Global Dust Collection Systems Market Size, Growth & Revenue 2025-2034

Global Dust Collection Systems Market is segmented by Product Type (Baghouse Collectors, Cartridge Collectors, Electrostatic Precipitators, Cyclone Collectors, Wet Scrubbers), Application (Industrial Manufacturing, Power Generation, Pharmaceuticals, Food Processing, Chemical Processing), End-Use Industry (Metals & Mining, Cement & Construction, Automotive, Electronics), Distribution Channel (Direct Sales, Distributors, After-Sales Service Networks), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

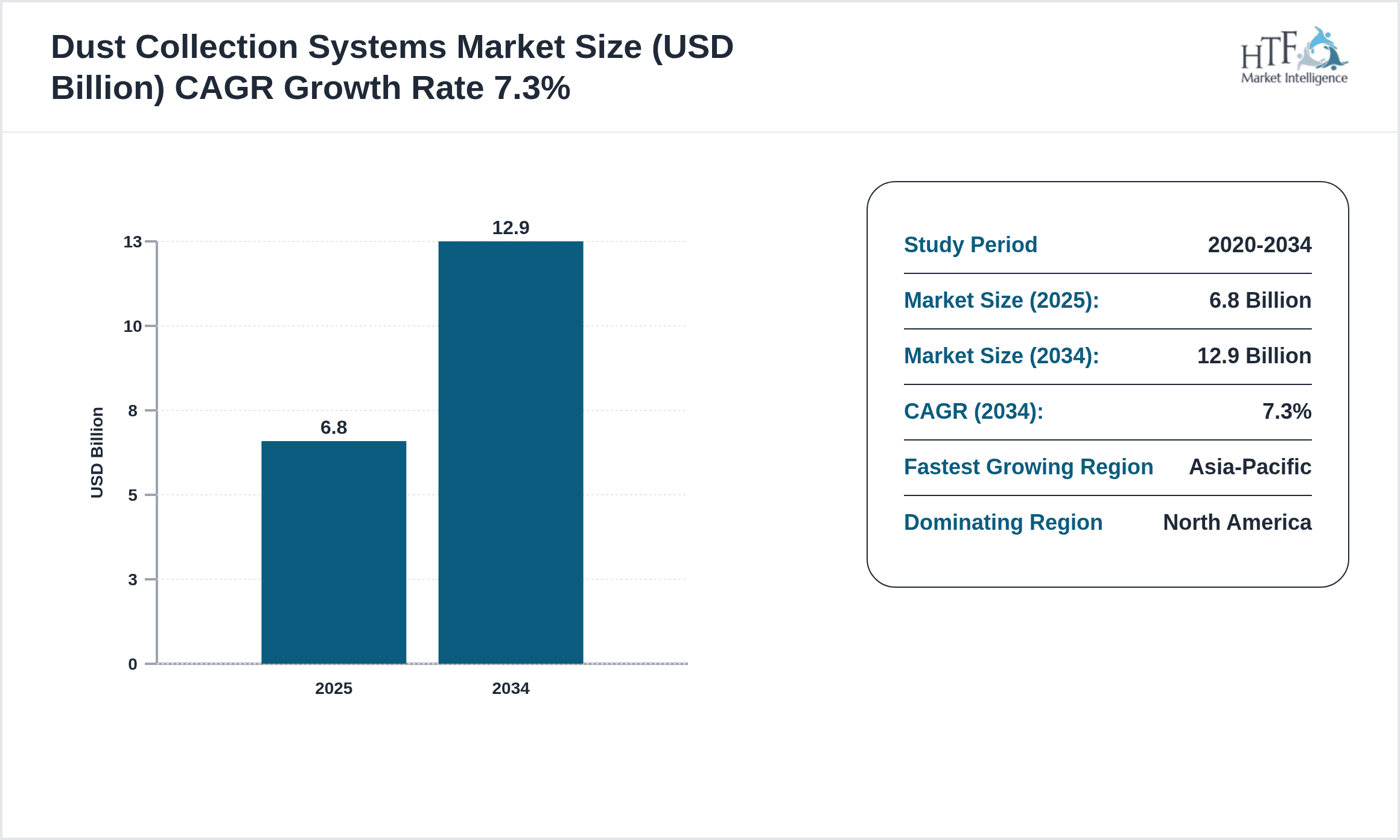

- •The global Dust Collection Systems market is a critical segment within industrial environmental control, focusing on technologies that capture and filter airborne dust and particulates to ensure compliance with environmental standards and promote occupational health. The market consists of diverse product types including Baghouse Collectors, Cartridge Collectors, Electrostatic Precipitators, Cyclone Collectors, and Wet Scrubbers, each optimized for specific operational conditions and dust characteristics. Applications are widespread across industrial manufacturing, power generation, pharmaceuticals, food processing, and chemical processing sectors, reflecting the essential role of dust collection in maintaining process integrity and environmental safety. Market growth is stimulated by increasing industrial activities worldwide alongside tightening regulatory frameworks aimed at reducing air pollution and safeguarding worker health. Advances in filtration technology, automation, and energy-efficient designs are propelling innovation within the market. Regionally, North America dominates due to stringent regulations and technological advancements, while Asia-Pacific is the fastest growing region, driven by rapid industrialization and urban expansion. This comprehensive report delivers a detailed analysis of market trends, key players, growth drivers, challenges, and opportunities, supporting strategic decision-making for manufacturers, investors, and policy makers across the globe.

- •Key market highlights include a base market size of USD 6.8 Billion in 2025, with projections to reach USD 12.9 Billion by 2034, reflecting a robust CAGR of 7.3%. The Baghouse Collectors segment leads the product category, benefiting from its versatility and efficiency in various dust control applications, whereas Cartridge Collectors are identified as the fastest growing product type due to their compact design and enhanced filtration capabilities. Regional dynamics illustrate North America’s dominance attributed to regulatory rigor and technological leadership, while Asia-Pacific’s rapid economic growth and expanding industrial base contribute to its status as the fastest growing region. Market challenges such as high capital investment and complex maintenance requirements persist but are mitigated by opportunities in emerging economies and technological innovations.

