Global Thermal Bonding Film Market Size, Growth & Revenue 2025-2034

Global Thermal Bonding Film Market is segmented by Product Type (Hot-Melt Adhesive Film, Reactive Adhesive Film, Pressure Sensitive Film, Heat-Activated Film, UV-Curable Film), Application (Electronics Assembly, Automotive Components, Medical Devices, Packaging, Textile), End-Use Industry (Electronics, Automotive, Healthcare, Packaging), Distribution Channel (Direct Sales, Distributors, Converters), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global thermal bonding film market encompasses adhesive films that facilitate bonding of diverse substrates through heat and pressure application. This market spans multiple adhesive types such as hot-melt, reactive, pressure-sensitive, heat-activated, and UV-curable films, each tailored to meet specific industrial requirements. Key applications include electronics assembly, automotive component manufacturing, medical device fabrication, packaging, and textile lamination, highlighting the versatility of these films. The value chain involves raw material procurement, adhesive formulation, film manufacturing, and integration by end-use industries. Market growth is driven by rising demand for lightweight, durable bonding solutions to enhance product performance and manufacturing efficiency. Technological innovations focus on developing eco-friendly adhesives with faster curing times and enhanced bond strength, addressing sustainability and operational challenges. Regional demand varies with North America dominating due to advanced manufacturing sectors, while Asia-Pacific exhibits the highest growth propelled by expanding industrialization and automotive production. This research report provides an in-depth analysis of market size, segmentation, competitive dynamics, and future prospects through 2034, supporting stakeholders in strategic planning and investment decisions.

