Global Flavour for Pet Food Market Size, Growth & Revenue 2025-2034

Global Flavour for Pet Food Market is segmented by Product Type (Natural Flavours, Artificial Flavours, Organic Flavours, Meat-Based Flavours, Plant-Based Flavours), Application (Dry Pet Food, Wet Pet Food, Treats & Snacks, Supplements, Others), End-Use Industry (Pet Food Manufacturers, Pet Treat Producers, Pet Supplements Industry, Pet Food Retailers), Distribution Channel (Direct Sales, Distributors & Wholesalers, Online Retail), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global Flavour for Pet Food market is a specialized segment of the pet nutrition industry focusing on flavoring agents that enhance palatability and consumer appeal of pet food products. This market includes natural, artificial, organic, meat-based, and plant-based flavors used across various applications such as dry and wet pet foods, treats, and nutritional supplements. The value chain stretches from raw material extraction and flavor formulation to delivery to pet food manufacturers and ultimately to pet owners. Driven by increasing pet humanization, rising demand for premium and organic pet foods, and growing awareness of pet health, the market is witnessing robust growth. Innovation in flavor technology, regulatory compliance, and sustainability considerations are shaping product development and market expansion globally. Major regions contributing to the market include North America, Europe, and Asia-Pacific, with emerging markets in Latin America and Middle East & Africa offering significant growth opportunities.

