Global Online K-12 Education Market Size, Growth & Revenue 2024-2034

Global Online K-12 Education Market is segmented by Type (Synchronous Learning, Asynchronous Learning, Hybrid Learning, AI-enabled Learning, Gamified Learning), Application (Virtual Classroom, Self-paced Learning, Blended Learning, Tutoring Services, Assessment & Evaluation), End-User (Students, Teachers, Educational Institutions, Parents), Distribution Channel (Direct Sales, Online Platforms, Partnerships & Collaborations), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The Global Online K-12 Education Market represents a rapidly evolving sector focused on delivering educational content and interactive learning experiences digitally to primary and secondary students worldwide. This market integrates various learning methodologies including synchronous, asynchronous, hybrid, AI-enabled, and gamified learning, facilitating real-time interaction, flexible pacing, and enhanced engagement. It covers applications like virtual classrooms, self-paced courses, blended instruction, tutoring services, and comprehensive assessment tools designed to improve learning outcomes and accessibility. The market scope extends to advanced digital platforms, content providers, and supporting technologies such as cloud computing, AI, and data analytics, which enable personalized and scalable education solutions beyond traditional classrooms. The growth is driven by increasing internet penetration, technological advancements, demand for flexible and remote learning options, and government initiatives supporting digital education infrastructure. Key stakeholders include educational institutions, edtech companies, governments, and learners seeking innovative and effective K-12 educational experiences globally. This market is characterized by continuous innovation, strategic partnerships, and expanding adoption across diverse geographies and demographics, redefining how foundational education is delivered and consumed worldwide.

