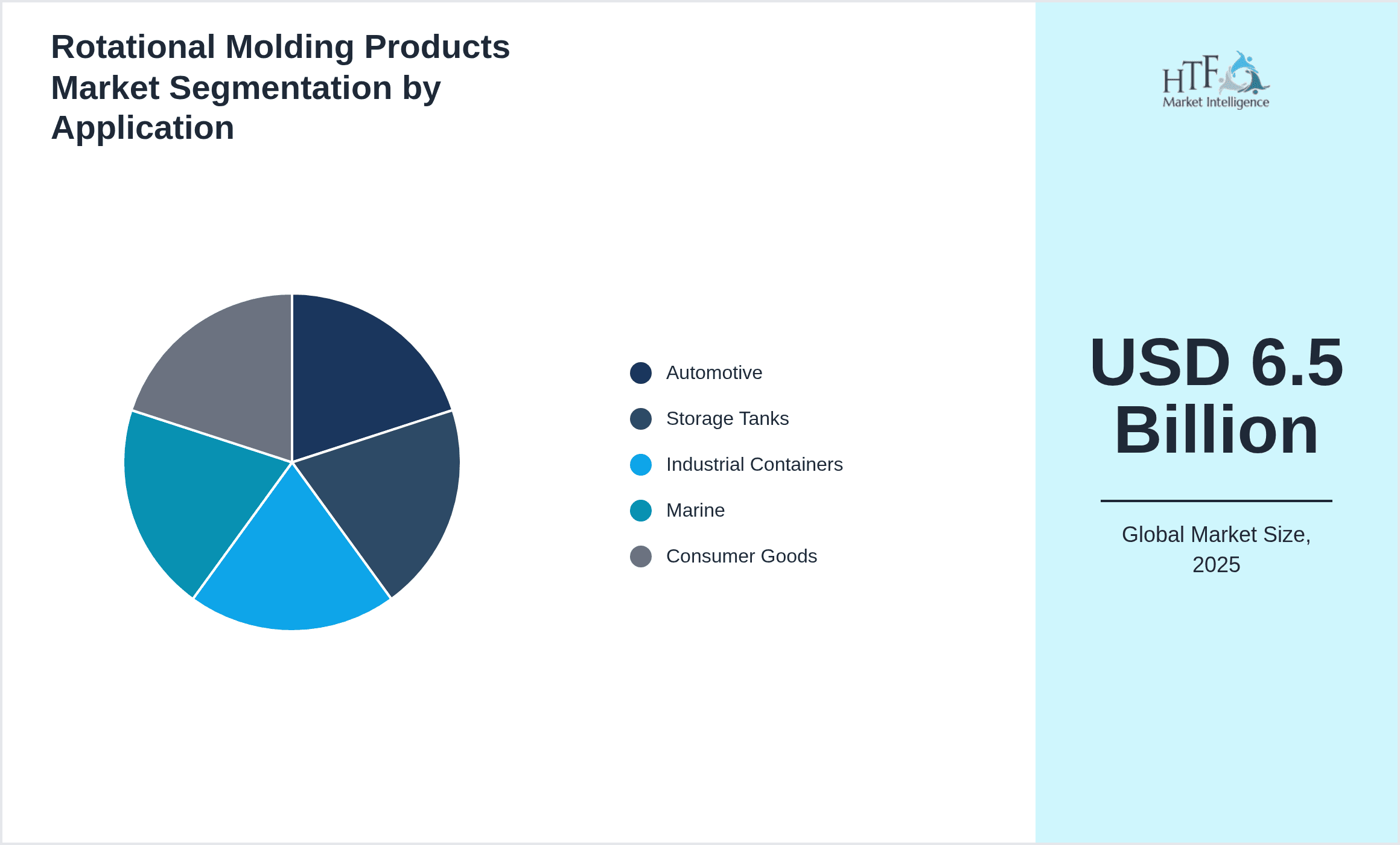

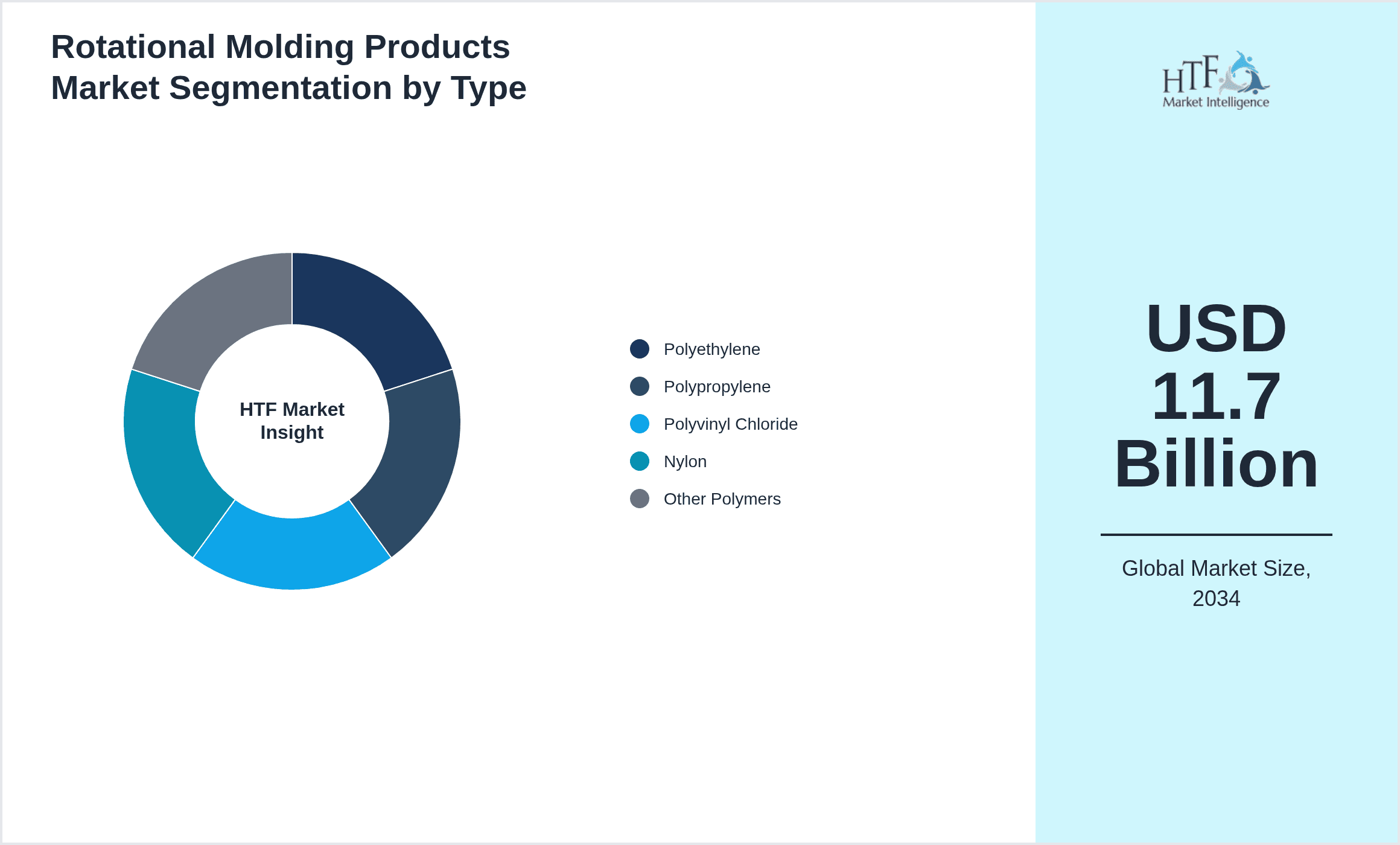

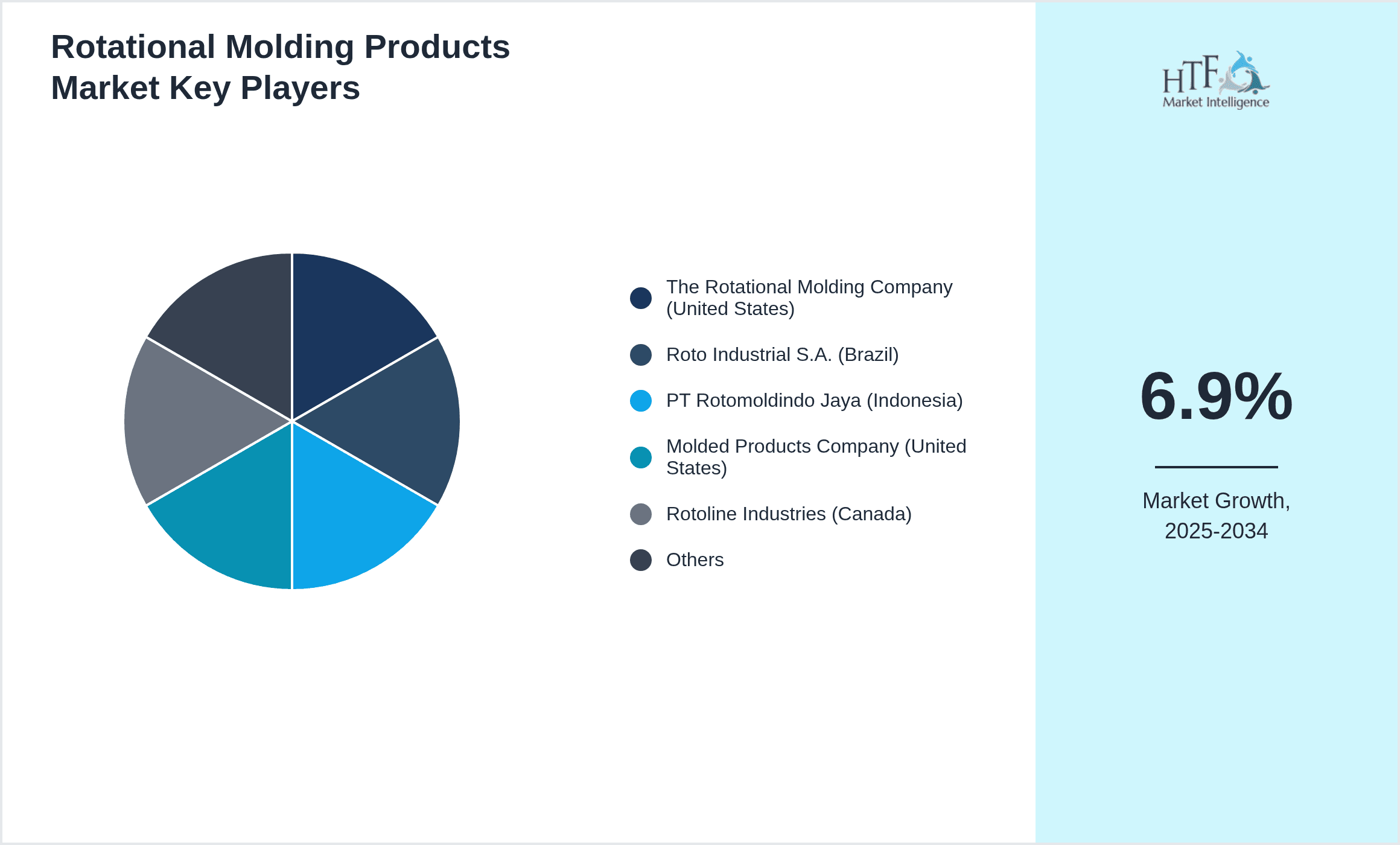

- •The global market size stood at USD 6.5 Billion in 2025 and is projected to grow to USD 11.7 Billion by 2034, reflecting a robust CAGR of 6.9%. North America holds the largest share due to advanced manufacturing infrastructure, while Asia-Pacific is the fastest-growing region propelled by expanding automotive and industrial sectors. Polyethylene dominates product types, accounting for the largest market share, whereas nylon exhibits the highest growth rate owing to its superior mechanical properties. Automotive and storage tank applications lead the demand segments, fueled by increasing vehicle production and water storage needs worldwide. Market players focus on product innovation, sustainability, and regional expansion to capitalize on emerging opportunities. The competitive landscape is marked by strategic partnerships and technological advancements enhancing product offerings and supply chain efficiency.

- •Rotational molding products offer significant value propositions including design versatility, lower tooling costs, and the ability to produce large, hollow parts with excellent mechanical properties. These advantages support industries in reducing weight and enhancing product durability, contributing to cost savings and performance improvements. The market’s strategic importance extends to sectors such as automotive, where lightweight components improve fuel efficiency, and marine, where corrosion-resistant parts extend service life. Additionally, the plastics industry's shift toward sustainable materials aligns with rotational molding's potential for recyclable polymers. Stakeholders benefit from the market's growth by leveraging innovative technologies and expanding into emerging regions with increasing industrial activities, thus fostering competitive advantage and long-term profitability.

