Global Smart Windows Materials Market Size, Growth & Revenue 2025-2034

Global Smart Windows Materials Market is segmented by Type (Electrochromic, Thermochromic, Photochromic, Suspended Particle Devices, Liquid Crystal Devices), Application (Residential Buildings, Commercial Buildings, Automotive, Aerospace, Healthcare), End-Use Industry (Construction, Automotive, Transportation, Healthcare), Distribution Channel (Direct Sales, Distributors, Online Platforms), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global smart windows materials market comprises innovative glazing technologies that dynamically regulate light and thermal transmission using materials such as electrochromic, thermochromic, photochromic, suspended particle devices, and liquid crystal devices. These materials serve a broad spectrum of applications including residential and commercial buildings, automotive, aerospace, and healthcare industries. The market addresses rising energy efficiency demands by enabling adaptive control of solar heat gain and daylight penetration, which contributes to reduced HVAC energy consumption and enhanced occupant comfort. Growing environmental concerns and stringent regulations worldwide accelerate the adoption of smart window technologies, fostering advancements and integration with smart building systems. The market's evolving landscape reflects the intersection of material science innovation, sustainability imperatives, and increasing urbanization, positioning smart windows materials as critical components in achieving energy-efficient infrastructure and reducing carbon footprints globally.

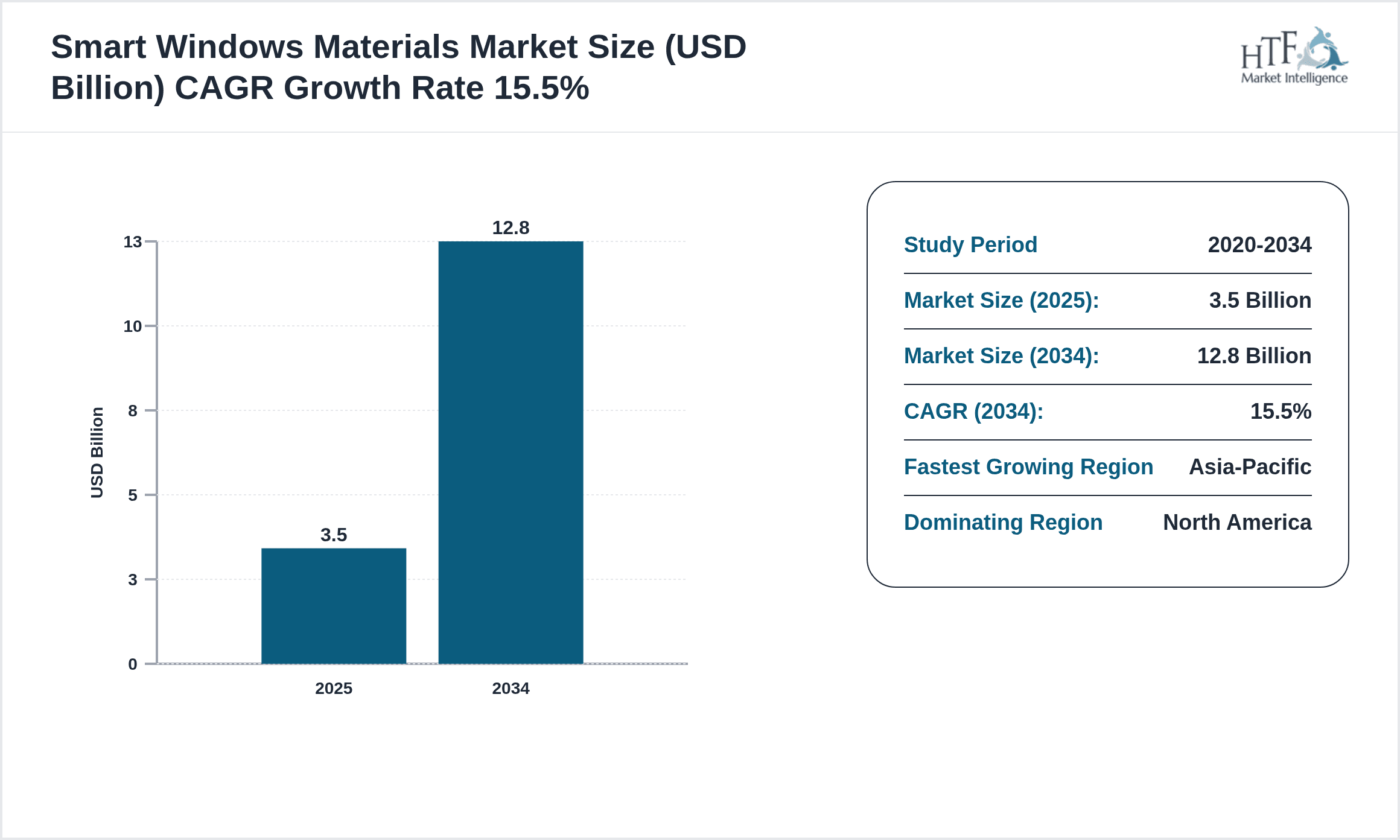

- •Key highlights include a robust CAGR of 15.5% forecasted from 2025 to 2034, driven by technological advancements and expanding applications across diverse sectors. The base market size of USD 3.5 Billion in 2025 is projected to reach USD 12.8 Billion by 2034. North America dominates the market due to early technological adoption and favorable regulations, while Asia-Pacific is the fastest growing region fueled by rapid urbanization and infrastructure development. Electrochromic materials hold the leading product type market share, with liquid crystal devices demonstrating the highest growth rate. Commercial and residential buildings remain the primary applications supporting sustained demand. Increasing investments in smart infrastructure and energy conservation policies underpin the strategic significance of this market worldwide.