- •The strategic importance of dust collection systems spans multiple industries, offering critical solutions for air quality management, regulatory compliance, and operational efficiency. Stakeholders including manufacturers, end-users, policymakers, and investors benefit from understanding the evolving market dynamics, technological advancements, and regional growth patterns. The market’s value proposition lies in its ability to reduce environmental pollution, enhance worker safety, and optimize industrial processes, thereby driving sustainability and economic viability. This report equips decision-makers with actionable insights to capitalize on emerging opportunities and navigate challenges within the global dust collection systems landscape.

Competitive Landscape

The global Dust Collection Systems market exhibits a highly competitive environment characterized by the presence of multinational corporations and regional players striving for technological leadership and market share expansion. Competitors employ diverse strategies including product innovation, strategic partnerships, mergers and acquisitions, and geographic expansion to enhance their positioning. Innovation is primarily focused on improving filtration efficiency, reducing energy consumption, and integrating automation to meet evolving regulatory standards and customer expectations. Pricing strategies vary by region, with developed markets emphasizing quality and compliance while emerging markets prioritize cost-effectiveness. Distribution channels encompass direct sales, distributors, and after-sales service networks, enabling wide market reach. Barriers to entry include substantial capital investment requirements, technological complexity, and stringent compliance mandates, which collectively consolidate the market among established players. Regional competition is influenced by differing regulatory regimes and industrial growth rates, with North America and Europe dominated by technologically advanced companies, and Asia-Pacific marked by rapid market entry and expansion of local manufacturers. Future competitive trends suggest increased consolidation, adoption of Industry 4.0 technologies, and a growing focus on sustainable and energy-efficient solutions, shaping the market’s competitive trajectory.