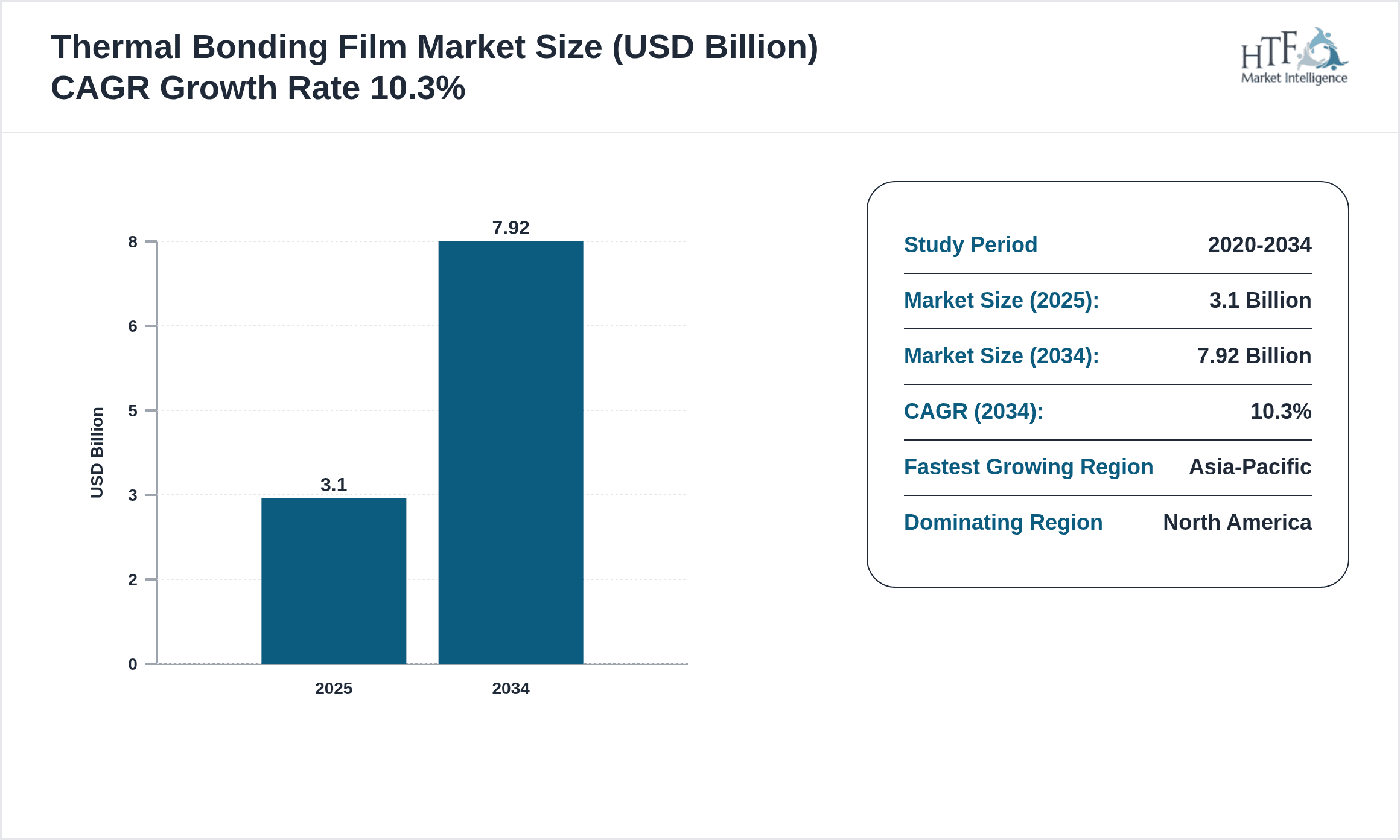

- •The thermal bonding film market recorded a base size of USD 3.1 billion in 2025, growing at a CAGR of 10.3% to reach USD 7.92 billion by 2034. The market growth is characterized by strong year-on-year expansion averaging 9.9%, underpinned by increasing adoption in electronics and automotive sectors. Key highlights include the dominance of hot-melt adhesive films representing the largest product segment and the rapid rise of UV-curable films driven by advanced manufacturing demands. Regionally, North America holds the largest market share due to well-established industrial infrastructure, whereas Asia-Pacific is the fastest growing region fueled by burgeoning automotive and electronics markets. These trends underscore the strategic relevance of thermal bonding films as enabling materials for modern manufacturing, with significant growth potential across emerging economies and innovative product developments.

- •Thermal bonding films offer critical value propositions by enhancing product durability, reducing manufacturing cycle times, and enabling environmentally sustainable adhesive solutions. Their strategic importance spans multiple industries including electronics, automotive, healthcare, packaging, and textiles, where reliable bonding technologies are essential for product integrity and performance. For manufacturers and suppliers, thermal bonding films provide opportunities to differentiate through innovation in adhesive chemistries and process efficiencies. For end-users, these films facilitate lightweight construction, cost-effective assembly, and compliance with stringent regulatory standards. This comprehensive market report serves as a vital resource for investors, industry players, and technology developers seeking actionable insights into market dynamics, competitive landscape, and future growth avenues globally.

Competitive Landscape

The competitive environment of the global thermal bonding film market is characterized by a diverse array of players ranging from multinational chemical conglomerates to specialized adhesive formulators. Market dynamics are driven by continuous innovation in adhesive technology, strategic partnerships, and mergers and acquisitions aimed at expanding product portfolios and geographic reach. Companies emphasize differentiation through the development of eco-friendly and high-performance films that meet evolving industry standards and customer demands. Pricing strategies balance raw material cost fluctuations and the value proposition of advanced adhesive properties. Distribution channels include direct sales to industrial manufacturers and partnerships with converters and distributors, optimizing market penetration. Barriers to entry remain moderate, influenced by technological expertise requirements and regulatory compliance. Regional competition is intense, with North American and European players leading in innovation, while Asia-Pacific companies aggressively pursue market share through capacity expansion and cost competitiveness. Future trends will likely focus on digitalization of manufacturing processes and integration of smart adhesive systems to enhance functionality and efficiency.

