North America Automotive Chassis Market Size, Growth & Revenue 2024-2034

North America Automotive Chassis Market is segmented by Product Type (Ladder Frame Chassis, Monocoque Chassis, Backbone Frame Chassis, Space Frame Chassis, Tubular Frame Chassis), Application (Passenger Vehicles, Commercial Vehicles, Off-Highway Vehicles, Electric Vehicles, Autonomous Vehicles), End-Use Industry (Automotive OEMs, Aftermarket, Fleet Operators, Agricultural & Construction Equipment), Distribution Channel (Direct OEM Supply, Aftermarket Distribution, Tier 1 Supplier Networks), and Geography (United States, Canada, Mexico)

Pricing

Report Overview

Executive Summary

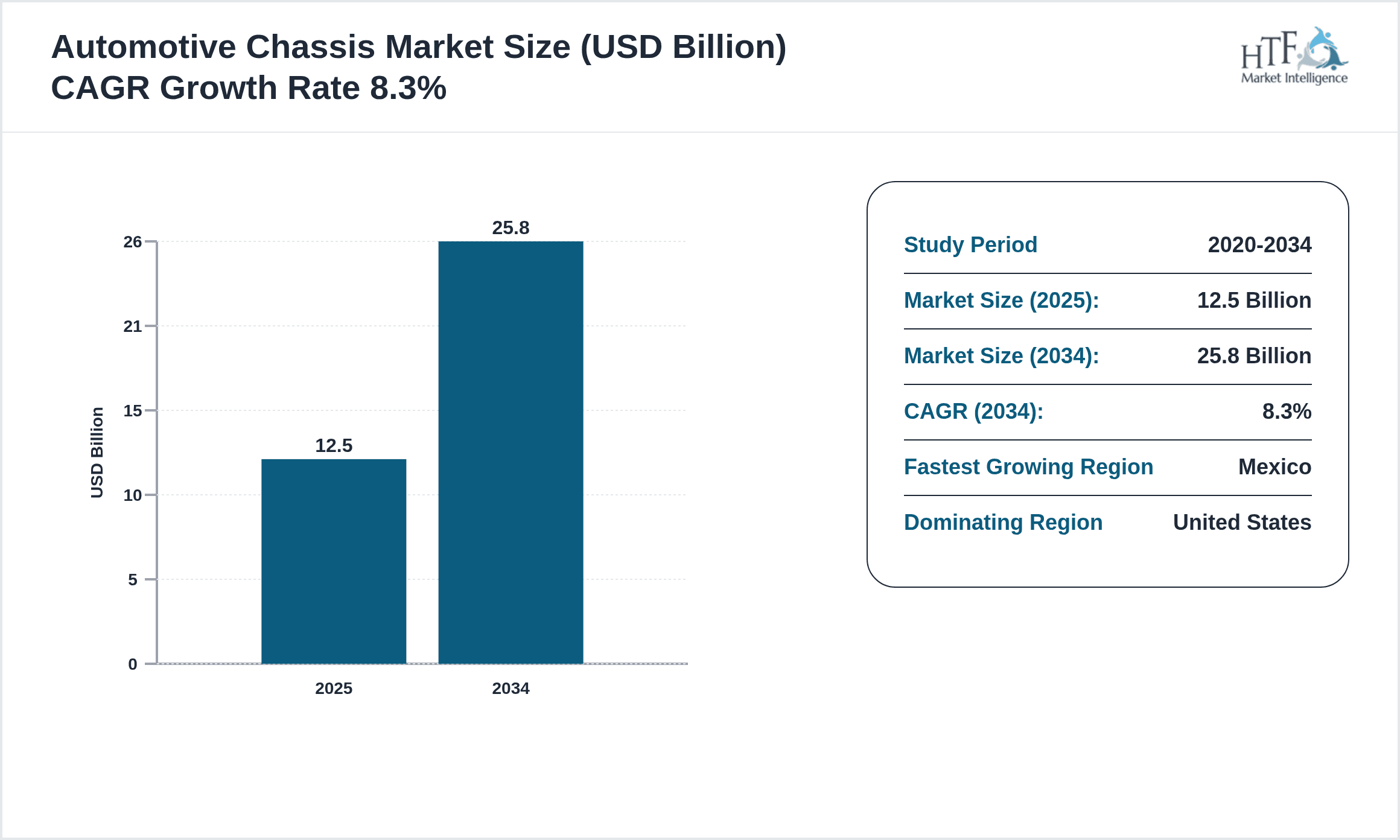

- •The North America Automotive Chassis Market is a critical segment of the automotive industry focused on the development and production of chassis systems that form the structural backbone of vehicles. This market covers a wide range of chassis types including ladder frames, monocoque, backbone, space, and tubular frames, which are utilized across passenger vehicles, commercial trucks, off-highway machinery, electric vehicles, and autonomous vehicles. The chassis not only supports vehicle weight but also influences safety, handling, and ride quality, making it integral to vehicle performance and consumer satisfaction. Increasing demand for lightweight and high-strength materials to improve fuel efficiency and reduce emissions is pushing innovation within this market. Additionally, the shift towards electric and autonomous vehicles is driving the adoption of new chassis designs that accommodate battery packs and advanced sensors. The market encompasses OEMs, Tier 1 suppliers, and aftermarket providers operating across the United States, Canada, and Mexico, reflecting the region's dynamic automotive ecosystem and regulatory environment focused on safety and emissions standards.

