Global FRP GRP GRE Pipe Market Size, Growth & Revenue 2025-2034

Global FRP GRP GRE Pipe Market is segmented by Product Type (Filament Wound Pipes, Centrifugally Cast Pipes, Pultruded Pipes, Molded Pipes, Hand Lay-Up Pipes), Application (Water Supply, Oil & Gas, Chemical Processing, Construction, Power Generation), End-Use Industry (Municipal Water Systems, Oil & Gas Industry, Chemical Manufacturing, Infrastructure & Construction), Distribution Channel (Direct Sales, Distributors, Project-Based Tenders), and Geography (North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA)

Pricing

Report Overview

Executive Summary

- •The global FRP, GRP, and GRE pipe market is characterized by the manufacturing and application of composite pipes primarily used across water supply, oil and gas, chemical processing, construction, and power generation sectors. These pipes are manufactured using advanced technologies including filament winding, centrifugal casting, pultrusion, molding, and hand lay-up techniques, each offering specific mechanical and chemical advantages. Due to their superior corrosion resistance, lightweight nature, and high strength-to-weight ratio, FRP/GRP/GRE pipes are increasingly replacing traditional materials such as steel, concrete, and ductile iron pipes in demanding industrial environments. The market growth is further supported by expanding infrastructure projects, rising environmental concerns favoring sustainable materials, and increasing regulatory mandates on pipeline safety and durability. Asia-Pacific leads in rapid adoption propelled by industrialization and urbanization, while North America represents the largest market by revenue driven by mature infrastructure replacement and retrofit activities. Key trends include integration of smart sensor technologies for pipeline monitoring and innovations in resin chemistries to enhance performance under extreme conditions. The market outlook anticipates robust growth through 2034, fueled by increased investment in oil & gas exploration, water management projects, and chemical processing plants worldwide.

