Global HVAC Control Systems Market Size, Growth & Revenue 2024-2034

Global HVAC Control Systems Market is segmented by Product Type (Programmable Thermostats, Smart Thermostats, Building Automation Systems, Zone Control Systems, Others), Application (Residential, Commercial, Industrial, Institutional, Others), End-Use Industry (Construction, Healthcare, Education, Hospitality), Distribution Channel (Direct Sales, Distributors/Dealers, Online Retail), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global HVAC Control Systems market represents an essential sector focusing on technologies that regulate and optimize heating, ventilation, and air conditioning within various building environments. The market includes a wide array of control systems such as programmable thermostats, smart thermostats, building automation systems, and zone control systems, serving residential, commercial, industrial, and institutional applications. These systems integrate advanced IoT and AI technologies to enhance energy efficiency, occupant comfort, and operational automation, aligning with global sustainability goals and regulatory mandates. Growing urbanization, rising environmental awareness, and the increasing adoption of smart building technologies drive the expansion of this market. Additionally, digital transformation and the shift toward cloud-based HVAC management solutions broaden the scope of deployment. This market is characterized by rapid innovation, competitive dynamics, and increasing investments across regions such as North America, Europe, and Asia-Pacific. The report provides a detailed analysis of market segmentation, key players, growth drivers, restraints, opportunities, and forecasts through 2034, offering stakeholders insightful perspectives to capitalize on emerging trends and challenges.

