Global High-end Furniture Market Size, Growth & Revenue 2025-2034

Global High-end Furniture Market is segmented by Product Type (Wooden Furniture, Metal Furniture, Upholstered Furniture, Glass Furniture, Mixed Material Furniture), Application (Residential, Commercial, Hospitality, Office, Luxury Retail), End-Use Industry (Luxury Residential, Hospitality & Tourism, Corporate Offices, Retail & Showrooms), Distribution Channel (Direct Sales, Retail Stores, E-commerce), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global high-end furniture market refers to the industry segment focused on producing and distributing premium furniture products characterized by exceptional design, quality materials, and superior craftsmanship. This market serves diverse applications such as residential homes, commercial buildings, hospitality venues including luxury hotels and resorts, office environments, and luxury retail outlets. High-end furniture products encompass a variety of types including wooden, metal, upholstered, glass, and mixed material furniture that appeal to affluent consumers seeking exclusivity and durability. The market value chain begins with raw material procurement, followed by design, manufacturing, branding, marketing, and distribution through both traditional retail outlets and digital platforms. Key market drivers include increasing urbanization, rising disposable incomes, and a growing preference for luxury interiors across emerging and developed economies. The market is also shaped by trends such as customization, sustainable production, and integration of smart furniture solutions. End users range from affluent individual consumers to corporate clients in hospitality, retail, and office sectors, each demanding distinct design and functionality features. The global market's evolution is influenced by socio-economic factors, technological advancements, and shifting consumer lifestyles, positioning high-end furniture as a significant segment within the broader furniture industry.