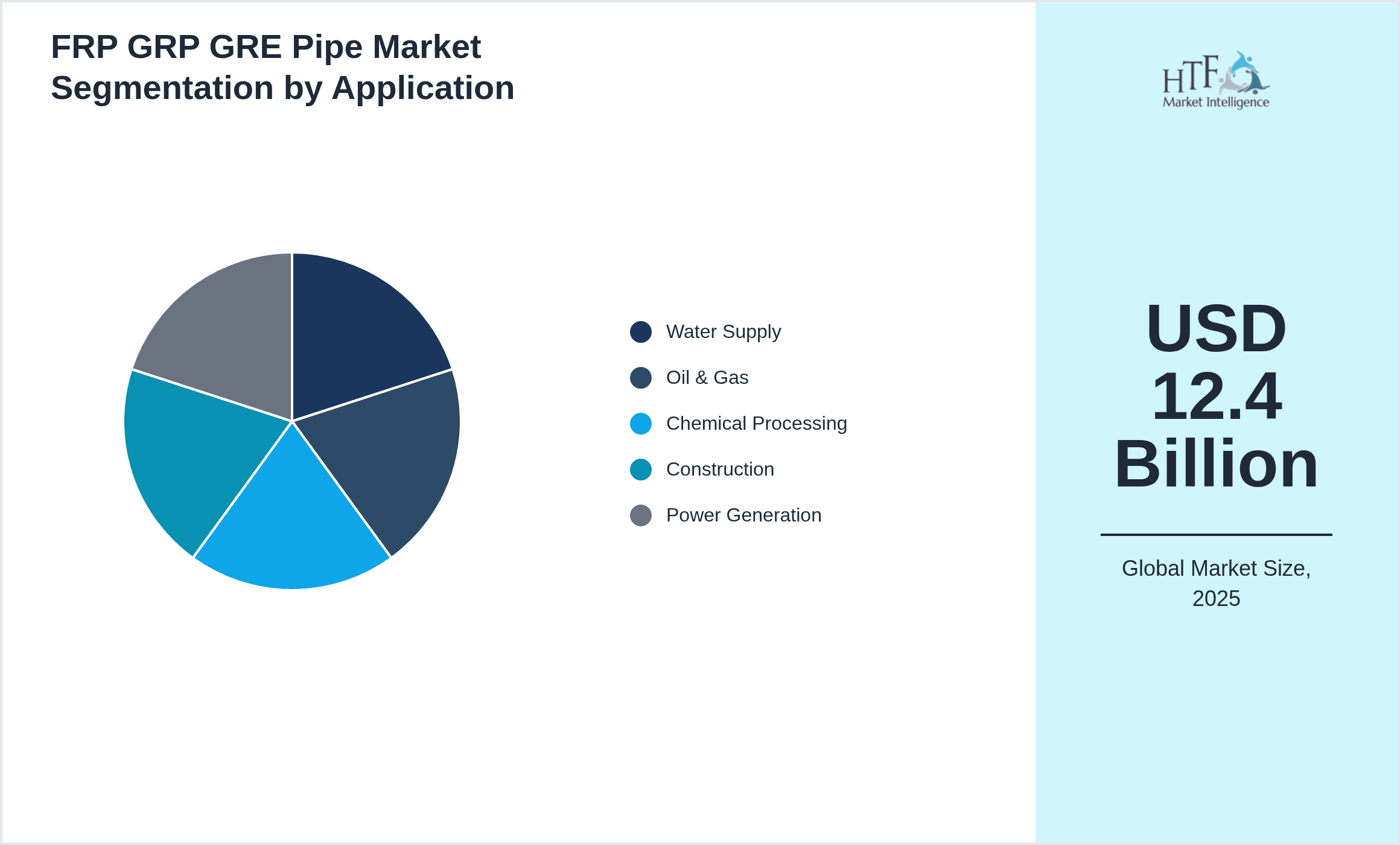

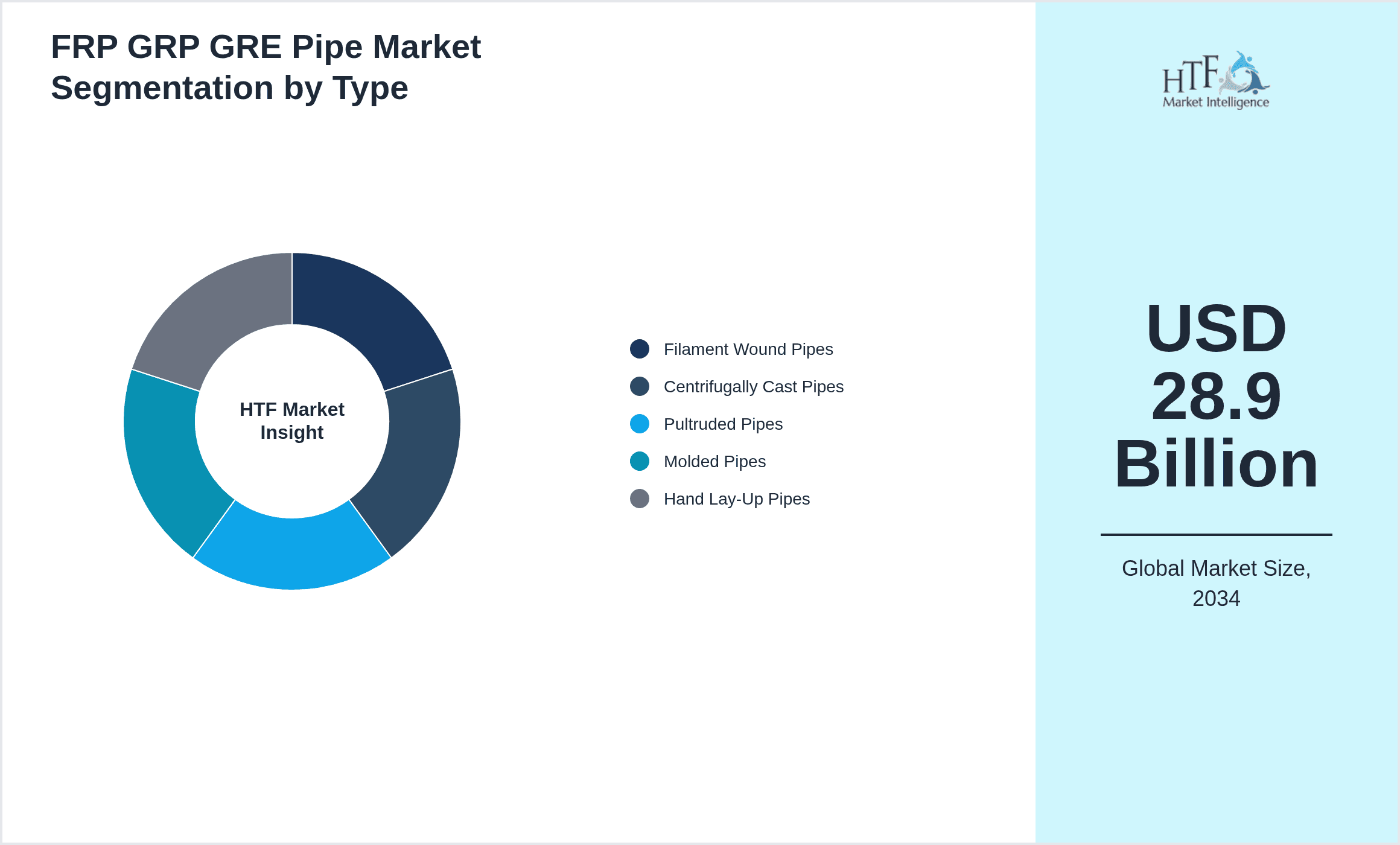

- •Significant market highlights encompass the expected growth at a compound annual growth rate (CAGR) of 9.2% from USD 12.4 billion in 2025 to USD 28.9 billion by 2034, reflecting strong demand across all major regions. North America dominates the market in revenue share due to stringent regulatory frameworks and focus on infrastructure modernization, while Asia-Pacific exhibits the fastest growth driven by rapid industrialization and large-scale urban water projects. Filament wound pipes remain the leading product type given their versatility and strength, whereas pultruded pipes demonstrate the fastest growth due to ease of manufacturing and cost-effectiveness. The market exhibits increasing consolidation with strategic partnerships and technological collaborations enhancing product offerings and geographical reach. Challenges such as high initial costs and technical skill requirements persist but are progressively mitigated by innovation and economies of scale.

- •The value proposition of FRP, GRP, and GRE pipes lies in their capacity to offer durable, corrosion-resistant, and lightweight solutions essential for modern infrastructure and industrial applications. Their strategic importance spans water conservation efforts, safer hydrocarbon transport, and chemical process integrity, making them indispensable to stakeholders including utilities, oil and gas operators, construction firms, and governments. The market delivers sustainable benefits by reducing carbon footprints through longer service life and lower maintenance needs compared to metallic alternatives. Continuous advancements in composite materials and manufacturing techniques are expected to unlock new application areas and enhance market penetration, further solidifying the pipes' role in future infrastructure development globally.

Competitive Landscape

The competitive environment in the global FRP GRP GRE pipe market is marked by intense rivalry among established players and emerging manufacturers striving to capitalize on growing demand across multiple industries. Market leaders are leveraging a combination of product innovation, strategic partnerships, and geographic expansion to strengthen their market positions. Companies invest heavily in research and development to improve resin formulations, enhance mechanical properties, and integrate smart monitoring technologies for predictive maintenance. Pricing strategies vary by region and product complexity, with premium offerings targeting high-end industrial applications and cost-effective solutions addressing emerging markets. Distribution channels include direct sales, distributors, and project-based tenders, with digital platforms increasingly facilitating order management and customer engagement. Barriers to entry include high capital investment for advanced manufacturing capabilities and stringent certification requirements, which protect incumbents. Regional competition is influenced by local regulatory compliance and availability of raw materials. The market is expected to witness consolidation through mergers and acquisitions, facilitating technology sharing and broader customer access, with competitive dynamics evolving towards sustainability and digitalization in pipeline infrastructure solutions.