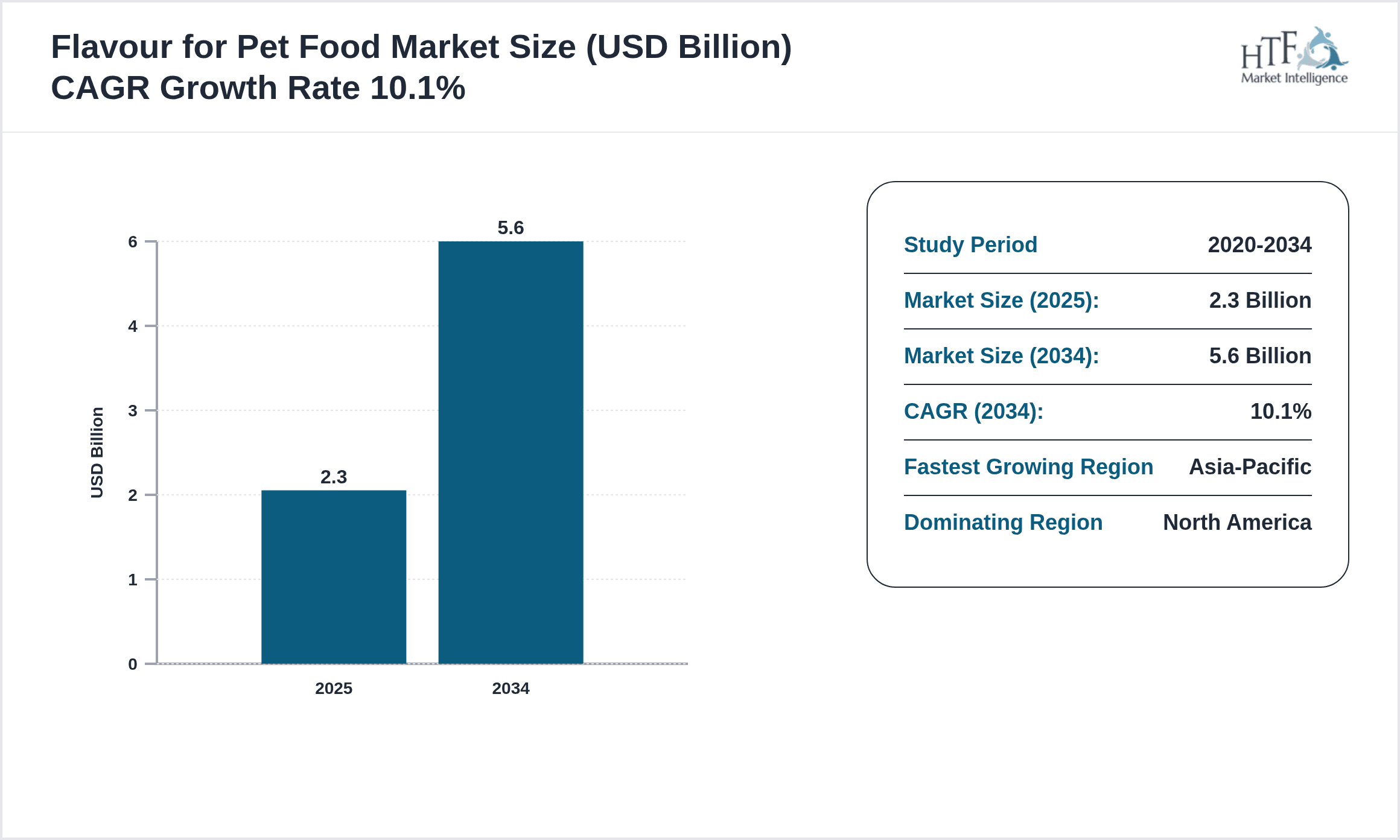

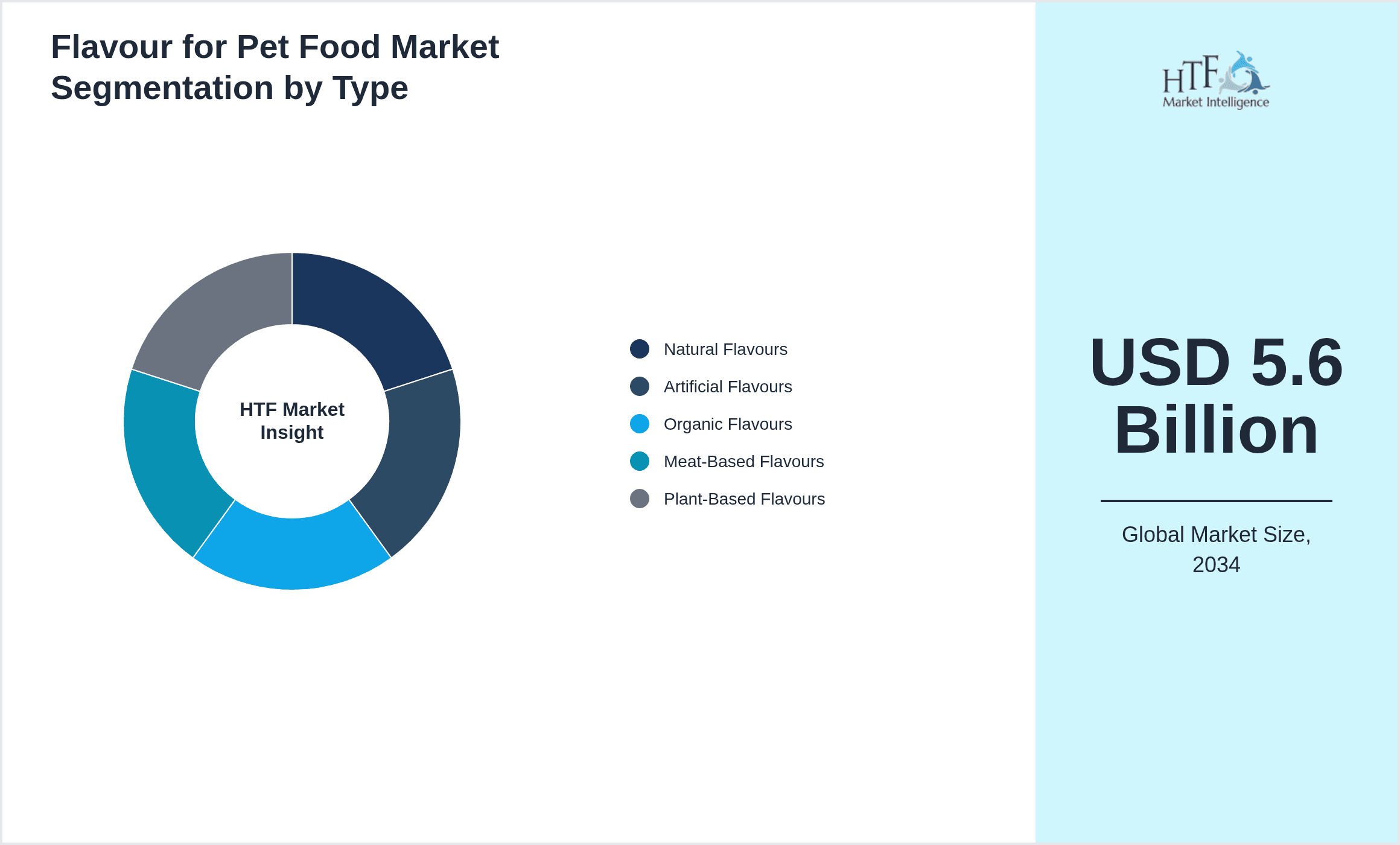

- •Key highlights include a base year market size of USD 2.3 billion in 2025, forecasted to reach USD 5.6 billion by 2034 with a CAGR of 10.1%. North America currently dominates the market due to high pet ownership and premiumization trends, while Asia-Pacific is the fastest-growing region fueled by rising disposable incomes and urbanization. Natural flavors lead the product segment, reflecting consumer preference for clean-label and health-conscious pet food options. Plant-based flavors are the fastest-growing product type, driven by shifting consumer attitudes towards sustainability and innovation in alternative ingredients. The market's year-on-year growth rate stands at 9.7%, underscoring steady expansion supported by evolving pet care trends and regulatory frameworks.

- •The flavor for pet food market offers strategic value to pet food manufacturers, ingredient suppliers, and investors by enabling differentiation and meeting evolving consumer expectations for palatability and nutritional benefits. It supports the development of specialized pet food formulations that address health, dietary restrictions, and taste preferences. Moreover, flavor innovation contributes to sustainability by incorporating organic and plant-based ingredients, aligning with environmental goals. This market also plays a critical role in expanding pet food consumption patterns globally, supporting industry growth and competitive positioning in a dynamic pet care ecosystem.

Competitive Landscape

The global Flavour for Pet Food market is characterized by intense competition among established multinational ingredient suppliers and emerging specialized players focusing on innovation and sustainability. Market dynamics include aggressive product development strategies, technological advancements in flavor formulation, and strategic partnerships with pet food manufacturers to tailor flavor solutions. Companies leverage R&D investments to develop natural, organic, and plant-based flavor options that meet regulatory standards and consumer demand for clean-label products. Competitive advantages are derived from proprietary technology platforms, robust supply chains, and compliance with global food safety regulations. Pricing strategies vary by product type and region, with premium flavors commanding higher margins in developed markets. Market entry barriers include stringent regulatory requirements and high research costs, while regional competition is influenced by differing consumer preferences and ingredient availability. Future competition will likely center on digitalization of R&D, sustainable sourcing, and expanding footprint in emerging markets.

