Global Capnography Equipment Market Size, Growth & Revenue 2024-2034

Global Capnography Equipment Market is segmented by Type (Mainstream Capnography, Sidestream Capnography, Microstream Capnography, Portable Capnography, Wireless Capnography), Application (Operating Rooms, Intensive Care Units, Emergency Care, Ambulatory Surgical Centers, Home Care), End-Use Industry (Hospitals, Ambulatory Care Centers, Home Healthcare Providers, Research & Academic Institutes), Distribution Channel (Direct Sales, Distributors and Dealers, Online Sales), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global Capnography Equipment market is dedicated to devices that measure carbon dioxide levels in exhaled air, critical for monitoring patient ventilation in medical environments. This market covers a diverse range of equipment including mainstream, sidestream, microstream, portable, and wireless devices tailored for applications such as operating rooms, intensive care units, emergency care, ambulatory surgical centers, and home healthcare. These devices enhance clinical decision-making by providing real-time respiratory data, reducing risks during anesthesia, and improving patient outcomes. The market scope extends to technological innovations incorporating wireless connectivity and integration with hospital information systems to facilitate seamless monitoring. With increasing awareness of patient safety, rising surgical procedures, and expanding critical care infrastructure worldwide, the demand for capnography equipment is growing robustly. The market's boundaries include hardware devices, software interfaces, and services supporting device operation and maintenance across healthcare settings globally.