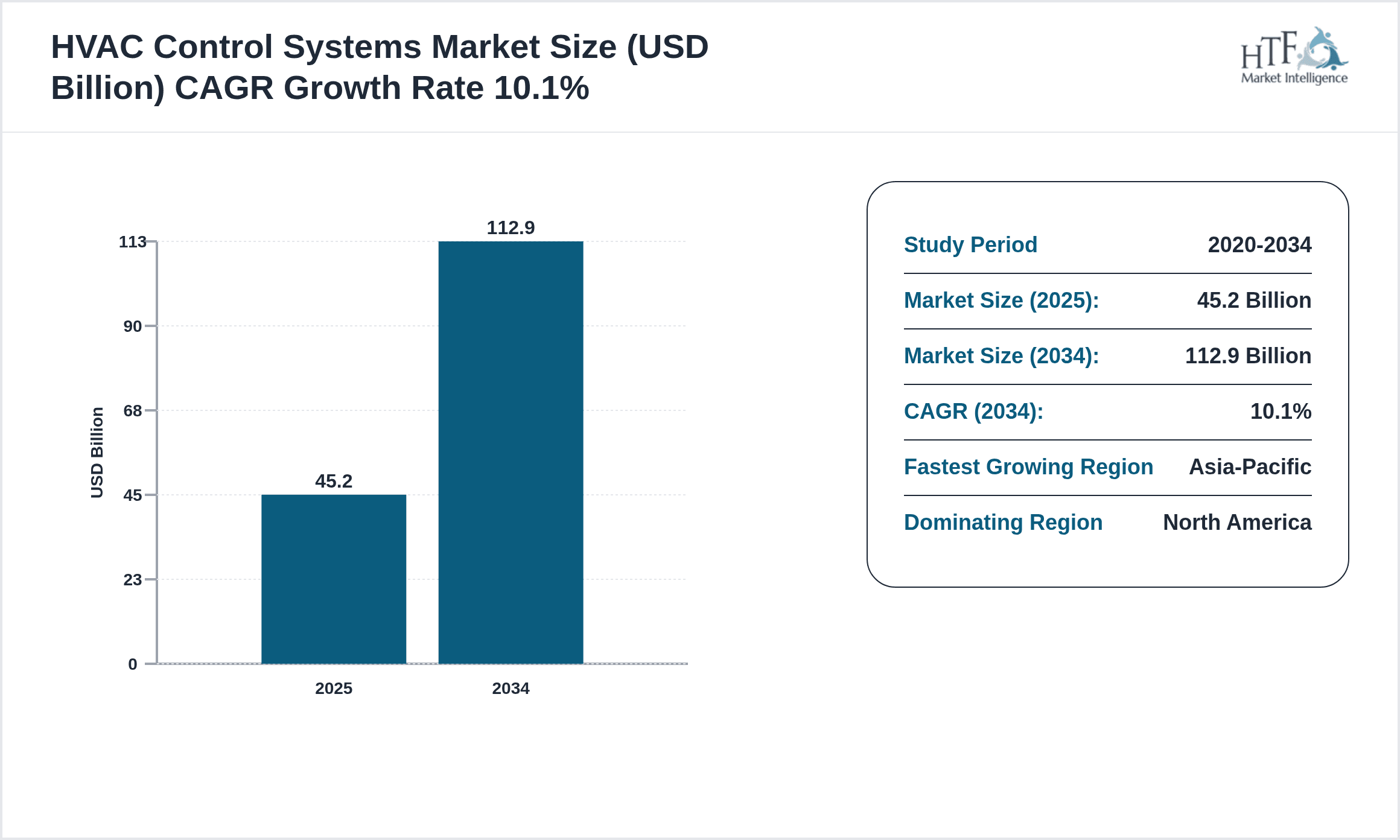

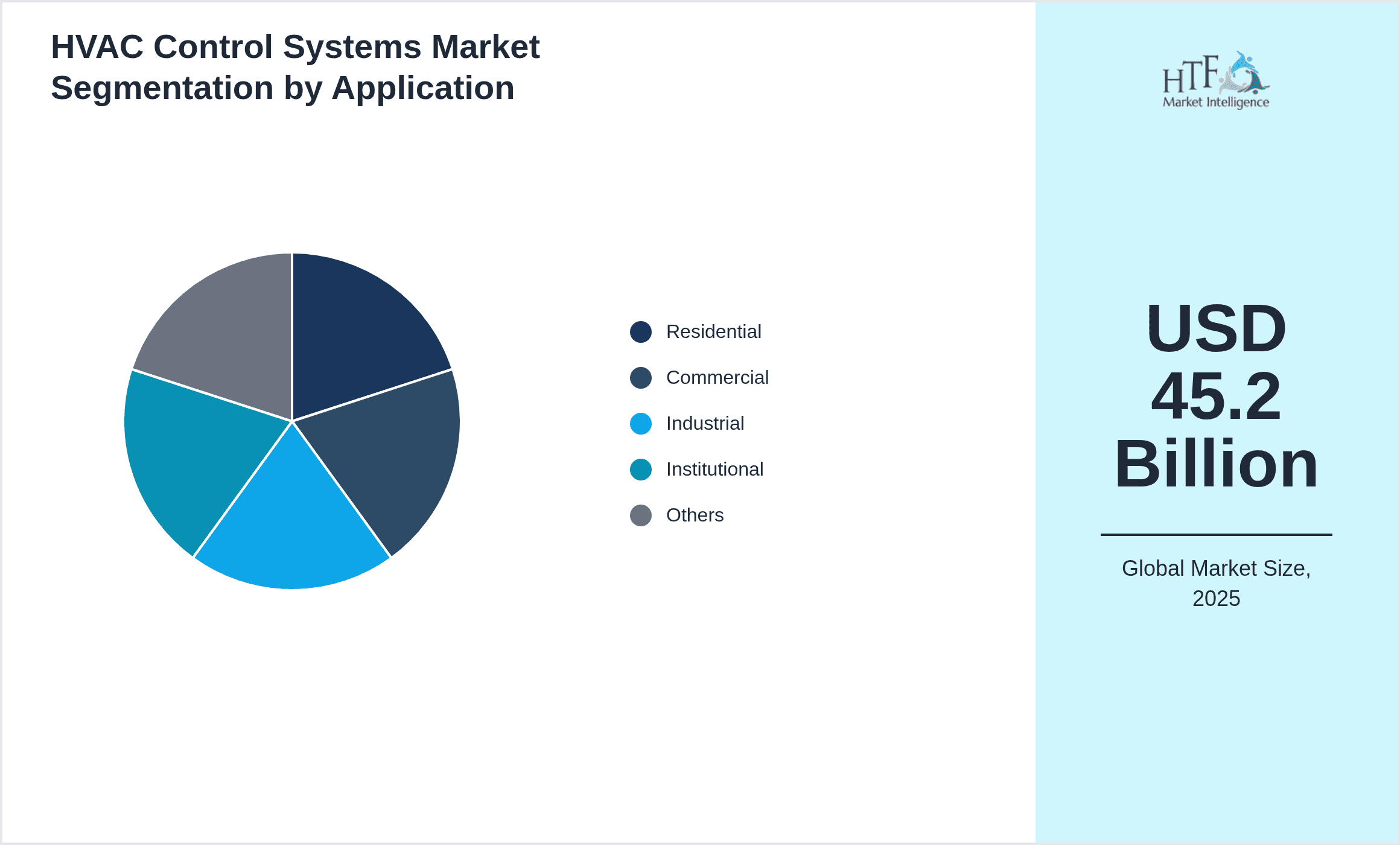

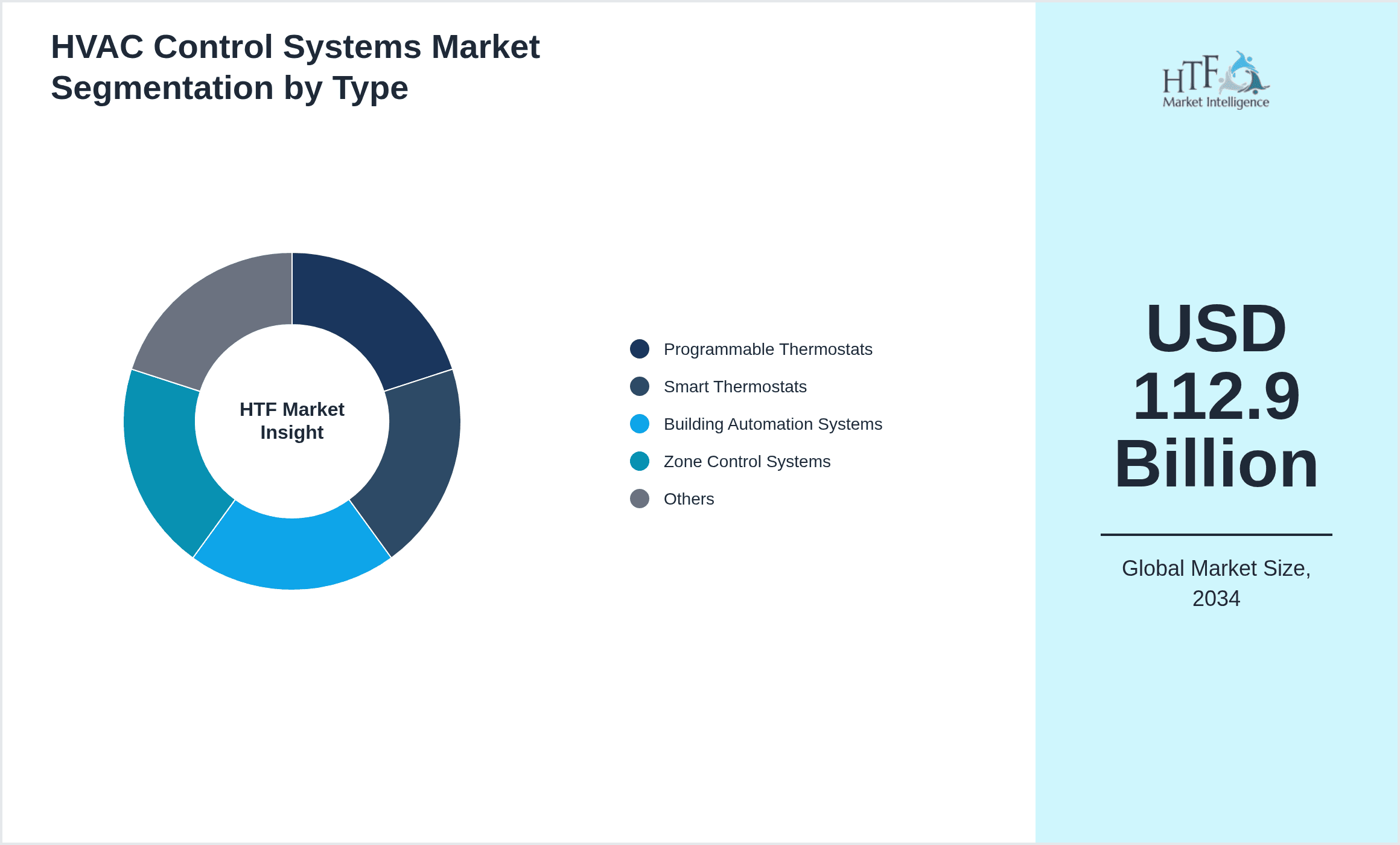

- •Key market highlights indicate a robust CAGR of 10.1% between 2024 and 2034, driven primarily by the rising demand for energy-efficient HVAC solutions and smart building integrations. The base market size was USD 45.2 Billion in 2024, with forecasts projecting growth to USD 112.9 Billion by 2034. North America dominates the market due to established infrastructure and technological advancements, while Asia-Pacific is the fastest-growing region, fueled by rapid industrialization and urban expansion. Building automation systems lead product types, reflecting their comprehensive control capabilities, whereas smart thermostats are the fastest-growing segment, benefiting from IoT proliferation and consumer preference for remote control. Applications in commercial and residential sectors remain significant with increasing automation and energy management needs. Market dynamics also include evolving regulatory frameworks focusing on energy conservation and emissions reduction across major regions.

- •The HVAC Control Systems market offers critical value propositions by enabling energy savings, reducing carbon footprints, and enhancing occupant comfort, which are vital for building owners, facility managers, and technology integrators. Strategic importance is underscored by the integration of AI, cloud computing, and IoT