Global Gas Detection Equipment Market Size, Growth & Revenue 2024-2034

Global Gas Detection Equipment Market is segmented by Type (Fixed Gas Detectors, Portable Gas Detectors, Wireless Gas Detectors, Photoionization Detectors, Flame Detectors), Application (Industrial Safety, Environmental Monitoring, Oil & Gas, Chemical Processing, Mining), End-Use Industry (Oil & Gas, Chemical Manufacturing, Mining & Metals, Construction & Infrastructure), Distribution Channel (Direct Sales, Distributors, Online Retail), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global gas detection equipment market is a vital segment within industrial safety and environmental monitoring sectors, tasked with identifying gas leaks and hazardous atmospheres to prevent accidents and ensure compliance with safety standards. This market covers a broad product portfolio including fixed, portable, wireless, photoionization, and flame detectors, utilized across diverse applications such as oil & gas exploration, chemical processing plants, mining operations, and environmental surveillance. The equipment integrates advanced sensor technologies to detect toxic, combustible, and oxygen-deficient gases, facilitating real-time alerts and automated responses critical to safeguarding human life and infrastructure. Increasing industrial activities, rapid urbanization, and growing regulatory mandates worldwide have expanded the market scope and complexity. The rising adoption of wireless and IoT-enabled solutions is transforming traditional gas detection methods, enabling remote monitoring and data analytics. Market participants are focusing on innovation, strategic partnerships, and geographic expansion to capitalize on emerging opportunities and address evolving safety challenges globally.

