Global Engine Water Pumps Market Size, Growth & Revenue 2024-2034

Global Engine Water Pumps Market is segmented by Product Type (Mechanical Water Pumps, Electrical Water Pumps, Centrifugal Water Pumps, Positive Displacement Water Pumps, Others), Application (Passenger Vehicles, Commercial Vehicles, Industrial Machinery, Agricultural Equipment, Marine), End-Use Industry (Automotive, Industrial, Agriculture, Marine & Shipping), Distribution Channel (OEM (Original Equipment Manufacturer), Aftermarket, Direct Sales), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global Engine Water Pumps market represents a critical segment within the automotive and industrial machinery industries, focusing on the production and supply of pumps designed to regulate engine temperature through efficient coolant circulation. This market spans various pump types including mechanical, electrical, centrifugal, and positive displacement variants, tailored to meet the cooling requirements of passenger vehicles, commercial trucks, agricultural machinery, marine vessels, and industrial equipment. Increasing demand for fuel-efficient and low-emission engines is driving innovation towards electrically powered water pumps, which offer enhanced control and energy saving. Geographically, North America leads with a mature automotive industry, while rapid industrialization and vehicle production growth in Asia-Pacific position it as the fastest-growing market. The market is shaped by OEM and aftermarket dynamics, stringent regulatory frameworks on emissions, and technological advancements focusing on smart pump systems integrated with vehicle electronics. Competitive strategies emphasize product differentiation, material innovation, and strategic partnerships to expand market share globally.

