North America Automotive Central Locking Market Size, Growth & Revenue 2024-2034

North America Automotive Central Locking Market is segmented by Type (Remote Keyless Systems, Passive Keyless Entry Systems, Central Door Locking Systems, Smart Locking Systems, Manual Locking Systems), Application (Passenger Cars, Commercial Vehicles, Electric Vehicles, Two-Wheelers, Aftermarket), End-Use Industry (Automotive OEMs, Aftermarket Suppliers, Fleet Operators, Vehicle Rental Services), Distribution Channel (Original Equipment Manufacturer (OEM), Aftermarket Retail, Online Sales), and Geography (United States, Canada, Mexico)

Pricing

Report Overview

Executive Summary

- •The North America Automotive Central Locking market is a crucial segment within the automotive security and convenience domain, comprising a variety of locking technologies designed to secure vehicle access across passenger, commercial, and electric vehicles. The market includes traditional manual locking systems, remote keyless entry, passive keyless entry, and emerging smart locking mechanisms, reflecting the increasing integration of electronics and wireless technologies into vehicle security. The scope spans OEM installations and aftermarket upgrades, responding to rising consumer demand for enhanced security features and ease of use. This market is driven by automotive safety regulations, technological innovation such as IoT-enabled locks, and the proliferation of electric and autonomous vehicles requiring sophisticated access control. Geographically, the market covers the United States, Canada, and Mexico, with the U.S. leading in market size due to its mature automotive industry and high consumer adoption of advanced locking systems. The segment also captures the rising necessity for vehicle anti-theft solutions amid increasing vehicle theft incidents and insurance industry demands.