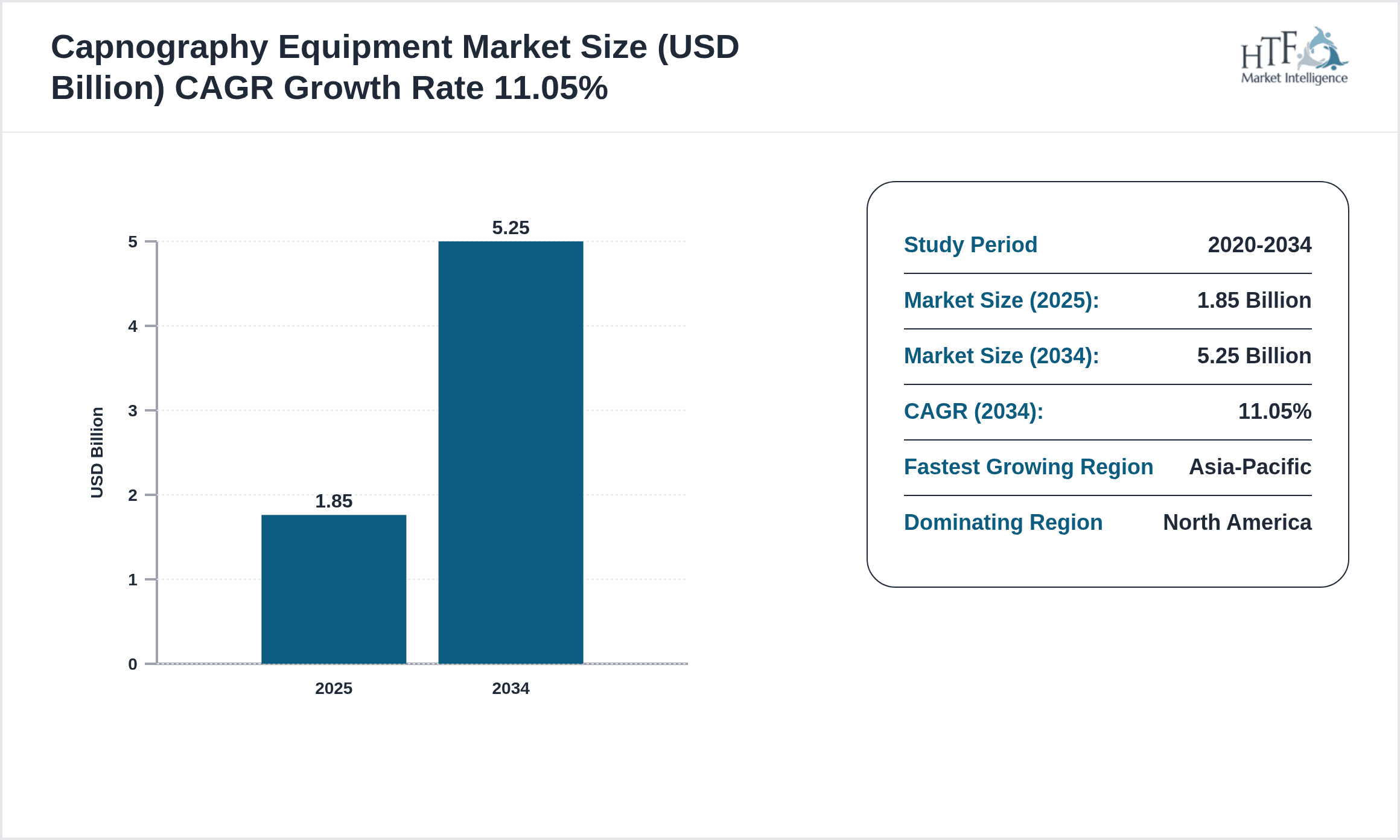

- •Key market highlights reveal a robust compound annual growth rate (CAGR) of 11.05% projected through 2034, driven by technological advancements and growing adoption in emerging economies. In 2024, the market valuation stands at USD 1.85 Billion and is forecasted to reach USD 5.25 Billion by 2034, reflecting increasing clinical reliance on respiratory monitoring. Sidestream capnography dominates product types due to its versatility and accuracy, while wireless capnography is identified as the fastest-growing segment, propelled by demand for portability and remote monitoring. North America leads the regional market share with 35%, supported by advanced healthcare infrastructure and regulatory frameworks, whereas Asia-Pacific emerges as the fastest-growing region, fueled by expanding healthcare access and investments. Market penetration in Latin America and Middle East & Africa is gradually rising, shaped by growing medical facilities and awareness.

- •The market presents strategic importance across healthcare stakeholders including hospitals, surgical centers, emergency services, and homecare providers. The value proposition lies in enhanced patient safety through continuous respiratory monitoring, early detection of ventilation issues, and improved anesthetic management. Industry players benefit from innovation-driven differentiation and regulatory compliance that facilitate market entry and expansion. Increasing surgical volumes, aging populations, and rising incidence of respiratory diseases globally underline the critical need for reliable capnography equipment. Additionally, integration with digital health systems offers opportunities for data-driven care and operational efficiency. Thus, this market is positioned as a vital component in modern healthcare delivery, fostering improved clinical outcomes and reduced healthcare costs worldwide.

Competitive Landscape

The global capnography equipment market is characterized by intense competition among established multinational corporations and emerging regional players. Market leaders leverage innovation, extensive product portfolios, and strategic partnerships to maintain dominance. Competition is driven by continuous technological advancements such as wireless monitoring, miniaturized sensors, and integration with digital health platforms. Companies adopt differentiation strategies focusing on device accuracy, user interface, and patient comfort to capture market share. Price competition remains moderate due to the critical nature of the devices and regulatory standards ensuring quality. Strategic alliances, mergers, and acquisitions are common to expand geographic reach and product offerings. Additionally, companies invest in R&D to address challenges like sensor calibration and data interoperability. Regional competition is particularly dynamic in Asia-Pacific, where local manufacturers are emerging. Overall, the competitive landscape is shaped by innovation, regulatory compliance, and evolving healthcare demands, with future trends expected to focus on connectivity and AI-driven analytics integration.

Leading Companies in Capnography Equipment Market

- •Medtronic plc (Ireland)

- •Philips Healthcare (Netherlands)

- •Drägerwerk AG & Co. KGaA (Germany)

- •GE Healthcare (United States)

- •Masimo Corporation (United States)

- •Smiths Medical (United Kingdom)

- •Nihon Kohden Corporation (Japan)

- •Spacelabs Healthcare (United States)

- •Nonin Medical, Inc. (United States)

- •ConvaTec Group plc (United Kingdom)

- •Fisher & Paykel Healthcare Corporation Limited (New Zealand)

- •CareFusion Corporation (United States)

- •Cardinal Health, Inc. (United States)

- •Becton, Dickinson and Company (United States)

- •Teleflex Incorporated (United States)

- •Invacare Corporation (United States)

- •Hill-Rom Holdings, Inc. (United States)

- •Smith & Nephew plc (United Kingdom)

- •Vyaire Medical, Inc. (United States)

- •Welch Allyn, Inc. (United States)

- •Natus Medical Incorporated (United States)

- •Teleflex Medical (United States)

