Asia-Pacific Canned and Chilled Soup Market - Outlook 2025-2034

Asia-Pacific Canned and Chilled Soup Market is segmented by Product Type (Canned Soup, Chilled Soup, Ready-to-Eat Soup, Frozen Soup, Concentrated Soup), Application (Retail, Foodservice, Online Sales, Institutional Catering, Convenience Stores), End-Use Industry (Household Consumption, Hospitality, Healthcare, Educational Institutions), Distribution Channel (Supermarkets/Hypermarkets, Specialty Stores, E-commerce Platforms), and Geography (Japan, China, Southeast Asia, India, Australia, South Korea, Others)

Pricing

Report Overview

Executive Summary

- •The Asia-Pacific canned and chilled soup market represents a dynamic segment within the broader convenience food industry, focused on providing consumers with ready-to-eat, nutrition-rich soup products preserved primarily through canning and chilling methods. This market covers a variety of product types including canned, chilled, ready-to-eat, frozen, and concentrated soups, each tailored to meet diverse consumer taste profiles and lifestyle demands across key applications such as retail outlets, foodservice operations, online platforms, institutional catering, and convenience stores. The market's scope encompasses multiple countries including China, India, Japan, South Korea, Australia, and Southeast Asia, reflecting significant cultural diversity and consumption patterns. Rising urbanization, increasing disposable incomes, and a growing trend towards healthy and convenient food options are significant drivers shaping the market landscape. Innovations in packaging technology and cold chain logistics enhance product freshness and shelf-life, further boosting market penetration. The industry also benefits from expanding distribution networks and rising awareness of nutritional benefits, positioning it as a high-growth sector within the Asia-Pacific food market.