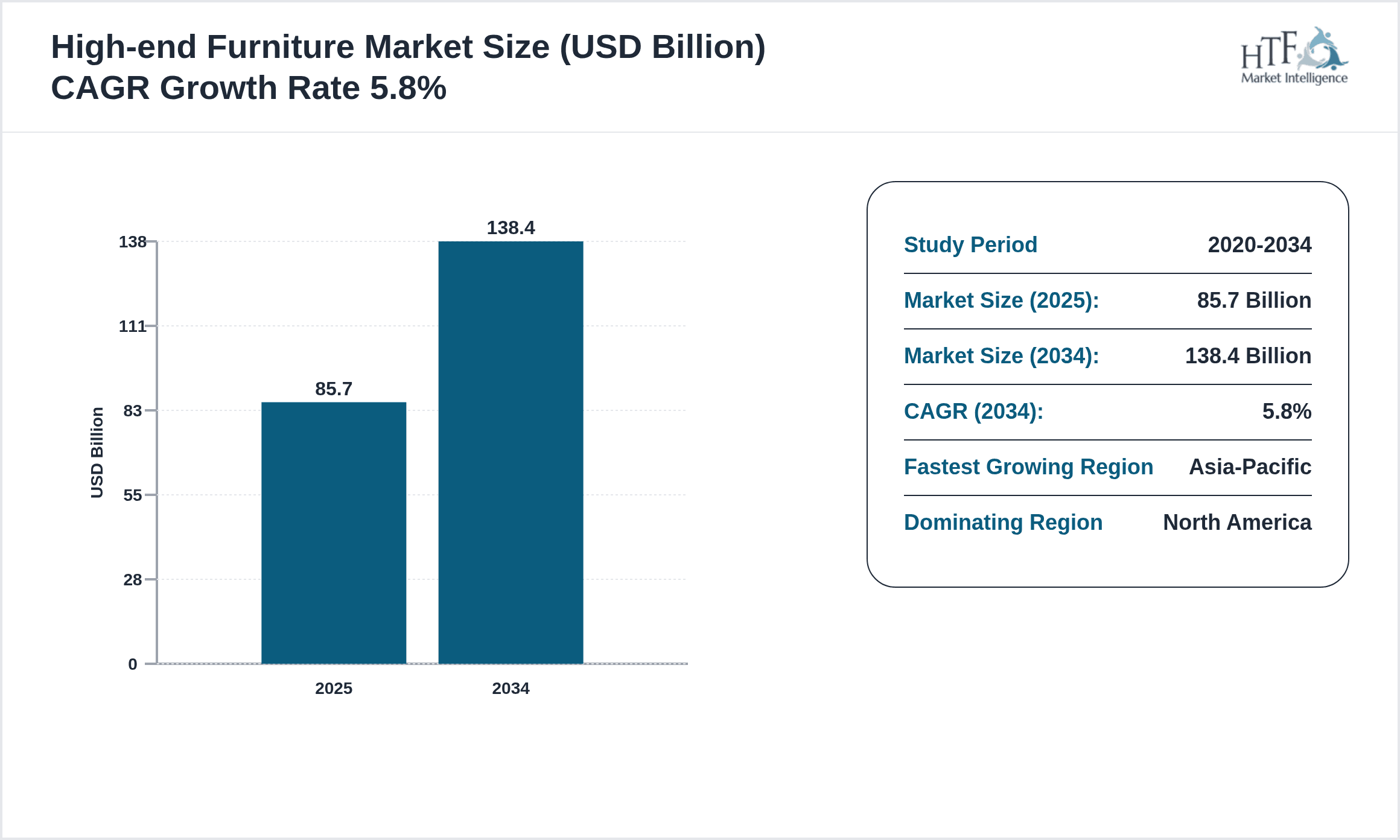

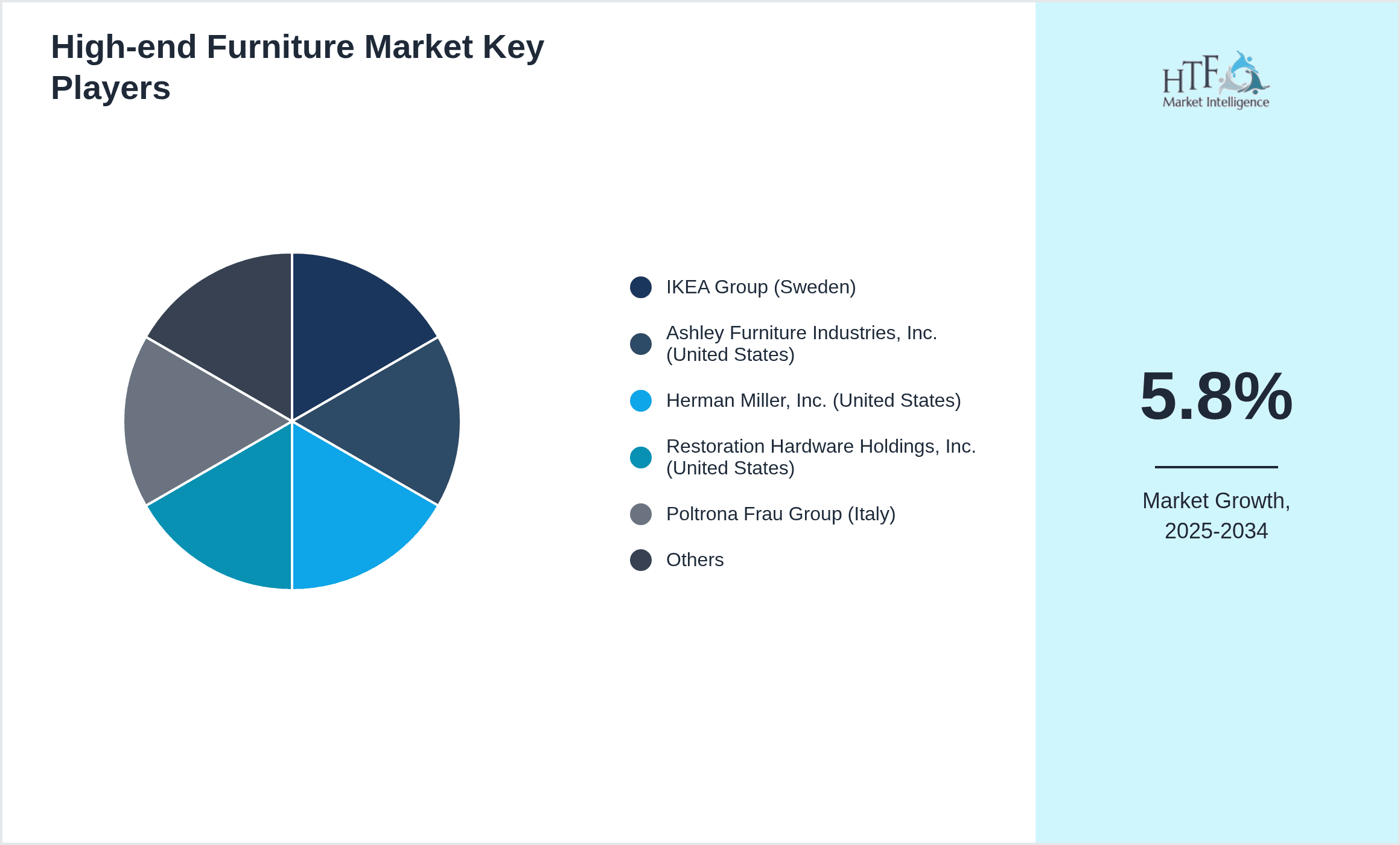

- •The market has demonstrated robust growth with a base market size of USD 85.7 Billion in 2025, expanding to an expected USD 138.4 Billion by 2034 at a CAGR of 5.8%. Key highlights include sustained demand from emerging markets in Asia-Pacific and increasing investments in luxury hospitality projects worldwide. The segment for wooden furniture currently leads in market share, while mixed material furniture is witnessing the fastest growth due to its innovative appeal and design versatility. The North American region dominates the market owing to high consumer purchasing power and a mature luxury furniture ecosystem. Asia-Pacific is the fastest-growing region driven by rapid urbanization, increasing affluent population, and rising interest in premium interior design.

- •High-end furniture plays a pivotal role in enhancing the aesthetic and functional value of living and working spaces, making it a strategic investment for residential buyers, commercial enterprises, and hospitality sectors. The market's value proposition lies in offering unique, high-quality products that combine artful design with comfort and durability. Stakeholders including manufacturers, designers, distributors, and retailers benefit from the growing demand for luxury furnishings as consumer preferences shift towards personalized and sustainable products. The industry's growth contributes to employment, innovation, and the promotion of craftsmanship traditions globally, while also aligning with trends in smart homes and eco-friendly materials.

Competitive Landscape

The global high-end furniture market is characterized by intense competition among established luxury furniture manufacturers and emerging boutique brands. Market dynamics are influenced by product innovation, brand reputation, and the ability to cater to evolving consumer preferences for bespoke designs and sustainable materials. Competitive strategies include strategic partnerships