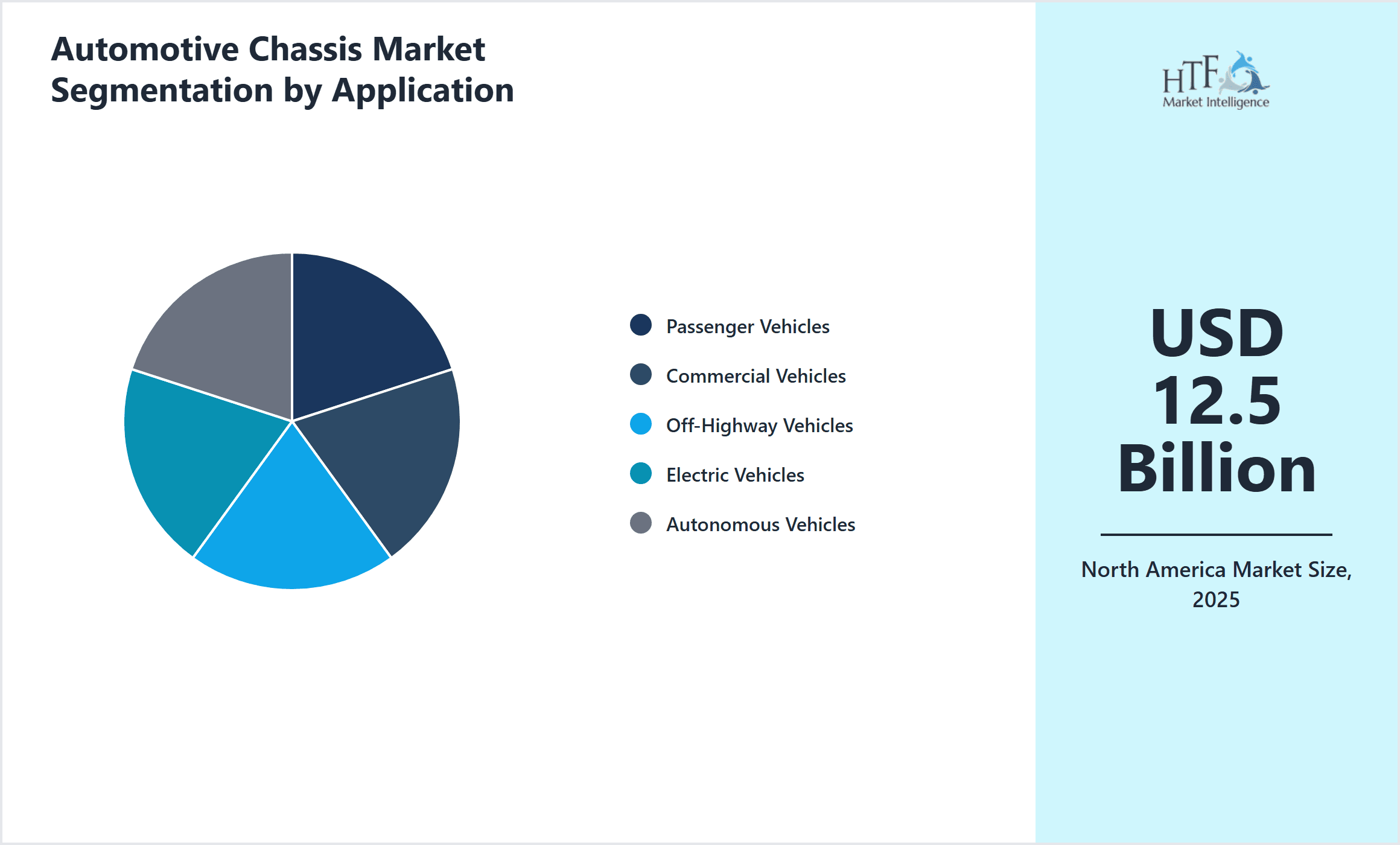

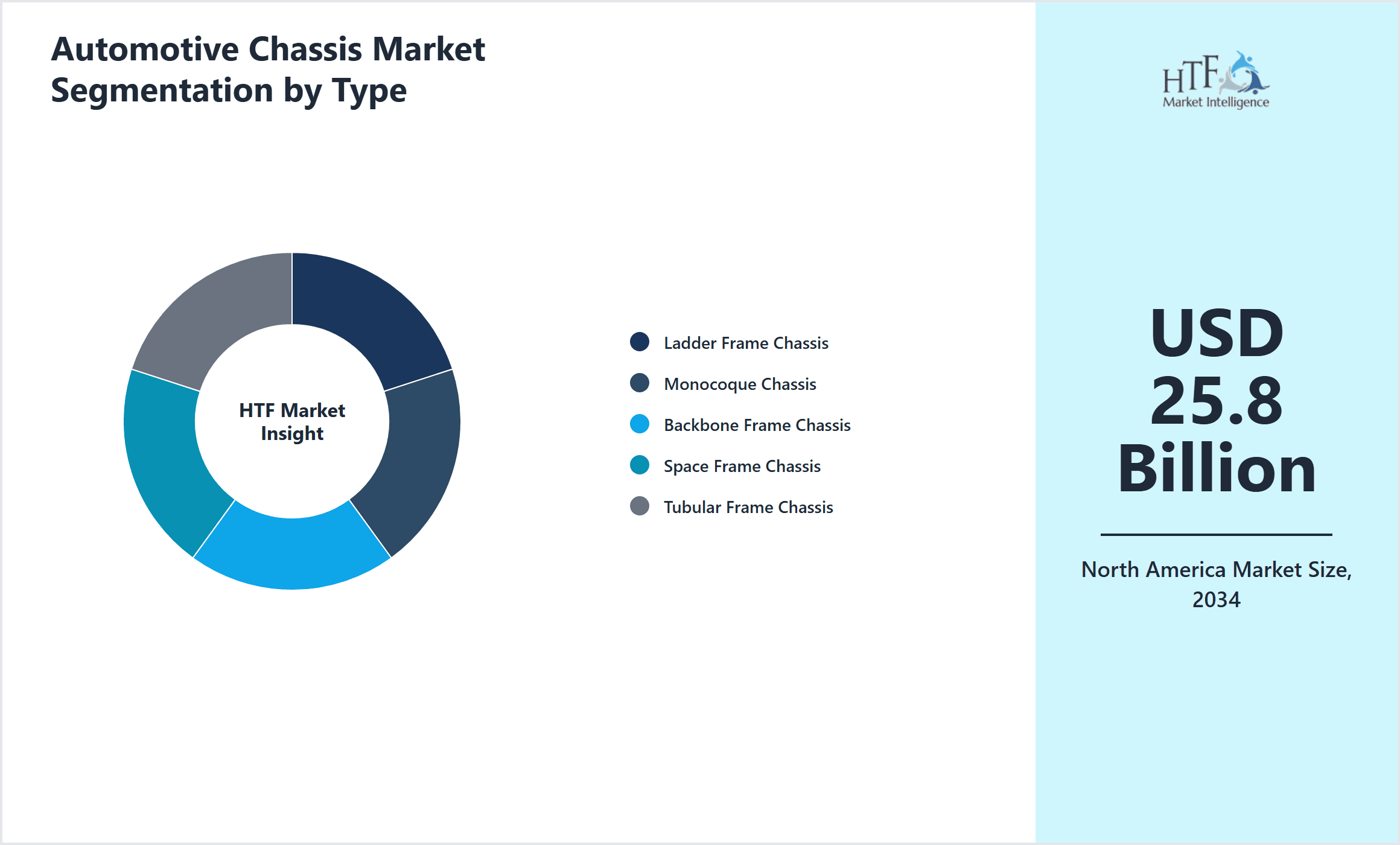

- •Key market highlights indicate a robust CAGR of 8.3% from 2025 to 2034, with the market expected to more than double from USD 12.5 Billion in 2025 to USD 25.8 Billion by 2034. The monocoque chassis segment dominates due to its widespread adoption in passenger vehicles, while the space frame chassis exhibits the fastest growth, driven by its application in electric and autonomous vehicles. The United States holds the largest market share as the dominating country, supported by its well-established automotive manufacturing base and strong R&D capabilities. Mexico is identified as the fastest-growing country within North America, benefiting from increasing automotive assembly plants and export-oriented growth. The passenger vehicle application remains the largest segment, with commercial vehicles following closely due to growth in logistics and transportation sectors.