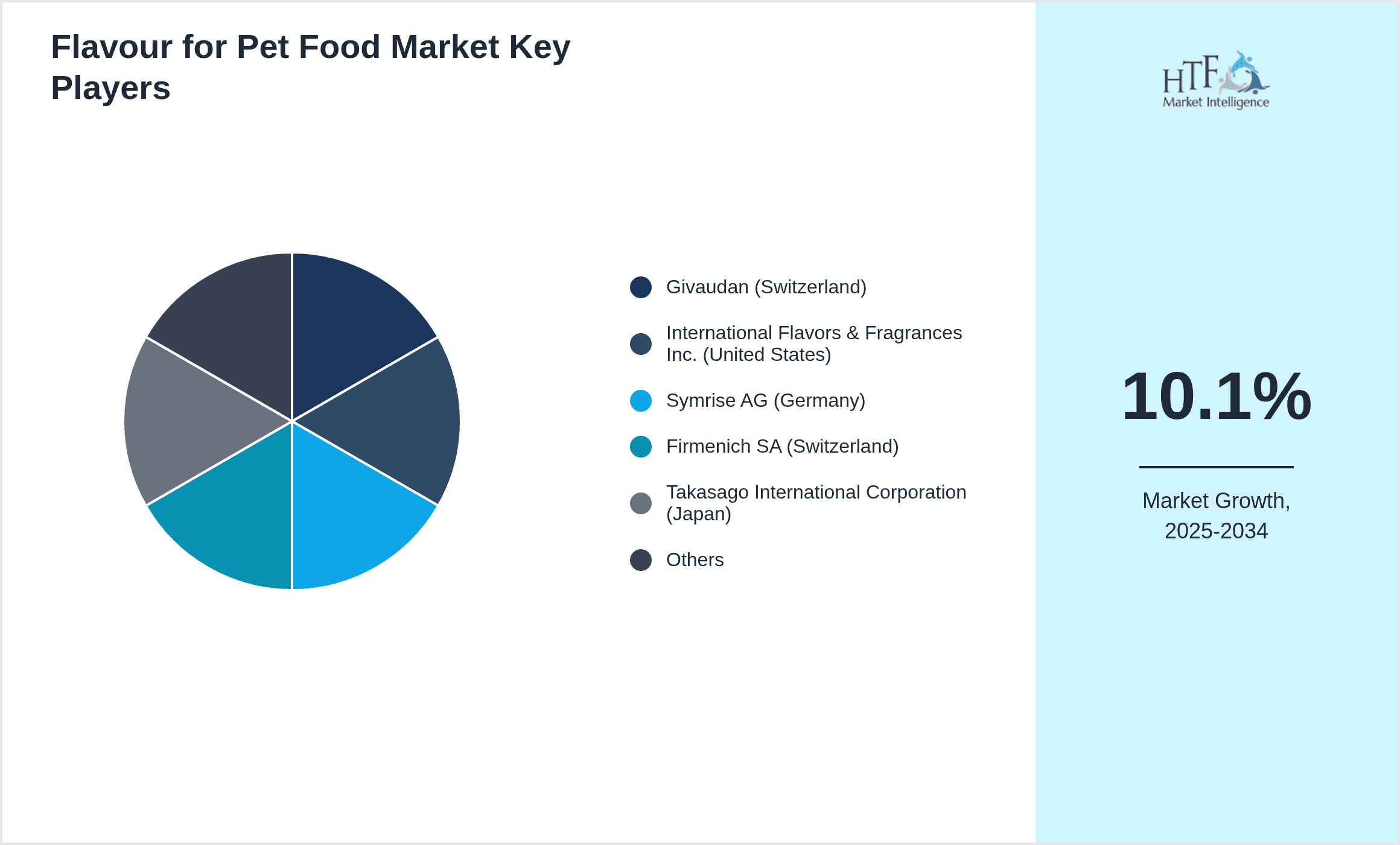

Leading Companies in Flavour for Pet Food Market

- •Givaudan (Switzerland)

- •International Flavors & Fragrances Inc. (United States)

- •Symrise AG (Germany)

- •Firmenich SA (Switzerland)

- •Takasago International Corporation (Japan)

- •Sensient Technologies Corporation (United States)

- •Mane SA (France)

- •Kerry Group plc (Ireland)

- •BENEO GmbH (Germany)

- •Chr. Hansen Holding A/S (Denmark)

- •Bell Flavors & Fragrances (United States)

- •Döhler Group (Germany)

- •International Ingredient Corporation (United States)

- •FutureCeuticals, Inc. (United States)

- •NATURAL FLAVORS, INC. (United States)

- •Frutarom Industries Ltd. (Israel)

- •T. Hasegawa Co., Ltd. (Japan)

- •AgroFresh Solutions, Inc. (United States)

- •Riken Vitamin Co., Ltd. (Japan)

- •Naturex SA (France)

- •Symrise AG (Germany)

- •Aromatech SA (France)

- •Firmenich SA (Switzerland)

- •Flavorchem Corporation (United States)

- •Zhejiang Medicine Co., Ltd. (China)