- •Analogic Corporation (United States)

- •Zoll Medical Corporation (United States)

- •B. Braun Melsungen AG (Germany)

Market Breakdown

- •By Type

- ◦Mainstream Capnography

- ◦Sidestream Capnography

- ◦Microstream Capnography

- ◦Portable Capnography

- ◦Wireless Capnography

- •By Application

- ◦Operating Rooms

- ◦Intensive Care Units

- ◦Emergency Care

- ◦Ambulatory Surgical Centers

- ◦Home Care

- •By End-Use Industry

- ◦Hospitals

- ◦Ambulatory Care Centers

- ◦Home Healthcare Providers

- ◦Research & Academic Institutes

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors and Dealers

- ◦Online Sales

Growth Dynamics

The global capnography equipment market is propelled by an increasing volume of surgical procedures worldwide, driven by aging populations and rising prevalence of chronic respiratory diseases. Technological advancements such as wireless capnography devices and integration with hospital information systems enhance monitoring capabilities, fostering adoption. Growing awareness among healthcare professionals about the critical role of respiratory monitoring in anesthesia and critical care further stimulates demand. Additionally, expanding healthcare infrastructure in emerging economies supports market penetration. Rising government initiatives promoting patient safety and stringent monitoring standards in perioperative care also act as significant growth drivers. The availability of portable and user-friendly capnography devices broadens usage beyond traditional hospital settings to ambulatory and home care, opening new application avenues. Overall, these factors collectively contribute to robust market expansion over the forecast period.

Market Trends

Current market trends include the miniaturization of capnography devices enabling portability and ease of use in diverse clinical settings. The integration of wireless technology facilitates remote patient monitoring and real-time data transmission to healthcare providers. Artificial intelligence and data analytics are increasingly incorporated for predictive respiratory assessments and enhanced diagnostic accuracy. Companies are focusing on developing multi-parameter monitors combining capnography with pulse oximetry and other vital signs monitoring to offer comprehensive respiratory assessments. Additionally, growing interest in non-invasive ventilation support and home healthcare is driving innovations targeting user-friendly interfaces and extended battery life. Sustainability trends encourage manufacturers to develop eco-friendly and reusable sensor technologies, aligning with global environmental goals. These trends collectively shape the evolution of the capnography equipment market, enhancing its clinical utility and market penetration.

Market Opportunities

Emerging opportunities arise from expanding healthcare access in developing regions where growing investments in critical care infrastructure create demand for advanced respiratory monitoring devices. The rising prevalence of respiratory illnesses such as COPD and COVID-19 sequelae underscores the need for continuous ventilation monitoring, particularly in home care settings. Technological innovations, including integration with telemedicine platforms, present significant growth potential by enabling remote monitoring and reducing hospital stays. Strategic partnerships between device manufacturers and healthcare providers can accelerate product adoption and customization for specific clinical environments. Additionally, the evolution of wearable and wireless capnography devices offers opportunities for market diversification and new application segments. Regulatory incentives promoting patient safety and quality standards also encourage market growth by facilitating device approvals and hospital procurement. Capitalizing on these trends can enhance market share and foster innovation-driven expansion.

Market Challenges

The capnography equipment market faces challenges such as high device costs, which limit adoption in cost-sensitive and developing markets. Technical limitations including sensor calibration requirements and susceptibility to interference can affect measurement accuracy, impacting clinical trust and usage. Regulatory compliance complexity and varying standards across regions pose hurdles for manufacturers seeking global market entry. Additionally, lack of trained personnel to operate sophisticated devices restricts effective utilization in some healthcare settings. Market fragmentation with numerous small players creates competitive pressure and pricing challenges. Supply chain disruptions and component shortages may delay product availability, affecting sales. Furthermore, reimbursement policies in certain regions do not adequately cover capnography equipment, limiting hospital procurement. Addressing these challenges requires strategic investments in cost reduction, training, and regulatory harmonization to sustain growth.