- •The North America Automotive Chassis Market offers substantial value propositions by enabling automotive OEMs to meet stringent safety and emissions regulations while enhancing vehicle performance and customer experience. Strategic importance lies in the integration of advanced materials such as high-strength steel, aluminum, and composites, which help reduce vehicle weight and improve fuel economy. Additionally, the market supports the transition towards electrification and autonomous driving technologies by providing adaptable chassis platforms. Stakeholders including manufacturers, suppliers, and technology developers leverage this market to innovate and capture emerging opportunities driven by evolving consumer preferences and regulatory frameworks. The market's growth trajectory also highlights the increasing collaboration between automotive and technology sectors to develop next-generation chassis solutions that align with future mobility trends.

Competitive Landscape

The competitive environment in the North America Automotive Chassis Market is characterized by intense rivalry among established global automotive component manufacturers and specialized Tier 1 suppliers. Companies compete through continuous innovation in lightweight materials, advanced manufacturing technologies, and modular chassis platforms that cater to electric and autonomous vehicle segments. Market positioning is influenced by the ability to provide cost-effective, high-performance chassis solutions that comply with stringent safety and environmental regulations. Strategic partnerships and collaborations with OEMs are common to accelerate product development and integration. Mergers and acquisitions serve as critical strategies for expanding technological capabilities and geographic reach. Pricing strategies balance cost competitiveness with the value added through innovation and quality. Distribution channels are diversified, including direct OEM supply and aftermarket services. The market also sees emerging competition from technology-driven startups focusing on advanced materials and smart chassis systems. Overall, companies leverage R&D investments, supply chain optimization, and customer-centric innovation to sustain competitive advantages and capture growing market demand.