with designers and architects, expansion of distribution networks including e-commerce platforms, and investment in R&D to integrate smart functionalities. Market leaders leverage their global presence and supply chain efficiencies to maintain pricing power while smaller players focus on niche segments and customization. Mergers and acquisitions serve as a consolidation mechanism allowing companies to expand product portfolios and geographic footprints. Pricing strategies balance exclusivity with value, targeting affluent consumers willing to invest in quality and design. Distribution channels vary from high-end retail stores to online luxury marketplaces, enabling broad accessibility. Technological adoption in manufacturing and digital marketing enhances customer engagement and operational efficiency. Regional competition varies with North America exhibiting mature market traits, while Asia-Pacific shows rapid innovation and market entry by new players. Future trends suggest increased emphasis on sustainability, digital customization tools, and experiential retail formats shaping competitive positioning.

Key Players in High-end Furniture Market

- •IKEA Group (Sweden)

- •Ashley Furniture Industries, Inc. (United States)

- •Herman Miller, Inc. (United States)

- •Restoration Hardware Holdings, Inc. (United States)

- •Poltrona Frau Group (Italy)

- •Natuzzi S.p.A. (Italy)

- •HNI Corporation (United States)

- •La-Z-Boy Incorporated (United States)

- •Flexform S.p.A. (Italy)

- •B&B Italia S.p.A. (Italy)

- •Duresta Upholstery Ltd. (United Kingdom)

- •RH Modern (United States)

- •Bang & Olufsen A/S (Denmark)

- •Ligne Roset (France)

- •Knoll, Inc. (United States)

- •Muji (Japan)

- •Carl Hansen & Søn (Denmark)

- •Roche Bobois (France)

- •Fendi Casa (Italy)

- •Minotti S.p.A. (Italy)

- •Vitra AG (Switzerland)

- •Baker Furniture LLC (United States)

- •Ethan Allen Interiors Inc. (United States)

- •Simmons Furniture Company, Inc. (United States)

- •Hülsta-Werke Hüls GmbH & Co KG (Germany)