- •The value proposition of smart windows materials lies in their ability to improve energy efficiency, reduce operational costs, and enhance occupant well-being across multiple industries. They offer strategic benefits for stakeholders including manufacturers, architects, automotive producers, and policymakers seeking sustainable solutions. Integration with IoT and smart building technologies further amplifies their importance in modern infrastructure. This market presents opportunities for innovation, geographic expansion, and cross-industry collaborations, making smart windows materials a pivotal segment in the global transition towards greener, more adaptive environments.

Competitive Landscape

The competitive landscape of the global smart windows materials market is marked by intense innovation, strategic partnerships, and expansion initiatives to consolidate market presence and leverage emerging opportunities. Companies focus on continuous product development to enhance performance, durability, and cost-efficiency of smart glazing solutions. Technology adoption, such as integration with building management systems and IoT platforms, differentiates market participants. Collaborations with construction firms, automotive manufacturers, and technology providers facilitate market penetration across applications. Mergers and acquisitions remain instrumental for expanding product portfolios and geographic reach. Regional competition is influenced by local regulatory frameworks and infrastructure development priorities, requiring tailored strategies. Pricing strategies emphasize balancing affordability with advanced features to capture diverse customer segments. Distribution channels are evolving to include direct sales, channel partners, and digital platforms. Future trends indicate a shift towards sustainable manufacturing and smart coatings that offer multifunctional benefits. Companies investing in R&D and customer-centric innovations are positioned to sustain competitive advantages amid rising market complexities.