Regulatory Framework

Between 2020 and 2024, global regulatory bodies have emphasized stringent standards for capnography equipment to ensure patient safety and device reliability. The U.S. FDA updated guidance on respiratory monitoring devices focusing on performance testing and post-market surveillance, requiring manufacturers to demonstrate device accuracy and robustness. The European Union implemented the Medical Device Regulation (MDR) in 2021, imposing rigorous compliance requirements including clinical evaluation and traceability, impacting market entry and ongoing certification. Regulatory authorities in Asia-Pacific countries have also enhanced approval processes to align with international standards, facilitating safer device deployment. Additionally, cybersecurity guidelines for connected medical devices have been introduced globally, mandating protection against data breaches. Governments continue to promote harmonization of standards and incentivize innovation through fast-track approvals for advanced technologies. These regulatory frameworks shape market dynamics by balancing innovation with safety and efficacy.

Market Intelligence

- •15th January 2024, Medtronic plc launched its latest wireless capnography monitor aimed at ambulatory surgical centers and home care settings. The device features continuous real-time CO2 monitoring with Bluetooth connectivity, allowing seamless integration with mobile health applications. It is designed for ease of use with a compact form factor and long battery life, addressing the need for portability in non-traditional care environments. Medtronic’s strategic objective includes expanding remote patient monitoring capabilities and enhancing data analytics to improve respiratory care outcomes. This launch strengthens its position in the rapidly growing wireless capnography segment and aligns with global trends towards digital health.

- •22nd September 2023, Philips Healthcare introduced an advanced sidestream capnography system incorporating AI-driven algorithms for predictive respiratory failure detection in intensive care units. The innovation enables early warning alerts to clinicians based on continuous CO2 waveform analysis, enhancing patient safety during critical care. Philips positioned this product as part of its broader strategy to integrate AI into clinical monitoring solutions, aiming to reduce adverse events and improve workflow efficiency. The system supports interoperability with hospital electronic health records, facilitating comprehensive patient data management and decision support.

- •30th March 2024, Drägerwerk AG & Co. KGaA announced a strategic partnership with a leading telehealth provider to develop integrated capnography solutions for remote respiratory monitoring. The collaboration focuses on combining Dräger’s sensor technology with telehealth platforms to enable continuous monitoring of patients with chronic respiratory conditions outside hospital settings. This initiative addresses the growing demand for home healthcare solutions and aims to reduce hospital readmissions. The partnership emphasizes innovation in connectivity and data security to meet regulatory standards and improve patient engagement.

- •18th November 2023, GE Healthcare completed the acquisition of a specialized capnography sensor technology startup to enhance its product portfolio with next-generation microstream capnography devices. The acquisition aims to accelerate GE’s development of compact, low-power sensors for use in portable and wireless monitors. This move strengthens GE’s competitive positioning in the fast-growing segments of capnography equipment and aligns with ongoing trends toward miniaturization and enhanced sensor accuracy. The integration of the startup’s technology is expected to improve product differentiation and support GE’s global expansion strategy.

- •Source: Official company press releases, industry publications, and regulatory announcements

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 1.85 Billion |

| Forecast Year Market Size | USD 5.25 Billion |

| CAGR | 11.05% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 11% |

| Scope of Report | Market is segmented by Type (Mainstream Capnography, Sidestream Capnography, Microstream Capnography, Portable Capnography, Wireless Capnography), Application (Operating Rooms, Intensive Care Units, Emergency Care, Ambulatory Surgical Centers, Home Care), End-Use Industry (Hospitals, Ambulatory Care Centers, Home Healthcare Providers, Research & Academic Institutes), Distribution Channel (Direct Sales, Distributors and Dealers, Online Sales) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Medtronic plc (Ireland), Philips Healthcare (Netherlands), Drägerwerk AG & Co. KGaA (Germany), GE Healthcare (United States), Masimo Corporation (United States), Smiths Medical (United Kingdom), Nihon Kohden Corporation (Japan), Spacelabs Healthcare (United States), Nonin Medical, Inc. (United States), ConvaTec Group plc (United Kingdom), Fisher & Paykel Healthcare Corporation Limited (New Zealand), CareFusion Corporation (United States), Cardinal Health, Inc. (United States), Becton, Dickinson and Company (United States), Teleflex Incorporated (United States), Invacare Corporation (United States), Hill-Rom Holdings, Inc. (United States), Smith & Nephew plc (United Kingdom), Vyaire Medical, Inc. (United States), Welch Allyn, Inc. (United States), Natus Medical Incorporated (United States), Teleflex Medical (United States), Analogic Corporation (United States), Zoll Medical Corporation (United States), B. Braun Melsungen AG (Germany) |

Global Capnography Equipment Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.