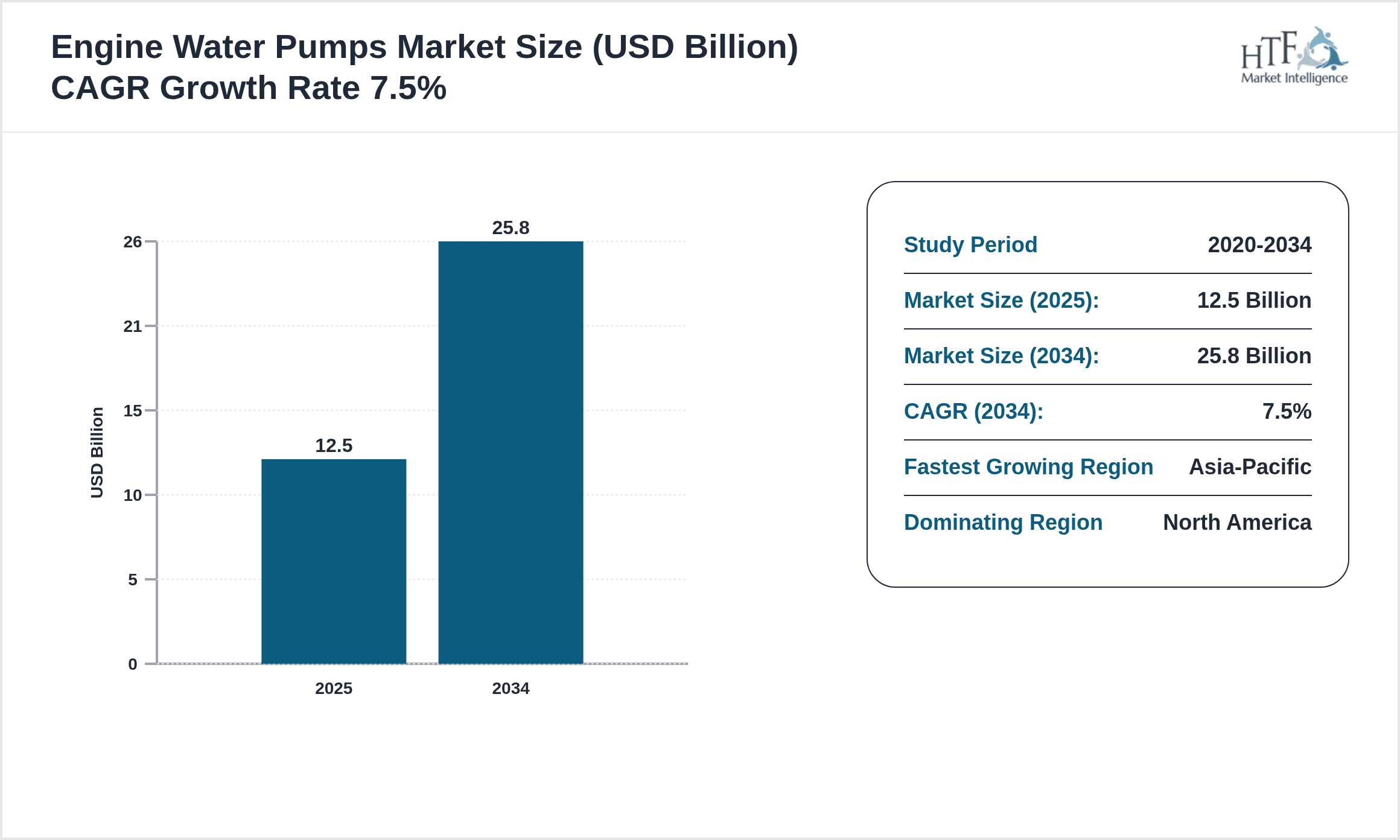

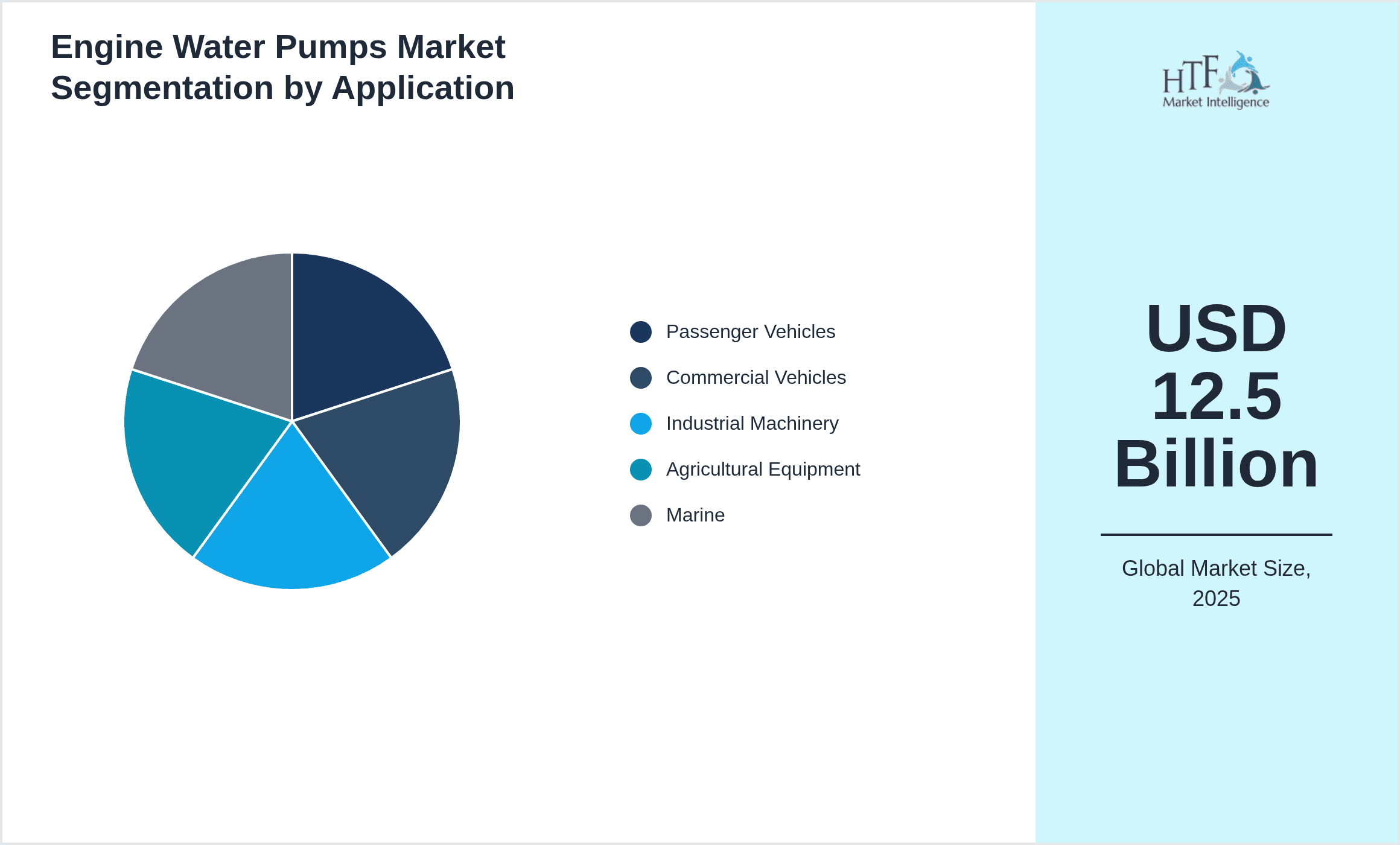

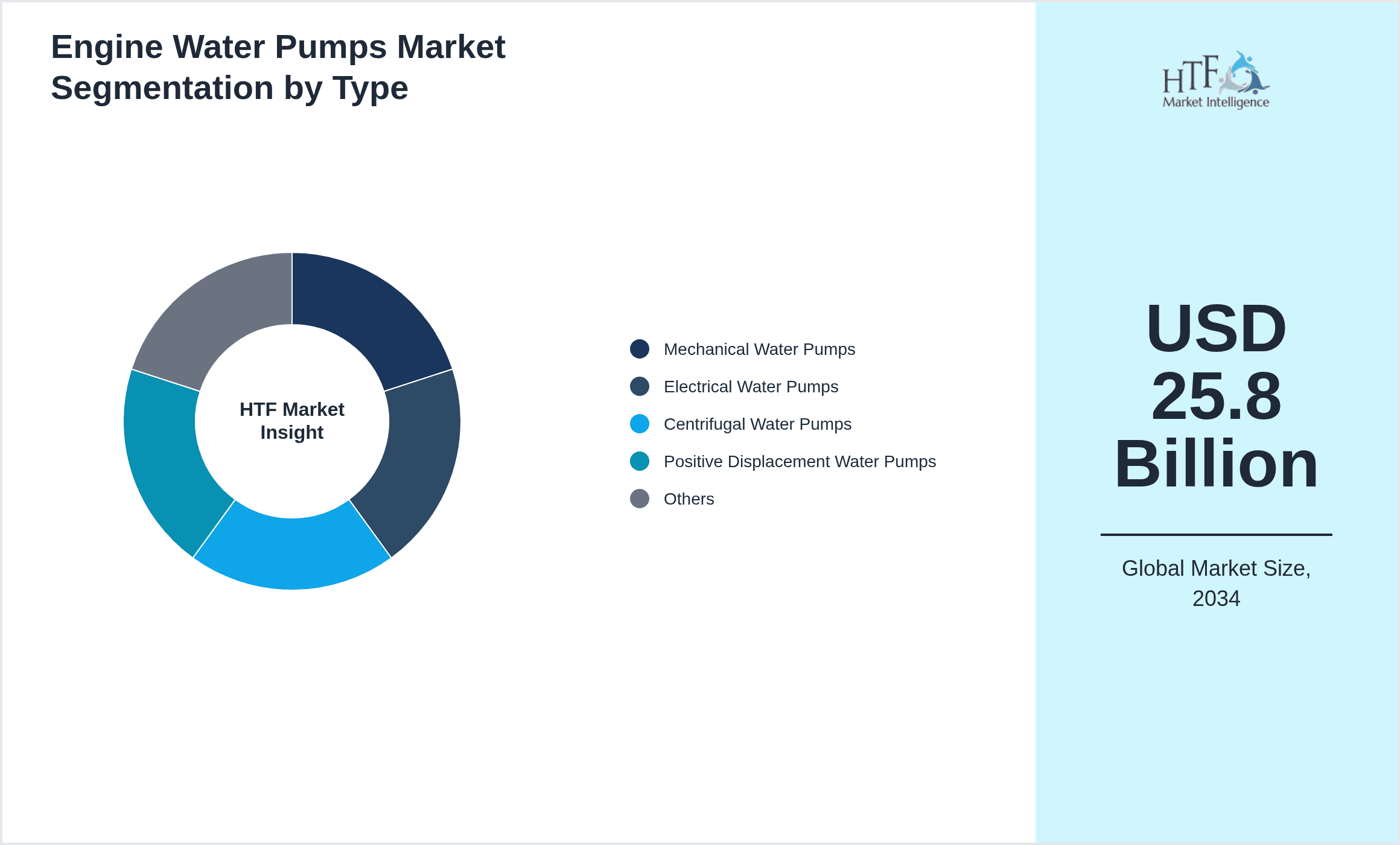

- •Key market highlights include a forecasted CAGR of 7.5% between 2024 and 2034, with the market expected to grow from USD 12.5 billion in 2024 to USD 25.8 billion by 2034. Mechanical water pumps currently dominate the market due to their widespread use in traditional combustion engines, but electrical water pumps are rapidly gaining traction due to their application in hybrid and electric vehicles. Passenger vehicles remain the largest application segment, followed closely by commercial vehicles and industrial machinery. North America commands the highest market share, benefiting from advanced automotive technologies and high aftermarket demand, whereas Asia-Pacific exhibits the highest growth rate driven by expanding vehicle production and modernization of industrial sectors. Market growth is propelled by rising automotive production, technological innovations, and increasing focus on sustainability and emissions reduction.