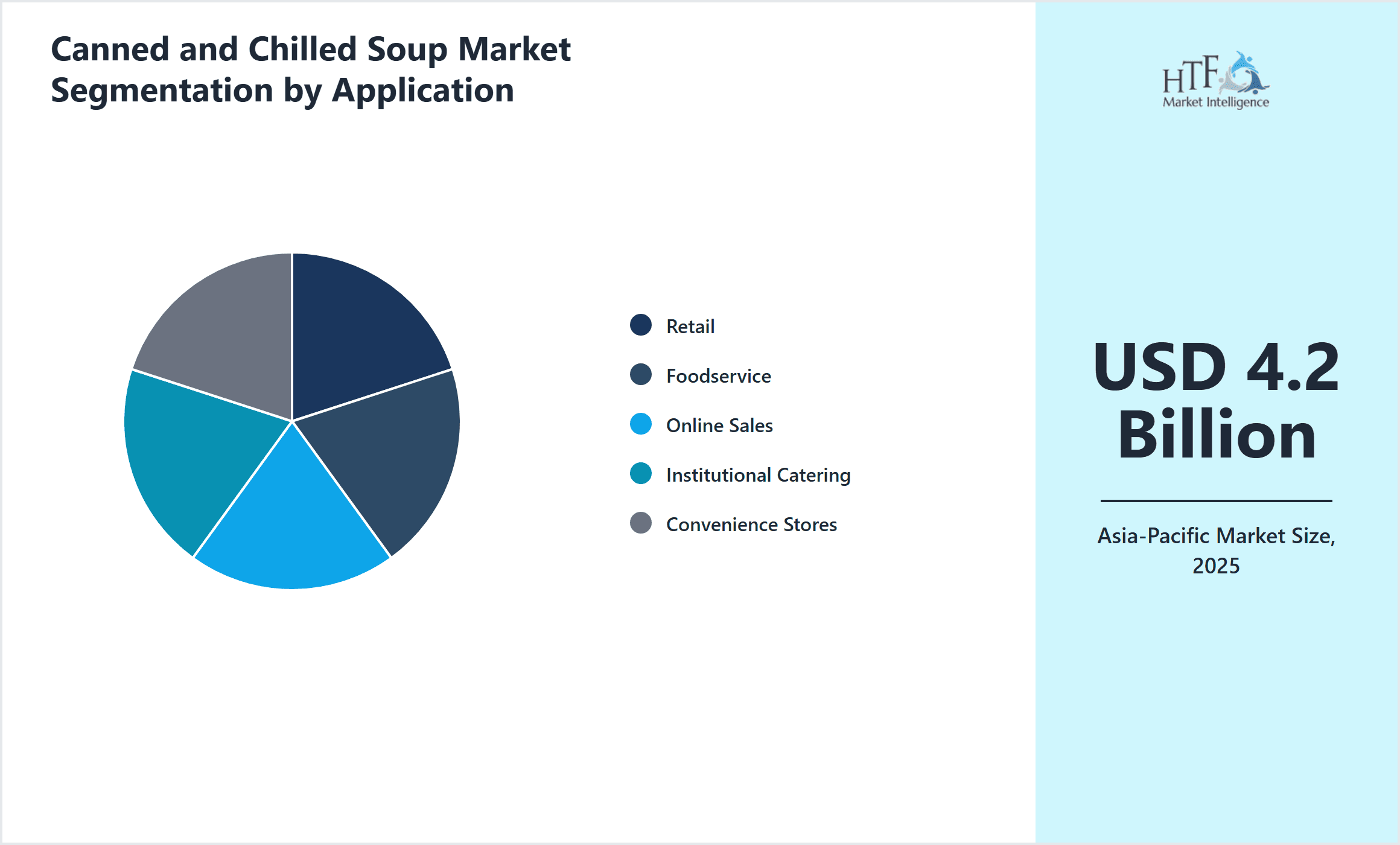

- •Key market highlights include a base market size of USD 4.2 Billion in 2025, projected to reach USD 8.75 Billion by 2034, reflecting a robust CAGR of 8.3%. The canned soup segment currently dominates product types, but chilled soup is emerging rapidly due to consumer preferences for fresh, preservative-free options. Retail remains the leading application channel, supported by increasing supermarket penetration and online grocery sales. China holds the dominant regional market share, driven by its large population and evolving consumer lifestyles, while India is identified as the fastest-growing country owing to rising urbanization and westernization of food habits. The market is characterized by intense competition, innovation in product formulations, and strategic expansions by key players.

- •The value proposition of the Asia-Pacific canned and chilled soup market lies in delivering convenient, nutritious, and diverse meal solutions aligned with modern consumer demands. The sector is strategically important to food manufacturers, retailers, and distributors seeking growth in emerging markets with increasing health consciousness and busy lifestyles. It also offers opportunities for innovation in packaging, flavor development, and distribution models. Stakeholders benefit from rising demand for ready-to-eat foods that balance taste, health, and convenience, supported by regulatory frameworks that ensure food safety and quality. Consequently, the market is poised for sustained expansion driven by evolving consumer behavior and technological progress.

Competitive Landscape

The Asia-Pacific canned and chilled soup market is highly competitive, featuring a mix of multinational corporations and regional players vying for market share through innovation, branding, and distribution excellence. Market leaders focus on product differentiation by introducing new flavors, healthier ingredient profiles, and convenient packaging solutions such as easy-open cans and eco-friendly materials. Companies invest heavily in research and development to incorporate natural ingredients, reduce sodium content, and meet clean-label demands, thereby appealing to health-conscious consumers. Strategic partnerships and expansions into emerging markets are common tactics to enhance regional presence. Pricing strategies vary, with premium segments offering gourmet and organic soups, while value segments compete on affordability and accessibility. The rivalry also extends to distribution channels, with players strengthening their online and offline retail footprints to capture diverse customer segments. Technology adoption in manufacturing and cold chain logistics further intensifies competition, enabling faster product launches and improved freshness. Barriers to entry include stringent food safety regulations and high capital requirements, which favor established brands but also encourage innovation-driven startups. The market is expected to evolve with increased consolidation, strategic alliances, and focus on sustainable growth practices.

Prominent Players in Canned and Chilled Soup Market

- •Campbell Soup Company (United States)

- •Nestlé S.A. (Switzerland)

- •Unilever PLC (United Kingdom/Netherlands)

- •Kraft Heinz Company (United States)

- •Ajinomoto Co., Inc. (Japan)

- •Heinz India Pvt. Ltd. (India)

- •Hain Celestial Group, Inc. (United States)

- •Kerry Group plc (Ireland)

- •Campbell Soup Asia (Singapore)

- •CJ CheilJedang Corporation (South Korea)

- •McCormick & Company, Inc. (United States)

- •ConAgra Brands, Inc. (United States)

- •Nissin Foods Holdings Co., Ltd. (Japan)

- •Lotte Foods Co., Ltd. (South Korea)

- •Yum China Holdings, Inc. (China)

- •Hengstenberg GmbH & Co. KG (Germany)