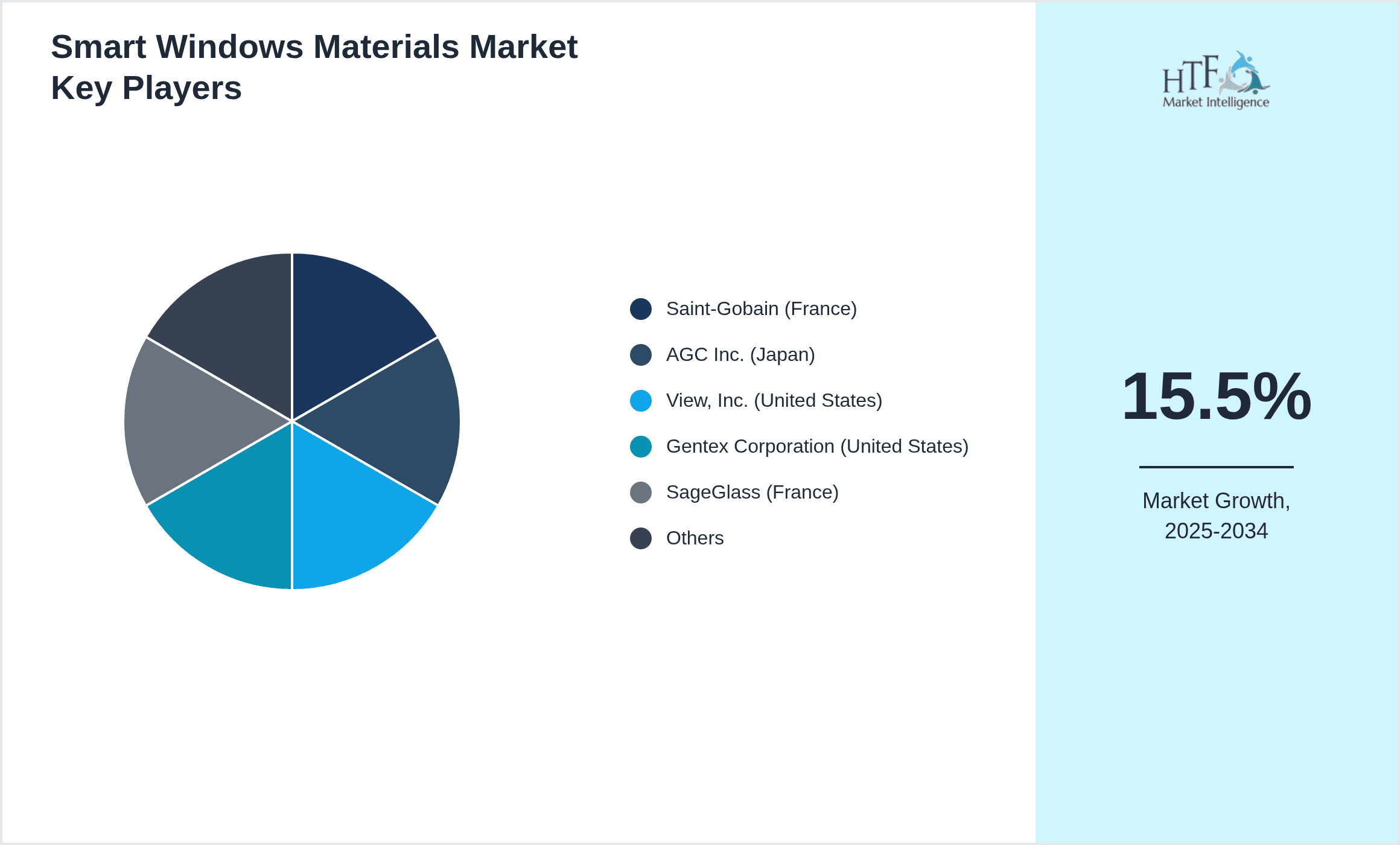

Leading Companies in Smart Windows Materials Market

- •Saint-Gobain (France)

- •AGC Inc. (Japan)

- •View, Inc. (United States)

- •Gentex Corporation (United States)

- •SageGlass (France)

- •Halio Inc. (United States)

- •Research Frontiers Inc. (United States)

- •Guardian Glass (United States)

- •Kinestral Technologies (United States)

- •Polytronix, Inc. (United States)

- •Chromogenics ASA (Norway)

- •Smartglass International (United Kingdom)

- •Gentex Corporation (United States)

- •Pleotint, LLC (United States)

- •View Inc. (United States)

- •Eastman Chemical Company (United States)

- •YKK AP Inc. (Japan)

- •AGP Lighting Solutions (South Korea)

- •Smartglass Australia Pty Ltd (Australia)

- •KDX Group (Japan)