Competitive Landscape

The competitive environment in the global rotational molding products market is shaped by companies employing strategies such as technological innovation, strategic mergers and acquisitions, and global expansion to sustain and enhance their market positions. Firms invest heavily in research and development to improve polymer formulations and molding processes, focusing on enhancing product durability, reducing cycle times, and enabling complex geometries. Partnerships with raw material suppliers and end-users enable customization and supply chain optimization. Market leaders adopt digital manufacturing technologies including automation and IoT-enabled equipment to increase operational efficiency and product quality. Competitive pricing strategies combined with a focus on sustainable and recyclable materials address evolving regulatory standards and consumer preferences. Regional diversification efforts target high-growth areas like Asia-Pacific to capture emerging demand, while established players in North America and Europe consolidate their presence through service excellence and product portfolio expansion. Future trends indicate intensified competition around innovation and sustainability initiatives.

Leading Companies in Rotational Molding Products Market

- •The Rotational Molding Company (United States)

- •Roto Industrial S.A. (Brazil)

- •PT Rotomoldindo Jaya (Indonesia)

- •Molded Products Company (United States)

- •Rotoline Industries (Canada)

- •Polymer Rotomolding Ltd. (United Kingdom)

- •Roto Plastics Pvt Ltd (India)

- •Lind Plastics (Germany)

- •Rotomold Solutions Inc. (United States)

- •S & S Rotomolding (Australia)

- •Mega Rotomolding (Mexico)

- •Roto-Tech (South Korea)

- •Rotomold Manufacturing Inc. (United States)

- •Sunrise Rotomolding (China)

- •Rotomold Europe (Netherlands)

- •Plastics Rotomolding Corporation (Italy)

- •Advanced Rotational Molding (France)

- •Rotoform Ltd. (United Kingdom)

- •Global Rotomolding Solutions (United States)

- •Rotoplast GmbH (Germany)

- •Poly Rotomolding Inc. (Canada)

- •Rototech Industries (Japan)

- •Omega Rotomolding (South Africa)

- •Pacific Rotomolding (New Zealand)

- •Techmold Rotomolding (Russia)

Market Breakdown

- •By Type

- ◦Polyethylene

- ◦Polypropylene

- ◦Polyvinyl Chloride

- ◦Nylon

- ◦Other Polymers

- •By Application

- ◦Automotive

- ◦Storage Tanks

- ◦Industrial Containers

- ◦Marine

- ◦Consumer Goods

- •By End-Use Industry

- ◦Automotive Manufacturing

- ◦Agriculture

- ◦Chemical Processing

- ◦Marine Industry

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors

- ◦Online Platforms

Growth Dynamics

Global rotational molding products market experiences robust growth driven by rapid industrialization and infrastructure development in emerging economies. Increasing demand for lightweight and durable automotive components enhances the adoption of rotational molding technology, especially with polyethylene products. Expansion of water storage and chemical containment infrastructure globally fuels applications in storage tanks and industrial containers. Technological advancements in polymer materials, such as nylon with enhanced mechanical properties, contribute to product diversification and market expansion. Environmental regulations promoting recyclable plastics and sustainable manufacturing practices drive innovation. Strategic investments by market leaders in Asia-Pacific accelerate capacity expansions, contributing to the region’s fastest growth. The growing marine industry demands corrosion-resistant components, further bolstering market prospects. Rising consumer awareness about product quality and design flexibility supports rotational molding adoption in consumer goods sectors worldwide, reinforcing steady market momentum over the forecast period.

Market Trends

The rotational molding products market is evolving with increased focus on sustainable and bio-based polymers to address environmental concerns. Industry players integrate digital manufacturing technologies, including automation and AI-driven process controls, enhancing production efficiency and reducing waste. Emerging trends include development of multi-layer rotational molding allowing composite material integration for improved product performance. The automotive sector shifts toward electric vehicles, requiring specialized rotational molded components with lightweight and thermal management properties. Expanding applications in the marine and agricultural industries highlight the versatility of rotational molding. Regional diversification, particularly growth in Asia-Pacific due to infrastructure investments, reshapes global market dynamics. Collaborations between polymer manufacturers and molders foster innovation in material science, propelling the introduction of high-performance polymers like nylon. These trends position the market for sustainable growth, technological leadership, and expanded application horizons through 2034.