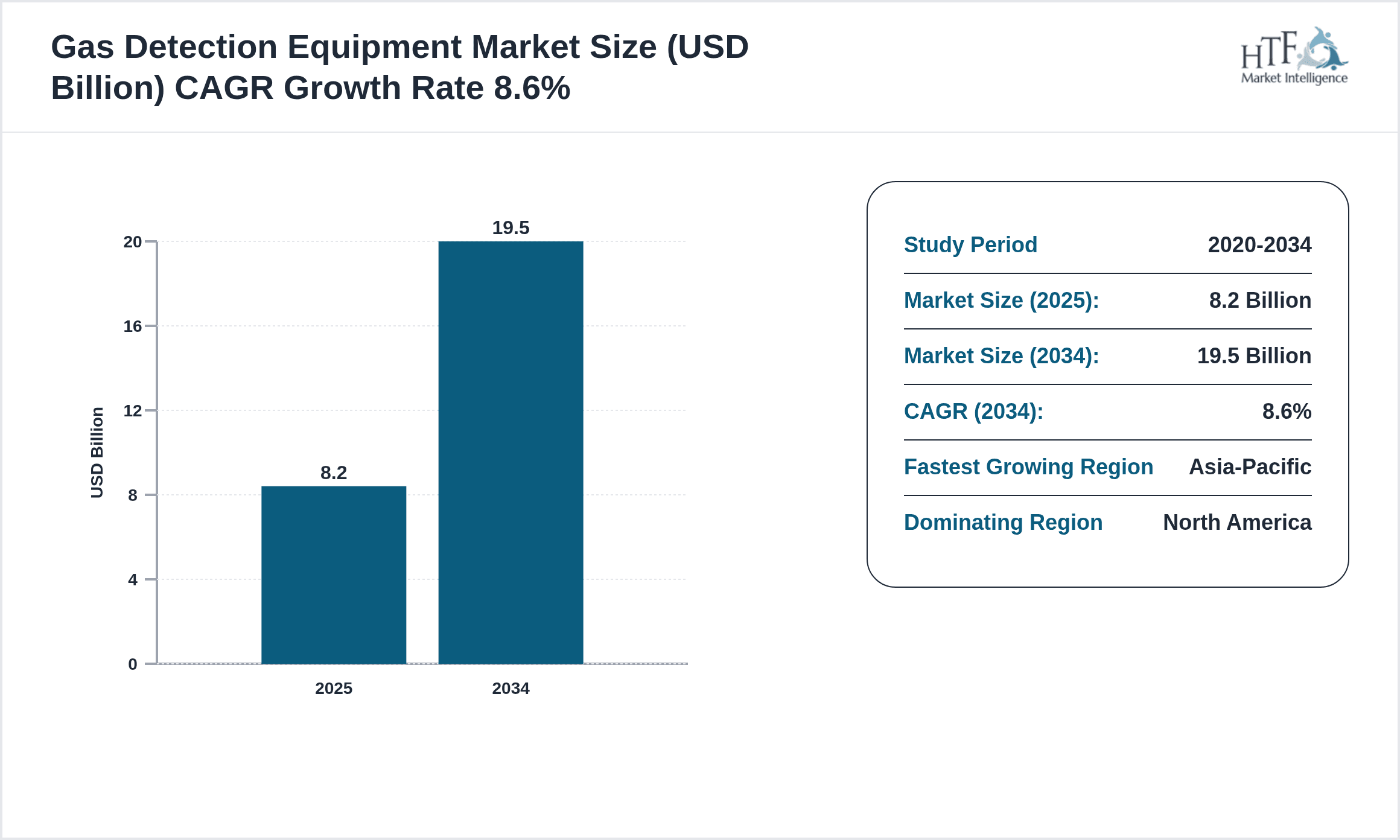

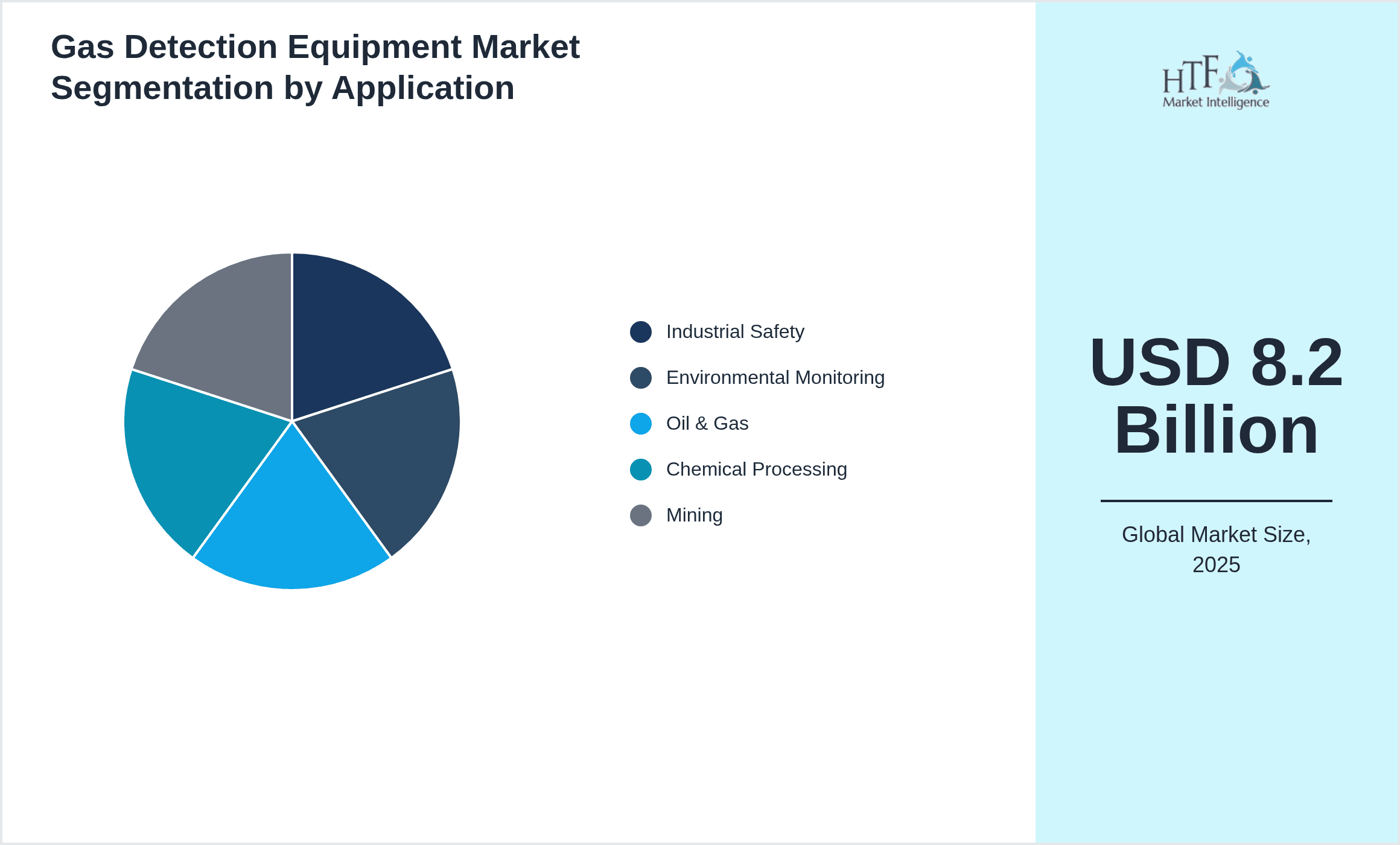

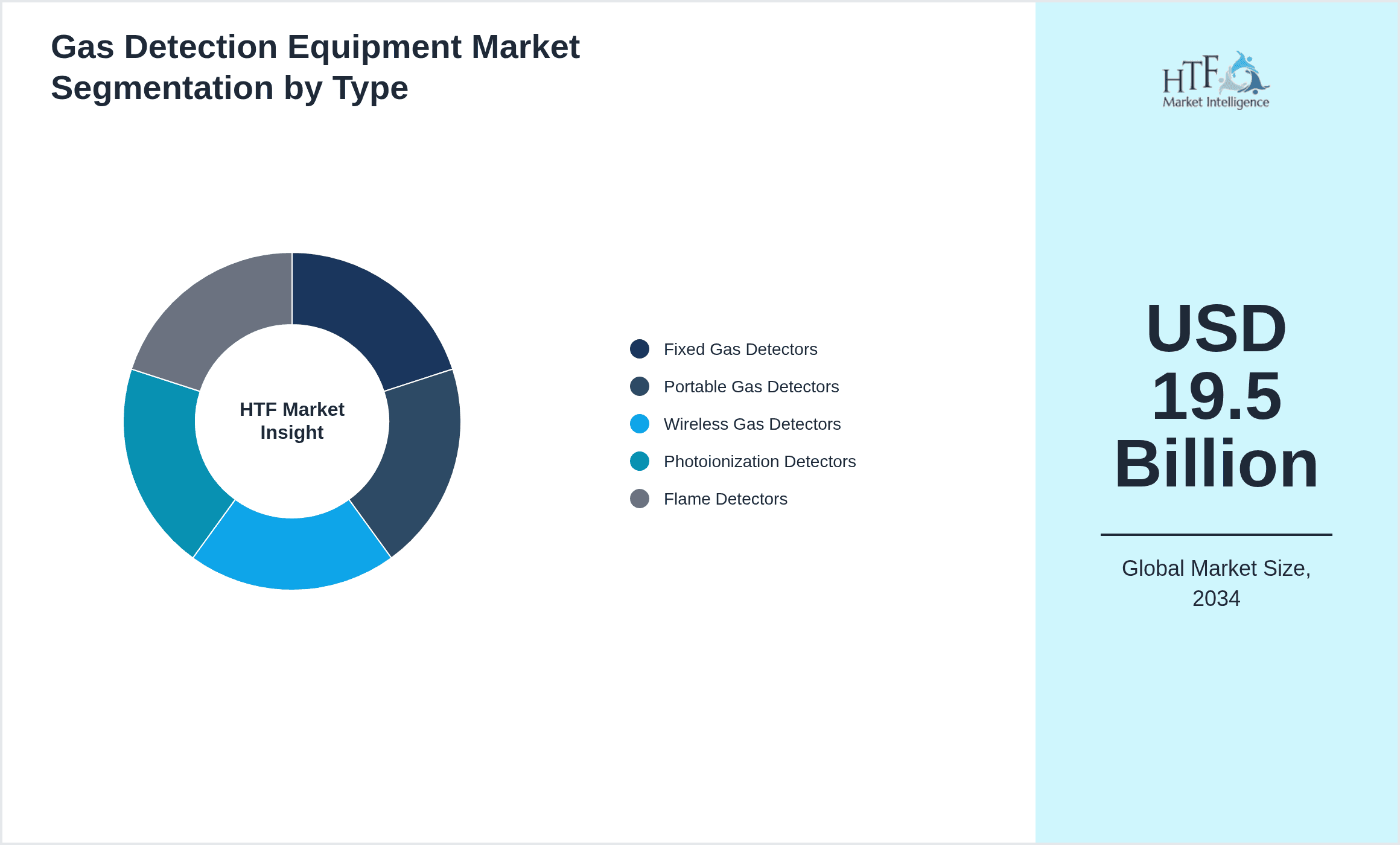

- •Key market highlights include a 2024 base valuation of USD 8.2 Billion, with projections reaching USD 19.5 Billion by 2034, reflecting a compound annual growth rate (CAGR) of 8.6%. North America currently dominates the market due to stringent safety regulations and advanced industrial infrastructure, while Asia-Pacific is the fastest-growing region driven by industrialization and infrastructure development. Fixed gas detectors hold the largest market share due to their extensive use in permanent installations, whereas wireless gas detectors are the fastest-growing product segment due to flexibility and integration with smart systems. Industrial safety remains the leading application, closely followed by environmental monitoring, underscoring the market’s dual focus on operational safety and ecological compliance.