Prominent Players in FRP GRP GRE Pipe Market

- •Aegion Corporation (United States)

- •Saint-Gobain PAM (France)

- •Johns Manville (United States)

- •Amiblu Holding GmbH (Austria)

- •Jushi Group Co., Ltd. (China)

- •Reinforced Plastic Systems (United States)

- •Kembla Advanced Composites (Australia)

- •Future Pipe Industries (United Arab Emirates)

- •LyondellBasell Industries (Netherlands)

- •Lanxess AG (Germany)

- •Georgia-Pacific LLC (United States)

- •Simona AG (Germany)

- •Trelleborg AB (Sweden)

- •Nordion Polymers Pvt. Ltd. (India)

- •Zhejiang Jinggong Science & Technology Co., Ltd. (China)

- •Pipelife International GmbH (Austria)

- •National Oilwell Varco, Inc. (United States)

- •Hexcel Corporation (United States)

- •Owens Corning (United States)

- •SGL Carbon SE (Germany)

- •Mitsubishi Chemical Corporation (Japan)

- •Saint-Gobain Performance Plastics (France)

- •Asahi Glass Co., Ltd. (Japan)

- •Owens Corning (United States)

- •CETCO (United States)

Market Breakdown

- •By Product Type

- ◦Filament Wound Pipes

- ◦Centrifugally Cast Pipes

- ◦Pultruded Pipes

- ◦Molded Pipes

- ◦Hand Lay-Up Pipes

- •By Application

- ◦Water Supply

- ◦Oil & Gas

- ◦Chemical Processing

- ◦Construction

- ◦Power Generation

- •By End-Use Industry

- ◦Municipal Water Systems

- ◦Oil & Gas Industry

- ◦Chemical Manufacturing

- ◦Infrastructure & Construction

- •By Distribution Channel

- ◦Direct Sales

- ◦Distributors

- ◦Project-Based Tenders

Growth Dynamics

The global FRP GRP GRE pipe market growth is primarily driven by rising demand for corrosion-resistant and lightweight piping solutions across water supply and oil & gas sectors. Increasing infrastructure investments worldwide, particularly in Asia-Pacific and North America, stimulate adoption, as governments prioritize sustainable and durable materials. Additionally, technological advances in resin chemistry and manufacturing processes improve product performance and reduce costs, making composite pipes more competitive against traditional metals. Environmental regulations aimed at reducing pipeline failures and leaks further propel market expansion. The trend towards smart pipeline systems equipped with real-time monitoring capabilities enhances safety and operational efficiency, broadening the application scope. Strategic collaborations between manufacturers and end-users accelerate customized solutions development. Economic growth in emerging regions coupled with urbanization drives expanded use in construction and power generation, supporting robust market momentum through 2034.

Market Trends

A prominent trend in the FRP GRP GRE pipe market is the integration of digital sensor technology within pipelines to enable real-time condition monitoring and predictive maintenance, significantly reducing downtime and operational costs. Manufacturers are increasingly adopting advanced resin formulations that offer enhanced chemical resistance and higher temperature tolerance, catering to more demanding industrial applications. The shift towards sustainable manufacturing practices, including the use of recycled raw materials and eco-friendly resins, is gaining traction, aligning with global environmental goals. Modular pipe systems designed for ease of installation and maintenance are becoming popular in infrastructure projects. Additionally, market players are exploring hybrid composites combining different fiber reinforcements to optimize strength and flexibility. These trends collectively contribute to improved product lifecycles and broadened market applications.