- •The engine water pumps market offers significant value propositions to automotive OEMs, aftermarket suppliers, and industrial machinery manufacturers by enabling enhanced engine efficiency, reliability, and compliance with environmental standards. Strategic importance lies in the integration of advanced pump technologies such as electrically controlled variable flow pumps that optimize coolant circulation based on engine load and temperature, thereby improving fuel economy and reducing emissions. Stakeholders benefit from opportunities in emerging markets where industrial growth and vehicle electrification are accelerating demand. Additionally, collaborations between pump manufacturers and automotive companies foster innovation in smart cooling systems, enhancing overall vehicle performance. The market's continuous evolution is vital for industries aiming to meet regulatory challenges while delivering cost-effective and high-performance engine cooling solutions globally.

Competitive Landscape

The global engine water pumps market is highly competitive, characterized by the presence of numerous multinational corporations and regional manufacturers striving for technological supremacy and market share. Competition revolves around continuous product innovation, cost optimization, and strategic alliances to broaden geographic presence and application segments. Leading players leverage advanced R&D capabilities to develop electric and hybrid-compatible pumps that meet stringent emission regulations and enhance fuel efficiency. Market rivalry also focuses on expanding aftermarket services and improving supply chain efficiency to reduce lead times and costs. Mergers and acquisitions play a pivotal role in consolidating market positions, enabling companies to access new technologies and customer bases. Pricing strategies vary by region, with developed markets emphasizing quality and performance, while emerging markets prioritize affordability and durability. The competitive dynamics drive rapid adoption of smart pump technologies, digital monitoring, and integration with vehicle electronics, shaping the future landscape of engine water pump solutions.