- •The global gas detection equipment market offers significant value propositions including enhanced worker safety, reduced accident risks, regulatory compliance facilitation, and operational efficiency improvements across industries. Strategic importance is underscored by the critical role these devices play in preventing catastrophic events like explosions and toxic exposures, thereby protecting human health and assets. For stakeholders, the market represents opportunities for technological advancements, portfolio diversification, and entry into emerging economies with increasing industrial activities. Continuous innovation in sensor accuracy, connectivity, and data analytics capabilities positions the market as a key enabler of smart industrial safety ecosystems worldwide.

Competitive Landscape

The competitive landscape of the global gas detection equipment market is characterized by intense rivalry among multinational corporations and regional players focusing on technological innovation, strategic partnerships, and geographic expansion to consolidate market share. Leading companies emphasize research and development to enhance sensor accuracy, integrate wireless communication, and develop IoT-enabled platforms, thereby differentiating their offerings. Market participants adopt diverse strategies including mergers and acquisitions to acquire complementary technologies, expand product portfolios, and enter new markets. Pricing strategies vary across regions reflecting differing regulatory frameworks and customer purchasing power, while distribution channels are optimized for global reach and rapid service support. The competition also involves establishing long-term contracts with key industrial clients and government agencies, enhancing brand recognition and customer loyalty. Future trends indicate increasing collaboration within ecosystems to develop comprehensive safety solutions integrating gas detection with broader industrial automation systems, intensifying competitive dynamics.