Market Breakdown

- •By Product Type

- ◦Natural Flavours

- ◦Artificial Flavours

- ◦Organic Flavours

- ◦Meat-Based Flavours

- ◦Plant-Based Flavours

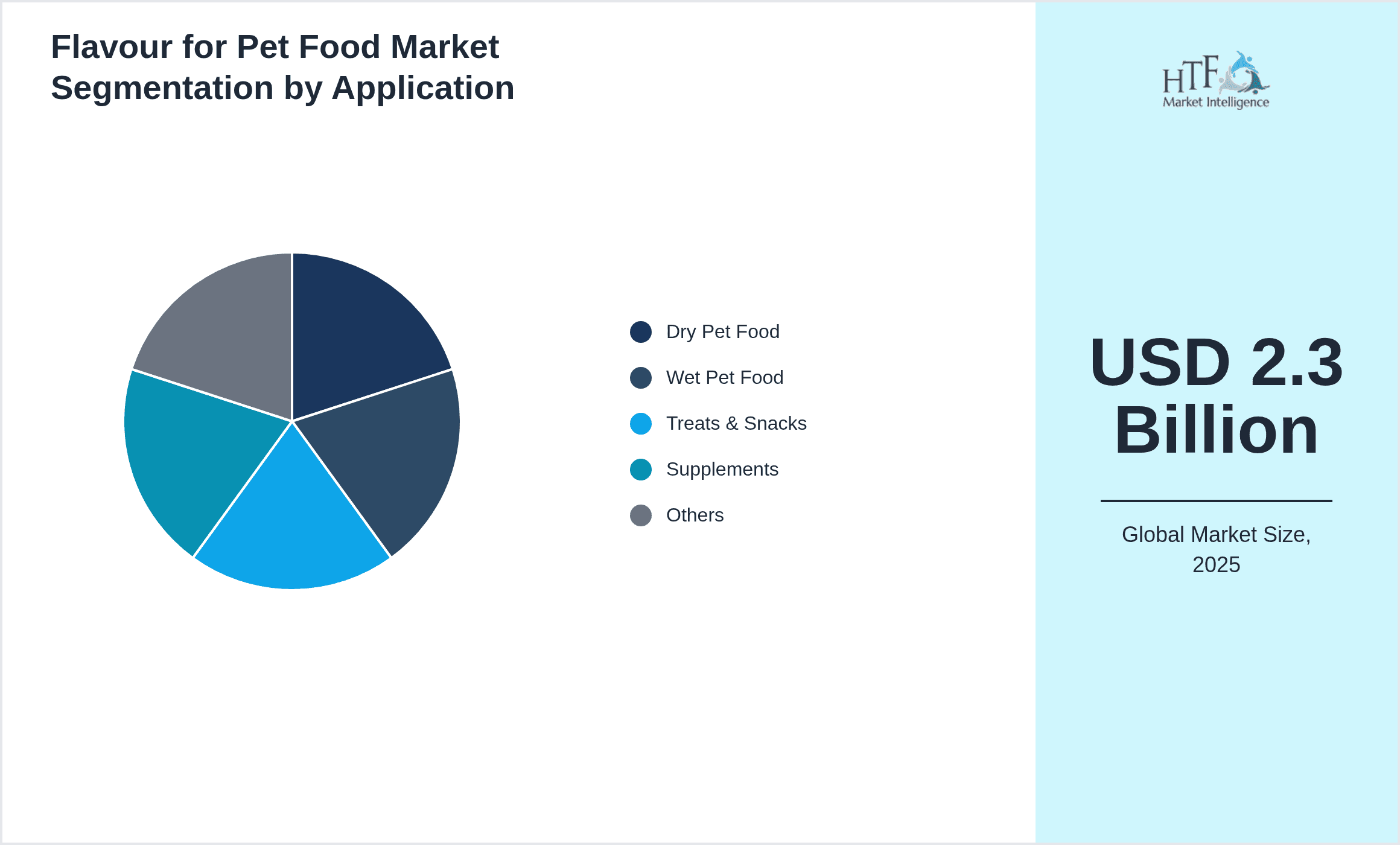

- •By Application

- ◦Dry Pet Food

- ◦Wet Pet Food

- ◦Treats & Snacks

- ◦Supplements

- ◦Others

- •By End-Use Industry

- ◦Pet Food Manufacturers

- ◦Pet Treat Producers

- ◦Pet Supplements Industry

- ◦Pet Food Retailers

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors & Wholesalers

- ◦Online Retail

Growth Dynamics

- •Increasing consumer focus on pet health and natural ingredients is driving demand for natural and organic flavors in pet food products. This trend is supported by rising pet humanization and willingness to invest in premium pet nutrition.