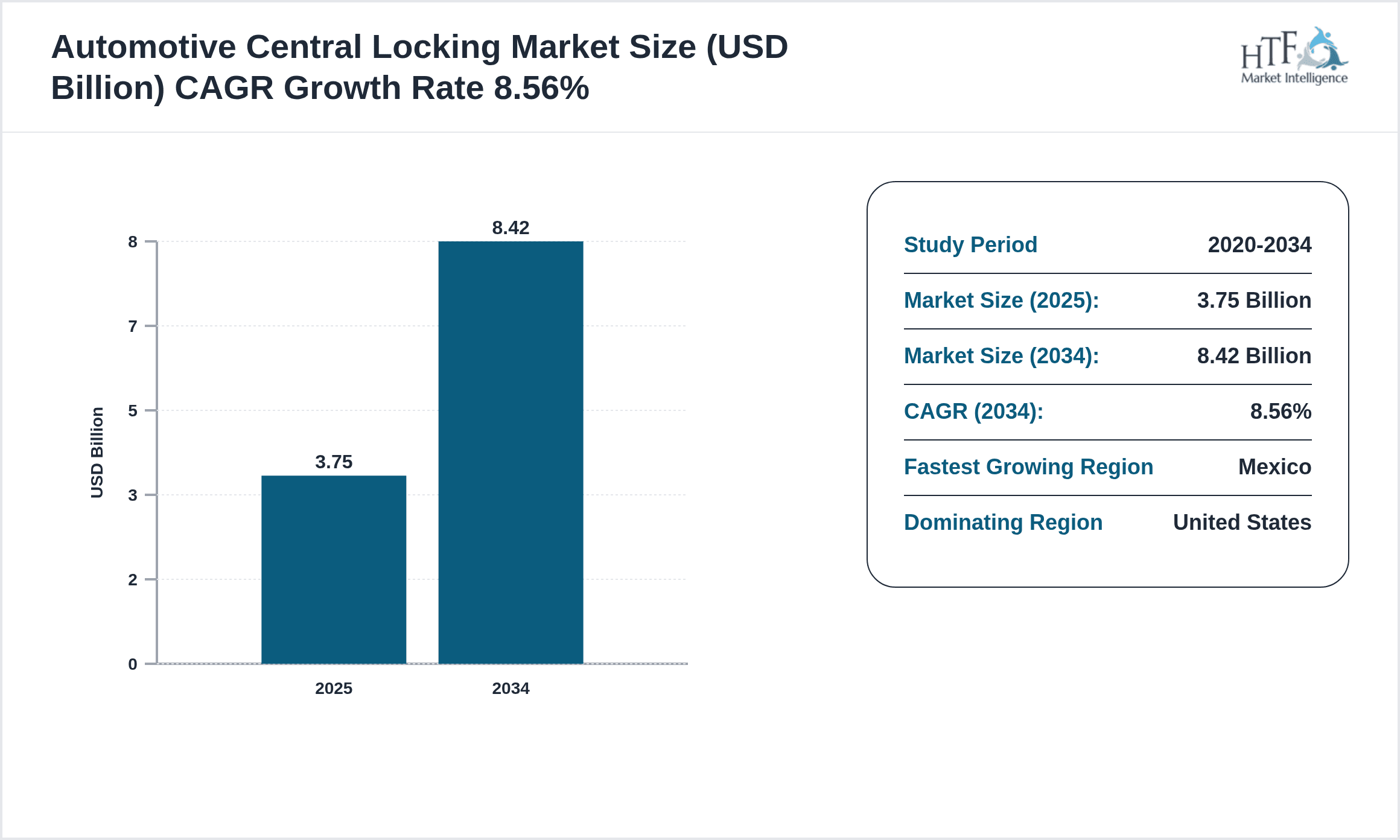

- •Key highlights of the North America Automotive Central Locking market include a base market size of USD 3.75 Billion in 2024, projected to reach USD 8.42 Billion by 2034, representing a robust CAGR of 8.56%. The remote keyless systems segment dominates due to its widespread adoption in passenger vehicles, while smart locking systems exhibit the fastest growth driven by advancements in vehicle connectivity and security. The passenger cars application segment accounts for the largest market share, with increasing penetration in commercial and electric vehicles contributing to rapid growth. The United States remains the dominating country in market revenue, whereas Mexico is recognized as the fastest-growing market, fueled by expanding automotive manufacturing and rising vehicle sales. The market is also shaped by evolving consumer preferences, stricter safety standards, and ongoing innovations in locking technologies.

- •The value proposition of the Automotive Central Locking market lies in its contribution to vehicle security enhancement, user convenience, and integration with smart vehicle ecosystems. Automotive manufacturers and aftermarket suppliers leverage these technologies to differentiate products, comply with safety regulations, and satisfy consumer expectations. The market's strategic importance extends to insurers, law enforcement, and technology developers seeking to mitigate theft risks and improve vehicle control. Investment in R&D is fostering innovations in biometric authentication, wireless control, and integration with vehicle telematics, creating new opportunities for competitive advantage. Overall, the market plays a pivotal role in advancing automotive safety, driving product innovation, and shaping the future of connected vehicle systems in North America.