Market Opportunities

Significant opportunities arise from increasing demand for customized, high-performance rotational molded products in sectors such as automotive, agriculture, and marine. Emerging markets in Asia-Pacific and Latin America offer expansion potential due to growing manufacturing bases and infrastructural development. Innovations in polymer blends and composites enable enhanced product functionalities, opening avenues for new applications and premium products. Regulatory emphasis on sustainability promotes development of recyclable and bio-based polymers, creating niches for eco-friendly rotational molding solutions. Strategic alliances and joint ventures facilitate technology transfer and market penetration, especially in developing regions. Advancements in automation and digitalization reduce production costs and improve scalability, enabling manufacturers to serve diverse customer needs effectively. The rise of electric vehicles and smart farming equipment further boosts demand for rotational molded components, supporting long-term growth and profitability.

Market Challenges

The rotational molding products market faces challenges including high initial capital investment for advanced molding equipment and tooling. Technical limitations in cycle times compared to other molding methods constrain high-volume production scalability. Raw material price volatility, especially for specialty polymers like nylon, affects profit margins and pricing strategies. Regulatory compliance with environmental standards requires continuous innovation in polymer formulations, increasing R&D expenses. Competition from alternative manufacturing processes such as injection molding and blow molding limits market share in certain applications. Supply chain disruptions and logistics complexities, exacerbated by global events, impact timely delivery and cost management. Additionally, shortage of skilled workforce with expertise in rotational molding technology hinders operational efficiency. These factors create obstacles that companies must address through strategic planning and investment to sustain market growth.

Regulatory Framework

Recent regulations have focused on promoting sustainable manufacturing and reducing environmental impact within the plastics industry. The European Union’s 2021 Circular Economy Action Plan mandates increased use of recyclable materials and restricts single-use plastics, influencing rotational molding polymer selections. North America has implemented stricter emissions and waste management standards for manufacturing facilities between 2020 and 2025, requiring compliance with EPA guidelines. Asia-Pacific countries have introduced regulations encouraging the adoption of bio-based polymers and sustainable production methods, supported by government incentives. These regulations drive innovation in polymer chemistry and manufacturing processes to meet compliance while maintaining product performance. Industry players must align strategies with evolving regulatory landscapes across regions to ensure market access and avoid penalties, emphasizing sustainability and environmental responsibility in product development and operations.

Market Intelligence

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 6.5 Billion |

| Forecast Year Market Size | USD 11.7 Billion |

| CAGR | 6.9% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 6.7% |

| Scope of Report | Market is segmented by Type (Polyethylene, Polypropylene, Polyvinyl Chloride, Nylon, Other Polymers), Application (Automotive, Storage Tanks, Industrial Containers, Marine, Consumer Goods), End-Use Industry (Automotive Manufacturing, Agriculture, Chemical Processing, Marine Industry), Distribution Channel (Direct Sales, Distributors, Online Platforms) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | The Rotational Molding Company (United States), Roto Industrial S.A. (Brazil), PT Rotomoldindo Jaya (Indonesia), Molded Products Company (United States), Rotoline Industries (Canada), Polymer Rotomolding Ltd. (United Kingdom), Roto Plastics Pvt Ltd (India), Lind Plastics (Germany), Rotomold Solutions Inc. (United States), S & S Rotomolding (Australia), Mega Rotomolding (Mexico), Roto-Tech (South Korea), Rotomold Manufacturing Inc. (United States), Sunrise Rotomolding (China), Rotomold Europe (Netherlands), Plastics Rotomolding Corporation (Italy), Advanced Rotational Molding (France), Rotoform Ltd. (United Kingdom), Global Rotomolding Solutions (United States), Rotoplast GmbH (Germany), Poly Rotomolding Inc. (Canada), Rototech Industries (Japan), Omega Rotomolding (South Africa), Pacific Rotomolding (New Zealand), Techmold Rotomolding (Russia) |

Global Rotational Molding Products Market Size, Growth & Revenue 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.