Market Breakdown

- •By Type

- ◦Electrochromic

- ◦Thermochromic

- ◦Photochromic

- ◦Suspended Particle Devices

- ◦Liquid Crystal Devices

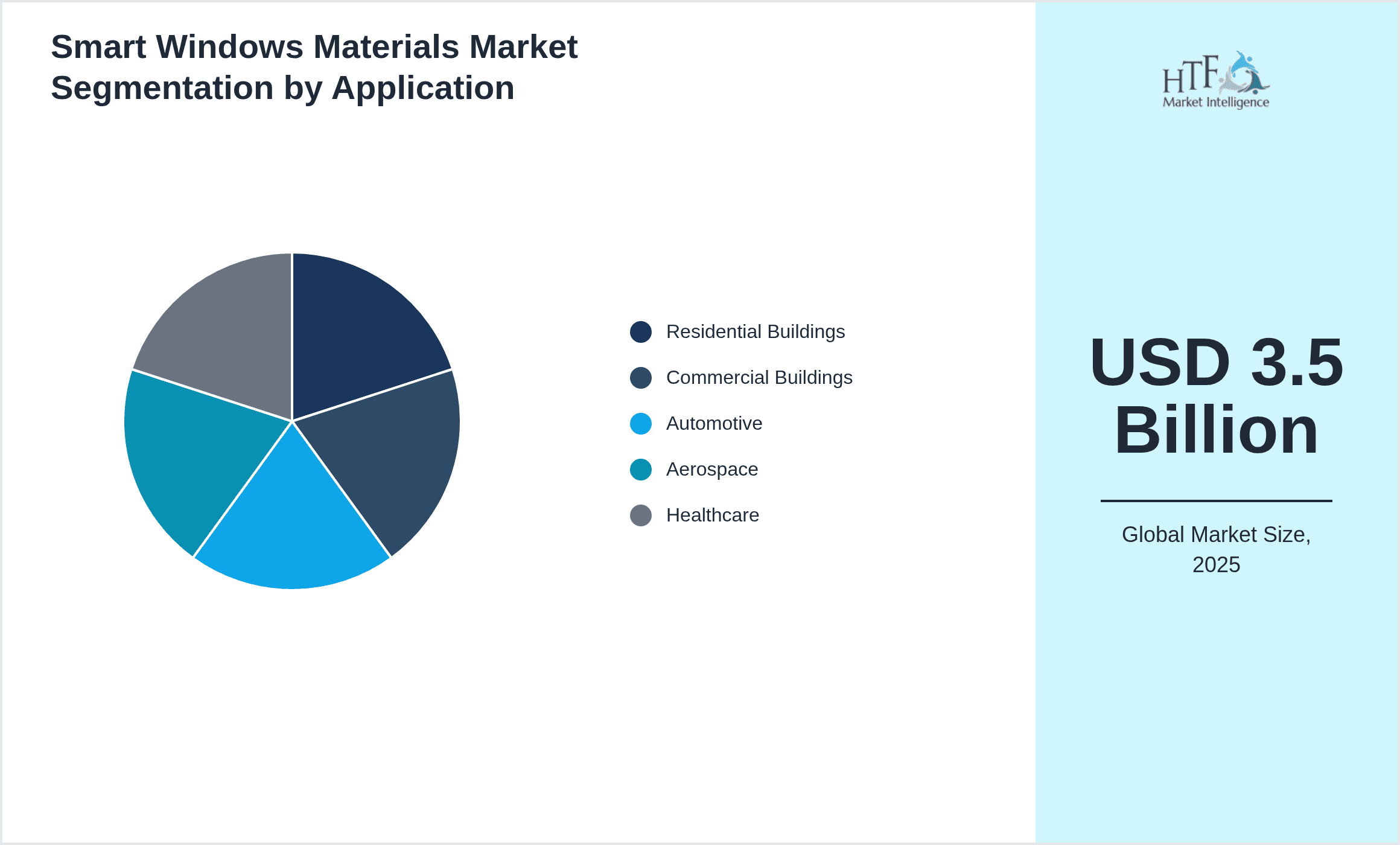

- •By Application

- ◦Residential Buildings

- ◦Commercial Buildings

- ◦Automotive

- ◦Aerospace

- ◦Healthcare

- •By End-Use Industry

- ◦Construction

- ◦Automotive

- ◦Transportation

- ◦Healthcare

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors

- ◦Online Platforms

Growth Dynamics

Rapid urbanization and increasing demand for energy-efficient buildings significantly drive the smart windows materials market. Governments globally implement stringent energy regulations promoting green building certifications, compelling stakeholders to integrate smart glazing solutions. Recent initiatives like the European Green Deal and the U.S. Energy Star program incentivize adoption through subsidies and tax benefits. Technological advancements in electrochromic materials enhance durability and responsiveness, reducing installation costs and improving ROI. For example, View Inc. recently expanded its smart window installations across commercial complexes in North America, showcasing scalable applications. The escalating focus on occupant comfort by regulating daylight and thermal gain further accelerates market growth. Integration with smart home automation and IoT elevates the market potential by enabling remote control and data analytics. Additionally, the automotive sector increasingly incorporates smart windows for passenger comfort and energy savings, with OEMs collaborating with material manufacturers for customized solutions. Collectively, these factors create a robust ecosystem supporting sustained market expansion globally.

Market Trends

Smart windows materials trend towards multifunctionality combining energy efficiency with aesthetics and user experience. Innovations include integrating photovoltaic capabilities that generate electricity while modulating light transmission, as demonstrated by AGC Inc.'s recent R&D breakthroughs. The rising adoption of liquid crystal devices offers faster switching times and improved clarity, gaining traction in automotive and aerospace applications. Digitalization trends propel the incorporation of sensors and AI algorithms enabling adaptive glazing that responds to environmental conditions autonomously. Sustainability drives material development focusing on recyclable and environmentally friendly components, aligning with circular economy principles. Regional markets like Asia-Pacific witness rapid growth fueled by smart city projects and infrastructure modernization, creating lucrative opportunities for market entrants. Moreover, collaborations between tech startups and established manufacturers foster innovation ecosystems accelerating commercialization. The shift towards retrofit solutions for existing buildings expands the addressable market, supported by growing awareness among consumers and architects. These evolving trends position smart windows materials as integral to next-generation building technologies worldwide.