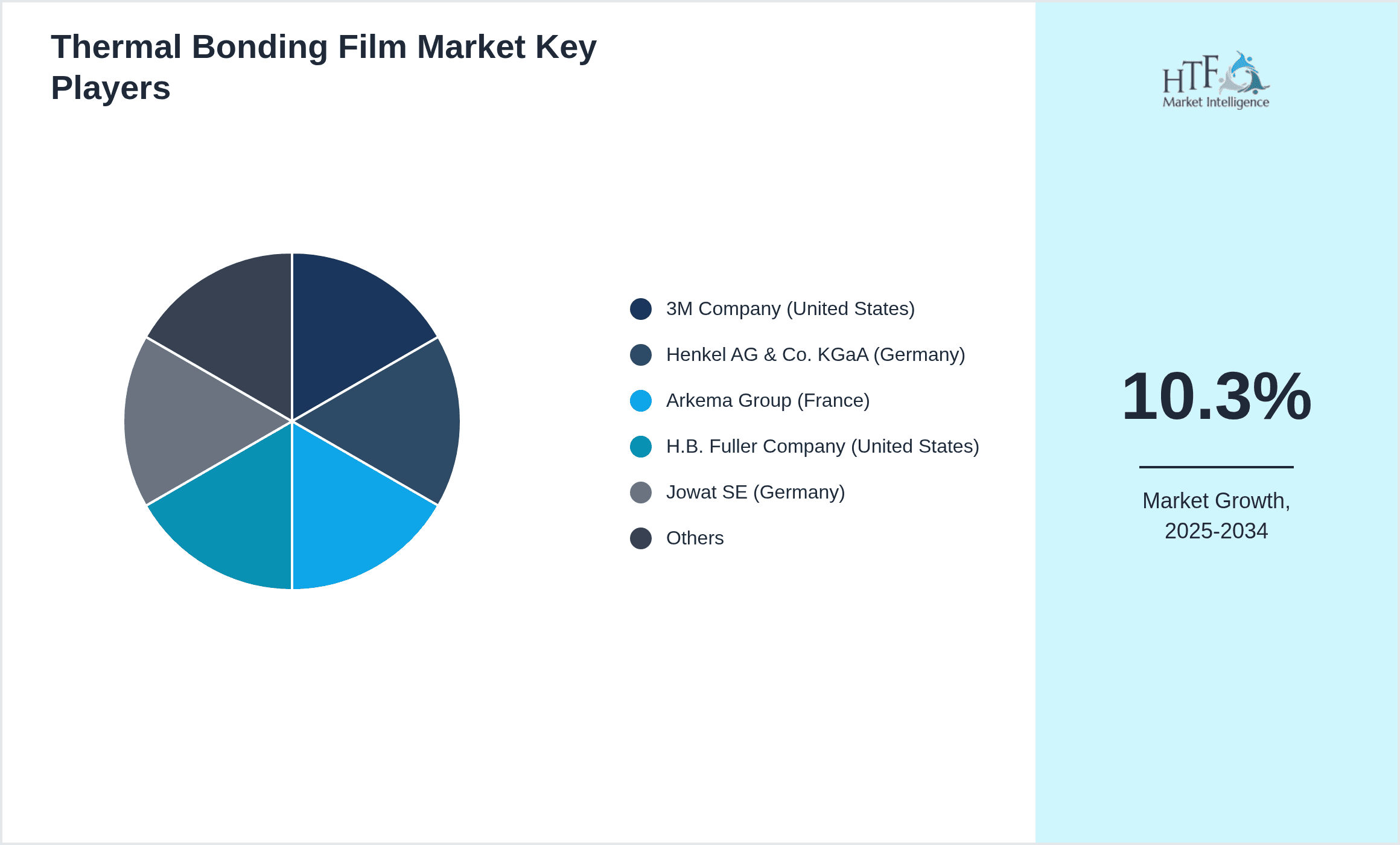

Leading Companies in Thermal Bonding Film Market

- •3M Company (United States)

- •Henkel AG & Co. KGaA (Germany)

- •Arkema Group (France)

- •H.B. Fuller Company (United States)

- •Jowat SE (Germany)