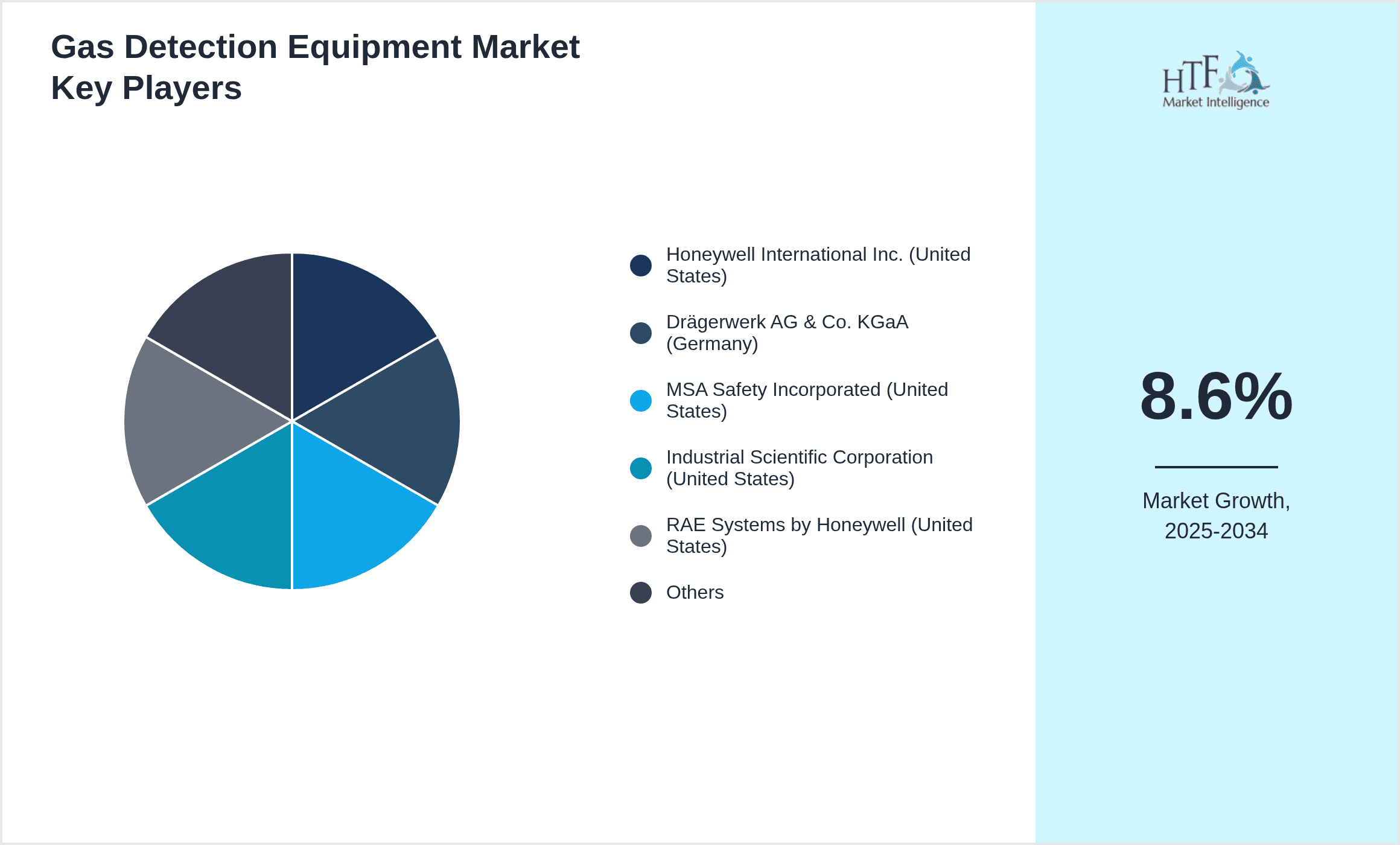

Companies Shaping the Gas Detection Equipment Market

- •Honeywell International Inc. (United States)

- •Drägerwerk AG & Co. KGaA (Germany)

- •MSA Safety Incorporated (United States)

- •Industrial Scientific Corporation (United States)

- •RAE Systems by Honeywell (United States)

- •Emerson Electric Co. (United States)

- •Crowcon Detection Instruments Ltd. (United Kingdom)

- •Riken Keiki Co., Ltd. (Japan)

- •Sensidyne, LP (United States)

- •Miranova Technologies Pvt Ltd (India)

- •Blackline Safety Corp. (Canada)

- •Teledyne Technologies Incorporated (United States)

- •Yokogawa Electric Corporation (Japan)

- •General Electric Company (United States)

- •Siemens AG (Germany)

- •Sensit Technologies, Inc. (United States)

- •GfG Gesellschaft für Gerätebau mbH (Germany)

- •Det-Tronics (United States)

- •Mine Safety Appliances Company (United States)

- •Crowcon Detection Instruments Ltd. (United Kingdom)

- •Industrial Scientific Corporation (United States)

- •Honeywell Analytics (United States)

- •Amphenol Advanced Sensors (United States)

- •Sensorex (United States)

- •Dynament Ltd. (United Kingdom)

Market Breakdown

- •By Type

- ◦Fixed Gas Detectors

- ◦Portable Gas Detectors

- ◦Wireless Gas Detectors

- ◦Photoionization Detectors

- ◦Flame Detectors

- •By Application

- ◦Industrial Safety

- ◦Environmental Monitoring

- ◦Oil & Gas

- ◦Chemical Processing

- ◦Mining

- •By End-Use Industry

- ◦Oil & Gas

- ◦Chemical Manufacturing

- ◦Mining & Metals

- ◦Construction & Infrastructure

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors

- ◦Online Retail

Growth Dynamics

- •Increasing industrial safety regulations globally are a primary growth driver, compelling industries to adopt advanced gas detection equipment to comply with stringent occupational health standards. For example, regulatory mandates in North America and Europe require continuous gas monitoring in hazardous environments, boosting fixed gas detector adoption.

- •Technological advancements such as integration of wireless communication and IoT capabilities in gas detectors enable real-time remote monitoring and predictive maintenance, significantly enhancing operational efficiency and safety management across sectors.