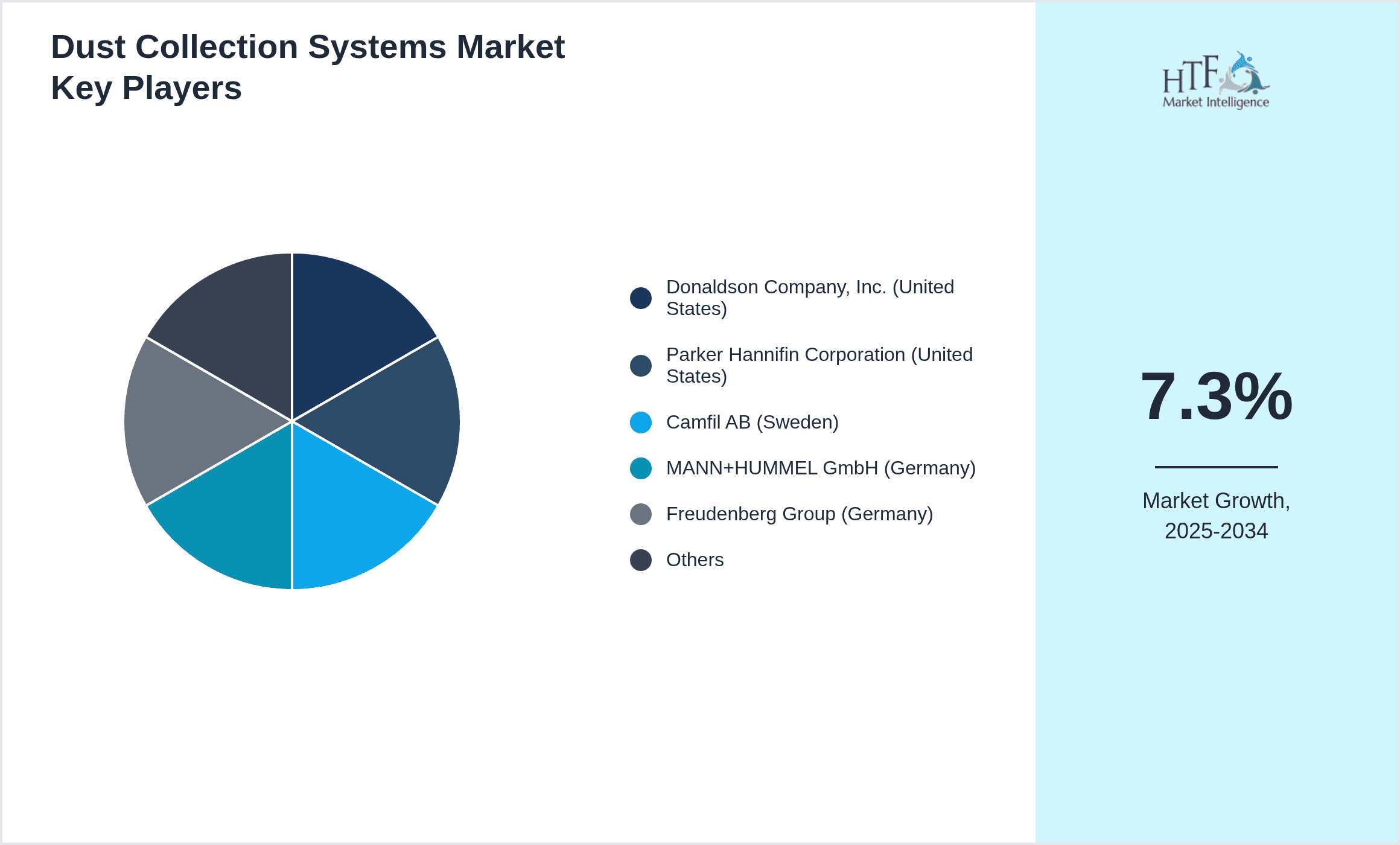

Prominent Players in Dust Collection Systems Market

- •Donaldson Company, Inc. (United States)

- •Parker Hannifin Corporation (United States)

- •Camfil AB (Sweden)

- •MANN+HUMMEL GmbH (Germany)

- •Freudenberg Group (Germany)