- •Advancements in flavor technology, including microencapsulation and flavor masking, are enhancing the effectiveness and stability of flavors, enabling manufacturers to meet diverse palatability and nutritional requirements.

- •Expansion of the pet food market in emerging economies such as Asia-Pacific is fueling growth due to rising disposable incomes, urbanization, and increasing pet ownership, creating new opportunities for flavor manufacturers.

- •Stringent regulatory standards for pet food safety and quality are promoting the development of clean-label and sustainable flavors, encouraging innovation and compliance among industry players.

- •Growing preference for plant-based and alternative protein flavors aligns with sustainability goals and evolving consumer dietary preferences, accelerating market adoption of novel flavor solutions.

- •Investment in R&D and strategic collaborations between flavor houses and pet food manufacturers are catalyzing product innovation and customized flavor solutions tailored to specific pet species and dietary needs.

- •The rise of e-commerce and online retail channels is expanding market reach and accessibility of flavored pet food products, driving sales growth and consumer engagement.

Market Trends

- •The adoption of natural and organic flavors has accelerated as consumers seek transparency and wellness-oriented pet food products, influencing formulation strategies across the industry.

- •Integration of clean-label trends with flavor innovation is leading to reduced use of artificial additives, positioning brands to meet regulatory and consumer expectations for safety and quality.

- •Collaborative innovation between flavor manufacturers and pet food companies is enhancing product differentiation through unique taste profiles and health-beneficial flavor compounds.

- •Sustainability initiatives are driving the use of plant-based and eco-friendly flavor ingredients, reflecting broader environmental concerns and corporate responsibility commitments.

- •Advanced flavor delivery systems such as encapsulation and controlled release are improving flavor longevity and masking undesirable tastes, enhancing pet acceptance and satisfaction.

- •Digitalization in product development, including AI-driven flavor modeling, is optimizing formulation efficiency and reducing time-to-market for new flavor innovations.

- •Market segmentation based on pet species and dietary needs is fostering tailored flavor solutions, addressing specific nutritional and sensory preferences.

Market Opportunities

- •Expanding premium and super-premium pet food segments present significant opportunities for innovative flavors that enhance taste and nutritional appeal, attracting health-conscious consumers.

- •Emerging markets in Asia-Pacific and Latin America offer growth potential due to increasing pet ownership and rising awareness of pet nutrition and wellness.

- •Development of plant-based and alternative protein flavors aligns with consumer demand for sustainable and ethical pet food options, providing avenues for product diversification.

- •Technological advancements in flavor encapsulation and delivery can unlock new applications in wet and dry pet food formats, improving shelf life and palatability.

- •Customization of flavor profiles for specific pet species and dietary requirements creates niche markets and enhances brand loyalty through targeted product offerings.

- •Partnerships and collaborations between flavor manufacturers and pet food companies can accelerate innovation and market penetration, leveraging combined expertise and resources.

- •Increasing online retail and e-commerce penetration facilitates direct consumer access to flavored pet food products, expanding market reach and consumer engagement.

Market Challenges

- •Regulatory complexities and varying global standards for pet food flavor ingredients pose challenges for manufacturers aiming for international market access and compliance.

- •High costs of natural and organic flavor ingredients can limit adoption in price-sensitive markets and affect product pricing strategies.

- •Technical challenges related to flavor stability, masking undesirable tastes, and maintaining shelf life require ongoing R&D investment and innovation.

- •Competition from generic flavor suppliers and substitute technologies can pressure profit margins and limit differentiation opportunities.

- •Supply chain disruptions and raw material availability issues, especially for natural and plant-based ingredients, can affect production continuity and costs.

- •Consumer skepticism and misinformation about artificial additives necessitate transparent communication and education to maintain trust and acceptance.

- •Balancing flavor enhancement with pet health requirements, including allergen management, requires careful formulation and testing.

Regulatory Framework

- •The U.S. Food and Drug Administration (FDA) updated pet food flavor ingredient guidelines between 2020 and 2025, emphasizing safety, labeling accuracy, and ingredient sourcing transparency, impacting manufacturer compliance protocols.