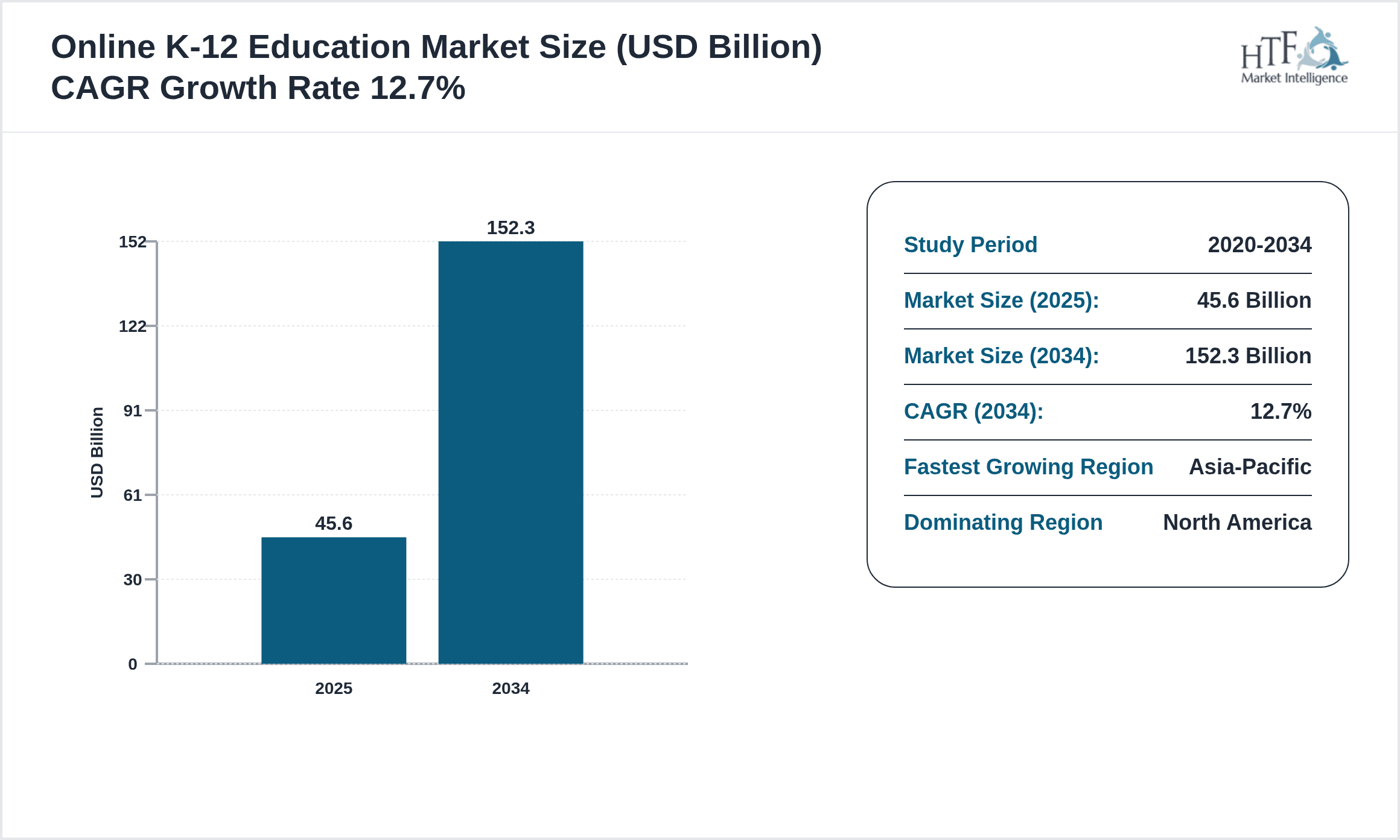

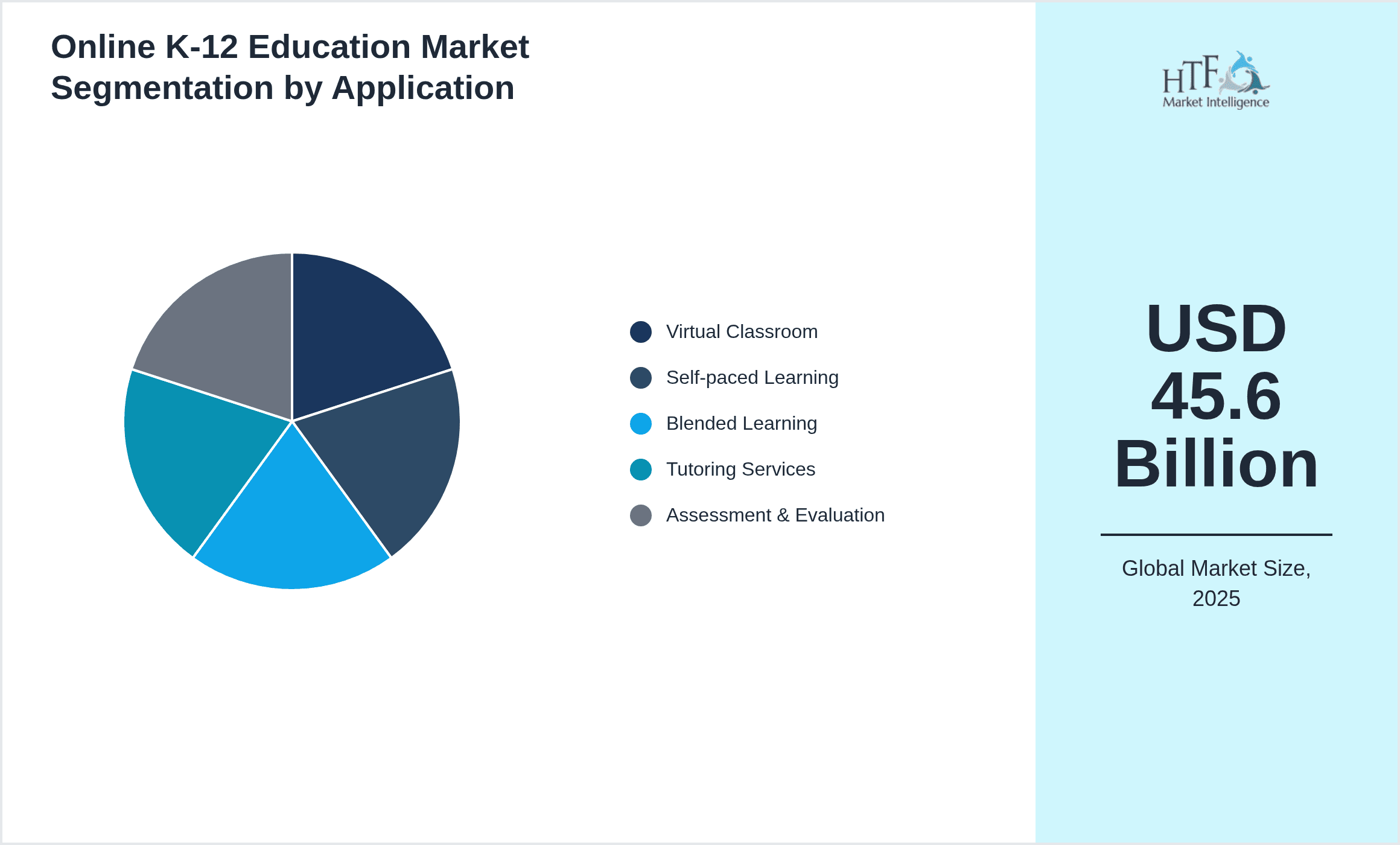

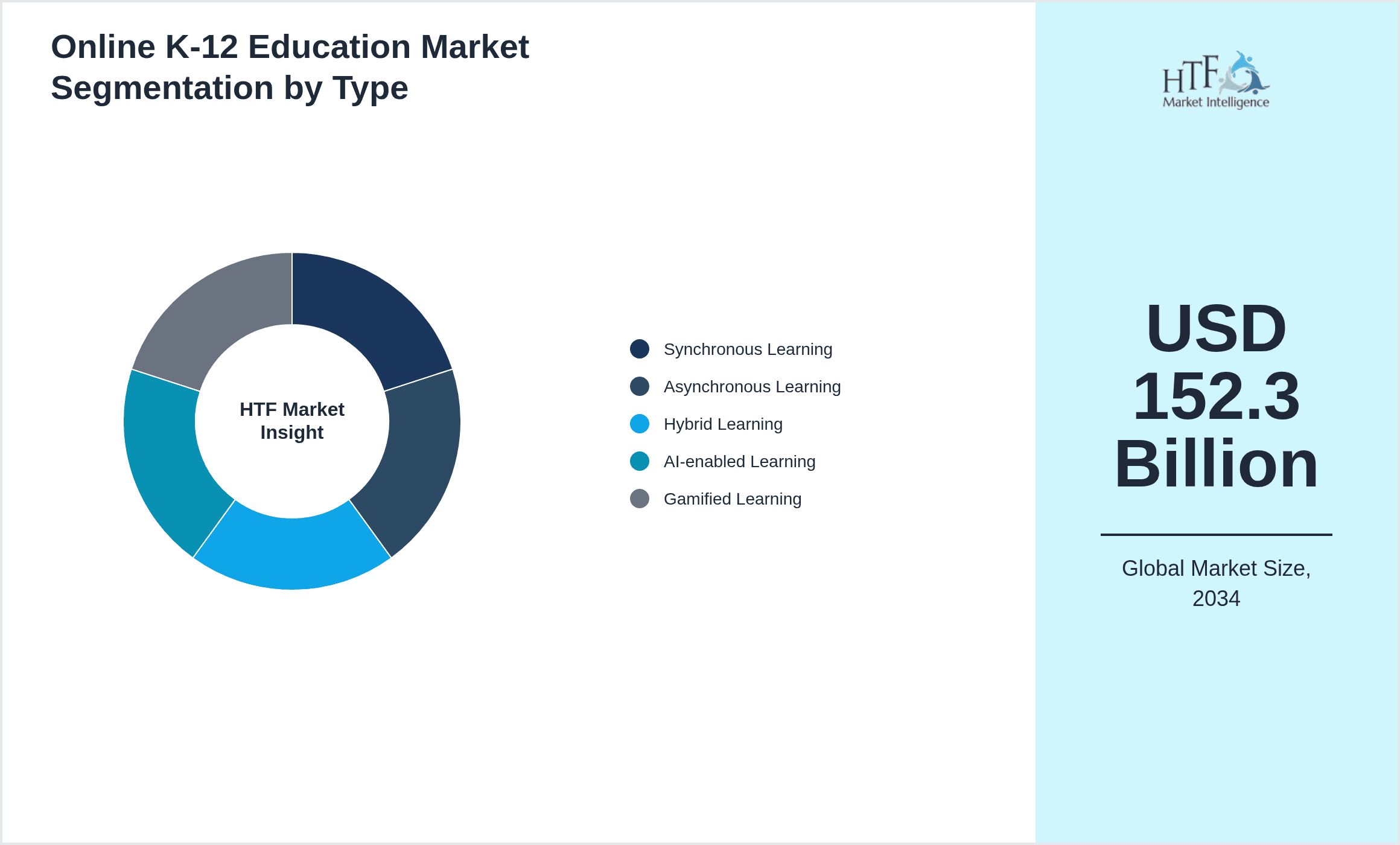

- •Key market highlights include a projected CAGR of 12.7% from 2024 to 2034, with the market size expected to grow from USD 45.6 Billion in 2024 to USD 152.3 Billion by 2034. North America currently dominates the market, owing to advanced infrastructure and high adoption of digital learning tools, while Asia-Pacific is the fastest growing region driven by expanding internet access and government digital education initiatives. Synchronous learning remains the leading product type due to its real-time interaction benefits, whereas AI-enabled learning is the fastest growing segment propelled by advancements in adaptive learning technologies. Virtual classrooms and self-paced learning are the dominant applications, reflecting diverse learning preferences and operational flexibility. These trends underscore the increasing integration of technology in K-12 education, fostering personalized, accessible, and engaging learning experiences across regions.