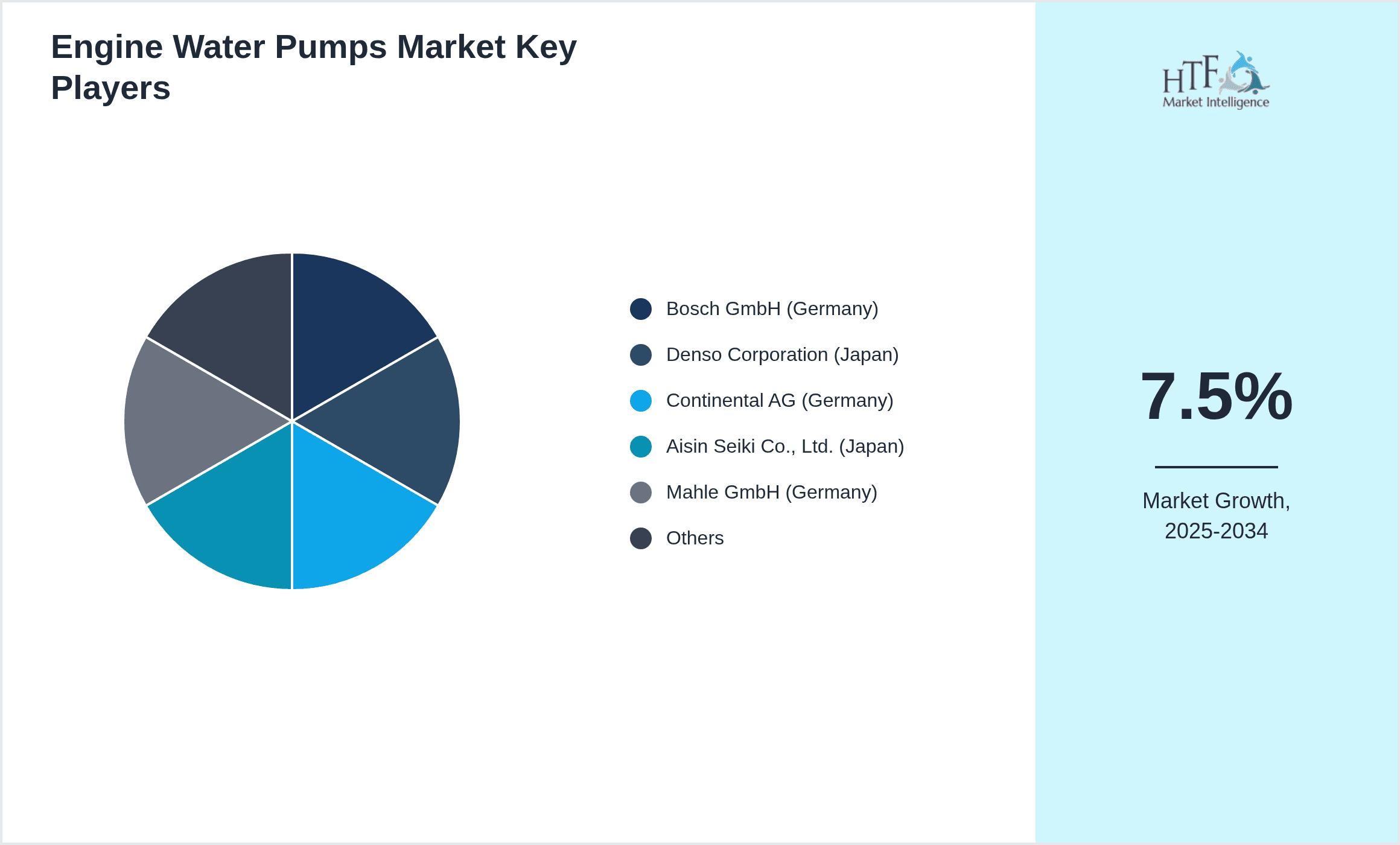

Leading Companies in Engine Water Pumps Market

- •Bosch GmbH (Germany)

- •Denso Corporation (Japan)

- •Continental AG (Germany)

- •Aisin Seiki Co., Ltd. (Japan)

- •Mahle GmbH (Germany)

- •Valeo SA (France)

- •Pierburg Pump Technology GmbH (Germany)

- •Gates Corporation (United States)

- •Mitsubishi Electric Corporation (Japan)

- •Hanon Systems (South Korea)

- •BorgWarner Inc. (United States)

- •SKF Group (Sweden)

- •Luzhou Water Pump Co., Ltd. (China)

- •Calsonic Kansei Corporation (Japan)

- •Modine Manufacturing Company (United States)

- •Hitachi Automotive Systems (Japan)

- •Thermo King Corporation (United States)

- •JTEKT Corporation (Japan)

- •SKF Automotive (Sweden)

- •Eaton Corporation (Ireland)

- •Valeo Thermal Systems (France)

- •Schaeffler Technologies AG & Co. KG (Germany)

- •Danfoss A/S (Denmark)

- •Magneti Marelli S.p.A. (Italy)

- •Nidec Corporation (Japan)

Market Breakdown

- •By Product Type

- ◦Mechanical Water Pumps

- ◦Electrical Water Pumps

- ◦Centrifugal Water Pumps

- ◦Positive Displacement Water Pumps

- ◦Others

- •By Application

- ◦Passenger Vehicles

- ◦Commercial Vehicles

- ◦Industrial Machinery

- ◦Agricultural Equipment

- ◦Marine

- •By End-Use Industry

- ◦Automotive

- ◦Industrial

- ◦Agriculture

- ◦Marine & Shipping

- •By Distribution Channel

- ◦OEM (Original Equipment Manufacturer)

- ◦Aftermarket

- ◦Direct Sales

Growth Dynamics

- •The increasing adoption of electric and hybrid vehicles globally is a significant growth driver for electrical engine water pumps, which offer enhanced efficiency and precise thermal management compared to mechanical variants. As governments enforce stricter emission norms, manufacturers are incentivized to integrate advanced cooling technologies that reduce fuel consumption and improve engine performance.

- •Rapid industrialization and expansion of the agricultural sector in emerging economies such as those in Asia-Pacific are driving demand for engine water pumps in industrial machinery and agricultural equipment segments. This growth is supported by increasing mechanization and modernization efforts in these regions.

- •Stringent environmental regulations worldwide require manufacturers to develop low-emission engines with optimized cooling systems, fostering innovation in pump designs and materials. This regulatory pressure accelerates market growth by promoting adoption of electric water pumps and smart cooling solutions.