Competitive Landscape

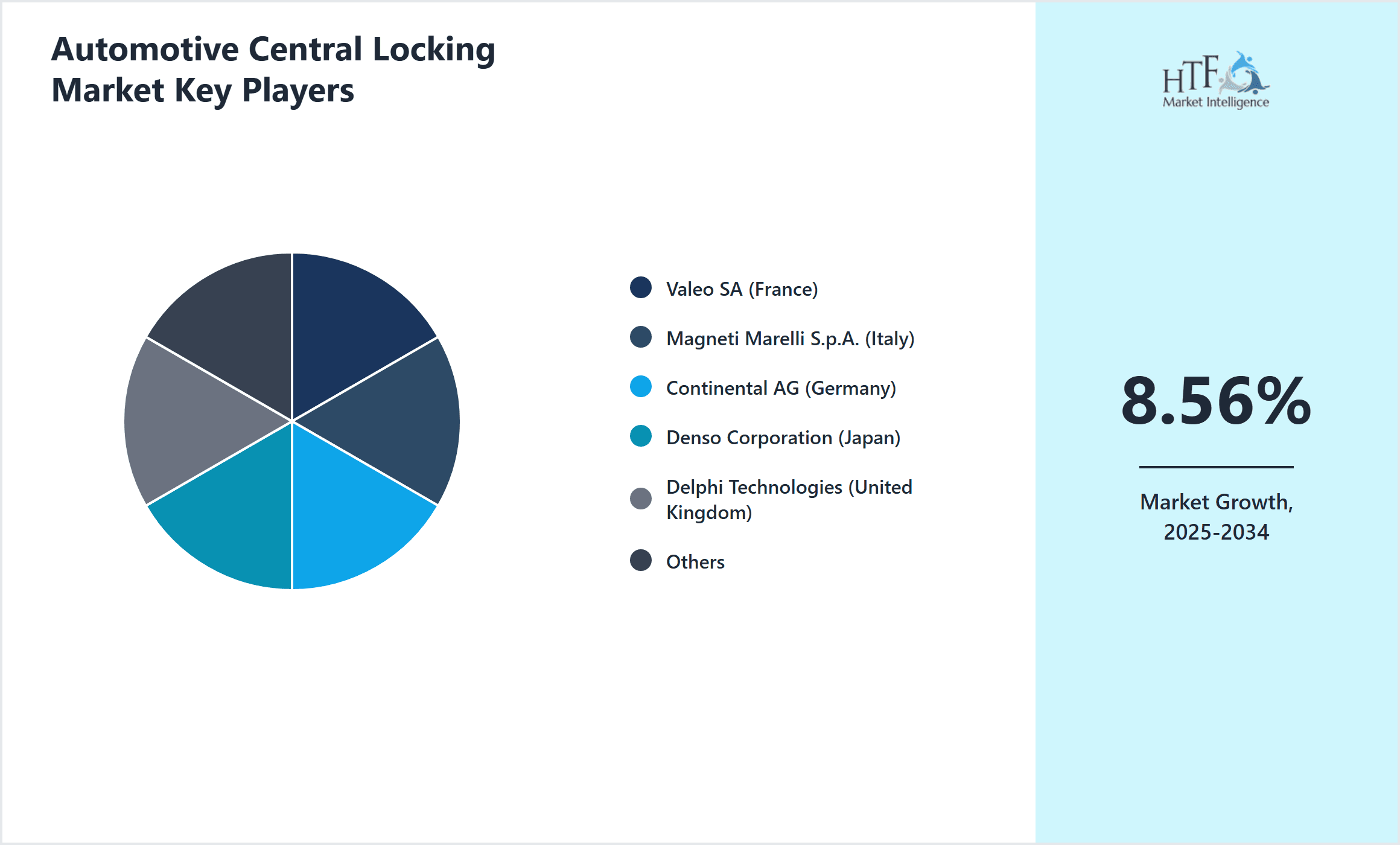

The North America Automotive Central Locking market is characterized by intense competition among global automotive component manufacturers, technology innovators, and aftermarket suppliers. Market players compete through continuous innovation in locking technologies, including wireless keyless entry, smart locks with biometric features, and integration with vehicle security systems. Strategic partnerships with OEMs and tier-1 suppliers are critical for securing contracts and expanding market presence. Companies focus on enhancing product reliability, reducing costs, and complying with evolving regulatory standards. Competition also revolves around intellectual property portfolios, with firms investing heavily in R&D to develop proprietary technologies that offer enhanced security and convenience. Additionally, pricing strategies and broad distribution networks influence market positioning. Regional competition sees established players dominating in the United States, while emerging manufacturers in Mexico and Canada leverage cost advantages and local partnerships. Overall, the competitive landscape is dynamic, marked by technological advancements, consolidation efforts, and a focus on meeting rising consumer and regulatory demands.

Leading Companies in Automotive Central Locking Market

- •Valeo SA (France)

- •Magneti Marelli S.p.A. (Italy)

- •Continental AG (Germany)

- •Denso Corporation (Japan)

- •Delphi Technologies (United Kingdom)

- •Huf Hülsbeck & Fürst GmbH & Co. KG (Germany)

- •Minda Corporation Limited (India)

- •Mitsuba Corporation (Japan)

- •Nippon Seiki Co., Ltd. (Japan)

- •Johnson Controls International plc (Ireland)

- •Autoliv Inc. (Sweden)

- •Stanley Electric Co., Ltd. (Japan)

- •Sumitomo Electric Industries, Ltd. (Japan)

- •Aisin Seiki Co., Ltd. (Japan)

- •Gentex Corporation (United States)

- •Omron Corporation (Japan)

- •Laird PLC (United Kingdom)