Market Opportunities

Expanding urban water infrastructure in developing economies presents significant opportunities for FRP GRP GRE pipe manufacturers, driven by increasing demand for reliable and corrosion-resistant piping systems. The growing focus on offshore oil and gas exploration, particularly in Asia-Pacific and Latin America, offers lucrative growth avenues due to the pipes’ superior durability in harsh marine environments. Innovations in composite materials enabling higher pressure and temperature handling open new markets in chemical processing and power generation sectors. Moreover, retrofitting and replacement of aging metallic pipelines in mature markets like North America and Europe creates continuous demand for advanced composite pipes. Strategic partnerships and localized manufacturing can facilitate market penetration in unserved regions, enhancing growth potential. The development of customized pipe solutions for niche industrial applications remains an untapped area with high revenue prospects.

Market Challenges

High initial capital investment required for advanced manufacturing facilities and skilled workforce presents a significant barrier for new entrants and smaller players in the FRP GRP GRE pipe market. The technical complexity of composite pipe production necessitates strict quality control and certification adherence, which can delay product launches and increase costs. Market adoption is sometimes hindered by limited awareness among end-users about the long-term benefits and lifecycle cost advantages of composite pipes compared to traditional materials. Additionally, variability in regional regulatory standards complicates global market penetration and product standardization. The price sensitivity in emerging markets challenges manufacturers to balance cost and performance. Furthermore, supply chain disruptions for raw materials such as specialized resins and reinforcing fibers can impact production schedules and profitability. Addressing these challenges requires continuous innovation, education, and strategic supply chain management.

Regulatory Framework

- •Between 2020 and 2025, several key regulations have influenced the FRP GRP GRE pipe market globally, mandating stringent quality and safety standards for pipeline materials used in critical infrastructure. Notably, the American Society for Testing and Materials (ASTM) updated standards such as ASTM D2996 and D3262, specifying performance criteria for filament wound and centrifugally cast pipes. The European Committee for Standardization (CEN) implemented EN standards focusing on environmental impact and mechanical integrity, compelling manufacturers to enhance product durability and sustainability. In Asia-Pacific, countries like Japan and South Korea introduced national regulations promoting corrosion-resistant materials in water and oil pipelines, further supporting composite pipe adoption. Additionally, environmental agencies worldwide have enforced regulations limiting pipeline leakages and emissions, enhancing the demand for high-integrity piping systems. Governments have also introduced incentive programs encouraging infrastructure upgrades with advanced composite materials. These regulations collectively shape market compliance requirements, manufacturing practices, and product innovation, driving higher quality benchmarks and operational safety across regions.

- •Regulatory enforcement mechanisms include mandatory third-party certifications, routine pipeline inspections, and penalties for non-compliance, affecting manufacturers and end-users alike. Industry bodies collaborate with regulators to align standards and facilitate market acceptance. The regulatory landscape continues to evolve with increasing focus on sustainability, recyclability, and lifecycle assessment of composite pipes, prompting manufacturers to invest in eco-friendly technologies and transparent reporting. Regional differences in certification processes and material approvals require companies to adopt flexible strategies for product registration and market entry. The regulatory framework also addresses installation practices and jointing methods to ensure pipeline integrity, influencing supply chain and service provider capabilities. Overall, this evolving regulatory environment fosters innovation, market transparency, and end-user confidence, supporting the sustained growth of the FRP GRP GRE pipe market.