- •Technological advancements such as electronically controlled variable flow pumps and integration with vehicle electronic control units (ECUs) are creating new growth avenues by enhancing system efficiency and enabling real-time thermal management, which is particularly crucial for electric and hybrid vehicles.

- •The expansion of aftermarket services and replacement demand in mature markets like North America and Europe contributes to steady revenue streams for engine water pump manufacturers, bolstering overall market growth.

- •Increasing investments in R&D by key players focusing on durable materials and corrosion-resistant coatings enhance the reliability and lifespan of water pumps, creating competitive advantages and driving market expansion.

- •Growth in the marine and shipping industries, driven by increasing global trade and demand for efficient engine cooling systems in vessels, opens additional opportunities for specialized engine water pumps adapted to harsh marine environments.

Market Trends

- •The transition towards electric and hybrid vehicles is fostering widespread adoption of electrical water pumps due to their ability to operate independently of engine speed, providing superior thermal management and energy savings. Companies are investing in developing compact, high-efficiency pump designs compatible with new powertrain architectures.

- •Integration of smart sensors and IoT connectivity in engine water pumps is emerging as a trend, enabling predictive maintenance and real-time monitoring of coolant flow and temperature, thereby reducing downtime and operational costs for vehicle fleets and industrial machinery.

- •Sustainability is influencing material selection, with manufacturers adopting eco-friendly and recyclable materials for pump components to reduce environmental impact and comply with global green initiatives.

- •Collaborations between automotive OEMs and pump manufacturers are intensifying to co-develop customized cooling solutions that optimize engine performance and comply with evolving emission standards, highlighting a trend towards deeper supply chain integration.

- •Emerging markets are witnessing increased demand for aftermarket engine water pumps due to rising vehicle parc and extended equipment lifecycles, driving companies to expand distribution networks and service offerings in these regions.

- •Advancements in additive manufacturing and 3D printing technologies are being explored for rapid prototyping and production of complex pump components, reducing lead times and enabling design flexibility.

- •The marine segment shows growing interest in specialized corrosion-resistant engine water pumps designed for saltwater environments, driven by increased regulatory focus on marine engine efficiency and emissions.

Market Opportunities

- •The rising electrification of vehicles offers substantial opportunities for manufacturers to develop advanced electrical water pumps tailored for hybrid and fully electric powertrains, which demand precise thermal regulation to maximize battery and motor performance.

- •Emerging regions such as Latin America and the Middle East & Africa present untapped markets with growing automotive production and industrialization, enabling expansion through localized manufacturing and distribution partnerships.

- •Innovation in smart cooling systems integrated with vehicle telematics is an opportunity to offer value-added services such as predictive maintenance and remote diagnostics, enhancing customer loyalty and creating new revenue streams.

- •Collaborative ventures between pump manufacturers and technology providers to develop IoT-enabled, energy-efficient engine water pumps can capture demand from fleet operators seeking operational cost reductions and sustainability compliance.

- •Growing demand for aftermarket replacement parts in mature markets creates opportunities for companies to expand product portfolios and service networks, focusing on high-quality, durable engine water pumps compatible with older vehicle models.

- •Development of corrosion-resistant and high-temperature tolerant materials presents a growth avenue for specialized applications in marine and heavy industrial machinery, where environmental conditions are challenging.

- •Investment in additive manufacturing for rapid prototyping and small-batch production can reduce costs and speed up innovation cycles, enabling companies to respond quickly to market demands and customization needs.

Market Challenges

- •High initial costs associated with electrical engine water pumps and advanced smart cooling systems restrict adoption in cost-sensitive markets, limiting growth potential in developing economies.

- •Stringent regulatory requirements and variability across regions create compliance complexities for manufacturers, necessitating significant investments in certification and testing processes.

- •Competition from low-cost regional manufacturers offering cheaper mechanical pumps poses challenges for global players in maintaining market share and pricing power, especially in emerging markets.

- •Supply chain disruptions and raw material price volatility, particularly for specialized metals and electronic components, impact production schedules and profitability margins across the industry.

- •Technical challenges related to integration of electrical water pumps with diverse vehicle electronic architectures require continuous R&D efforts, increasing development costs and time-to-market.

- •Limited consumer awareness about the benefits of advanced engine water pumps and reluctance to switch from traditional mechanical systems slow market penetration in certain regions.

- •Aftermarket fragmentation and lack of standardized replacement parts complicate service and warranty management, affecting customer satisfaction and brand loyalty.