- •Murata Manufacturing Co., Ltd. (Japan)

- •Alps Alpine Co., Ltd. (Japan)

- •Magneti Marelli S.p.A. (Italy)

- •Aptiv PLC (Ireland)

- •ZF Friedrichshafen AG (Germany)

- •Robert Bosch GmbH (Germany)

- •Lear Corporation (United States)

- •Faurecia S.A. (France)

Market Breakdown

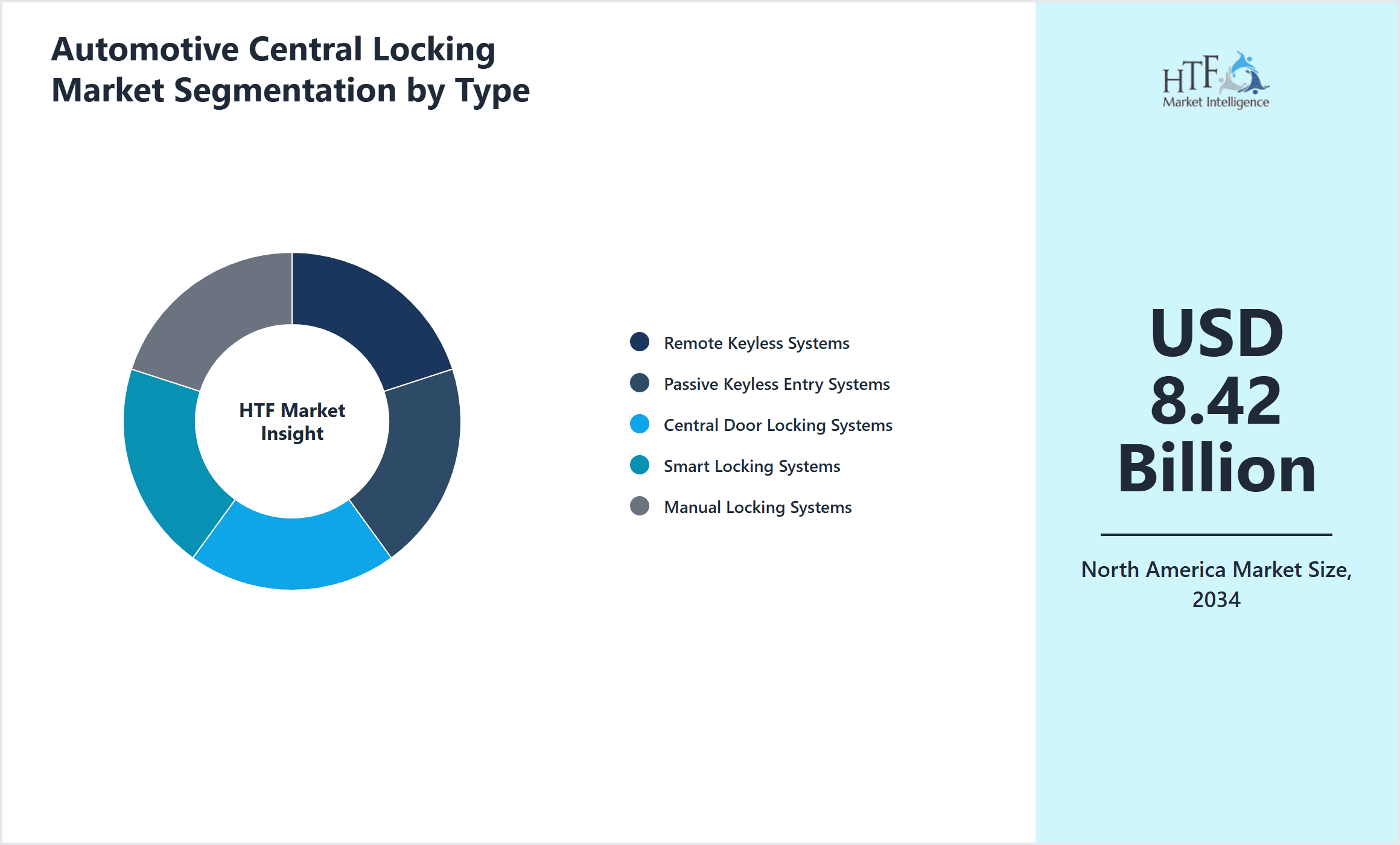

- •By Type

- ◦Remote Keyless Systems

- ◦Passive Keyless Entry Systems