- •FLSmidth & Co. A/S (Denmark)

- •Ahlstrom-Munksjö (Finland)

- •Babcock & Wilcox Enterprises, Inc. (United States)

- •Nederman Holding AB (Sweden)

- •Eaton Corporation plc (Ireland)

- •ABB Ltd. (Switzerland)

- •Thermax Limited (India)

- •Pulva Corporation (Japan)

- •Koch Filter Corporation (United States)

- •Aqua-Air Systems, Inc. (United States)

- •Camfil APC (United States)

- •General Electric Company (United States)

- •Alstom SA (France)

- •Hitachi Zosen Corporation (Japan)

- •Lindberg & Lund AB (Sweden)

- •Nordfab Industrial Ducting (United States)

- •Met-Pro Corporation (United States)

- •B+S Group (Germany)

- •Clarke Energy (United Kingdom)

- •Dustcontrol AB (Sweden)

Market Breakdown

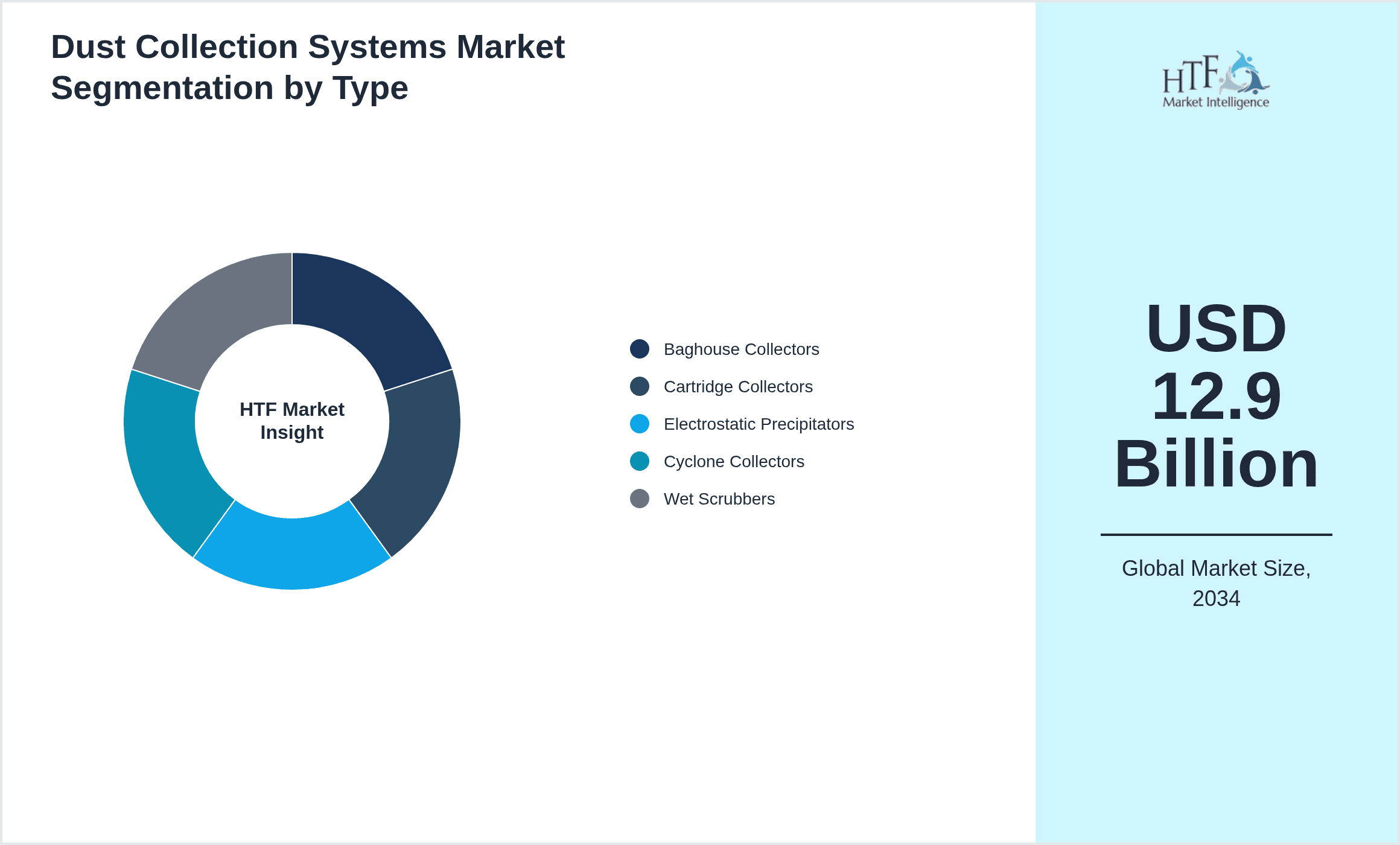

- •By Product Type

- ◦Baghouse Collectors

- ◦Cartridge Collectors

- ◦Electrostatic Precipitators

- ◦Cyclone Collectors

- ◦Wet Scrubbers

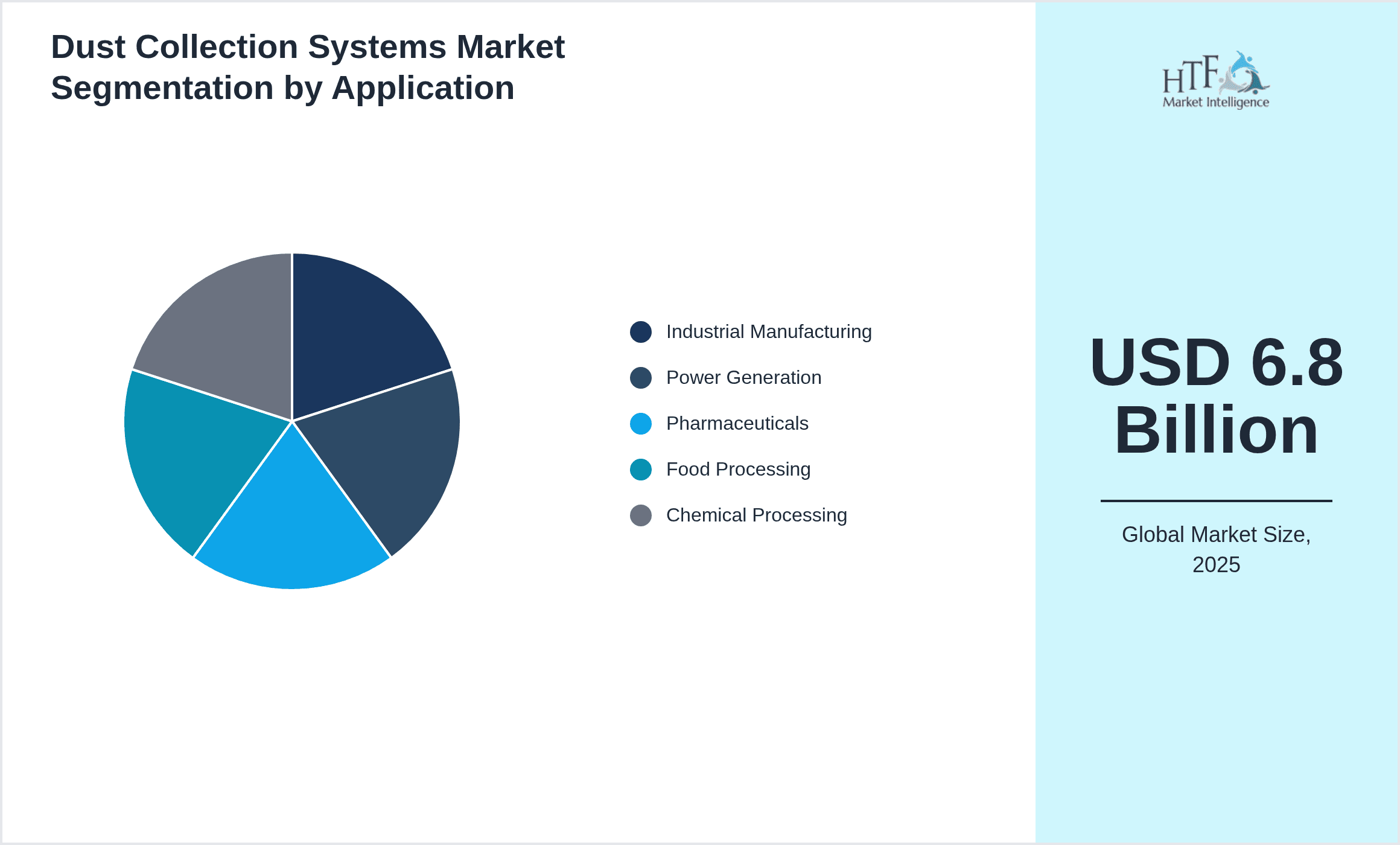

- •By Application

- ◦Industrial Manufacturing

- ◦Power Generation

- ◦Pharmaceuticals

- ◦Food Processing

- ◦Chemical Processing

- •By End-Use Industry

- ◦Metals & Mining

- ◦Cement & Construction

- ◦Automotive

- ◦Electronics

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors

- ◦After-Sales Service Networks

Growth Dynamics

The global Dust Collection Systems market is propelled by stringent environmental regulations worldwide that mandate industries to reduce particulate emissions, driving widespread adoption of advanced dust control technologies. Industrialization and urbanization in emerging economies increase demand for efficient dust collection solutions to mitigate pollution and safeguard worker