- •H.B. Fuller Company (United States)

- •Bostik SA (France)

- •Sika AG (Switzerland)

- •Tesa SE (Germany)

- •Dow Inc. (United States)

- •Eastman Chemical Company (United States)

- •Covestro AG (Germany)

- •Kuraray Co., Ltd. (Japan)

- •Henkel Adhesive Technologies (Germany)

- •Honeywell International Inc. (United States)

- •Shin-Etsu Chemical Co., Ltd. (Japan)

- •Huntsman Corporation (United States)

- •Solvay SA (Belgium)

- •Mitsui Chemicals, Inc. (Japan)

- •Süd-Chemie AG (Germany)

- •Celanese Corporation (United States)

- •Wacker Chemie AG (Germany)

- •Evonik Industries AG (Germany)

- •Sekisui Chemical Co., Ltd. (Japan)

- •Nitto Denko Corporation (Japan)

Market Breakdown

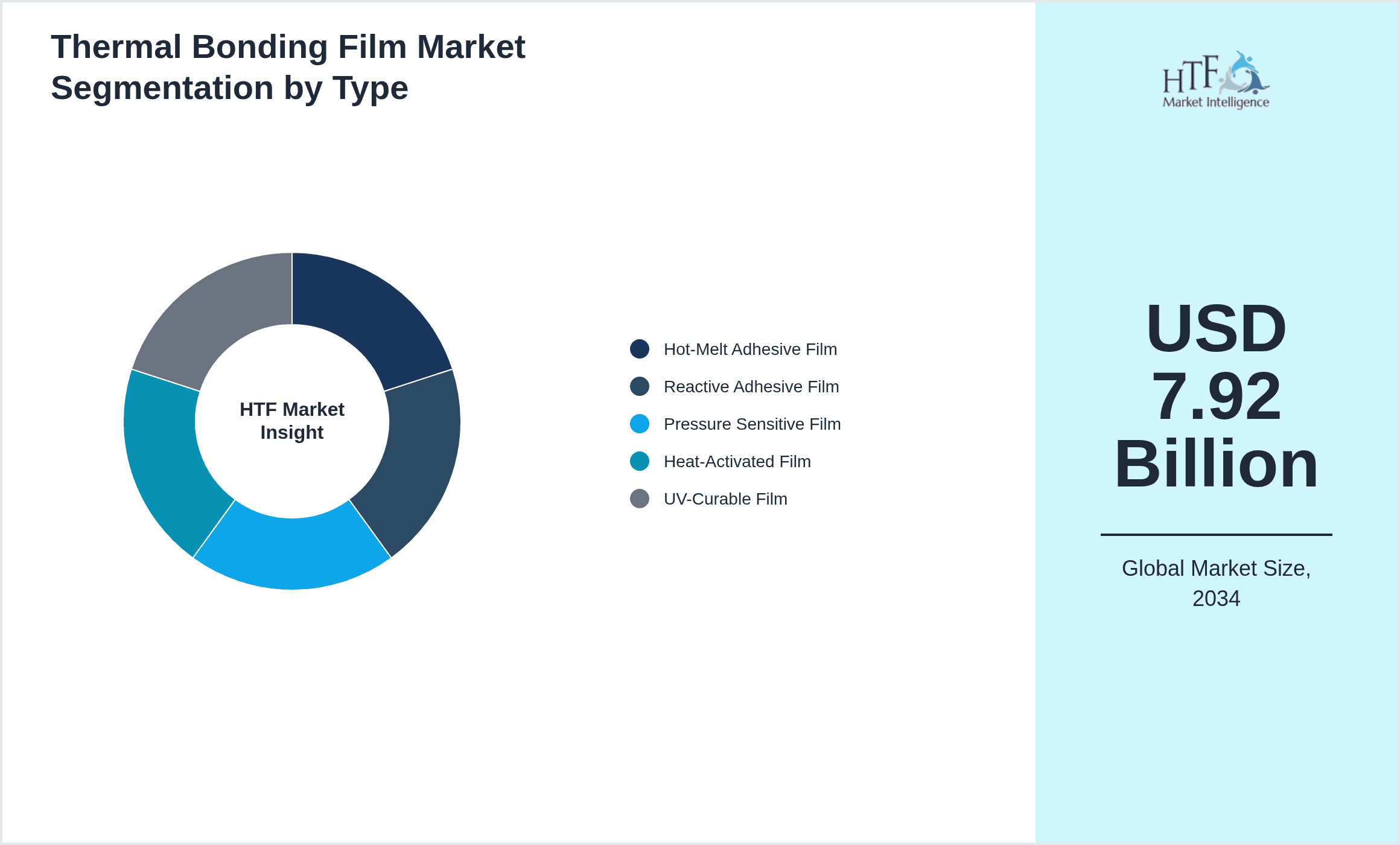

- •By Product Type

- ◦Hot-Melt Adhesive Film

- ◦Reactive Adhesive Film

- ◦Pressure Sensitive Film

- ◦Heat-Activated Film

- ◦UV-Curable Film

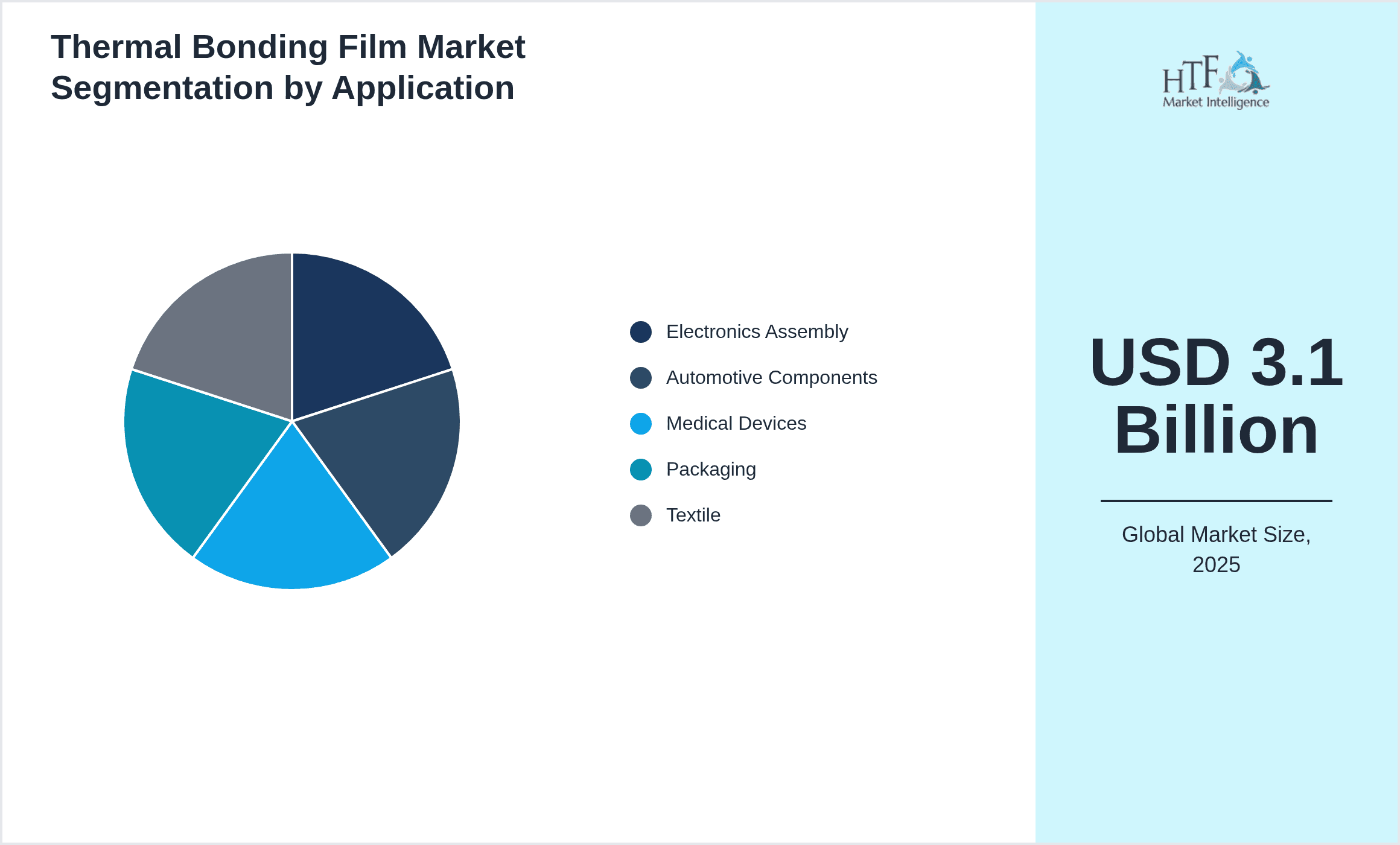

- •By Application

- ◦Electronics Assembly

- ◦Automotive Components

- ◦Medical Devices

- ◦Packaging

- ◦Textile

- •By End-Use Industry

- ◦Electronics

- ◦Automotive

- ◦Healthcare

- ◦Packaging

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors

- ◦Converters

Growth Dynamics

- •The growth of the global thermal bonding film market is propelled by increasing demand for lightweight and durable bonding solutions in the automotive and electronics industries. For instance, automotive manufacturers are adopting thermal bonding films to reduce vehicle weight, improving fuel efficiency and reducing emissions. This trend is particularly pronounced in North America and