- ◦Central Door Locking Systems

- ◦Smart Locking Systems

- ◦Manual Locking Systems

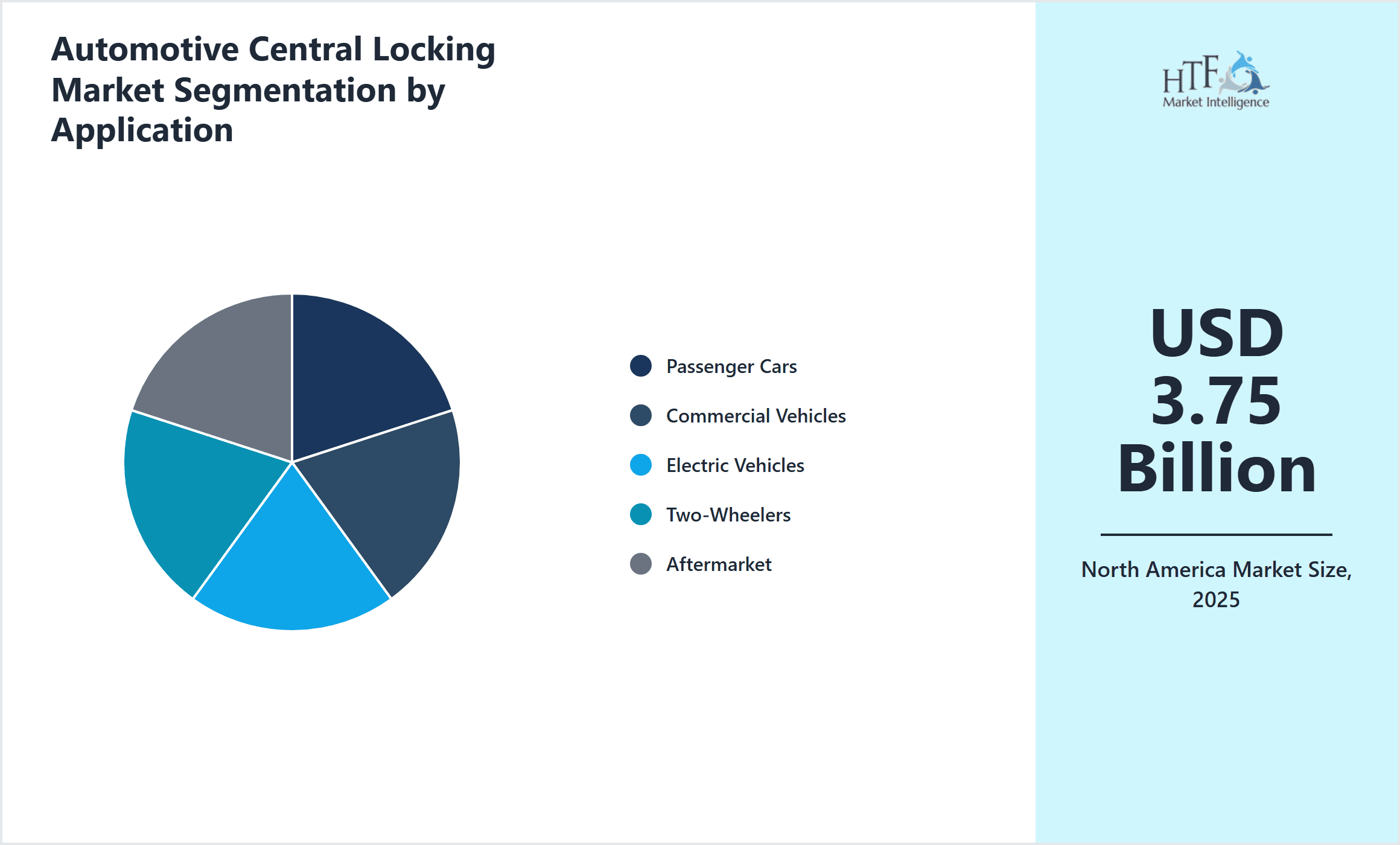

- •By Application

- ◦Passenger Cars

- ◦Commercial Vehicles

- ◦Electric Vehicles

- ◦Two-Wheelers

- ◦Aftermarket

- •By End-Use Industry

- ◦Automotive OEMs

- ◦Aftermarket Suppliers

- ◦Fleet Operators

- ◦Vehicle Rental Services

- •By Distribution Channel

- ◦Original Equipment Manufacturer (OEM)