Market Intelligence

- •15th February 2025, Aegion Corporation announced the launch of its next-generation filament wound pipe series featuring enhanced epoxy resin systems that improve chemical resistance and mechanical strength for oil and gas applications. The new product line aims to reduce downtime and maintenance costs while extending service life under harsh environmental conditions. Designed for subsea and onshore pipelines, the pipes comply with updated ASTM standards and offer compatibility with smart monitoring sensors. This strategic product introduction positions Aegion as a leading innovator in composite piping solutions, targeting expanding offshore drilling markets in Asia-Pacific and Latin America. The company plans to increase production capacity at its Texas facility to meet anticipated demand growth. Source: Aegion Corporation Official Press Release

- •10th April 2024, Saint-Gobain PAM unveiled a modular GRP pipe system designed for rapid installation in municipal water projects. This system incorporates lightweight jointing technology and improved sealing mechanisms to minimize leakage and installation time. The innovation targets urban infrastructure upgrades across Europe and North America, aiming to support sustainability goals by reducing water loss and energy consumption. The company also announced partnerships with leading water utilities to pilot the system in smart city initiatives. This launch reflects a growing trend towards adaptable and eco-friendly composite piping solutions in public infrastructure. Source: Saint-Gobain PAM Corporate Website

- •5th June 2025, Johns Manville reported a strategic collaboration with a major chemical processing firm to develop customized GRE pipes capable of handling higher temperatures and aggressive chemicals. The joint development project focuses on resin optimization and enhanced fiber reinforcement to meet stringent industrial safety standards. This initiative is expected to open new market segments within the chemical manufacturing industry globally, especially in Asia-Pacific and Middle East & Africa regions. The partnership exemplifies the increasing focus on tailored composite solutions to address specific end-user requirements, driving product differentiation and competitive advantage. Source: Johns Manville Press Release

- •Recent market developments and strategic initiatives are continuously tracked through industry publications, company announcements, and regulatory filings. For the most current information, stakeholders are advised to monitor official corporate communications and recognized market intelligence platforms.

Regional Outlook

The North America currently holds a significant share of the market, primarily due to several key factors: increasing consumption rates, a burgeoning population, and robust economic momentum. These elements collectively drive demand, positioning this region as a leader in the market. On the other hand, Asia-Pacific is rapidly emerging as the fastest-growing area within the industry. This remarkable growth can be attributed to swift infrastructure development, the expansion of various industrial sectors, and a marked increase in consumer demand. These dynamics make this region a crucial player in shaping future market growth.

In our report, we cover a comprehensive analysis of the following regions and countries:

- North America

- LATAM

- West Europe

- Central & Eastern Europe

- Northern Europe

- Southern Europe

- East Asia

- Southeast Asia

- South Asia

- Central Asia

- Oceania

- MEA

| Feature | Details |

|---|---|

| Base Year Market Size | USD 12.4 Billion |

| Forecast Year Market Size | USD 28.9 Billion |

| CAGR | 9.2% |

| Forecast Period | 2026 to 2033 |

| YoY Growth | 9% |

| Scope of Report | Market is segmented by Product Type (Filament Wound Pipes, Centrifugally Cast Pipes, Pultruded Pipes, Molded Pipes, Hand Lay-Up Pipes), Application (Water Supply, Oil & Gas, Chemical Processing, Construction, Power Generation), End-Use Industry (Municipal Water Systems, Oil & Gas Industry, Chemical Manufacturing, Infrastructure & Construction), Distribution Channel (Direct Sales, Distributors, Project-Based Tenders) |

| Regions Covered | North America, LATAM, West Europe, Central & Eastern Europe, Northern Europe, Southern Europe, East Asia, Southeast Asia, South Asia, Central Asia, Oceania, MEA |

| Key Companies | Aegion Corporation (United States), Saint-Gobain PAM (France), Johns Manville (United States), Amiblu Holding GmbH (Austria), Jushi Group Co., Ltd. (China) |

Global FRP GRP GRE Pipe Market Size, Growth & Revenue 2025-2034 - Table of Contents

Frequently Asked Questions (FAQ):

The Compact Track Loaders market is expected to see value worth 5.3 Billion in 2025.

North America currently leads the market with approximately 45% market share, followed by Europe at 28% and Asia-Pacific at 22%. The remaining regions account for 5% of the global market.

Key growth drivers include increasing construction activities, rising demand for versatile equipment in agriculture, technological advancements in track loader design, and growing preference for compact equipment in urban construction projects.