- •The online K-12 education market offers significant value propositions to educational institutions, learners, policymakers, and technology providers by enabling scalable, cost-effective, and flexible learning solutions. It supports continuity of education during disruptions such as pandemics, expands access to quality resources irrespective of geography, and fosters skill development aligned with digital age demands. For stakeholders, this market presents strategic opportunities to innovate through AI, gamification, and immersive learning technologies, collaborate via partnerships, and address evolving educational needs globally. The market’s growth also stimulates investment in infrastructure, content localization, and teacher training, thereby enhancing overall educational ecosystems. Consequently, the online K-12 education market is pivotal in shaping future-ready learners and transforming traditional education paradigms worldwide.

Competitive Landscape

The competitive environment in the global Online K-12 Education Market is characterized by intense rivalry among established edtech giants, emerging innovative startups, and regional players striving to capture market share through differentiated offerings and technological advancements. Companies compete primarily on product innovation, platform scalability, content quality, and user experience, leveraging AI, gamification, and analytics to enhance engagement and learning outcomes. Strategic partnerships and collaborations with educational institutions and governments are common to expand reach and credibility. Mergers and acquisitions play a significant role in consolidating market presence and accessing new technologies, while pricing strategies and subscription models are adapted to diverse regional affordability levels. Moreover, the market witnesses continuous entry barriers due to technological expertise requirements and regulatory compliance. Overall, competitive dynamics emphasize innovation-led growth, customer-centric solutions, and global as well as localized approaches to meet diverse educational demands effectively.