Market Opportunities

Emerging opportunities in the smart windows materials market center around expanding applications in transportation and healthcare sectors. The automotive industry's shift to electric vehicles creates demand for energy-saving smart windows that extend driving range and enhance passenger comfort, exemplified by Gentex Corporation's partnerships with leading OEMs. Healthcare facilities seek smart glazing solutions to improve patient well-being by controlling daylight exposure and reducing glare, driving demand in hospital infrastructure projects. Geographic expansion in developing regions such as Latin America and Middle East & Africa offers untapped markets with rising construction activities and urbanization. Advances in nanotechnology and material science open avenues for next-generation smart windows with improved responsiveness and durability, encouraging R&D investments. Integration with renewable energy systems like building-integrated photovoltaics presents cross-sector growth potential. Strategic collaborations and mergers enable companies to penetrate new markets and diversify offerings. Government incentives for sustainable construction and energy-efficient transportation further stimulate demand, making the smart windows materials market a promising domain for innovation and investment.

Market Challenges

High initial costs of smart windows materials and complex installation processes pose significant challenges impacting widespread adoption, particularly in price-sensitive regions. The durability and long-term performance concerns associated with some technologies, such as electrochromic coatings, limit customer confidence. Supply chain disruptions and raw material price volatility further strain manufacturers’ operational efficiency and profitability. Regulatory heterogeneity across regions complicates compliance and market entry strategies for global players. For instance, varying safety and environmental standards require product customization, increasing development costs. The lack of standardized testing protocols for smart glazing performance undermines market transparency and customer decision-making. Additionally, limited awareness and understanding among end-users and architects about smart window benefits constrain demand growth. Recent reports indicate delays in project implementations due to integration challenges with building management systems. Intellectual property disputes and intense competition also create barriers for smaller companies striving to scale. Addressing these multifaceted challenges necessitates coordinated efforts among stakeholders to enable sustainable market development.

Regulatory Framework

In the past five years, regulatory frameworks such as the European Union’s Energy Performance of Buildings Directive and the U.S. Department of Energy’s building codes have mandated increased energy efficiency standards that directly impact smart windows materials adoption. These regulations enforce minimum thermal performance and solar heat gain coefficients for glazing products, incentivizing the use of dynamic smart window technologies. Additionally, certifications like LEED and WELL integrate smart window performance criteria, influencing architectural specifications globally. In Asia-Pacific, government policies promoting green buildings and sustainable urban development encourage manufacturers to comply with rigorous environmental standards. Safety regulations addressing fire resistance, chemical emissions, and impact resistance also guide product development and testing procedures. Compliance with these evolving regulatory landscapes ensures market access and fosters innovation aligned with sustainability goals. Industry players actively engage with regulatory bodies to shape standards supporting technology advancement while meeting environmental and occupant health objectives.

Market Intelligence

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

- •Source: Market research industry publications

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 3.5 Billion |

| Forecast Year Market Size | USD 12.8 Billion |

| CAGR | 15.5% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 15.4% |

| Scope of Report | Market is segmented by Type (Electrochromic, Thermochromic, Photochromic, Suspended Particle Devices, Liquid Crystal Devices), Application (Residential Buildings, Commercial Buildings, Automotive, Aerospace, Healthcare), End-Use Industry (Construction, Automotive, Transportation, Healthcare), Distribution Channel (Direct Sales, Distributors, Online Platforms) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Saint-Gobain (France), AGC Inc. (Japan), View, Inc. (United States), Gentex Corporation (United States), SageGlass (France), Halio Inc. (United States), Research Frontiers Inc. (United States), Guardian Glass (United States), Kinestral Technologies (United States), Polytronix, Inc. (United States), Chromogenics ASA (Norway), Smartglass International (United Kingdom), Gentex Corporation (United States), Pleotint, LLC (United States), View Inc. (United States), Eastman Chemical Company (United States), YKK AP Inc. (Japan), AGP Lighting Solutions (South Korea), Smartglass Australia Pty Ltd (Australia), KDX Group (Japan) |

Global Smart Windows Materials Market Size, Growth & Revenue 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.