Market Breakdown

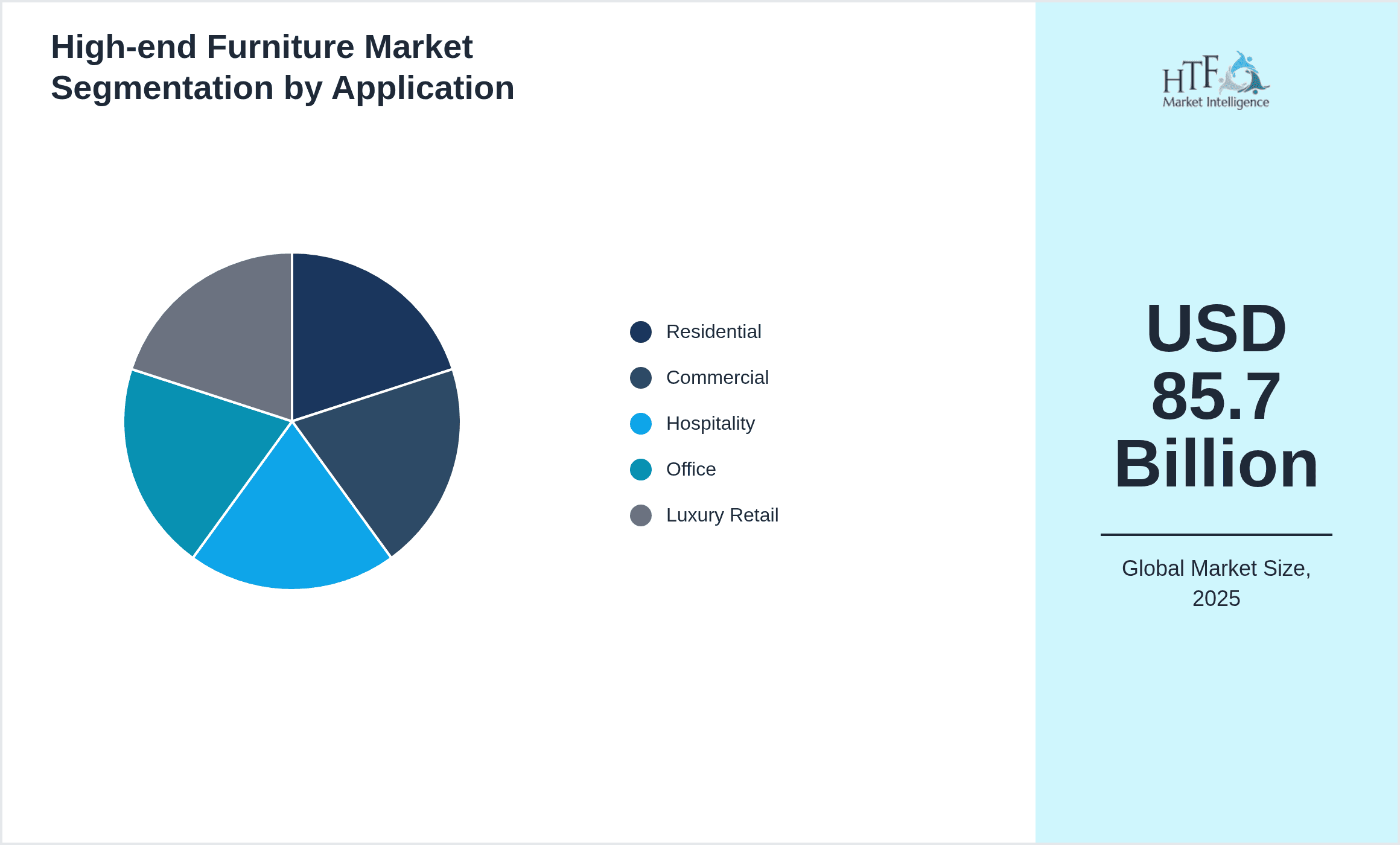

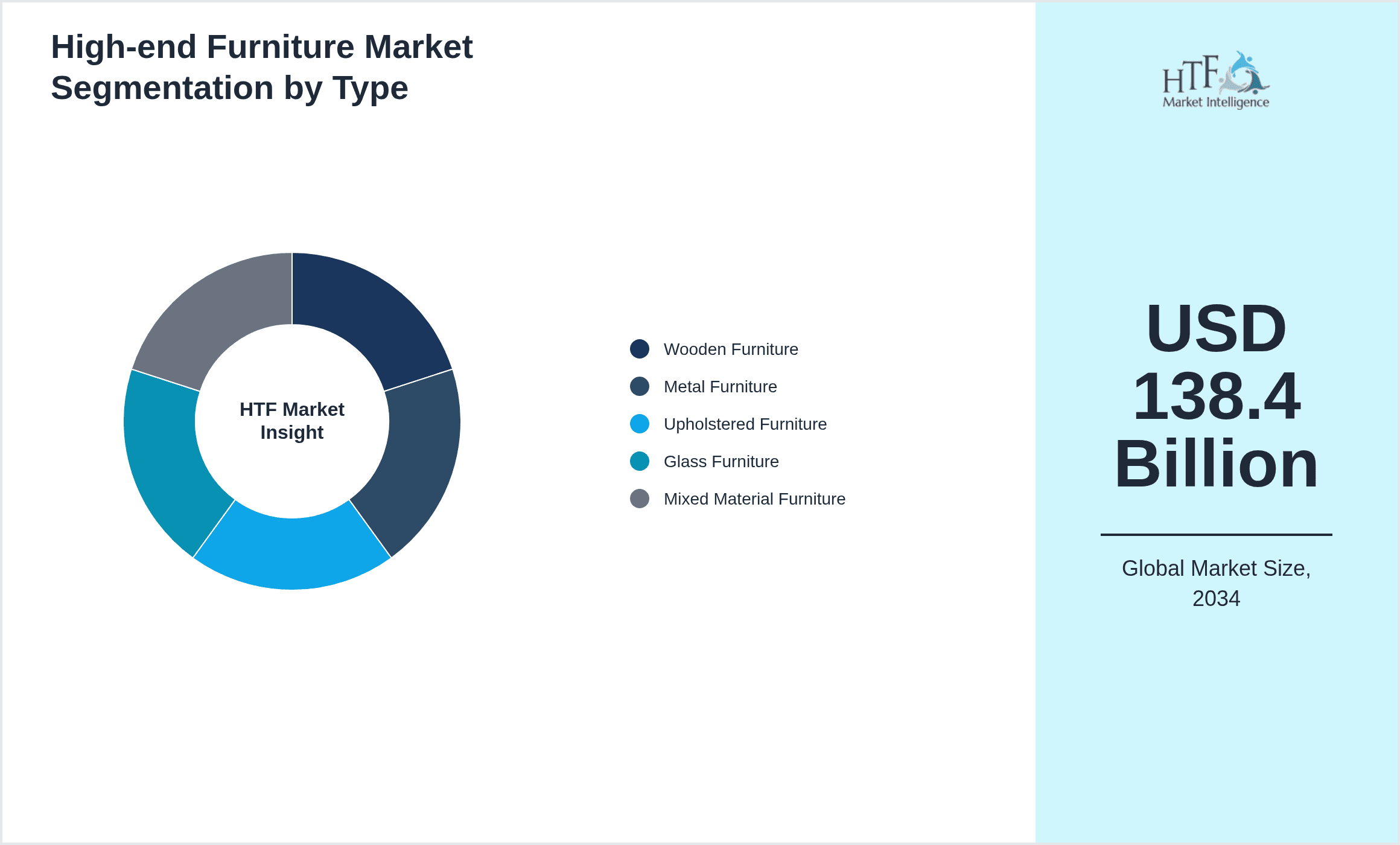

- •By Product Type

- ◦Wooden Furniture

- ◦Metal Furniture

- ◦Upholstered Furniture

- ◦Glass Furniture

- ◦Mixed Material Furniture

- •By Application

- ◦Residential

- ◦Commercial

- ◦Hospitality

- ◦Office

- ◦Luxury Retail

- •By End-Use Industry

- ◦Luxury Residential

- ◦Hospitality & Tourism

- ◦Corporate Offices

- ◦Retail & Showrooms

- •By Distribution Channel

- ◦Direct Sales

- ◦Retail Stores

- ◦E-commerce

Growth Dynamics

- •Rising disposable incomes and increasing urbanization in emerging markets such as Asia-Pacific are driving the demand for high-end furniture, as affluent consumers seek premium products to enhance their living spaces. This dynamic fuels market expansion through both residential and commercial sectors.