Asia-Pacific, where stringent environmental regulations are promoting adoption. Additionally, the expansion of consumer electronics with miniaturized components necessitates advanced bonding technologies that thermal bonding films provide, supporting market growth.

- •Technological advancements such as the development of UV-curable thermal bonding films are accelerating market growth by offering faster curing times and enhanced bond strength. These innovations enable manufacturers to increase production throughput while maintaining high quality, which is critical in sectors like medical devices and packaging. Companies investing in R&D to develop sustainable, solvent-free adhesive films are also tapping into growing environmental concerns, thereby expanding their market presence.

- •The rising industrialization and urbanization in emerging economies, especially in Asia-Pacific, are creating significant market opportunities. Growing automotive production facilities and expansion of electronics manufacturing hubs in countries such as China, India, and Southeast Asia are driving demand for thermal bonding films. Increased consumer spending on medical devices and packaging solutions further contributes to the demand surge in these regions.

- •Government initiatives promoting green manufacturing and energy-efficient products are encouraging the adoption of eco-friendly thermal bonding films. Incentives for sustainable product development and regulations limiting volatile organic compounds (VOCs) in adhesives are influencing manufacturers to shift towards environmentally benign bonding solutions. This regulatory support is a key driver behind the increasing market penetration of advanced thermal bonding films.

- •The growing automation and digitization in manufacturing processes are driving the need for reliable and fast-curing adhesive films. Thermal bonding films that integrate with automated assembly lines reduce human error and improve product consistency. This trend is especially relevant in electronics and medical device manufacturing, where precision bonding is essential for product performance.

- •Investment trends indicate increasing capital allocation towards adhesive technology innovation, with companies focusing on multifunctional films that combine bonding with other properties such as electrical conductivity or barrier protection. This diversification strategy enhances the value proposition of thermal bonding films, encouraging adoption across new applications.

- •Future growth prospects are supported by expanding applications in emerging sectors such as flexible electronics, wearable devices, and advanced packaging. These sectors require innovative bonding solutions that offer flexibility, durability, and environmental resistance, which thermal bonding films are increasingly able to provide through ongoing R&D efforts.

Market Trends

- •The market is witnessing a shift towards bio-based and solvent-free thermal bonding films driven by sustainability concerns and regulatory mandates. Companies like Henkel and 3M are launching eco-friendly adhesive products that reduce environmental impact without compromising performance, influencing market dynamics globally.