- •European Union regulations such as Regulation (EC) No 1831/2003 on feed additives were reinforced during this period to ensure rigorous evaluation of pet food flavor additives, fostering harmonized standards across member states.

- •The Association of American Feed Control Officials (AAFCO) introduced stricter definitions and monitoring practices for natural and organic flavor claims in pet food products, influencing product formulation and marketing strategies.

- •China’s Ministry of Agriculture and Rural Affairs (MARA) implemented updated safety standards for pet food flavoring agents, with mandatory registration and quality certifications effective from 2023, enhancing market entry requirements.

- •Government incentives and voluntary programs promoting sustainable ingredient sourcing and clean-label pet food production have encouraged industry adoption of eco-friendly flavors, supporting market growth and innovation.

Market Intelligence

- •15th February 2025, Givaudan announced the launch of its new range of plant-based pet food flavors designed to enhance palatability while supporting sustainability goals. The product line features natural extracts and innovative encapsulation technology to maintain flavor stability and mask undesirable tastes. Targeting premium pet food manufacturers globally, this initiative aligns with rising consumer demand for clean-label and eco-friendly pet nutrition. The launch is expected to strengthen Givaudan's market position and expand its portfolio in the fast-growing sustainable pet food segment. Source: Givaudan Official Press Release

- •10th April 2025, International Flavors & Fragrances Inc. (IFF) introduced an AI-driven flavor development platform to accelerate innovation in the pet food sector. This technology enables rapid formulation of customized flavor profiles tailored to specific pet species and dietary requirements, enhancing product differentiation. The platform integrates sensory data and predictive modeling to optimize flavor combinations, reducing time-to-market and R&D costs. IFF aims to collaborate with leading pet food brands to implement this technology across multiple geographic markets, reinforcing its leadership in flavor innovation. Source: IFF Corporate Announcement

- •8th January 2025, Symrise AG announced a strategic partnership with a major Asian pet food manufacturer to co-develop natural and organic flavor ingredients tailored for emerging markets. The collaboration focuses on leveraging Symrise's expertise in sustainable sourcing and flavor technology to meet the rising demand in Asia-Pacific. This initiative includes joint research projects and pilot production facilities to ensure compliance with regional regulatory standards. The partnership is expected to accelerate regional market penetration and foster innovation aligned with local consumer preferences. Source: Symrise Press Release

- •Market Intelligence: Recent developments and industry insights are being monitored. For latest updates, consult official company announcements and industry publications.

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 2.3 Billion |

| Forecast Year Market Size | USD 5.6 Billion |

| CAGR | 10.1% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 9.7% |

| Scope of Report | Market is segmented by Product Type (Natural Flavours, Artificial Flavours, Organic Flavours, Meat-Based Flavours, Plant-Based Flavours), Application (Dry Pet Food, Wet Pet Food, Treats & Snacks, Supplements, Others), End-Use Industry (Pet Food Manufacturers, Pet Treat Producers, Pet Supplements Industry, Pet Food Retailers), Distribution Channel (Direct Sales, Distributors & Wholesalers, Online Retail) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Givaudan (Switzerland), International Flavors & Fragrances Inc. (United States), Symrise AG (Germany), Firmenich SA (Switzerland), Takasago International Corporation (Japan), Sensient Technologies Corporation (United States), Mane SA (France), Kerry Group plc (Ireland), BENEO GmbH (Germany), Chr. Hansen Holding A/S (Denmark), Bell Flavors & Fragrances (United States), Döhler Group (Germany), International Ingredient Corporation (United States), FutureCeuticals, Inc. (United States), NATURAL FLAVORS, INC. (United States), Frutarom Industries Ltd. (Israel), T. Hasegawa Co., Ltd. (Japan), AgroFresh Solutions, Inc. (United States), Riken Vitamin Co., Ltd. (Japan), Naturex SA (France), Symrise AG (Germany), Aromatech SA (France), Firmenich SA (Switzerland), Flavorchem Corporation (United States), Zhejiang Medicine Co., Ltd. (China) |

Global Flavour for Pet Food Market Size, Growth & Revenue 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.