within HVAC solutions that enhance predictive maintenance and operational efficiency. Stakeholders ranging from manufacturers, system integrators, to end-users benefit from optimized energy consumption and regulatory compliance. Furthermore, the convergence of HVAC control with smart city initiatives and green building certifications presents new avenues for growth. The market also supports broader sustainability agendas and digital transformation efforts globally, making it a pivotal segment in the evolving landscape of building management and environmental stewardship.

Competitive Landscape

The global HVAC Control Systems market is highly competitive, featuring a diverse mix of multinational corporations and specialized regional players. Competitive dynamics are shaped by continuous innovation in smart technologies, system integration capabilities, and energy-efficient solutions. Market leaders leverage extensive R&D investments to develop next-generation HVAC controls incorporating IoT, AI, and cloud platforms, enhancing product differentiation and customer value. Strategic partnerships, mergers, and acquisitions are prevalent strategies to expand product portfolios, geographic reach, and technological expertise. Pricing strategies balance advanced features with cost competitiveness, catering to various end-user segments. Distribution channels range from direct sales to digital platforms, enabling wider market penetration. Additionally, regulatory compliance and sustainable product offerings act as competitive differentiators. The rivalry drives accelerated product launches, customization, and after-sales services to capture and retain market share. Regional competition is influenced by localized needs, infrastructure maturity, and regulatory environments, with emerging markets presenting substantial growth opportunities.

Leading Companies in HVAC Control Systems Market

- •Honeywell International Inc. (United States)

- •Johnson Controls International plc (Ireland)

- •Siemens AG (Germany)

- •Schneider Electric SE (France)

- •Emerson Electric Co. (United States)

- •Trane Technologies plc (Ireland)

- •ABB Ltd. (Switzerland)

- •Delta Electronics, Inc. (Taiwan)

- •United Technologies Corporation (United States)

- •Lennox International Inc. (United States)

- •Mitsubishi Electric Corporation (Japan)

- •Daikin Industries, Ltd. (Japan)

- •Carrier Global Corporation (United States)

- •Bosch Thermotechnology (Germany)

- •Samsung Electronics Co., Ltd. (South Korea)

- •Siemens Building Technologies Division (Germany)

- •Azbil Corporation (Japan)

- •Legrand S.A. (France)

- •Johnson Controls-Hitachi Air Conditioning (Japan)

- •Honeywell Building Solutions (United States)

- •Ingersoll Rand Inc. (United States)

- •Eaton Corporation plc (Ireland)

- •Rockwell Automation, Inc. (United States)

- •Siemens Smart Infrastructure (Germany)

- •ABB Smart Buildings (Switzerland)