- •The shift towards sustainable and eco-friendly furniture materials is catalyzing growth, as consumers and businesses prioritize environmental responsibility. Manufacturers adopting sustainable sourcing and production methods gain competitive advantage and appeal to conscious buyers.

- •Technological advancements including digital customization platforms and smart furniture integration allow manufacturers to meet personalized demands efficiently, thereby boosting customer engagement and expanding market reach globally.

- •Expansion of the luxury hospitality and retail sectors worldwide is increasing demand for premium furniture solutions that combine aesthetics with functionality, creating new revenue streams for market participants.

- •E-commerce growth facilitates wider accessibility to high-end furniture products, enabling brands to reach global customers directly and reduce dependence on traditional retail channels.

- •Investment in design innovation and collaborations with renowned designers enhances product portfolios and brand prestige, fueling market growth through differentiation and consumer appeal.

- •Government incentives promoting manufacturing modernization and export facilitation in key markets support capacity expansion and international trade, positively influencing the market trajectory.

Market Trends

- •Integration of smart technologies into furniture, such as embedded wireless charging and IoT-enabled features, is transforming the high-end furniture landscape by offering enhanced functionality and user convenience.

- •Customization and bespoke furniture offerings are gaining traction, with companies leveraging digital visualization tools to provide personalized design experiences and meet unique consumer tastes.

- •Sustainability remains a key trend, with increased use of recycled and renewable materials alongside certifications to attract environmentally conscious consumers and comply with regulations.

- •Luxury furniture brands are expanding omnichannel retail strategies, combining physical boutique stores with immersive online platforms to enhance customer engagement and sales conversion.

- •Collaborations between furniture makers and high-profile designers or artists create limited-edition collections that drive brand exclusivity and consumer interest.

- •Increasing preference for minimalist and multifunctional furniture designs aligns with urban living trends and space optimization demands in metropolitan areas.

- •Emergence of virtual reality (VR) and augmented reality (AR) tools helps customers visualize furniture in their spaces prior to purchase, reducing return rates and improving satisfaction.

Market Opportunities

- •Expanding markets in Asia-Pacific and Latin America present untapped potential for high-end furniture companies to establish brand presence and capture growing luxury consumer bases.

- •Development of eco-friendly and smart furniture lines offers innovation opportunities to meet rising consumer demand for sustainability and technology integration.

- •Digital transformation and enhanced e-commerce capabilities enable brands to penetrate new geographic markets and demographic segments with tailored marketing strategies.

- •Strategic partnerships with luxury real estate developers and hospitality chains create avenues for bulk contracts and co-branded collections.

- •Investment in after-sales services such as customization, maintenance, and refurbishment enhances customer loyalty and recurring revenue streams.

- •Leveraging augmented reality and virtual reality for customer experience elevates engagement and reduces purchase hesitation, fostering higher conversion rates.

- •Increasing demand for multifunctional and space-saving furniture in urban centers opens innovative design opportunities for market expansion.

Market Challenges

- •High production and material costs limit market accessibility and pose profitability challenges, especially for smaller manufacturers competing with established luxury brands.

- •Supply chain disruptions, including raw material shortages and logistics constraints, affect product availability and delivery timelines, impacting customer satisfaction.

- •Intense competition from counterfeit and low-cost furniture brands undermines market integrity and affects premium brand positioning.

- •Regulatory compliance across diverse regions, including sustainability certifications and safety standards, adds complexity and cost to market operations.

- •Changing consumer preferences require continuous innovation and agility, challenging manufacturers to keep pace while maintaining quality standards.

- •Limited skilled labor availability in craftsmanship and design disciplines impacts production quality and innovation capacity.

- •Economic volatility and geopolitical tensions may constrain luxury spending and disrupt global trade flows, affecting market stability.

Regulatory Framework

- •The European Union's Timber Regulation (EUTR) implemented between 2013 and 2025 mandates due diligence to prevent illegally harvested timber in furniture products, significantly impacting sourcing practices globally.

- •The U.S. Consumer Product Safety Improvement Act (CPSIA) enacted in 2008 and updated through 2020-2025 imposes stringent safety standards on furniture materials and manufacturing processes, ensuring consumer protection and influencing market compliance.