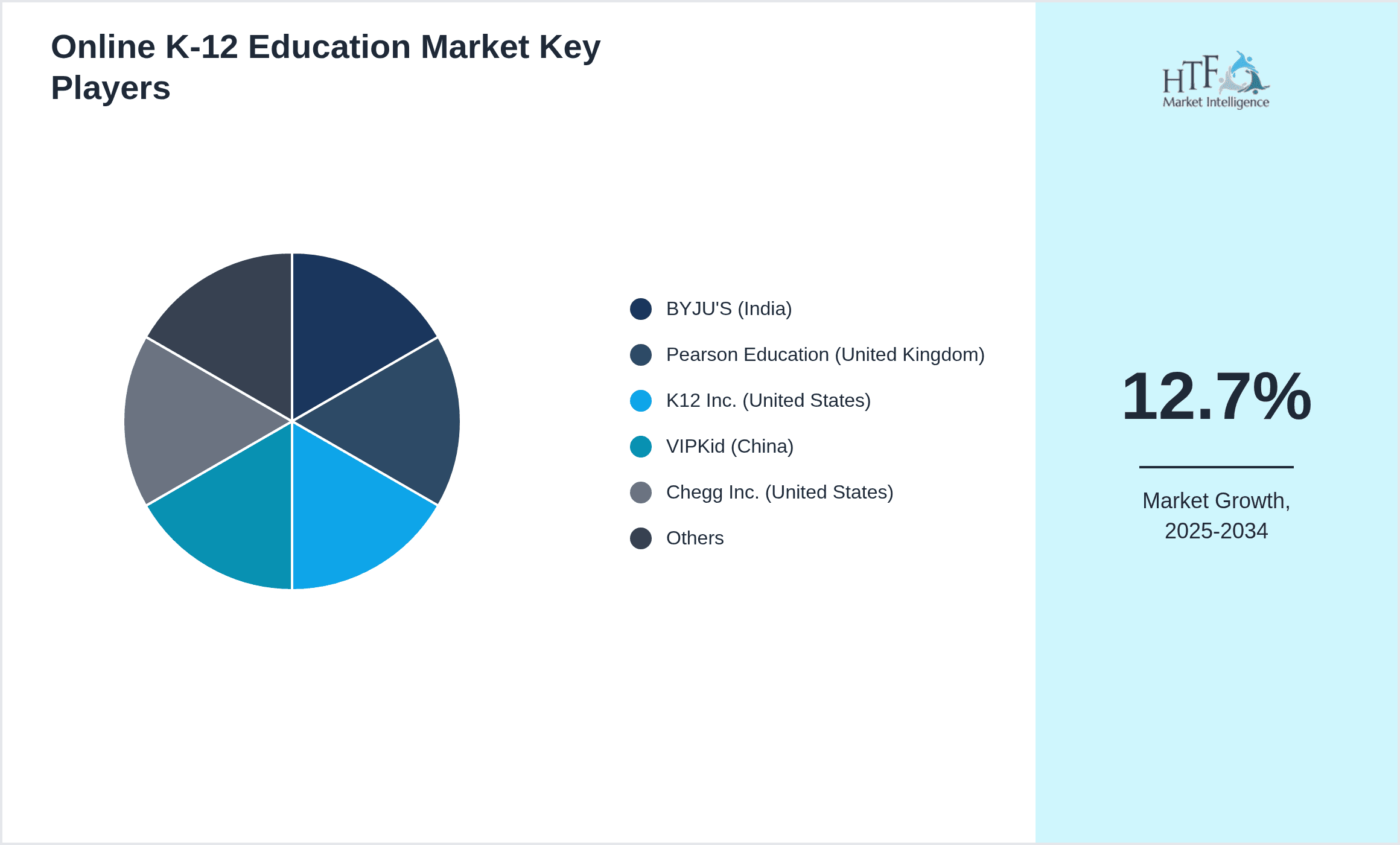

Leading Companies in Online K-12 Education Market

- •BYJU'S (India)

- •Pearson Education (United Kingdom)

- •K12 Inc. (United States)

- •VIPKid (China)

- •Chegg Inc. (United States)

- •Duolingo Inc. (United States)

- •Outschool Inc. (United States)

- •Age of Learning, Inc. (United States)

- •Brainly, Inc. (Poland)