- •Integration of smart adhesive technologies with functionalities such as electrical conductivity and thermal management is gaining traction. This trend enables thermal bonding films to serve dual purposes, particularly in electronics and automotive applications, enhancing product value.

- •Strategic collaborations between adhesive manufacturers and technology firms are accelerating innovation cycles. For example, partnerships focusing on additive manufacturing and customized bonding solutions have been initiated, enabling faster go-to-market strategies for new thermal bonding films.

- •Digitalization of manufacturing through Industry 4.0 adoption is influencing the thermal bonding film market, with increased use of automated application systems improving precision and reducing waste. This trend is particularly prominent in developed regions like North America and Europe.

- •Rising demand for lightweight and flexible bonding solutions in packaging and textile sectors is driving product innovation. Thermal bonding films with enhanced elasticity and adhesion to diverse substrates are being developed to meet these market needs.

- •Market segmentation based on end-use industries is evolving, with medical devices and electronics gaining higher shares due to stringent bonding requirements and growth in these sectors worldwide.

- •The emergence of regional manufacturing hubs in Asia-Pacific and Latin America is reshaping global supply chains for thermal bonding films, leading to localized production and faster delivery times.

Market Opportunities

- •Expanding applications in flexible electronics and wearable devices present significant growth opportunities for thermal bonding films with adaptable and durable adhesive properties. Market players investing in specialized formulations can capitalize on this emerging segment.

- •Untapped potential in emerging economies due to increasing industrialization and consumer demand offers avenues for market expansion. Localized manufacturing and tailored product offerings can enhance penetration in regions like Latin America and Middle East & Africa.

- •Development of multifunctional thermal bonding films that integrate electrical conductivity, moisture barrier, or antimicrobial properties can open new markets in healthcare and electronics, driving differentiation and premium pricing.

- •Strategic partnerships and acquisitions focused on sustainable adhesive technologies can accelerate innovation and market access, providing competitive advantages to early movers.

- •Geographical expansion, especially in Asia-Pacific, supported by government incentives for advanced manufacturing, can boost revenue streams and strengthen global market presence.

- •Growing demand for eco-friendly packaging solutions creates opportunities for thermal bonding films that comply with regulatory standards while maintaining performance.

- •Investment in advanced R&D for faster curing, lower energy consumption, and improved adhesion to diverse substrates can enhance product appeal across industries.

Market Challenges

- •High raw material costs and supply chain disruptions pose significant challenges, impacting pricing and availability of thermal bonding films globally. Volatility in petrochemical feedstocks affects adhesive formulation costs, pressuring manufacturer margins.

- •Technical limitations in achieving universal adhesion across diverse substrates can restrict application scope. Development cycles for new formulations are lengthy and capital intensive, delaying market entry.

- •Stringent environmental regulations require reformulation of adhesives to reduce VOC emissions and hazardous components, necessitating substantial investment and compliance efforts.

- •Competitive pressure from alternative bonding technologies such as mechanical fastening or liquid adhesives may limit market share growth in certain applications.

- •Lack of standardized testing and certification protocols across regions can create market entry barriers and increase commercialization complexity.

- •End-user resistance to adoption due to legacy manufacturing processes and cost concerns can slow market penetration, particularly in traditional industries.

- •Supply chain complexities, including dependency on specialized raw materials and logistics issues, can hamper timely delivery and production scalability.

Regulatory Framework

- •The EU's REACH regulation, updated between 2020 and 2025, mandates rigorous chemical safety assessments and restrictions on hazardous substances used in adhesives, compelling manufacturers to reformulate thermal bonding films for compliance and market access.

- •In North America, the EPA's VOC content limits introduced during this period require adhesive producers to reduce emissions, driving development of low-VOC and solvent-free thermal bonding films.

- •Japan's Chemical Substances Control Law revisions from 2021 emphasize environmental safety and biodegradability of chemical products, influencing adhesive formulation standards in the region.