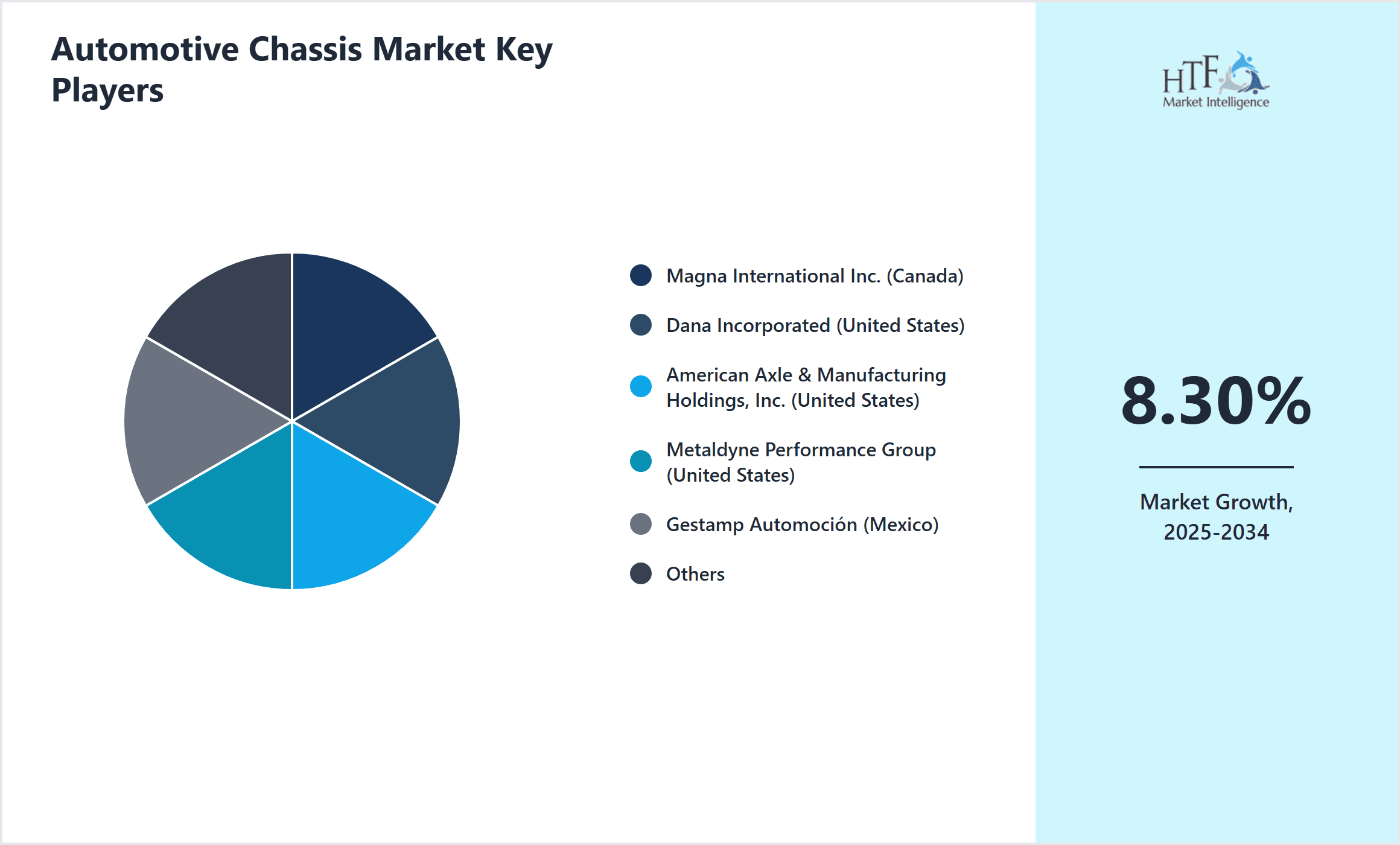

Leading Companies in Automotive Chassis Market

- •Magna International Inc. (Canada)

- •Dana Incorporated (United States)

- •American Axle & Manufacturing Holdings, Inc. (United States)

- •Metaldyne Performance Group (United States)

- •Gestamp Automoción (Mexico)

- •Tower International, Inc. (United States)

- •Linamar Corporation (Canada)

- •TRW Automotive Holdings Corp. (United States)

- •Martinrea International Inc. (Canada)

- •BorgWarner Inc. (United States)

- •Meritor, Inc. (United States)

- •Continental AG (United States - NA Operations)

- •ZF Friedrichshafen AG (United States - NA Operations)

- •Autoliv Inc. (United States)

- •Flex-N-Gate Corporation (United States)

- •Valeo SA (United States - NA Operations)

- •KYB Corporation (United States - NA Operations)

- •Hitachi Astemo, Ltd. (United States - NA Operations)

- •Adient plc (United States)

- •Faurecia S.A. (United States - NA Operations)

- •Nissin Kogyo Co., Ltd. (United States - NA Operations)