- •Menora Foods Co., Ltd. (Thailand)

- •Sapporo Holdings Limited (Japan)

- •GreenMax (China)

- •Sunshine Foods (Australia)

- •Otsuka Foods Co., Ltd. (Japan)

- •Vitasoy International Holdings Ltd. (Hong Kong)

- •Fonterra Co-operative Group Limited (New Zealand)

- •AFC Foods Pvt. Ltd. (India)

- •Prima Taste Singapore Pte Ltd (Singapore)

Market Breakdown

- •By Product Type

- ◦Canned Soup

- ◦Chilled Soup

- ◦Ready-to-Eat Soup

- ◦Frozen Soup

- ◦Concentrated Soup

- •By Application

- ◦Retail

- ◦Foodservice

- ◦Online Sales

- ◦Institutional Catering

- ◦Convenience Stores

- •By End-Use Industry

- ◦Household Consumption

- ◦Hospitality

- ◦Healthcare

- ◦Educational Institutions

- •By Distribution Channel

- ◦Supermarkets/Hypermarkets

- ◦Specialty Stores

- ◦E-commerce Platforms

Growth Dynamics

- •Rapid urbanization and increasing urban workforce in countries like China and India are driving demand for convenient meal solutions such as canned and chilled soups, as busy lifestyles limit time for traditional cooking.

- •Rising health consciousness among consumers in Asia-Pacific encourages the consumption of soups fortified with natural ingredients and low sodium content, prompting manufacturers to innovate healthier product variants.

- •Expansion of modern retail chains and growth of e-commerce platforms in the region enhance product availability and accessibility, making canned and chilled soups more convenient for a wider consumer base.

- •Advancements in packaging technologies such as vacuum sealing and aseptic processing improve product shelf life and quality, supporting market growth by enabling wider distribution.

- •Increasing penetration of Western dietary habits and exposure to global cuisines in the Asia-Pacific region stimulates demand for diverse and premium soup flavors, expanding market scope.

Market Trends

- •There is a growing trend towards clean-label soups with organic and non-GMO certifications, driven by consumers’ desire for transparency and natural ingredients in the Asia-Pacific market.

- •Plant-based and vegan soups are gaining popularity as part of the sustainability movement and increasing vegetarian populations in countries like India and Australia.

- •Integration of technology in supply chains, such as blockchain for traceability, enhances consumer trust and meets regulatory demands for food safety in the region.

- •Collaborations between local soup manufacturers and international food brands are increasing, allowing cross-border flavor innovation and expanded distribution channels.

- •The rise of online grocery shopping accelerated by the COVID-19 pandemic continues to influence purchasing habits, with canned and chilled soups becoming key convenience items in e-commerce sales.

Market Opportunities

- •Emerging markets within Southeast Asia and India present significant growth opportunities due to expanding middle-class populations and rising disposable incomes demanding convenient food options.

- •Innovation in functional soups enriched with vitamins, minerals, and probiotics targets health-conscious consumers, creating new product segments and boosting market expansion.

- •Development of sustainable packaging solutions offers manufacturers the chance to differentiate products and appeal to environmentally aware consumers in the Asia-Pacific region.

- •Increasing partnerships between foodservice operators and soup producers can drive bulk purchases and institutional adoption, broadening market reach beyond retail channels.

- •Digital marketing and direct-to-consumer sales channels provide opportunities for startups and smaller players to build brand awareness and establish niche market positions.

Market Challenges

- •High competition from local and international brands pressures pricing and profit margins, making it challenging for new entrants to establish themselves in the Asia-Pacific market.

- •Stringent food safety regulations and compliance requirements across multiple countries add complexity and cost to product development and market entry.

- •Consumer skepticism about preservatives and additives in canned products can limit market acceptance, requiring manufacturers to balance shelf life with natural ingredient claims.

- •Logistical challenges in cold chain management impact the distribution of chilled soups, especially in less developed regions with inadequate infrastructure.

- •Fluctuations in raw material prices, particularly vegetables and meats, can increase production costs and affect pricing strategies.

Regulatory Framework

- •Between 2020 and 2025, Asia-Pacific countries have implemented stricter food safety regulations focusing on hygiene standards, labeling accuracy, and traceability to enhance consumer protection.

- •Mandatory nutrition labeling and allergen disclosures are now enforced in key markets such as China and India, compelling manufacturers to provide transparent ingredient and nutritional information.