- •TAL Education Group (China)

- •Edmodo (United States)

- •Rosetta Stone (United States)

- •Cambly Inc. (United States)

- •Zearn (United States)

- •Unacademy (India)

- •Knewton (United States)

- •Udemy (United States)

- •ClassDojo (United States)

- •Quizlet Inc. (United States)

- •VIPKid (China)

- •Top Hat (Canada)

- •Blackboard Inc. (United States)

- •Seesaw Learning, Inc. (United States)

- •Schoology (United States)

- •DreamBox Learning (United States)

Market Breakdown

- •By Type

- ◦Synchronous Learning

- ◦Asynchronous Learning

- ◦Hybrid Learning

- ◦AI-enabled Learning

- ◦Gamified Learning

- •By Application

- ◦Virtual Classroom

- ◦Self-paced Learning

- ◦Blended Learning

- ◦Tutoring Services

- ◦Assessment & Evaluation

- •By End-User

- ◦Students

- ◦Teachers

- ◦Educational Institutions

- ◦Parents

- •By Distribution Channel

- ◦Direct Sales

- ◦Online Platforms

- ◦Partnerships & Collaborations

Growth Dynamics

- •Rising internet penetration and smartphone adoption worldwide have significantly increased access to online K-12 education, enabling students in remote and underserved areas to receive quality learning experiences. This technological proliferation facilitates widespread adoption and market expansion.

- •Government initiatives promoting digital literacy and education reform, along with increased funding for edtech infrastructure, are critical growth drivers enhancing the availability and quality of online K-12 education across various regions.

- •The COVID-19 pandemic accelerated the adoption of online K-12 education, demonstrating the need for flexible and remote learning models, which remain in demand due to their convenience and ability to personalize education.

- •Advancements in AI and machine learning enable adaptive learning platforms that cater to individual student needs and learning paces, improving engagement and educational outcomes, thus driving market growth.

- •Increasing awareness among parents and educators regarding the benefits of technology-enabled learning and the rising demand for supplementary tutoring services online are propelling market expansion globally.

- •Strategic collaborations between edtech providers and traditional educational institutions facilitate blended learning models, further popularizing online K-12 education and expanding market reach.

- •Growing investments by venture capitalists and technology companies in edtech startups foster innovation and scalability, strengthening market growth prospects significantly.

Market Trends

- •Integration of gamification elements in online K-12 education platforms is enhancing student engagement and motivation by making learning interactive and enjoyable, leading to improved retention rates.

- •The rise of AI-powered personalized learning tools is transforming the traditional one-size-fits-all approach, enabling customized content delivery based on individual student performance and preferences.

- •Hybrid learning models combining online and face-to-face instruction are gaining traction, offering flexibility while preserving social interaction and hands-on learning experiences.

- •Increased adoption of cloud-based platforms facilitates scalable, accessible, and cost-efficient deployment of online K-12 education solutions across diverse geographical locations.

- •Collaborations among edtech companies, content creators, and educational institutions are fostering the development of comprehensive and localized curriculum-aligned digital content.

- •Mobile-first learning approaches address the growing usage of smartphones among students, ensuring accessibility and promoting continuous learning beyond traditional settings.

- •Data analytics and learning management systems (LMS) are increasingly used to monitor student progress, tailor instruction, and provide actionable insights to educators and parents.

Market Opportunities

- •Expanding internet infrastructure in emerging economies presents vast untapped markets for online K-12 education providers aiming to reach millions of new learners.

- •Development of AI-driven assessment and feedback tools offers opportunities to enhance educational quality and personalize student support services effectively.

- •Strategic partnerships with governments and NGOs to support inclusive education initiatives can open new distribution channels and funding opportunities.

- •Growth in demand for STEM and coding education creates opportunities for specialized online K-12 programs focused on future-ready skills development.

- •Integration of virtual reality (VR) and augmented reality (AR) technologies can revolutionize experiential learning, offering immersive and interactive educational experiences.