- ◦Aftermarket Retail

- ◦Online Sales

Growth Dynamics

The North America Automotive Central Locking market growth is primarily driven by increasing consumer demand for convenience and advanced vehicle security amid rising vehicle theft rates. The proliferation of electric vehicles and connected cars has intensified the need for sophisticated locking solutions integrated with smart vehicle systems. Moreover, stringent government regulations mandating enhanced vehicle security features bolster market expansion. Automotive OEMs are investing in keyless and biometric locking technologies to meet evolving safety standards and consumer expectations. Additionally, the growth of the aftermarket segment, fueled by vehicle aging and replacement needs, contributes to sustained demand. Technological innovations such as smartphone-controlled locks and integration with vehicle telematics systems further enhance user experience, driving adoption across passenger and commercial vehicle segments. Expansion of automotive production in Mexico and adoption of advanced security systems in Canada also support regional market growth.

Market Trends

Emerging trends in the North America Automotive Central Locking market include the rapid adoption of smart locking systems featuring biometric authentication, smartphone integration, and wireless connectivity. Manufacturers are increasingly incorporating IoT-enabled locks that offer remote access control and real-time monitoring, enhancing vehicle security and user convenience. The shift toward electric and autonomous vehicles is accelerating the integration of advanced central locking technologies with vehicle electronic architectures. Additionally, aftermarket players are leveraging e-commerce platforms for wider product distribution, tapping into consumer preference for easy access to replacement and upgrade solutions. Another notable trend is the growing collaboration between automotive suppliers and technology firms to co-develop innovative locking mechanisms that support connected car ecosystems. Environmental sustainability considerations are also influencing the design of locking components, with a focus on lightweight, durable materials that reduce vehicle weight and improve fuel efficiency.

Market Opportunities

Significant opportunities exist in the North America Automotive Central Locking market driven by the expanding electric vehicle segment, which demands highly sophisticated locking systems integrated with smart vehicle networks. The increasing consumer acceptance of keyless and biometric entry technologies provides avenues for product innovation and premium offerings. Growth in vehicle fleet services and car-sharing platforms creates additional demand for advanced locking solutions with remote management capabilities. Moreover, the rising penetration of connected and autonomous vehicles opens prospects for integrating central locking with broader vehicle security and telematics systems. The aftermarket segment offers substantial potential as aging vehicle fleets require replacement and upgrade of locking components. Geographic expansion into emerging automotive hubs in Mexico and enhanced distribution through digital channels further bolster market potential. Strategic partnerships with technology companies and OEMs will be critical to capitalize on these opportunities and accelerate product adoption.

Market Challenges

The North America Automotive Central Locking market faces challenges such as high development and production costs associated with advanced smart locking technologies, which can limit adoption among cost-sensitive vehicle segments. Integration complexity with diverse vehicle electronic architectures creates technical hurdles for manufacturers and suppliers. Cybersecurity risks pertaining to wireless and keyless locking systems pose concerns about potential hacking and unauthorized access, necessitating rigorous security measures and compliance with evolving regulations. Additionally, the aftermarket segment is fragmented, with intense price competition and counterfeit products impacting profitability. Regulatory compliance across multiple jurisdictions in North America adds complexity to market entry and product certification. Supply chain disruptions and raw material price volatility further affect manufacturing costs and delivery timelines. These challenges require continuous innovation, robust quality assurance, and strategic collaborations to maintain competitiveness and market growth.