- •Rising industrialization and urbanization in emerging economies, especially in Asia-Pacific, have escalated demand for gas detection solutions to safeguard expanding industrial facilities and infrastructure projects from gas-related hazards.

- •Growing environmental concerns and stricter emission control policies drive the adoption of gas detection equipment in environmental monitoring applications, facilitating early detection of harmful gases and regulatory compliance.

- •The increasing use of portable and wireless gas detectors among field workers and emergency responders for enhanced flexibility and safety in dynamic environments contributes significantly to market expansion.

- •Investment in R&D by leading players to develop multi-gas detectors with improved sensitivity and longer battery life is fostering product innovation and market growth.

- •Strategic collaborations between technology providers and industrial companies enable customized gas detection solutions, further expanding market penetration and application scope.

Market Trends

- •The adoption of smart gas detection systems integrated with cloud-based analytics platforms is reshaping the market by providing actionable insights and predictive safety measures, improving decision-making processes for industrial safety managers.

- •Emerging trends include miniaturization and enhanced portability of gas detectors, facilitating wider deployment in confined spaces and remote locations without compromising detection accuracy.

- •Manufacturers are increasingly focusing on developing multi-gas detectors capable of simultaneously sensing various hazardous gases, reducing equipment redundancy and operational costs.

- •Sustainability initiatives are driving demand for environmentally friendly gas detection solutions that consume less power and utilize recyclable materials, aligning with global green policies.

- •Collaborative ecosystem development involving sensor manufacturers, software developers, and industrial end-users is fostering innovation and seamless integration of gas detection with broader industrial IoT frameworks.

- •Consumer preference is shifting towards advanced wireless and wearable gas detection devices that offer mobility, ease of use, and enhanced safety features, expanding market reach.

- •Disruptive innovations such as AI-powered gas detection analytics and autonomous monitoring drones are anticipated to transform future market landscapes by enabling proactive safety management.

Market Opportunities

- •Expanding industrial infrastructure in developing regions presents substantial growth opportunities for gas detection equipment manufacturers to introduce tailored solutions addressing local safety challenges and regulatory frameworks.

- •Untapped applications in sectors like agriculture and pharmaceuticals offer new avenues for product diversification and market expansion beyond traditional heavy industries.

- •Investment in developing wireless and IoT-enabled gas detection systems facilitates entry into smart factory and Industry 4.0 ecosystems, capitalizing on rising digital transformation trends.

- •Geographical expansion into emerging markets with rapidly growing industrial bases and lax existing safety infrastructure provides lucrative prospects for early market entrants.

- •Enhanced value propositions through integrated safety solutions combining gas detection with emergency response and environmental monitoring systems can differentiate offerings and capture new customer segments.

- •Strategic partnerships and acquisitions aimed at technology sharing and portfolio broadening can accelerate innovation cycles and market penetration.

- •Anticipated regulatory tightening globally is expected to increase mandatory gas detection deployments, creating sustained demand and long-term market stability.

Market Challenges

- •High initial investment and maintenance costs of advanced gas detection systems can hinder adoption, particularly among small and medium enterprises with limited safety budgets.

- •Technical limitations such as sensor cross-sensitivity, calibration complexity, and false alarm rates pose challenges to accuracy and reliability, affecting user confidence.

- •Fragmented regulatory standards across regions create compliance complexities for manufacturers and end-users, impeding streamlined global product deployment.

- •Intense competition from low-cost local manufacturers offering basic gas detection devices pressures pricing and profit margins of established players.

- •Supply chain disruptions and raw material volatility impact manufacturing schedules and cost structures, potentially delaying market growth.

- •Limited awareness and training regarding proper use and maintenance of gas detection equipment in certain regions reduce operational effectiveness and market penetration.

- •Challenges in integrating legacy industrial systems with modern gas detection technologies slow adoption of advanced solutions.

Regulatory Framework

- •From 2019 to 2024, multiple regions implemented stricter occupational safety regulations mandating continuous gas monitoring in hazardous industries, including the US OSHA updates and EU ATEX directives enforcing equipment certification and installation standards, significantly impacting market demand.

- •Enforcement of international standards such as IECEx and ISO 9001 for gas detection equipment manufacturing and quality assurance has led companies to enhance product reliability and compliance measures.

- •Environmental regulations targeting emission reductions and air quality improvements, notably in Asia-Pacific and Europe, require deployment of gas detectors for real-time pollution monitoring, expanding application scope.