health. Technological advancements such as high-efficiency filtration media, automation integration, and energy-saving designs enhance system performance and reduce operational costs, making adoption more attractive. Additionally, growing awareness about occupational safety and environmental sustainability among stakeholders fuels market growth. Investment in research and development by key players results in innovative product offerings tailored to industry-specific needs, further stimulating demand. The shift towards Industry 4.0 and smart manufacturing introduces opportunities for dust collection systems equipped with IoT capabilities for real-time monitoring and predictive maintenance, enhancing operational efficiency and compliance.

Market Trends

The dust collection systems market is witnessing a trend towards modular and compact designs such as cartridge collectors that enable flexible installation and space optimization in constrained industrial environments. Increasing adoption of automation and digital control systems is enabling improved monitoring, maintenance, and energy management, aligning with broader Industry 4.0 initiatives. Sustainability trends are driving demand for energy-efficient and low-emission dust collectors, with innovations focusing on reducing carbon footprint and lifecycle costs. Collaborations between technology providers and end-users are fostering co-development of tailored solutions that address specific operational challenges. Additionally, growing emphasis on compliance with global emission standards is incentivizing upgrades and retrofits of existing dust collection infrastructure, further supporting market expansion.

Market Opportunities

Emerging economies present significant growth opportunities due to rapid industrialization and increasing regulatory enforcement on air quality, creating demand for advanced dust collection solutions. Technological innovation in filtration materials and system automation opens avenues for product differentiation and value-added services. There is a rising need for retrofit solutions to upgrade legacy dust collectors for enhanced efficiency and compliance. Expansion into underpenetrated sectors such as pharmaceuticals and food processing offers new application potential. Strategic partnerships and collaborations between technology providers, system integrators, and end-users can accelerate market entry and adoption, while growing awareness about environmental sustainability among industries provides impetus for investing in cutting-edge dust control technologies.

Market Challenges

High capital expenditure and operational maintenance costs present significant barriers to adoption, particularly in price-sensitive emerging markets. Complex system designs and the need for skilled labor for installation and upkeep limit widespread deployment. Variability in global regulatory frameworks and enforcement creates challenges for manufacturers aiming to offer standardized solutions. Competition from alternative air pollution control technologies can restrict market growth. Additionally, disruptions in raw material supply chains and fluctuations in industrial production volumes due to economic uncertainties impact market stability. Addressing these challenges requires continuous innovation, cost optimization, and strategic market positioning.