- •GKN Automotive (United States - NA Operations)

- •Brembo S.p.A. (United States - NA Operations)

- •Aisin Seiki Co., Ltd. (United States - NA Operations)

- •Schaeffler AG (United States - NA Operations)

Market Breakdown

- •By Product Type

- ◦Ladder Frame Chassis

- ◦Monocoque Chassis

- ◦Backbone Frame Chassis

- ◦Space Frame Chassis

- ◦Tubular Frame Chassis

- •By Application

- ◦Passenger Vehicles

- ◦Commercial Vehicles

- ◦Off-Highway Vehicles

- ◦Electric Vehicles

- ◦Autonomous Vehicles

- •By End-Use Industry

- ◦Automotive OEMs

- ◦Aftermarket

- ◦Fleet Operators

- ◦Agricultural & Construction Equipment

- •By Distribution Channel

- ◦Direct OEM Supply

- ◦Aftermarket Distribution

- ◦Tier 1 Supplier Networks

Growth Dynamics

The North America Automotive Chassis Market is driven by increasing demand for lightweight and fuel-efficient vehicles, which is pushing adoption of advanced materials such as aluminum and composites in chassis design. Government regulations on emissions and safety standards compel manufacturers to innovate chassis architectures that improve crashworthiness while reducing weight. Electric and autonomous vehicle market expansion necessitates new chassis platforms that accommodate battery packs and sensor arrays, fostering growth in space frame and tubular chassis types. The rise in commercial vehicle demand, supported by growing logistics and transportation sectors, further fuels chassis market expansion. Additionally, technological advancements in manufacturing processes such as automation and additive manufacturing enable cost-effective production of complex chassis components, enhancing market growth prospects.

Market Trends

A prominent trend in the North America Automotive Chassis Market is the increasing integration of lightweight materials including carbon fiber reinforced plastics and high-strength steel to achieve weight reduction targets without compromising durability. Another significant trend is the modular chassis design approach that allows flexibility across various vehicle platforms, reducing development costs and time-to-market. Electrification and autonomous vehicle technologies are driving chassis innovation towards accommodating batteries and sensor integration, leading to a surge in demand for space frame and tubular chassis types. Collaborative partnerships between OEMs and material technology providers are becoming common to accelerate innovation. Furthermore, digital twin and simulation technologies are being adopted for chassis design optimization to improve performance and safety outcomes.

Market Opportunities

Opportunities in the North America Automotive Chassis Market arise from the growing electric vehicle segment, which requires specialized chassis designs to integrate heavy battery packs safely and efficiently. Expansion of autonomous vehicle programs offers additional avenues for chassis innovation in sensor mounting and structural adaptation. Increasing aftermarket demand for chassis upgrades and replacement parts provides another lucrative segment for suppliers. Furthermore, emerging materials such as graphene composites present future growth potential through improved strength-to-weight ratios. Geographical expansion into growing automotive manufacturing hubs in Mexico offers cost advantages and new customer bases. Strategic collaborations between technology developers and chassis manufacturers also open pathways for co-innovation and market penetration.

Market Challenges

The North America Automotive Chassis Market faces challenges including high production costs associated with advanced lightweight materials and manufacturing processes, which can impact vehicle pricing. Supply chain disruptions, particularly in sourcing specialized raw materials such as carbon fiber and aluminum, present risks to production continuity. Regulatory compliance with evolving safety and environmental standards requires continuous investment in R&D, increasing operational costs. Intense competition from global and regional players drives pricing pressures and margin constraints. Additionally, the transition to electric and autonomous vehicles demands significant redesign of chassis platforms, creating technical complexities and longer development cycles. Market volatility due to economic fluctuations and raw material price instability also poses challenges to sustained growth.

Regulatory Framework

Between 2020 and 2025, North America has seen the implementation of enhanced safety regulations such as the Federal Motor Vehicle Safety Standards (FMVSS) updates mandating improved crashworthiness and occupant protection, directly impacting chassis design and testing requirements. Emission reduction policies including Corporate Average Fuel Economy (CAFE) standards have driven automotive manufacturers to pursue lightweight chassis solutions to improve fuel efficiency. Additionally, new regulations targeting electric vehicle safety, such as battery crash integrity and electrical isolation standards, require chassis adaptations. The evolving regulatory landscape also includes incentives for adopting sustainable materials and manufacturing processes, promoting innovation in chassis components. Compliance with these regulations necessitates close collaboration among OEMs, suppliers, and regulatory bodies to ensure market readiness and certification.