Market Breakdown

- •By Product Type

- ◦Programmable Thermostats

- ◦Smart Thermostats

- ◦Building Automation Systems

- ◦Zone Control Systems

- ◦Others

- •By Application

- ◦Residential

- ◦Commercial

- ◦Industrial

- ◦Institutional

- ◦Others

- •By End-Use Industry

- ◦Construction

- ◦Healthcare

- ◦Education

- ◦Hospitality

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors/Dealers

- ◦Online Retail

Growth Dynamics

The global HVAC Control Systems market growth is propelled by the accelerating demand for energy-efficient and smart building solutions. Increasing awareness regarding environmental sustainability and stringent government regulations on energy consumption have compelled industries to adopt advanced HVAC controls that optimize energy use and reduce carbon footprints. Additionally, the rapid urbanization and expanding construction activities worldwide, especially in emerging economies, drive the demand for sophisticated HVAC solutions. Integration of IoT and AI in HVAC systems enhances remote monitoring, predictive maintenance, and personalized climate control, significantly boosting market adoption. Moreover, the rise in consumer preference for smart homes and commercial spaces with automated environmental controls further fuels growth. Investments in technological innovation, such as cloud-based HVAC management platforms, provide scalability and operational efficiency, supporting sustained market expansion. The convergence of digital technologies with traditional HVAC systems creates new business models and revenue streams, underpinning the robust CAGR observed in the forecast period.

Market Trends

The HVAC Control Systems market is witnessing a significant shift towards smart and connected devices driven by advancements in IoT technology. Adoption of AI algorithms for predictive analytics and energy optimization is becoming mainstream, enabling enhanced operational efficiency and user comfort. Integration with building management systems facilitates centralized control and data-driven decision-making, reflecting a trend towards holistic building automation. Furthermore, sustainability trends encourage the development of eco-friendly HVAC solutions with low environmental impact. Manufacturers are increasingly focusing on modular and scalable systems that can be customized to diverse building types and sizes, enhancing flexibility. The rise of cloud-based platforms has introduced subscription-based models, providing cost-effective solutions and continuous updates. Additionally, partnerships between technology providers and construction firms are shaping innovative HVAC integration approaches. Consumer demand for user-friendly interfaces and mobile app control is also influencing product design and development pipelines.

Market Opportunities

Emerging markets in Asia-Pacific and Latin America present significant opportunities due to rapid urbanization and industrial growth, driving demand for advanced HVAC control systems. The increasing focus on green buildings and smart city initiatives opens avenues for innovative HVAC solutions that align with sustainability goals. Integration of renewable energy sources with HVAC systems offers potential for reducing operational costs and environmental impact. Additionally, developing retrofit solutions for aging infrastructure in developed regions creates a substantial market segment. The proliferation of IoT and AI technologies enables providers to offer enhanced value-added services such as predictive maintenance and energy analytics, fostering customer loyalty and new revenue streams. Moreover, customized solutions tailored to specific regional climatic conditions and regulatory requirements can differentiate offerings. Strategic collaborations and partnerships to expand distribution networks and technology capabilities further enhance market penetration prospects globally.

Market Challenges

The HVAC Control Systems market faces challenges including high initial investment costs, which can deter small and medium enterprises from adopting advanced solutions. Integration complexities with existing building infrastructure, especially in retrofit scenarios, pose technical hurdles and increase implementation timelines. Additionally, the lack of standardized protocols across different systems and manufacturers limits interoperability, affecting seamless deployment. The market also contends with fluctuating raw material prices impacting production costs and supply chain stability. Data security and privacy concerns related to connected HVAC systems require robust cybersecurity measures, posing additional costs and technical demands. Furthermore, variations in regional regulations and compliance requirements create market entry barriers and complicate global product standardization. Skilled workforce shortages in emerging markets affect installation and maintenance quality, potentially impacting customer satisfaction and adoption rates.