Regulatory Framework

From 2020 to 2025, regulatory frameworks globally have become increasingly stringent, mandating industries to limit particulate emissions and improve workplace air quality. Key regulations such as the U.S. EPA’s National Emission Standards for Hazardous Air Pollutants (NESHAP) and the European Union’s Industrial Emissions Directive (IED) enforce strict compliance standards with defined emission limits and monitoring requirements. These regulations necessitate the adoption of efficient dust collection systems with certified filtration performance. Countries in Asia-Pacific, including China and India, have implemented tighter air pollution control policies, driving market demand. Compliance with Occupational Safety and Health Administration (OSHA) standards further emphasizes worker safety and exposure limits to airborne dust. Governments also provide incentives and subsidies encouraging the modernization of dust control equipment. The regulatory landscape influences market innovation, driving development of systems that meet evolving environmental and safety standards while balancing operational costs.

Market Intelligence

- •15th January 2025, Donaldson Company, Inc. launched its latest high-efficiency cartridge dust collector designed for pharmaceutical and food processing applications. The product features advanced filter media that improves particulate capture efficiency by 15% while reducing energy consumption by 10%. The system integrates IoT-enabled sensors for real-time monitoring and predictive maintenance, enhancing operational uptime and compliance with stringent industry standards. Donaldson aims to leverage this innovation to expand its footprint in emerging markets where regulatory enforcement is intensifying. This launch aligns with the company's strategy to focus on sustainable, smart dust collection solutions that meet diverse application needs. Source: Donaldson Official Press Release

- •30th March 2025, Camfil AB introduced a modular baghouse dust collector targeting the cement and mining industries. The design allows rapid customization and scalability, reducing installation time by 20%. Enhanced dust filtration technology meets updated EU emission standards, supporting customers in achieving compliance with lower operational costs. Camfil’s strategic initiative focuses on digital integration for remote diagnostics and lifecycle management, positioning it competitively in the European and Asia-Pacific markets. This innovation supports the company’s commitment to environmental sustainability and operational efficiency. Source: Camfil Annual Report 2025

- •10th June 2025, Parker Hannifin Corporation announced a partnership with a leading industrial IoT platform provider to develop smart dust collection systems with predictive analytics capabilities. This collaboration aims to enhance equipment reliability and reduce maintenance costs by leveraging data-driven insights. The initiative targets customers across power generation, chemical processing, and manufacturing sectors globally. Parker Hannifin plans to integrate these solutions into its existing product portfolio, improving customer value through enhanced operational efficiency and regulatory compliance. This partnership exemplifies the growing trend of digital transformation in industrial environmental controls. Source: Parker Hannifin Corporate News

- •5th September 2025, FLSmidth & Co. A/S completed the acquisition of a regional dust collection system manufacturer in Asia-Pacific, strengthening its market presence and product portfolio. The acquisition enables FLSmidth to offer localized solutions tailored to the unique requirements of rapidly industrializing economies. It also provides access to established distribution networks and technical expertise, fostering accelerated growth in the region. This strategic move supports the company’s expansion objectives and its commitment to delivering sustainable dust control technologies worldwide. Source: FLSmidth Investor Relations Announcement

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 6.8 Billion |

| Forecast Year Market Size | USD 12.9 Billion |

| CAGR | 7.3% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7% |

| Scope of Report | Market is segmented by Product Type (Baghouse Collectors, Cartridge Collectors, Electrostatic Precipitators, Cyclone Collectors, Wet Scrubbers), Application (Industrial Manufacturing, Power Generation, Pharmaceuticals, Food Processing, Chemical Processing), End-Use Industry (Metals & Mining, Cement & Construction, Automotive, Electronics), Distribution Channel (Direct Sales, Distributors, After-Sales Service Networks) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Donaldson Company, Inc. (United States), Parker Hannifin Corporation (United States), Camfil AB (Sweden), MANN+HUMMEL GmbH (Germany), Freudenberg Group (Germany) |

Global Dust Collection Systems Market Size, Growth & Revenue 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.