Regulatory Framework

Between 2019 and 2024, North America has seen the implementation of stringent automotive safety and anti-theft regulations that directly impact the Automotive Central Locking market. The U.S. National Highway Traffic Safety Administration (NHTSA) has updated standards mandating enhanced vehicle security features, including requirements for electronic immobilizers and standardized keyless entry systems. Canada has aligned its automotive safety regulations with these standards, emphasizing anti-theft technologies in passenger and commercial vehicles. Mexico, as part of trade agreements like USMCA, has adopted harmonized vehicle security regulations promoting the adoption of advanced central locking systems. These regulations impose compliance requirements on manufacturers and suppliers, influencing product development cycles, certification processes, and market entry strategies. Moreover, privacy and cybersecurity regulations are increasingly relevant due to the connectivity of modern locking systems, requiring adherence to data protection and security protocols. Government incentives for electric vehicles further encourage integration of smart locking technologies compatible with EV architectures.

Market Intelligence

- •15th February 2024, Valeo SA announced the launch of an advanced smart locking system featuring biometric fingerprint sensors and smartphone integration aimed at enhancing vehicle security and convenience in North America. The product leverages IoT connectivity to allow remote access control and real-time monitoring, targeting premium passenger cars and electric vehicles. This innovation aligns with growing consumer demand for keyless, secure vehicle entry solutions and supports OEMs' efforts to comply with stringent safety regulations while providing a differentiated user experience. Valeo’s strategic focus on integrating their locking systems with vehicle telematics platforms positions them as a technological leader in this segment.

- •10th August 2023, Gentex Corporation introduced a next-generation remote keyless entry system that incorporates AI-based anomaly detection to prevent unauthorized access attempts. Designed for commercial and passenger vehicles, the system provides enhanced security features including encrypted communication protocols and integration with vehicle alarm systems. This launch reflects growing market emphasis on cybersecurity and vehicle safety, particularly in the North American market where theft prevention and regulatory compliance are critical. Gentex’s product is expected to drive adoption among OEMs seeking to upgrade vehicle security offerings.

- •Market Intelligence: Recent developments and industry insights are being monitored. For latest updates, consult official company announcements and industry publications.

- •Market Intelligence: Recent developments and industry insights are being monitored. For latest updates, consult official company announcements and industry publications.

Regional Outlook

The United States currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Mexico is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- United States

- Canada

- Mexico

| Feature | Details |

|---|---|

| Base Year Market Size | USD 3.75 Billion |

| Forecast Year Market Size | USD 8.42 Billion |

| CAGR | 8.56% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 8.24% |

| Scope of Report | Market is segmented by Type (Remote Keyless Systems, Passive Keyless Entry Systems, Central Door Locking Systems, Smart Locking Systems, Manual Locking Systems), Application (Passenger Cars, Commercial Vehicles, Electric Vehicles, Two-Wheelers, Aftermarket), End-Use Industry (Automotive OEMs, Aftermarket Suppliers, Fleet Operators, Vehicle Rental Services), Distribution Channel (Original Equipment Manufacturer (OEM), Aftermarket Retail, Online Sales) |

| Regions Covered | United States, Canada, Mexico |

| Key Companies | Valeo SA (France), Magneti Marelli S.p.A. (Italy), Continental AG (Germany), Denso Corporation (Japan), Delphi Technologies (United Kingdom), Huf Hülsbeck & Fürst GmbH & Co. KG (Germany), Minda Corporation Limited (India), Mitsuba Corporation (Japan), Nippon Seiki Co., Ltd. (Japan), Johnson Controls International plc (Ireland), Autoliv Inc. (Sweden), Stanley Electric Co., Ltd. (Japan), Sumitomo Electric Industries, Ltd. (Japan), Aisin Seiki Co., Ltd. (Japan), Gentex Corporation (United States), Omron Corporation (Japan), Laird PLC (United Kingdom), Murata Manufacturing Co., Ltd. (Japan), Alps Alpine Co., Ltd. (Japan), Magneti Marelli S.p.A. (Italy), Aptiv PLC (Ireland), ZF Friedrichshafen AG (Germany), Robert Bosch GmbH (Germany), Lear Corporation (United States), Faurecia S.A. (France) |

North America Automotive Central Locking Market Size, Growth & Revenue 2024-2034 - Table of Contents

Multidisciplinary researcher with 10+ years of experience uncovering insights across diverse domains focused on uncovering insights that drive informed decisions.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.