- •Rising parental preference for flexible, supplementary tutoring services can be leveraged to develop tailored online tutoring platforms addressing diverse learner needs.

- •Localization of content to cater to regional languages and curricula can significantly increase adoption rates and market penetration in diverse geographies.

Market Challenges

- •Digital divide and unequal access to reliable internet and devices limit the reach of online K-12 education, particularly in rural and low-income regions, hindering market growth.

- •Concerns regarding data privacy and cybersecurity pose significant challenges, requiring stringent compliance and security measures by education providers.

- •Resistance to change from traditional educational institutions and educators may slow down the adoption of online learning technologies and methodologies.

- •Quality assurance and standardization of online content and teaching methods remain complex, impacting learner outcomes and trust in digital education platforms.

- •High initial investment costs for technology infrastructure and content development can be a barrier for smaller players and limit market entry.

- •Language barriers and lack of localized content restrict accessibility and effectiveness in diverse global markets.

- •Ensuring student engagement and motivation in a fully online environment is challenging due to limited social interaction and potential distractions.

Regulatory Framework

- •Between 2019 and 2024, multiple countries enacted regulations mandating minimum standards for online educational content, ensuring curriculum alignment and quality assurance to protect learners' interests.

- •Data protection laws such as GDPR in Europe and CCPA in North America have been enforced, requiring online K-12 education providers to implement rigorous data privacy and security protocols.

- •Several regions introduced accreditation frameworks for online education platforms to certify legitimacy and foster trust among users and educational institutions.

- •Government mandates supporting digital education infrastructure investments have increased, providing funding and incentives for edtech development and adoption in schools globally.

- •Policies promoting equal access to digital education aim to bridge the digital divide by subsidizing devices and internet connectivity for underprivileged students.

Market Intelligence

- •15th January 2025, BYJU'S launched an AI-powered adaptive learning platform targeting K-12 students globally, designed to personalize learning paths based on real-time performance data. The platform integrates gamification features and offers multilingual support to cater to diverse learner needs. This innovation aims to enhance student engagement and improve educational outcomes, positioning BYJU'S at the forefront of edtech innovation. Source: BYJU'S Official Press Release

- •8th March 2025, Pearson Education introduced a comprehensive virtual classroom solution incorporating VR technology to deliver immersive science and history lessons for K-12 students. The product focuses on experiential learning by simulating real-world environments, thereby increasing retention and interest. Pearson's strategic move is expected to strengthen its market position in North America and Europe by addressing demand for innovative digital education tools. Source: Pearson Education Corporate Announcement

- •22nd May 2024, K12 Inc. announced a global partnership with Google for Education to integrate cloud-based collaboration tools into its online learning platform. This initiative improves accessibility, real-time interaction, and resource sharing among students and educators, enhancing the overall learning experience. The collaboration is poised to accelerate digital transformation in K-12 education worldwide. Source: Google for Education Newsroom

- •30th September 2024, Duolingo Inc. expanded its K-12 language learning offerings by launching a gamified mobile app tailored for young learners. The app leverages AI to customize lessons and tracks progress through engaging exercises, aiming to increase language proficiency and motivation. This product launch supports Duolingo's strategy to penetrate the global K-12 education market further. Source: Duolingo Corporate Blog

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 45.6 Billion |

| Forecast Year Market Size | USD 152.3 Billion |

| CAGR | 12.7% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 12% |

| Scope of Report | Market is segmented by Type (Synchronous Learning, Asynchronous Learning, Hybrid Learning, AI-enabled Learning, Gamified Learning), Application (Virtual Classroom, Self-paced Learning, Blended Learning, Tutoring Services, Assessment & Evaluation), End-User (Students, Teachers, Educational Institutions, Parents), Distribution Channel (Direct Sales, Online Platforms, Partnerships & Collaborations) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | BYJU'S (India), Pearson Education (United Kingdom), K12 Inc. (United States), VIPKid (China), Chegg Inc. (United States) |

Global Online K-12 Education Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.