- •Country-specific mandates such as China’s GB standards for hazardous area equipment and India’s factory safety codes have driven regional market growth by enforcing mandatory safety equipment installation.

- •Government initiatives offering incentives and subsidies for workplace safety technology adoption have encouraged investments in advanced gas detection systems, facilitating market expansion globally.

Market Intelligence

- •15th January 2025, Honeywell International Inc. launched its next-generation wireless gas detection system featuring enhanced sensor accuracy, extended battery life, and seamless integration with cloud-based safety management platforms. This innovation targets industrial clients aiming to enhance operational safety and streamline monitoring processes with real-time data analytics and remote alerts. The system supports multi-gas detection capabilities and is designed for harsh environments, positioning Honeywell as a technology leader in the evolving gas detection market. This product launch is expected to accelerate wireless detector adoption and expand Honeywell’s market share globally. Source: Official Honeywell Press Release

- •20th March 2025, Drägerwerk AG & Co. KGaA introduced a new portable multi-gas detector equipped with AI-powered analytics to predict hazardous gas leaks before occurrence. The device enhances worker safety by providing early warnings and actionable insights through a mobile app interface. Dräger’s strategic focus on AI integration signifies a shift towards smart safety devices in industrial sectors. This launch strengthens the company’s product portfolio and addresses growing demand for intelligent monitoring solutions in mining and chemical industries. Source: Dräger Corporate News

- •10th May 2025, Industrial Scientific Corporation announced a global partnership with a leading cloud software provider to develop an integrated safety ecosystem combining gas detection hardware with advanced data analytics and workforce safety management tools. This collaboration aims to deliver comprehensive solutions for real-time hazard detection, compliance tracking, and emergency response optimization across multiple industries. The strategic alliance enhances Industrial Scientific’s competitive positioning by expanding its service offerings and digital capabilities, fostering deeper customer engagement and operational excellence. Source: Industrial Scientific Press Release

- •5th July 2025, Emerson Electric Co. completed the acquisition of a niche wireless sensor manufacturer specializing in IoT-enabled gas detection modules. This acquisition broadens Emerson’s technological capabilities and accelerates its entry into smart industrial safety markets. The integration is expected to generate synergies in product development and expand Emerson’s global footprint in emerging markets with rising safety infrastructure investments. The move reflects ongoing consolidation trends within the gas detection equipment industry aimed at innovation and market expansion. Source: Emerson Corporate Announcement

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 8.2 Billion |

| Forecast Year Market Size | USD 19.5 Billion |

| CAGR | 8.6% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7.9% |

| Scope of Report | Market is segmented by Type (Fixed Gas Detectors, Portable Gas Detectors, Wireless Gas Detectors, Photoionization Detectors, Flame Detectors), Application (Industrial Safety, Environmental Monitoring, Oil & Gas, Chemical Processing, Mining), End-Use Industry (Oil & Gas, Chemical Manufacturing, Mining & Metals, Construction & Infrastructure), Distribution Channel (Direct Sales, Distributors, Online Retail) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Honeywell International Inc. (United States), Drägerwerk AG & Co. KGaA (Germany), MSA Safety Incorporated (United States), Industrial Scientific Corporation (United States), RAE Systems by Honeywell (United States), Emerson Electric Co. (United States), Crowcon Detection Instruments Ltd. (United Kingdom), Riken Keiki Co., Ltd. (Japan), Sensidyne, LP (United States), Miranova Technologies Pvt Ltd (India), Blackline Safety Corp. (Canada), Teledyne Technologies Incorporated (United States), Yokogawa Electric Corporation (Japan), General Electric Company (United States), Siemens AG (Germany), Sensit Technologies, Inc. (United States), GfG Gesellschaft für Gerätebau mbH (Germany), Det-Tronics (United States), Mine Safety Appliances Company (United States), Crowcon Detection Instruments Ltd. (United Kingdom), Industrial Scientific Corporation (United States), Honeywell Analytics (United States), Amphenol Advanced Sensors (United States), Sensorex (United States), Dynament Ltd. (United Kingdom) |

Global Gas Detection Equipment Market Size, Growth & Revenue 2024-2034 - Table of Contents

Research enthusiast focused on transforming data uncovering into actionable insights through data-driven decision-making.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.