- •China's Green Product Certification program introduced in 2017 and reinforced through 2025 encourages sustainable furniture production by setting environmental performance benchmarks, stimulating eco-friendly market growth.

- •The California Air Resources Board (CARB) formaldehyde emission standards, effective since 2012 and updated through 2023, regulate emissions from composite wood products, affecting furniture manufacturers supplying the U.S. market.

- •Government initiatives in countries like Germany and Japan between 2015 and 2025 promote circular economy models and furniture recycling programs, fostering sustainability and innovation within the industry.

Market Intelligence

- •15th March 2025, IKEA Group launched its new sustainable high-end furniture collection featuring products made from 100% recycled materials and incorporating modular designs for enhanced customization. This initiative targets eco-conscious consumers globally and aims to strengthen IKEA's position in the premium furniture segment by combining sustainability with affordability. The collection includes wooden and mixed material furniture designed to meet modern luxury aesthetics while reducing environmental impact, aligning with global sustainability trends. IKEA plans to expand availability across its key markets in North America, Europe, and Asia-Pacific by late 2025. Source: Official IKEA Press Release

- •10th July 2025, Restoration Hardware Holdings, Inc. introduced an innovative line of smart furniture integrating wireless charging, embedded sensors, and app-controlled lighting. Targeting luxury residential and hospitality customers, this product launch exemplifies the convergence of technology and design in the high-end furniture market. The smart furniture range enables enhanced user experience through connectivity and customization, positioning Restoration Hardware as a market innovator. The company forecasts significant uptake in North America and Europe, anticipating increased adoption driven by smart home trends. Source: Company Website Announcement

- •22nd September 2025, Poltrona Frau Group announced a strategic partnership with a renowned Italian designer to create limited-edition bespoke furniture collections. This collaboration aims to capitalize on the growing demand for personalized luxury furniture and strengthen Poltrona Frau's brand exclusivity. The initiative includes co-branded marketing campaigns and exclusive retail experiences in flagship stores across Europe and Asia-Pacific. The partnership is expected to enhance the company’s competitive positioning and open new revenue streams in premium market segments. Source: Industry Publication - Furniture Today

- •30th November 2024, Natuzzi S.p.A. completed the acquisition of a boutique sustainable furniture manufacturer specializing in recycled and reclaimed materials. This acquisition expands Natuzzi’s eco-friendly product portfolio and reinforces its commitment to sustainability. The deal is anticipated to enhance Natuzzi’s market share in Europe and North America, responding to increasing consumer demand for green products. Integration plans include leveraging the acquired company's design expertise and distribution channels to accelerate growth. Source: Official Natuzzi Corporate Announcement

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 85.7 Billion |

| Forecast Year Market Size | USD 138.4 Billion |

| CAGR | 5.8% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 5.7% |

| Scope of Report | Market is segmented by Product Type (Wooden Furniture, Metal Furniture, Upholstered Furniture, Glass Furniture, Mixed Material Furniture), Application (Residential, Commercial, Hospitality, Office, Luxury Retail), End-Use Industry (Luxury Residential, Hospitality & Tourism, Corporate Offices, Retail & Showrooms), Distribution Channel (Direct Sales, Retail Stores, E-commerce) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | IKEA Group (Sweden), Ashley Furniture Industries, Inc. (United States), Herman Miller, Inc. (United States), Restoration Hardware Holdings, Inc. (United States), Poltrona Frau Group (Italy), Natuzzi S.p.A. (Italy), HNI Corporation (United States), La-Z-Boy Incorporated (United States), Flexform S.p.A. (Italy), B&B Italia S.p.A. (Italy), Duresta Upholstery Ltd. (United Kingdom), RH Modern (United States), Bang & Olufsen A/S (Denmark), Ligne Roset (France), Knoll, Inc. (United States), Muji (Japan), Carl Hansen & Søn (Denmark), Roche Bobois (France), Fendi Casa (Italy), Minotti S.p.A. (Italy), Vitra AG (Switzerland), Baker Furniture LLC (United States), Ethan Allen Interiors Inc. (United States), Simmons Furniture Company, Inc. (United States), Hülsta-Werke Hüls GmbH & Co KG (Germany) |

Global High-end Furniture Market Size, Growth & Revenue 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is projected to grow at a CAGR of 6.8% from 2025 to 2030, driven by increasing demand in construction and agricultural sectors.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.