Regulatory Framework

- •Between 2019 and 2024, multiple regions enacted stricter emission standards such as Euro 6 and EPA Tier 3, compelling engine manufacturers to optimize cooling systems, thus influencing engine water pump designs to meet thermal efficiency requirements.

- •Regulations mandating the reduction of fuel consumption and greenhouse gas emissions have driven the adoption of electrically driven water pumps, supported by government incentives in North America and Europe to promote clean vehicle technologies.

- •Safety standards for automotive components, including engine water pumps, have been updated to address durability and failure prevention, requiring compliance with ISO/TS 16949 quality management systems.

- •Country-specific mandates in Asia-Pacific emphasize localization of manufacturing and environmental compliance, influencing production processes and material sourcing for water pump manufacturers.

- •Government initiatives promoting electric vehicle adoption globally have indirectly impacted the market by accelerating the demand for advanced cooling technologies compatible with new powertrain configurations.

Market Intelligence

- •15th February 2025, Bosch GmbH launched a next-generation electrically driven engine water pump featuring integrated thermal management sensors and adaptive flow control, targeting hybrid and electric vehicles. This product aims to enhance energy efficiency by dynamically adjusting coolant flow based on real-time engine and battery temperature data, thereby improving vehicle range and reducing emissions. Bosch’s innovation underscores the ongoing shift towards electrification in engine cooling systems and positions the company as a leader in smart pump technology. Source: Bosch Official Press Release

- •10th April 2025, Denso Corporation introduced an advanced centrifugal water pump designed for heavy-duty commercial vehicles, incorporating corrosion-resistant materials and optimized impeller geometry to improve durability and cooling efficiency under extreme operating conditions. This launch supports Denso’s strategy to expand its presence in the commercial vehicle segment, particularly in emerging markets with growing logistics demands. The product's enhanced thermal performance contributes to lower engine wear and extended service intervals. Source: Denso News Portal

- •22nd July 2024, Continental AG announced a strategic partnership with a leading IoT solutions provider to develop connected engine water pumps with embedded sensors for predictive maintenance. This collaboration aims to enable real-time monitoring of pump health, reducing downtime and maintenance costs for fleet operators globally. By integrating IoT capabilities, Continental advances its portfolio towards Industry 4.0 standards, enhancing product value and customer service. Source: Continental Corporate News

- •5th November 2024, Valeo SA completed the acquisition of a specialty pump manufacturer to strengthen its thermal systems division and accelerate development of electric water pumps for next-generation electric vehicles. This acquisition enhances Valeo’s R&D capabilities and market reach, enabling quicker innovation cycles and broader product offerings tailored to evolving automotive cooling requirements. The move is aligned with Valeo’s strategic priorities of sustainability and technological leadership. Source: Valeo Press Release

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 12.5 Billion |

| Forecast Year Market Size | USD 25.8 Billion |

| CAGR | 7.5% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 7.2% |

| Scope of Report | Market is segmented by Product Type (Mechanical Water Pumps, Electrical Water Pumps, Centrifugal Water Pumps, Positive Displacement Water Pumps, Others), Application (Passenger Vehicles, Commercial Vehicles, Industrial Machinery, Agricultural Equipment, Marine), End-Use Industry (Automotive, Industrial, Agriculture, Marine & Shipping), Distribution Channel (OEM (Original Equipment Manufacturer), Aftermarket, Direct Sales) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Bosch GmbH (Germany), Denso Corporation (Japan), Continental AG (Germany), Aisin Seiki Co., Ltd. (Japan), Mahle GmbH (Germany), Valeo SA (France), Pierburg Pump Technology GmbH (Germany), Gates Corporation (United States), Mitsubishi Electric Corporation (Japan), Hanon Systems (South Korea), BorgWarner Inc. (United States), SKF Group (Sweden), Luzhou Water Pump Co., Ltd. (China), Calsonic Kansei Corporation (Japan), Modine Manufacturing Company (United States), Hitachi Automotive Systems (Japan), Thermo King Corporation (United States), JTEKT Corporation (Japan), SKF Automotive (Sweden), Eaton Corporation (Ireland), Valeo Thermal Systems (France), Schaeffler Technologies AG & Co. KG (Germany), Danfoss A/S (Denmark), Magneti Marelli S.p.A. (Italy), Nidec Corporation (Japan) |

Global Engine Water Pumps Market Size, Growth & Revenue 2024-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.