- •China's GB standards for adhesive materials, updated by 2025, include specifications for thermal bonding films used in electronics and automotive sectors, ensuring product safety and performance consistency.

- •Government incentives across Europe and Asia-Pacific promote sustainable manufacturing practices, encouraging adoption of eco-friendly adhesive technologies through subsidies and tax benefits.

Market Intelligence

- •15th February 2025, 3M Company unveiled its latest line of eco-friendly thermal bonding films designed for automotive and electronics applications. These new films utilize bio-based adhesive formulations that reduce environmental impact while maintaining high bond strength and heat resistance. The launch aims to support manufacturers in meeting stricter emission regulations and sustainability targets. Strategic partnerships with automotive OEMs are planned to integrate these films into next-generation vehicle models, enhancing fuel efficiency and assembly efficiency. Source: Official 3M Press Release

- •10th April 2025, Henkel AG & Co. KGaA introduced a UV-curable thermal bonding film targeting medical device manufacturers requiring rapid curing and sterile bonding processes. The product features enhanced biocompatibility and improved adhesion to polymer substrates, reducing production cycle times significantly. This innovation responds to growing demand for advanced adhesive solutions in healthcare amid increasing regulatory scrutiny. Henkel's collaboration with leading medical equipment manufacturers aims to accelerate adoption globally. Source: Henkel Corporate Website

- •28th June 2025, Dow Inc. announced a strategic alliance with a major electronics manufacturer to develop multifunctional thermal bonding films with integrated electrical conductivity and thermal management properties. This initiative targets the flexible electronics and wearable device markets, where enhanced material performance is critical. The partnership focuses on co-development and joint commercialization, aiming to shorten product development cycles and expand market reach. This collaboration is expected to strengthen Dow's position in high-growth adhesive segments. Source: Dow Newsroom

- •12th September 2025, Eastman Chemical Company completed the acquisition of a specialty adhesive film manufacturer to bolster its thermal bonding film portfolio. The acquisition enhances Eastman's technological capabilities in reactive adhesive systems and expands its presence in Asia-Pacific, a key growth region. The integration is projected to deliver synergies in R&D and manufacturing, accelerating innovation and market penetration. This move aligns with Eastman's strategic focus on sustainable and high-performance adhesive solutions. Source: Eastman Investor Relations

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 3.1 Billion |

| Forecast Year Market Size | USD 7.92 Billion |

| CAGR | 10.3% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 9.9% |

| Scope of Report | Market is segmented by Product Type (Hot-Melt Adhesive Film, Reactive Adhesive Film, Pressure Sensitive Film, Heat-Activated Film, UV-Curable Film), Application (Electronics Assembly, Automotive Components, Medical Devices, Packaging, Textile), End-Use Industry (Electronics, Automotive, Healthcare, Packaging), Distribution Channel (Direct Sales, Distributors, Converters) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | 3M Company (United States), Henkel AG & Co. KGaA (Germany), Arkema Group (France), H.B. Fuller Company (United States), Jowat SE (Germany), H.B. Fuller Company (United States), Bostik SA (France), Sika AG (Switzerland), Tesa SE (Germany), Dow Inc. (United States), Eastman Chemical Company (United States), Covestro AG (Germany), Kuraray Co., Ltd. (Japan), Henkel Adhesive Technologies (Germany), Honeywell International Inc. (United States), Shin-Etsu Chemical Co., Ltd. (Japan), Huntsman Corporation (United States), Solvay SA (Belgium), Mitsui Chemicals, Inc. (Japan), Süd-Chemie AG (Germany), Celanese Corporation (United States), Wacker Chemie AG (Germany), Evonik Industries AG (Germany), Sekisui Chemical Co., Ltd. (Japan), Nitto Denko Corporation (Japan) |

Global Thermal Bonding Film Market Size, Growth & Revenue 2025-2034 - Table of Contents

Research enthusiast focused on transforming data uncovering into actionable insights through data-driven decision-making.

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.