Market Intelligence

- •15th January 2025, Magna International Inc. unveiled a next-generation modular monocoque chassis platform designed specifically for electric vehicles, featuring integrated battery protection and enhanced lightweight aluminum structure. This innovation aims to improve vehicle range and safety, targeting leading EV manufacturers in North America. The platform supports scalable production across multiple vehicle segments and aligns with stricter regulatory mandates on emissions and crash safety. This launch positions Magna as a key technology leader in the evolving automotive chassis landscape.

- •10th March 2025, Dana Incorporated announced the commercial deployment of its advanced space frame chassis system optimized for autonomous commercial vehicles. The chassis incorporates smart sensor mounts and enhanced structural rigidity to support autonomous driving hardware. Dana's initiative is part of a strategic collaboration with major OEMs to accelerate adoption of autonomous transport solutions in North America. This development underscores the growing importance of tailored chassis architectures for emerging vehicle technologies.

- •20th July 2024, American Axle & Manufacturing Holdings, Inc. completed expansion of its manufacturing facility in Mexico to increase production capacity of lightweight ladder frame chassis components for commercial vehicles. This strategic move addresses rising demand in the logistics sector and leverages cost advantages in the region. The expanded facility is equipped with automated assembly lines and advanced quality control systems, enhancing operational efficiency and supply chain responsiveness.

- •5th November 2024, Gestamp Automoción introduced a new tubular frame chassis design that integrates carbon fiber composite reinforcements to reduce weight while maintaining structural integrity. Targeting electric and off-highway vehicles, this product aims to improve energy efficiency and durability. Gestamp's innovation reflects growing industry focus on material technology advancements to meet evolving customer and regulatory demands.

- •Source: Official Company Press Releases and Industry Publications

Regional Outlook

The United States currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Mexico is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- United States

- Canada

- Mexico

| Feature | Details |

|---|---|

| Base Year Market Size | USD 12.5 Billion |

| Forecast Year Market Size | USD 25.8 Billion |

| CAGR | 8.3% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7.9% |

| Scope of Report | Market is segmented by Product Type (Ladder Frame Chassis, Monocoque Chassis, Backbone Frame Chassis, Space Frame Chassis, Tubular Frame Chassis), Application (Passenger Vehicles, Commercial Vehicles, Off-Highway Vehicles, Electric Vehicles, Autonomous Vehicles), End-Use Industry (Automotive OEMs, Aftermarket, Fleet Operators, Agricultural & Construction Equipment), Distribution Channel (Direct OEM Supply, Aftermarket Distribution, Tier 1 Supplier Networks) |

| Regions Covered | United States, Canada, Mexico |

| Key Companies | Magna International Inc. (Canada), Dana Incorporated (United States), American Axle & Manufacturing Holdings, Inc. (United States), Metaldyne Performance Group (United States), Gestamp Automoción (Mexico), Tower International, Inc. (United States), Linamar Corporation (Canada), TRW Automotive Holdings Corp. (United States), Martinrea International Inc. (Canada), BorgWarner Inc. (United States), Meritor, Inc. (United States), Continental AG (United States - NA Operations), ZF Friedrichshafen AG (United States - NA Operations), Autoliv Inc. (United States), Flex-N-Gate Corporation (United States), Valeo SA (United States - NA Operations), KYB Corporation (United States - NA Operations), Hitachi Astemo, Ltd. (United States - NA Operations), Adient plc (United States), Faurecia S.A. (United States - NA Operations), Nissin Kogyo Co., Ltd. (United States - NA Operations), GKN Automotive (United States - NA Operations), Brembo S.p.A. (United States - NA Operations), Aisin Seiki Co., Ltd. (United States - NA Operations), Schaeffler AG (United States - NA Operations) |

North America Automotive Chassis Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.