- •Environmental regulations promoting sustainable packaging have gained momentum, with governments incentivizing biodegradable materials and restricting single-use plastics in countries like Japan and Australia.

- •Import-export policies have been streamlined in trade blocs like ASEAN to facilitate smoother cross-border distribution of canned and chilled soup products.

- •Government initiatives supporting local food startups and innovation hubs provide regulatory support and funding opportunities, fostering competitive product development in the region.

Market Intelligence

- •15th January 2025, Campbell Soup Company expanded its Asia-Pacific footprint by launching a new line of organic chilled soups in China and India, targeting health-conscious millennials seeking convenient meal options. The product range includes vegetable and legume-based soups free from artificial preservatives and additives, leveraging eco-friendly packaging to attract environmentally aware consumers. This strategic move aims to capture growing demand in urban centers and reinforce Campbell’s position as a market innovator. Source: Official company press release

- •7th March 2025, Nestlé S.A. introduced a premium canned soup brand in Southeast Asia featuring locally inspired flavors such as Tom Yum and Miso Soup. This launch integrates traditional culinary heritage with modern nutritional standards, appealing to both young adults and older consumers. Nestlé invested in cold chain infrastructure improvements to ensure product freshness and expanded its e-commerce presence to accelerate market penetration. This initiative underscores Nestlé’s commitment to regional customization and innovation in the Asia-Pacific market. Source: Industry publication

- •20th June 2025, Unilever PLC announced a strategic partnership with regional food retailers across India and Australia to enhance distribution of its chilled soup products. The collaboration focuses on joint marketing campaigns and supply chain optimization to increase availability in tier 2 and tier 3 cities. This approach aims to boost sales volumes and improve brand visibility in rapidly urbanizing areas. Unilever’s strategy also incorporates feedback mechanisms to tailor products to local taste preferences, supporting sustainable growth. Source: Company website

- •12th September 2025, Ajinomoto Co., Inc. completed the acquisition of a regional chilled soup manufacturer in South Korea, broadening its product portfolio and leveraging local expertise to accelerate innovation. The acquisition enhances Ajinomoto’s capacity to develop functional soups enriched with probiotics and vitamins, aligning with growing consumer health trends. This move is expected to consolidate market share and improve competitive positioning within the Asia-Pacific canned and chilled soup segment. Source: Official press announcement

Regional Outlook

The China currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, India is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- Japan

- China

- Southeast Asia

- India

- Australia

- South Korea

- Others

| Feature | Details |

|---|---|

| Base Year Market Size | USD 4.2 Billion |

| Forecast Year Market Size | USD 8.75 Billion |

| CAGR | 8.3% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 8% |

| Scope of Report | Market is segmented by Product Type (Canned Soup, Chilled Soup, Ready-to-Eat Soup, Frozen Soup, Concentrated Soup), Application (Retail, Foodservice, Online Sales, Institutional Catering, Convenience Stores), End-Use Industry (Household Consumption, Hospitality, Healthcare, Educational Institutions), Distribution Channel (Supermarkets/Hypermarkets, Specialty Stores, E-commerce Platforms) |

| Regions Covered | Japan, China, Southeast Asia, India, Australia, South Korea, Others |

| Key Companies | Campbell Soup Company (United States), Nestlé S.A. (Switzerland), Unilever PLC (United Kingdom/Netherlands), Kraft Heinz Company (United States), Ajinomoto Co., Inc. (Japan), Heinz India Pvt. Ltd. (India), Hain Celestial Group, Inc. (United States), Kerry Group plc (Ireland), Campbell Soup Asia (Singapore), CJ CheilJedang Corporation (South Korea), McCormick & Company, Inc. (United States), ConAgra Brands, Inc. (United States), Nissin Foods Holdings Co., Ltd. (Japan), Lotte Foods Co., Ltd. (South Korea), Yum China Holdings, Inc. (China), Hengstenberg GmbH & Co. KG (Germany), Menora Foods Co., Ltd. (Thailand), Sapporo Holdings Limited (Japan), GreenMax (China), Sunshine Foods (Australia), Otsuka Foods Co., Ltd. (Japan), Vitasoy International Holdings Ltd. (Hong Kong), Fonterra Co-operative Group Limited (New Zealand), AFC Foods Pvt. Ltd. (India), Prima Taste Singapore Pte Ltd (Singapore) |

Asia-Pacific Canned and Chilled Soup Market - Outlook 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.