Regulatory Framework

From 2019 to 2024, regulatory frameworks have increasingly emphasized energy efficiency and emissions reduction in the HVAC sector globally. Key mandates such as the International Energy Conservation Code (IECC) updates and regional standards like the EU’s Energy Performance of Buildings Directive (EPBD) set stringent requirements for HVAC system efficiency and environmental performance. North America introduced updated ENERGY STAR certifications and ASHRAE standards promoting sustainable HVAC solutions, influencing product development and market offerings. In Asia-Pacific, government incentives and regulations encourage adoption of smart HVAC technologies to reduce energy consumption in new and existing buildings. These regulations mandate manufacturers to meet minimum efficiency thresholds and incorporate environmentally friendly refrigerants. Compliance drives innovation in product design and facilitates the transition toward smart, automated HVAC systems. Additionally, safety and cybersecurity regulations related to IoT-enabled HVAC controls ensure data integrity and operational reliability. This evolving regulatory landscape shapes market dynamics by fostering sustainable practices and technological advancements.

Market Intelligence

- •15th January 2025, Honeywell International Inc. launched its next-generation smart thermostat featuring AI-powered adaptive learning technology capable of optimizing energy consumption based on user behavior and weather patterns. This product targets residential and commercial segments, offering seamless integration with existing building management systems and voice-controlled assistants. The innovation aligns with growing consumer demand for energy-efficient, connected devices and supports regulatory mandates for reduced carbon emissions. Honeywell aims to strengthen its market position in North America and expand in Asia-Pacific through this launch, enhancing its smart building portfolio significantly. Source: Honeywell Official Press Release

- •10th March 2025, Siemens AG introduced an advanced building automation system integrating real-time data analytics and cloud connectivity, enabling predictive maintenance and remote management across commercial infrastructure. The system leverages IoT devices to optimize HVAC operations, reduce energy costs, and improve occupant comfort. Siemens targets rapid deployment in Europe and North America with this innovation, emphasizing sustainability and operational efficiency. The strategic launch reflects Siemens’ commitment to digital transformation and smart infrastructure development. This product is expected to catalyze adoption of integrated HVAC control technologies globally. Source: Siemens Corporate News

- •20th April 2025, Johnson Controls International plc announced a strategic partnership with a leading AI software provider to develop enhanced HVAC control algorithms for commercial buildings. The collaboration aims to integrate machine learning models that predict system failures and optimize energy use dynamically. This initiative supports Johnson Controls’ objective to deliver cutting-edge smart building solutions and expand its footprint in emerging markets, especially in Asia-Pacific and Latin America. The partnership is poised to accelerate innovation and provide competitive advantages through technology differentiation. Source: Johnson Controls Press Statement

- •5th February 2025, Schneider Electric SE expanded its HVAC control systems portfolio with the launch of modular zone control units designed for flexible installation and customized climate management in residential buildings. These units feature enhanced connectivity options and user-friendly interfaces, targeting North American and European markets. The product addresses increasing demand for scalable HVAC solutions suitable for retrofit and new construction projects. Schneider Electric’s expansion reinforces its commitment to sustainable building technologies and digital solutions. Source: Schneider Electric Newsroom

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 45.2 Billion |

| Forecast Year Market Size | USD 112.9 Billion |

| CAGR | 10.1% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 9.7% |

| Scope of Report | Market is segmented by Product Type (Programmable Thermostats, Smart Thermostats, Building Automation Systems, Zone Control Systems, Others), Application (Residential, Commercial, Industrial, Institutional, Others), End-Use Industry (Construction, Healthcare, Education, Hospitality), Distribution Channel (Direct Sales, Distributors/Dealers, Online Retail) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Honeywell International Inc. (United States), Johnson Controls International plc (Ireland), Siemens AG (Germany), Schneider Electric SE (France), Emerson Electric Co. (United States), Trane Technologies plc (Ireland), ABB Ltd. (Switzerland), Delta Electronics, Inc. (Taiwan), United Technologies Corporation (United States), Lennox International Inc. (United States), Mitsubishi Electric Corporation (Japan), Daikin Industries, Ltd. (Japan), Carrier Global Corporation (United States), Bosch Thermotechnology (Germany), Samsung Electronics Co., Ltd. (South Korea), Siemens Building Technologies Division (Germany), Azbil Corporation (Japan), Legrand S.A. (France), Johnson Controls-Hitachi Air Conditioning (Japan), Honeywell Building Solutions (United States), Ingersoll Rand Inc. (United States), Eaton Corporation plc (Ireland), Rockwell Automation, Inc. (United States), Siemens Smart Infrastructure (Germany), ABB Smart Buildings (Switzerland) |

Global HVAC Control Systems Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.